The PFIC Tax Trap: Foreign ETFs That Cost Expats 37%+

10 min read · 2,472 words

Most US expats know they still owe the IRS a filing each April. What almost nobody warns them about is the secondary trap: the moment you open a local brokerage account or buy an ETF at a foreign bank, you may have just signed up for a tax rate that can exceed 50% on your investment gains — with interest charges that compound back to the year you bought the fund. The culprit is called a PFIC, and it’s arguably the most punishing provision in the entire US tax code for people living abroad.

The IRS doesn’t warn you. Your local bank definitely won’t. And the penalty kicks in automatically if you do nothing — which most expats do, because they have no idea the rule exists.

What Is a PFIC?

A Passive Foreign Investment Company (PFIC) is any foreign corporation where either:

- At least 75% of gross income is passive (dividends, interest, rents, capital gains), or

- At least 50% of assets produce or are held to produce passive income

In plain English: nearly every foreign-domiciled mutual fund, ETF, unit trust, or investment fund qualifies as a PFIC. That includes the funds sitting inside your German brokerage account, the UCITS ETFs a Singapore wealth manager recommended, and the local investment trust your Colombian banker suggested as a “safe” option.

Congress created PFIC rules in 1986 specifically to prevent Americans from deferring US taxes by parking money in foreign funds. The rules are designed to be punishing. They are not incidental collateral damage — they are the point.

How Expats Stumble In Without Knowing It

Here’s the scenario that plays out constantly: an American moves to Amsterdam, opens a brokerage with ING or Degiro, and buys the Vanguard FTSE All-World UCITS ETF because it tracks the same index as their old Vanguard account back home. The ISIN starts with “IE” — it’s Ireland-domiciled. It looks and acts exactly like an ETF. But for US tax purposes, it’s a PFIC, and they just started the clock on a potentially massive tax liability.

The same problem occurs with:

- Any UCITS fund (Europe’s equivalent of a US mutual fund)

- Funds with ISINs beginning with IE (Ireland), LU (Luxembourg), GB (United Kingdom), or FR (France)

- The local “pension fund” a Thai or Mexican bank auto-enrolled you in

- A Canadian mutual fund bought before you moved south

- Even some foreign-held life insurance policies with investment components

Note that FEIE doesn’t help here. The Foreign Earned Income Exclusion shields earned income from US tax, but PFIC gains are investment income — completely outside FEIE’s scope. The IRS still wants its cut, and then some. For context on how FEIE works and what it actually covers, see the FEIE full guide.

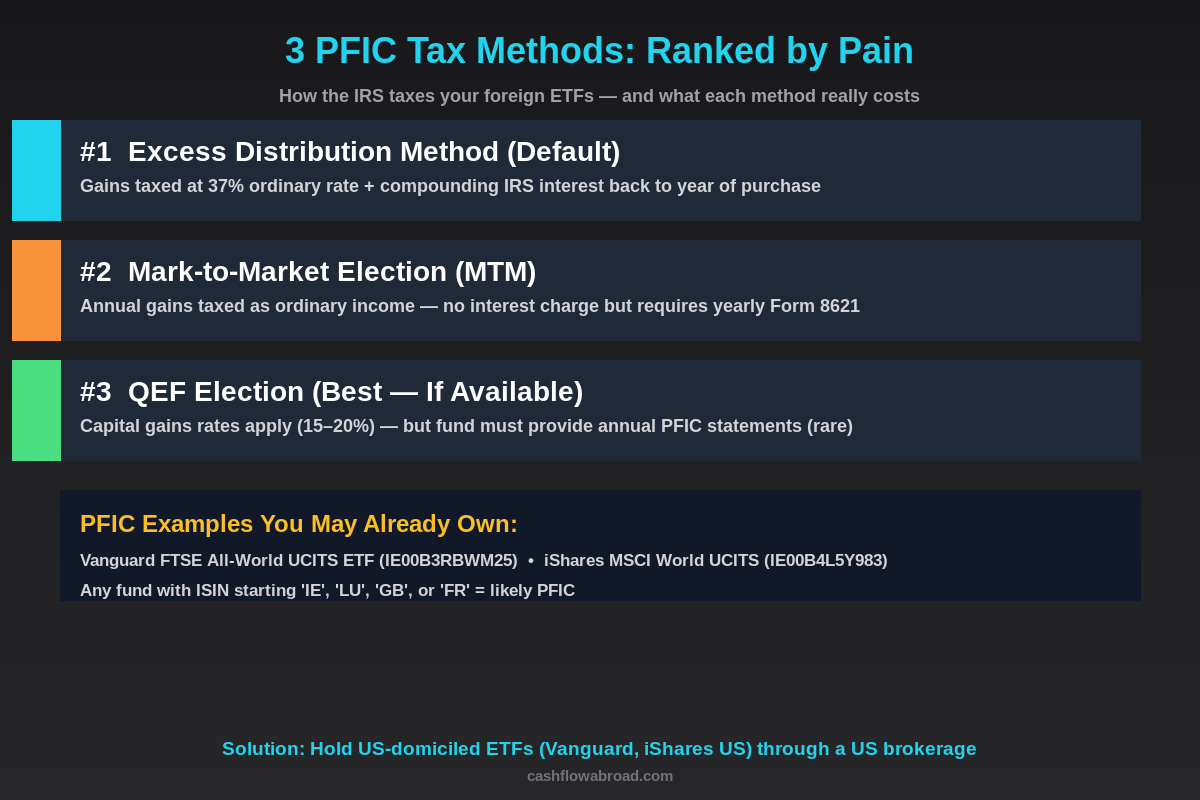

The 3 PFIC Tax Methods — And Their Real Costs

The IRS gives you three ways to handle PFIC taxation. The default is the worst. The best option usually isn’t available. Here’s what each method actually means for your wallet:

Method 1: Excess Distribution (The Default Trap)

If you file nothing and make no elections, the IRS applies the Excess Distribution method automatically. Under this approach:

- Any gain from selling the PFIC — or any distribution that exceeds 125% of the prior three-year average — is an “excess distribution”

- The gain gets spread ratably across every year you held the fund

- Each year’s share is taxed at the highest ordinary income tax rate for that year (currently 37%)

- An interest charge is added to account for deferred taxes — using the IRS underpayment rate (currently 8%), compounded annually from the midpoint of each prior year

The interest charge is what turns a painful tax rate into a potentially catastrophic one. Hold a PFIC for 10 years with modest gains, and the interest charge alone can push your effective rate above 50%. The IRS isn’t taxing your profit — it’s taxing the entire value of the deferral benefit you theoretically received by not paying US taxes each year.

And the clock keeps running as long as you don’t file. The statute of limitations on a tax return with an unfiled Form 8621 never starts running. The IRS can assess the tax, penalties, and interest years after the fact — with no time limit.

Method 2: Mark-to-Market Election

With a Mark-to-Market (MTM) election, you elect to report annual unrealized gains and losses as ordinary income each year. No deferred gains, no interest charge — you pay as you go.

The downside: all gains are taxed as ordinary income (up to 37%), not at preferential long-term capital gains rates (15–20%). You’re also paying tax on paper gains — positions you haven’t sold. And you must file Form 8621 annually even in years with no transactions. Losses in a down year give you a deduction, but only up to the amount of MTM income you previously recognized from that PFIC.

MTM is available for any “marketable” PFIC — one that trades on an established securities market. For listed ETFs and funds, this is usually an option. It’s the most commonly used election because it eliminates the catastrophic interest charge, even though the ordinary income rate stings.

Method 3: QEF Election (The Good One — Almost Never Available)

The Qualified Electing Fund (QEF) election is the only method that preserves preferential capital gains tax rates (15–20% for most expats). Under QEF, you include your share of the fund’s ordinary income and net capital gain annually — but long-term gains stay long-term gains, taxed at the lower capital gains rate.

There’s a critical catch: the foreign fund must provide you with an annual PFIC information statement certifying its income and gain breakdown. Almost no foreign funds do this, because it requires them to comply with IRS accounting rules designed for US entities. The QEF election is theoretically beautiful and practically useless for most expats — and you must make the election in the first year you own the PFIC. Miss that window and you’re locked out.

| Method | Tax Rate | Interest Charge? | Annual Filing? | Availability |

|---|---|---|---|---|

| Excess Distribution (default) | Up to 37% + interest | Yes — compounding back to year 1 | On sale/distribution only | Always (default) |

| Mark-to-Market (MTM) | Up to 37% ordinary | No | Yes, every year | Marketable PFICs only |

| QEF Election | 15–20% capital gains | No | Yes, every year | Rare — fund must provide PFIC statements |

A Real Numbers Example: The $13,000 Surprise

Here’s a concrete scenario. An American expat living in Dublin buys €30,000 (~$32,000) worth of the iShares Core MSCI World UCITS ETF (ISIN: IE00B4L5Y983) in 2020 and sells in 2026 for €50,000 (~$55,000). The gain is roughly $23,000.

Under US capital gains rules on a US-domiciled fund, that $23,000 held over 5 years would face a long-term capital gains rate of 15% for most earners — or about $3,450 in tax.

Under the PFIC Excess Distribution method with no election made:

- $23,000 gain spread equally over 6 years = ~$3,833 allocated per year

- Each year’s share taxed at 37% ordinary rate = ~$1,418 in base tax per year

- Interest charges added on prior years’ deferred tax — compounding at the IRS underpayment rate (~8%) from mid-year of each holding year

- Total estimated tax + interest: $11,000–$13,000

Same investment. Same gain. Four times the tax bill — simply because of where the fund was domiciled. And because no Form 8621 was filed, the statute of limitations never runs. The IRS could show up in 2030 and add another two years of compounded interest.

How to Tell If You Own a PFIC

The quickest check is the fund’s ISIN (International Securities Identification Number), usually printed on your brokerage statement or fund factsheet. The first two letters are the country of domicile:

| ISIN Prefix | Country of Domicile | PFIC Status |

|---|---|---|

| IE | Ireland | Almost certainly PFIC |

| LU | Luxembourg | Almost certainly PFIC |

| GB | United Kingdom | Likely PFIC |

| FR | France | Likely PFIC |

| US | United States | Not a PFIC — safe for US persons |

| CA | Canada | Likely PFIC — check each fund |

Common PFICs that expats routinely buy thinking they’re “normal” ETFs:

- Vanguard FTSE All-World UCITS ETF — ISIN IE00B3RBWM25

- iShares Core MSCI World UCITS ETF — ISIN IE00B4L5Y983

- Xtrackers MSCI World Swap UCITS ETF — ISIN LU0274208692

- Any fund with “UCITS” in its name — European regulatory wrapper = PFIC by definition

The Fix: How to Invest Globally Without the PFIC Problem

The solution is straightforward — but it requires acting before you buy, not after.

Keep a US-Domiciled Brokerage Account

The cleanest solution for most US expats is to maintain a US-domiciled brokerage account and buy US-domiciled ETFs (ISIN starting with “US”). Vanguard VT, iShares ACWI, Schwab’s international index funds — these all give you global diversification without touching PFIC rules.

The challenge: many major US brokerages have increasingly restricted accounts for customers with foreign addresses. The exceptions matter here. Charles Schwab International is the gold standard for expat investors — it actively services international clients, offers a debit card with fee-free ATM withdrawals worldwide, holds US-domiciled securities with no PFIC exposure, and supports IRAs for expats who have earned income. Opening or maintaining a Schwab account before you move abroad is one of the most important financial moves you can make.

For active traders who want options and futures on US-listed securities, tastytrade services international accounts in many countries and keeps you entirely within the US-domiciled, non-PFIC ecosystem.

Never Buy What Your Foreign Banker Recommends for Investment

Bank advisors in Europe, Asia, and Latin America are licensed to sell locally-domiciled products. A Singapore wealth manager recommending a UCITS fund is doing their job — and inadvertently creating a US tax nightmare for you. Unless you’ve confirmed the ISIN starts with “US,” assume every investment a foreign banker recommends is a PFIC. Use foreign banks for daily spending and transfers; never let them manage your investment portfolio.

Maintain a US Mailing Address

Most US brokerages require a US address on file to keep your account open. Once they detect a foreign address, account restrictions often follow. A virtual mailbox with a real US street address solves this. Traveling Mailbox provides a legitimate US street address in 50+ cities, mail scanning on demand, and check deposit capability for about $15/month. It’s the operational backbone that keeps Schwab open and your US financial life intact while you live abroad. We covered the full setup in the virtual mailbox guide for expats.

A Note on Foreign Crypto Exchanges

Crypto itself (Bitcoin, Ethereum) held directly on an exchange is property, not a PFIC — it’s taxed under a separate set of rules. But some crypto “yield” products and foreign-domiciled crypto funds may qualify as PFICs. If you’re trading crypto abroad, track everything carefully with a dedicated tool like CoinTracking, which handles international tax reporting and helps identify PFIC-adjacent exposure. See the full breakdown in the crypto taxes for US expats guide.

Already Own PFICs? Here’s What To Do

If you’ve been holding foreign funds without making any elections, you have options — but time is not on your side.

Option 1: Make a MTM election going forward. You can elect mark-to-market for the current tax year and stop the interest-charge clock from accumulating further. The catch: you’ll owe a “deemed disposition” tax on any accumulated gain as if you sold and repurchased at year-end, calculated at ordinary income rates. Painful, but it stops the compounding.

Option 2: Sell and move on. Dispose of the PFIC positions, report the gain as an excess distribution (accepting the full tax hit on this year’s return), and reinvest in US-domiciled equivalents. If your holding period is short, the interest charge is small. The longer you wait, the worse the math gets.

Option 3: IRS streamlined disclosure. If you’ve held PFICs for years without reporting Form 8621, you may have unfiled forms and potentially unreported assets. The IRS Streamlined Foreign Offshore Procedures (SFOP) allow qualifying expats to file 3 years of amended returns, 6 years of FBARs, and pay zero penalties — a lifeline for those who genuinely didn’t know these rules existed. This is a situation that warrants professional help; the savings from proper disclosure almost always exceed the cost of a qualified expat tax attorney.

The Form 8621 Burden: Annual Compliance That Adds Up

Every PFIC you own requires a separate Form 8621 filed with your annual tax return. There is no de minimis threshold — own one share of a foreign ETF, file the form. Own five different UCITS ETFs, file five forms.

Form 8621 is among the most technically complex forms in the US tax code. The IRS estimates a median of 16 hours per form to complete correctly — and that’s for someone who knows what they’re doing. Most CPA firms charge $500–$1,500 per PFIC per year for the reporting work, which means the annual compliance cost alone can make small foreign fund positions economically irrational. A $5,000 UCITS ETF position charging $700/year in accounting fees has already lost its entire projected return on tax preparation costs within a decade — before the actual tax bill.

The form must be filed if you receive distributions from a PFIC, dispose of PFIC shares, or make any elections. Miss the filing? The statute of limitations on your entire tax return remains open — not just the PFIC items. The IRS can audit anything on that return, years later, because of one unreported foreign fund.

For the broader picture on expat compliance obligations — FBARs, FATCA Form 8938, FBAR thresholds, and how these interact with FEIE — the complete US expat banking and tax guide covers the full framework.

A Special Note for Expat Business Owners

The PFIC rules have a cousin that catches expat business owners off guard: the Controlled Foreign Corporation (CFC) rules. If you own 10% or more of a foreign company (including your own foreign LLC or corporation), Subpart F rules may force you to include passive income from that entity on your US return — regardless of whether it was distributed. The interaction between CFC rules, PFIC classification, and GILTI tax creates one of the most complex areas of US international tax law. If you run a business abroad, get this reviewed by a specialist. The guide to running a US business while living abroad is a good starting point.

The Bottom Line

The PFIC rules are one of the most underappreciated financial risks facing American expats. You can do everything else right — claim FEIE, file FBARs, comply with FATCA — and still get blindsided by a 37%-plus tax rate plus compounding interest on investment gains, simply because your ETF was domiciled in Dublin instead of Delaware.

The solution isn’t complicated: invest through US-domiciled platforms using US-domiciled funds, keep your Schwab account active, and never let a foreign bank manage your investment portfolio. If you’ve already got PFICs, don’t wait — the interest charges compound every year you delay, and the IRS voluntary disclosure window is far more forgiving than a full audit.

The PFIC trap exists because Congress designed it to exist. The only way to win is to not play.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax or legal advice. PFIC rules are complex and fact-specific — consult a qualified US expat tax professional (CPA or tax attorney) before making any investment or filing decisions. Tax laws change; verify current rates and requirements with IRS.gov or a licensed advisor. Nothing in this article constitutes a recommendation to buy or sell any security.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.