Why Fidelity and Vanguard Close Expat Accounts (And What to Use)

In 2025, a reported 340,000 US brokerage accounts belonging to American expats were closed — not because of fraud, unpaid taxes, or any wrongdoing.

In 2025, a reported 340,000 US brokerage accounts belonging to American expats were closed — not because of fraud, unpaid taxes, or any wrongdoing.

In 2025, a reported 340,000 US brokerage accounts belonging to American expats were closed — not because of fraud, unpaid taxes, or any wrongdoing. The owners simply lived outside the United States. One day their portfolio was accessible; the next they received a letter giving them 30 to 60 days to transfer assets or watch positions get liquidated.

This is not a fringe problem. With roughly 9 million US citizens living abroad, the odds are high that if you move overseas without restructuring your finances first, you will come home — metaphorically — to find the locks changed on your investment accounts. Fidelity, Vanguard, Merrill Lynch, USAA, TIAA, Edward Jones, Ameriprise, Morgan Stanley, and UBS have all taken action against expat account holders in recent years. The wave is accelerating, not slowing down.

Here's everything you need to know about why this happens and, more importantly, how to stay fully invested as an American abroad.

Why US Brokerages Are Closing Expat Accounts

The short answer is FATCA — the Foreign Account Tax Compliance Act passed in 2010. FATCA was designed to force foreign banks to report US account holders to the IRS or face 30% withholding penalties on US-sourced payments. It worked, kind of. Foreign banks complied, but many found it easier to simply close all American accounts than deal with the reporting burden. The result: tens of thousands of expats found themselves unbanked abroad.

Now the blowback is running in the other direction. US brokerages — particularly those serving clients in countries with strict local regulations like the EU's MiFID II — face a maze of cross-border compliance requirements. Serving a client in Germany, France, or Japan means navigating local securities law on top of US law. The compliance cost doesn't scale for retail accounts.

So brokerages take the path of least resistance: restrict foreign-addressed accounts, block mutual fund purchases, and eventually close accounts entirely. The regulatory calculus is blunt — compliance risk from one expat holding a $50,000 IRA in France isn't worth the legal exposure.

What changed recently is enforcement. For years, many expats flew under the radar by keeping a US address on file — a parent's house, a friend's place. That worked until it didn't. Vanguard's 2025 platform migration to a new brokerage system triggered automatic Know Your Customer (KYC) reviews on every migrating account. The new system flagged foreign IP addresses and phone numbers in real time. Expats who simply logged in from abroad to check their balance suddenly faced account restrictions. Many never got their accounts migrated at all.

Which Institutions Will and Won't Serve Expats

The landscape is uneven, and official "policy" often differs from actual enforcement. Here's the current state based on what expat communities and financial advisors are reporting:

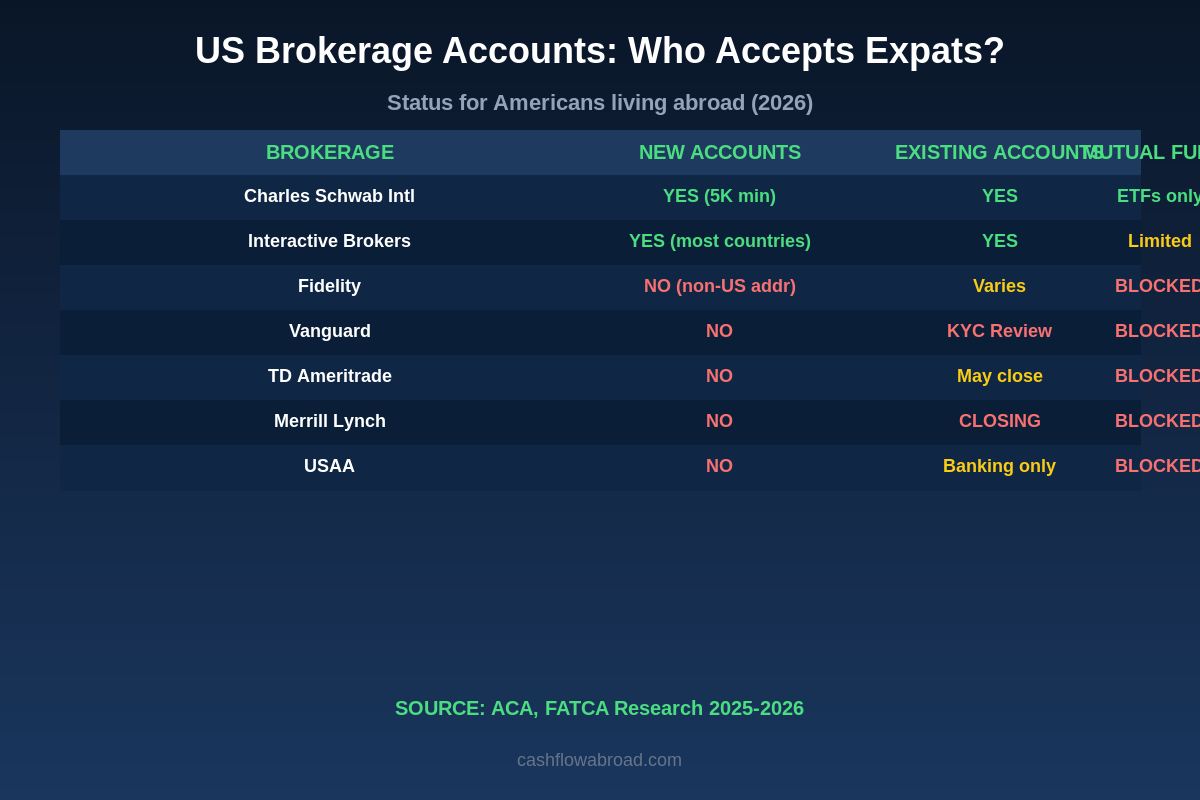

| Institution | New Accounts (Foreign Address) | Existing Accounts | Mutual Funds | Notes |

|---|---|---|---|---|

| Charles Schwab International | Yes ($25K minimum) | Yes | ETFs only | Purpose-built expat division |

| Interactive Brokers | Yes (most countries) | Yes | Limited | Country-by-country restrictions |

| Fidelity | No | May close or restrict | Blocked for foreign addresses | Enforcement varies by country |

| Vanguard | No | KYC review flagged expats in migration | Blocked | 2025 platform move triggered closures |

| Merrill Lynch | No | Actively closing foreign-address accounts | Blocked | EU/UK expats especially affected |

| USAA | No (brokerage) | Banking often maintained; brokerage restricted | Blocked | Military members may get exceptions |

| TD Ameritrade (now Schwab) | No | Migrated accounts under Schwab policy | Blocked | Policy convergence with Schwab underway |

| tastytrade | Limited | Selective | N/A | Options/futures focus; country-dependent |

The "varies by enforcement" caveat matters. Some expats have held Fidelity accounts for years by maintaining a US address and never triggering a review. But that's not a strategy — it's hoping nobody looks. When they do look, accounts get restricted fast.

What Actually Triggers an Account Closure

Brokerages don't randomly audit clients. Something trips the wire. Common triggers:

- Updating your address to a foreign address. The most common trigger by far. Never update your custodian address to a foreign one unless the custodian explicitly supports expat clients.

- Foreign IP address logins. Vanguard's new system and others flag logins from restricted countries. Even checking your balance from an airport abroad can create a flag.

- Foreign phone number on 2FA. If your verification code goes to a +52 or +57 number, that's visible to compliance systems.

- Foreign bank linked for ACH transfers. Connecting a Colombian or Thai bank account as a funding source is a dead giveaway.

- Frequent outbound wires to foreign banks. Pattern analysis on international wire transfers can trigger compliance review.

- FATCA cross-referencing. If your foreign bank reports your US citizenship to the IRS under FATCA, cross-referencing with existing US accounts can flag dormant positions.

Once flagged, most brokerages send a letter requesting documentation. If you can't produce a valid US residential street address — not a P.O. box — the clock starts on your account.

The Virtual Mailbox Fix That Actually Works

A US street address is the single most important piece of infrastructure for an American expat. Not just for brokerage accounts — for IRS correspondence, state domicile establishment, driver's license renewal, and dozens of other things that assume you have a US "residence."

I use Traveling Mailbox, which gives you a real street address in 50+ US cities — not a P.O. box number that flags instantly as mail forwarding. Mail gets scanned and available in a secure portal within hours. They deposit checks, forward physical mail, and shred junk. At $15/month it's the cheapest piece of expat financial infrastructure you'll ever buy. For a complete breakdown on how virtual mailboxes protect your banking and investment accounts, see the full virtual mailbox guide.

The key: use a state with no income tax as your domicile address. Texas, Florida, Nevada, Wyoming, and South Dakota are the standard choices. This matters because some states — California, New York, Virginia, New Jersey — continue taxing you as a resident even after you move abroad if they believe you maintain domicile ties there.

The State Tax Problem That Hits Right After the Brokerage Problem

While you're fixing your brokerage situation, there's a parallel threat most expats miss: state income tax that follows you overseas. The federal government lets you exclude up to $130,000 in foreign earned income via the FEIE. California doesn't care. California does not recognize the federal FEIE — if the state still considers you a resident, you owe California income tax up to 14.4% (including surcharges) on your entire foreign salary, even if the IRS taxes you nothing on it.

New York employs over 300 dedicated residency auditors whose entire job is proving that people who claim to have left still "domicile" there. They will pursue you based on where your spouse lives, where your kids attend school, where your primary doctor is, and where your "near and dear" possessions — jewelry, family heirlooms, original artwork — are kept.

California's Franchise Tax Board uses a comprehensive "close connection" test examining your driver's license, voter registration, bank accounts, property ownership, and professional memberships. In serious audits, they will subpoena credit card statements and cell phone location records to demonstrate physical presence during the year in question.

The fix: before moving abroad, formally establish domicile in a no-income-tax state. Close California or New York bank accounts, surrender your driver's license, cancel your voter registration, remove your name from any real property. Then maintain your new domicile address consistently across all financial accounts. For the full breakdown of how this interacts with FBAR and FATCA, see our complete US expat banking and tax guide.

Charles Schwab International: The Clearest Expat Solution

Schwab built a specific international division for this exact problem. The Schwab One International Account lets Americans abroad invest in US stocks, ETFs, and bonds with no commission on online equity trades. You get worldwide ATM fee reimbursement through Schwab Bank — which matters when you're withdrawing local currency in a different country every month.

The catch: $25,000 minimum deposit to open. Not a starter account for someone leaving the US with $8,000 in savings. For those who don't meet the minimum yet, Interactive Brokers is the main alternative — no minimum for cash accounts, accepts residents of most countries, and handles options and international securities across 150 markets.

What Schwab International supports:

- US stocks, ETFs, options, and bonds with no commission on equity trades

- IRAs (traditional and Roth) — critical for expat retirement planning

- International wire transfers with competitive exchange rates and no transaction fees

- A dedicated expat service team familiar with FBAR and FATCA reporting requirements

What Schwab International does not support: US-domiciled mutual funds. You'll hold ETFs — which is fine for most investors. VTI tracks the same index as VTSAX. VXUS covers the same international exposure as VTIAX. The fund structure changes; the underlying exposure doesn't.

What About IRAs and 401(k)s?

IRAs are more complicated than taxable brokerage accounts. Most IRA custodians will continue holding an existing IRA even for expats, but won't allow new contributions without a US address. Some close them outright.

The bigger issue: if you're using the FEIE, your foreign earned income doesn't count as "earned income" for IRA contribution purposes. You can only contribute to a Roth or traditional IRA if you have US-sourced income or income not excluded by the FEIE. This is the FEIE-IRA trap — you zero out your federal tax liability, then realize you've also frozen your ability to fund retirement accounts for the year.

For 401(k)s: if you leave a US employer, roll the 401(k) into an IRA at Schwab International before you lose your US address on record at that custodian. Once you update to a foreign address at most institutions, rollovers become complicated or impossible. Timing this correctly is one of the highest-leverage moves in the entire expat financial setup.

Interactive Brokers: The Backup Option

Interactive Brokers (IBKR) accepts clients from nearly every country in the world, has no minimum deposit for standard cash accounts, and handles stocks, ETFs, options, futures, forex, and international securities across 150 markets. The platform was built for active traders and shows it — the interface is complex compared to Schwab's cleaner layout — but it handles everything Schwab International doesn't.

For expats who are active traders, tastytrade is worth considering for options strategies, though country availability is more restricted than IBKR. If you're a passive index investor, Schwab International is the cleaner choice. If you trade actively or need access to international securities, IBKR has no real competition among platforms accessible to expats.

The Pre-Departure Checklist

The window to act is before you leave. Once you update any financial account to a foreign address, the compliance machinery starts moving and it's difficult to reverse. Do these steps in order:

- Open Schwab International or IBKR while you still have a US address. This is step one, not an afterthought. You need the account established and funded before anything triggers a KYC flag.

- Set up a virtual US mailbox in a no-income-tax state. Texas (Houston, Austin, Dallas) and Florida (Miami, Tampa) are the most practical. Use this address across all financial accounts going forward. Traveling Mailbox has real street addresses in both states for $15/month.

- Transfer existing brokerage accounts to the expat-friendly custodian via ACAT. Initiate the transfer from the receiving side — Schwab handles the mechanics. Do this before departure.

- Roll any orphaned 401(k) into an IRA at Schwab. Don't leave retirement assets at a custodian that may restrict access once your address situation changes.

- Switch all positions from mutual funds to equivalent ETFs. ETFs trade on exchanges and are universally accessible. Mutual funds get blocked first at almost every institution. VTI replaces VTSAX. VXUS replaces VTIAX. Do this swap before the transfer.

- Use a US IP address when accessing legacy accounts. A NordVPN US server prevents accidental IP-flag triggers at custodians that haven't confirmed expat support.

- Set automatic dividend reinvestment only on ETF positions. Reinvestment on mutual funds at restricted brokerages can be blocked mid-execution, creating fractional positions that then trigger compliance review.

Crypto, Stablecoins, and Alternatives Abroad

If you hold crypto, account closure doesn't apply the same way — you control the wallet. But US tax reporting still does. As a US citizen abroad, capital gains tax applies to every crypto disposal regardless of where you live. See the full crypto tax guide for US expats for what the IRS actually requires.

For expats in Latin America, ARQ Finance fills a different gap: dollar-based financial services with local currency access. Hold USDC/EURc balances, earn up to 4% on dollar holdings, swap to MXN, COP, ARS, or BRL at live rates, and invest in US stocks and ETFs — all in one platform. Available in Mexico, Colombia, Argentina, and Brazil. It's not a replacement for a US brokerage, but it handles the local-currency problem that Schwab and IBKR don't. (ARQ is not an investment advisor.)

For tracking portfolio performance and crypto gains across Schwab, IBKR, and any crypto wallets, CoinTracking generates IRS-compliant Form 8949 and the data you need for FBAR reporting — consolidating everything that would otherwise take hours to compile from separate platforms.

Banking for Business Expats: Mercury + Schwab

Brokerage accounts and business bank accounts are separate problems with an overlapping solution. If you run a US LLC or S-Corp from abroad, Mercury is the standard recommendation for business banking — online-only, no monthly fees, no minimum balances, fully remote account opening. It doesn't care that you're physically in Southeast Asia or South America.

Personal banking is covered by Schwab Bank's debit card, which reimburses all worldwide ATM fees with no foreign transaction charges. Together — Mercury for business, Schwab for personal — this is the zero-fee expat banking stack that actually holds up across borders. For a deeper breakdown on building this infrastructure from scratch, see the guide on the zero-fee expat banking stack.

The Bottom Line

The brokerage account closure problem is completely solvable — but only if you solve it before you board the plane. The expats who lose accounts are overwhelmingly the ones who moved abroad, updated their address somewhere, and discovered the restriction weeks later when they tried to log in. The ones who don't lose accounts opened expat-ready custodians first, used virtual US mailboxes for address consistency, switched from mutual funds to ETFs, and treated financial infrastructure like the logistics problem it actually is.

The sequence: Schwab International or IBKR, Traveling Mailbox in Texas or Florida, ETFs not mutual funds, no foreign IP logins to legacy accounts. That's the whole playbook. Nine million Americans live abroad. The US financial system wasn't built for them — but the workarounds exist, and they work, if you use them in the right order.

Financial Disclaimer: This post is for informational purposes only and does not constitute financial, legal, or tax advice. Brokerage policies change frequently — verify current account acceptance directly with any institution before transferring assets. Tax situations vary; consult a qualified expat CPA before making decisions about state domicile, IRA contributions, or FEIE elections. Some links in this post are affiliate links; we may receive compensation at no additional cost to you.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Investing & Wealth BuildingJuly 3, 2026

Investing & Wealth BuildingJuly 3, 2026

REITs for US Expats: Income, Tax Rules, and PFIC Traps

US expats can earn 4%+ REIT yields at a 29.6% effective rate with the permanent Section 199A deduction. Know which funds are PFICs and which are not.

Investing & Wealth BuildingJune 26, 2026

Investing & Wealth BuildingJune 26, 2026

Options Trading for US Expats: Tax Rules and Traps

Section 1256 contracts cap US expat options traders at a 26.8% blended rate. Understand wash sales, NIIT traps, mark-to-market, and Form 6781 rules.

Investing & Wealth BuildingJune 24, 2026

Investing & Wealth BuildingJune 24, 2026

W-8BEN: How Expats Cut US Withholding on Dividends

Nonresident aliens can halve 30% US dividend withholding with Form W-8BEN. See treaty rates by country, the portfolio interest exemption, and REIT