How Expats Beat Hyperinflation With Dollar Stablecoins

In 2023, Argentine residents watched 211% of their purchasing power evaporate in a single year. Turkish savers lost more than 60% of their lira's value.

In 2023, Argentine residents watched 211% of their purchasing power evaporate in a single year. Turkish savers lost more than 60% of their lira's value.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

In 2023, Argentine residents watched 211% of their purchasing power evaporate in a single year. Turkish savers lost more than 60% of their lira's value. Nigerians saw their naira shed 40% against the dollar in twelve months. If you were an expat holding savings in any of these currencies, you didn't just lose money — you got financially obliterated.

Here's the counterintuitive part: the expats who came out ahead weren't the ones with the savviest stock portfolios or the most aggressive real estate strategies. They were the ones who figured out how to park their money in dollar-pegged stablecoins — digital dollars that sit on a blockchain but behave exactly like the greenback — while everyone around them watched their savings melt.

And they did it while earning yield. Not the 2.5% you'd get from a US high-yield savings account, but anywhere from 4% to 18% annually on those same dollar-pegged assets. While local currencies burned, these expats were quietly compounding.

Related: crypto tax guide for expats

This is the expat stablecoin playbook. It's not theoretical. It's what millions of people in Argentina, Turkey, Nigeria, Egypt, and Colombia are doing right now — and it's what savvy expats living in those countries have been doing for years.

The Scale of the Problem: What Inflation Actually Does to Your Savings

Most people in stable economies understand inflation intellectually but have never truly felt it. Let's make it concrete.

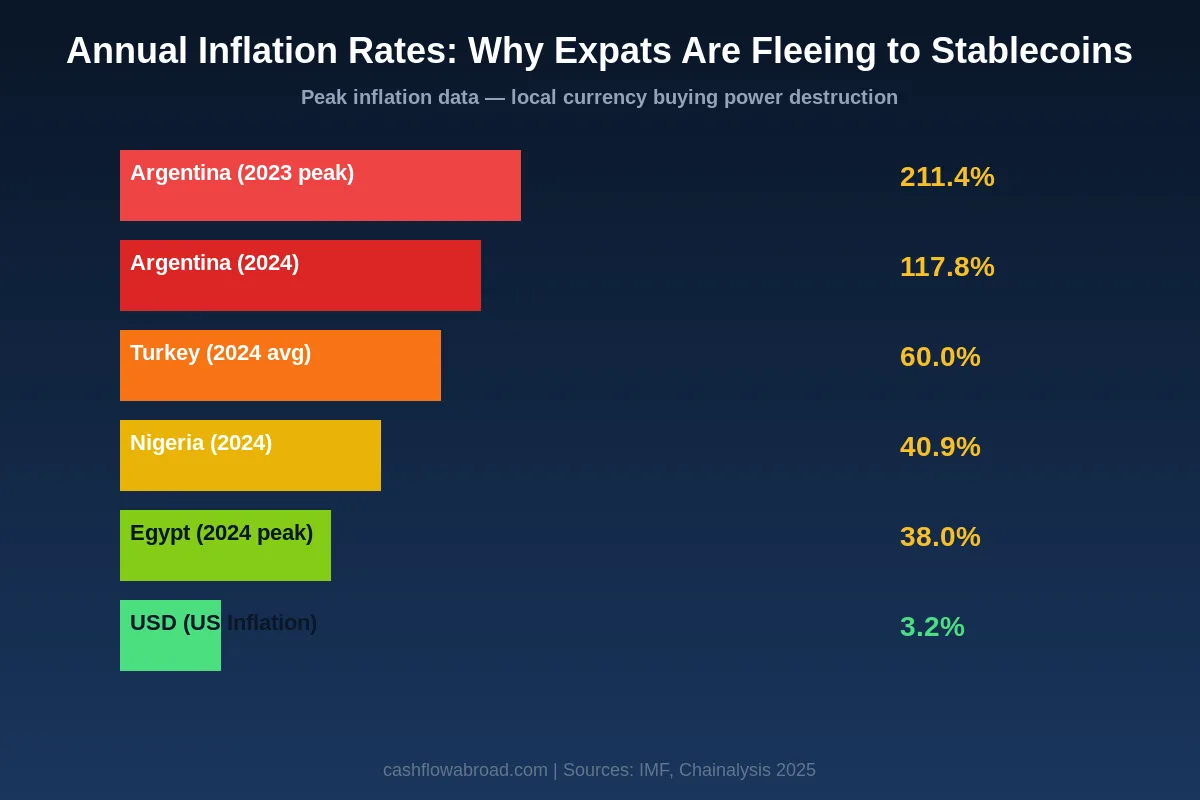

If you had $10,000 worth of Argentine pesos at the start of 2023 and left them in a savings account through year-end, you had the equivalent of roughly $2,600 left by December. Not because of bad investments. Because the currency itself collapsed. Argentina posted 211.4% annual inflation in 2023 — the highest since the hyperinflationary crises of the 1980s.

It didn't stop there. In 2024, annual inflation "cooled" to 117.8%. Still an absolute disaster. Still wealth destruction on a massive scale.

Turkey ran 60% average inflation through 2024, with the lira losing more than 450% of its purchasing power between 2020 and 2024. Nigeria's naira dropped 40%+ in 2024 alone. Egypt devalued its pound by over 35% in a single day in March 2024 — the third currency flotation in two years.

These aren't fringe cases. These are countries where millions of expats live and where many more digital nomads and retirees are considering relocating for cost-of-living advantages. The geographic arbitrage play is real — but only if you protect your savings from currency debasement while you're enjoying the lower costs.

The solution that's emerged organically — from the ground up, driven by ordinary people rather than financial institutions — is stablecoins.

What Stablecoins Actually Are (And Why They're Different)

A stablecoin is a cryptocurrency designed to maintain a fixed value relative to a reference asset — almost always the US dollar. The two dominant ones are USDT (Tether) and USDC (Circle). One USDC is always worth one dollar. One USDT is always worth one dollar.

They're not like Bitcoin, which swings 30% in a week. They're not like ETH or Solana. They're digital dollars — designed to stay at $1.00.

How do they maintain the peg? USDC, issued by Circle, is backed 1:1 by actual US dollars and short-term US Treasury bills held in regulated financial institutions. As of 2025, the total stablecoin market cap sits at $308 billion — up 50% year-over-year — and on-chain stablecoin transaction volume hit $33.4 trillion in 2025, up 74% from the prior year.

USDC leads on-chain transactions with a 54.8% market share. These aren't speculative assets. They're utility infrastructure.

For an expat in Buenos Aires, Istanbul, Lagos, or Cairo, holding USDC is functionally equivalent to holding US dollars — with one critical advantage: you don't need a US bank account or a US address to do it.

How Locals (and Expats) Are Using Stablecoins Country by Country

Argentina: The Most Advanced Use Case in the World

Argentina isn't just one of many countries adopting stablecoins — it's the global laboratory for what happens when currency collapses and stablecoins fill the void.

Stablecoins make up 61.8% of all crypto transactions in Argentina, compared to a global average of 44.7%. Argentinians transferred $91.1 billion in crypto between July 2023 and June 2024, surpassing Brazil's $90.3 billion in a country with a fraction of Brazil's population.

On Bitso, one of the leading Latin American exchanges, USDT represents 50% of all crypto purchases in Argentina. USDC accounts for another 22%. Bitcoin? Just 8%. This is not a country using crypto to speculate on digital gold — it's a country using stablecoins as a practical substitute for a currency that failed them.

Binance reported a 150% spike in USDT trading volume in Argentina in 2024. Over 100 businesses in Buenos Aires now accept stablecoin payments. The province of Mendoza accepts stablecoin payments for taxes. This is mainstream adoption driven by necessity.

For expats living in Argentina, the math is simple: earn in dollars (or convert to USDC immediately upon receipt), spend in pesos at the blue-chip dollar rate, and watch your real purchasing power stay intact while your peso-holding neighbors lose ground every month.

Related: zero-fee banking stack

For context on what life actually costs in Argentina and why the geographic arbitrage play still makes sense despite the volatility, see this cost-of-living comparison for LATAM — a similar dollar-stretching dynamic plays out across the region.

Turkey: The $22 Billion USDT Market

Turkey's crypto market is dominated by one overwhelming reality: USDT-TRY is the single largest trading pair on Binance Turkey, with over $22 billion in 2024 volume — more than five times the next largest pair.

USDT's share of quoted trading pairs on Turkish exchanges rose from approximately 20% in 2021 to over 50% by mid-2024. More than half of Turkey's population has invested in crypto. Half of all Bitcoin trades on Turkey's largest exchange are paired with USDT, not the lira.

With 2024 average inflation at 60% and the lira having lost more than 450% of its purchasing power between 2020 and 2024, Turkish savers aren't speculating — they're defending. For expats living in Istanbul or Izmir, the stablecoin stack isn't a sophisticated financial maneuver. It's basic wealth preservation.

Nigeria and Africa: Mobile-First Stablecoin Adoption

Nigeria processed nearly $22 billion in stablecoin transactions between July 2023 and June 2024. The naira's depreciation from roughly 460 to 1,500 per US dollar between 2023 and early 2025 represents a 60%+ loss in value — and that's the official rate.

USDT on the Tron network (TRC-20) dominates because transaction fees run under $1, often just cents. In a country where average monthly incomes can be $200–$400, Ethereum gas fees were prohibitive. Tron solved that. Nigeria ranked #6 globally in grassroots cryptocurrency adoption in 2025.

Colombia and Latin America: $1.5 Trillion in Annual Volume

Latin America as a whole processed $1.5 trillion in crypto volume (Chainalysis 2025), with USDT and USDC representing more than 90% of transfer volume on exchanges. Stablecoin flows through Latin American exchanges grew 800% from 2021 to 2024 — from $3 billion to $27 billion in annual volume.

MoneyGram launched a USDC-based cash-out service in Colombia in 2025, letting users convert USDC to pesos via 500,000+ retail agents. Bitso stablecoin transactions doubled between H2 2024 and H1 2025.

If you're living in or considering a move to Colombia — one of the most popular expat destinations in Latin America — understanding the local stablecoin infrastructure is increasingly relevant. This guide to moving to Colombia as an American covers the banking and financial setup in detail, and the stablecoin layer is becoming part of that picture.

The Yield Layer: Earning While You Hold

Here's where the stablecoin story gets genuinely interesting for wealth-building expats, not just those trying to preserve purchasing power.

The traditional approach to holding dollars abroad meant accepting near-zero interest in a foreign savings account, or jumping through hoops to maintain a US bank account from overseas. Neither was great.

Stablecoin lending and yield platforms changed that equation entirely. You can now earn meaningful yield on USDC or USDT while holding it on a platform, available to anyone in the world with an internet connection.

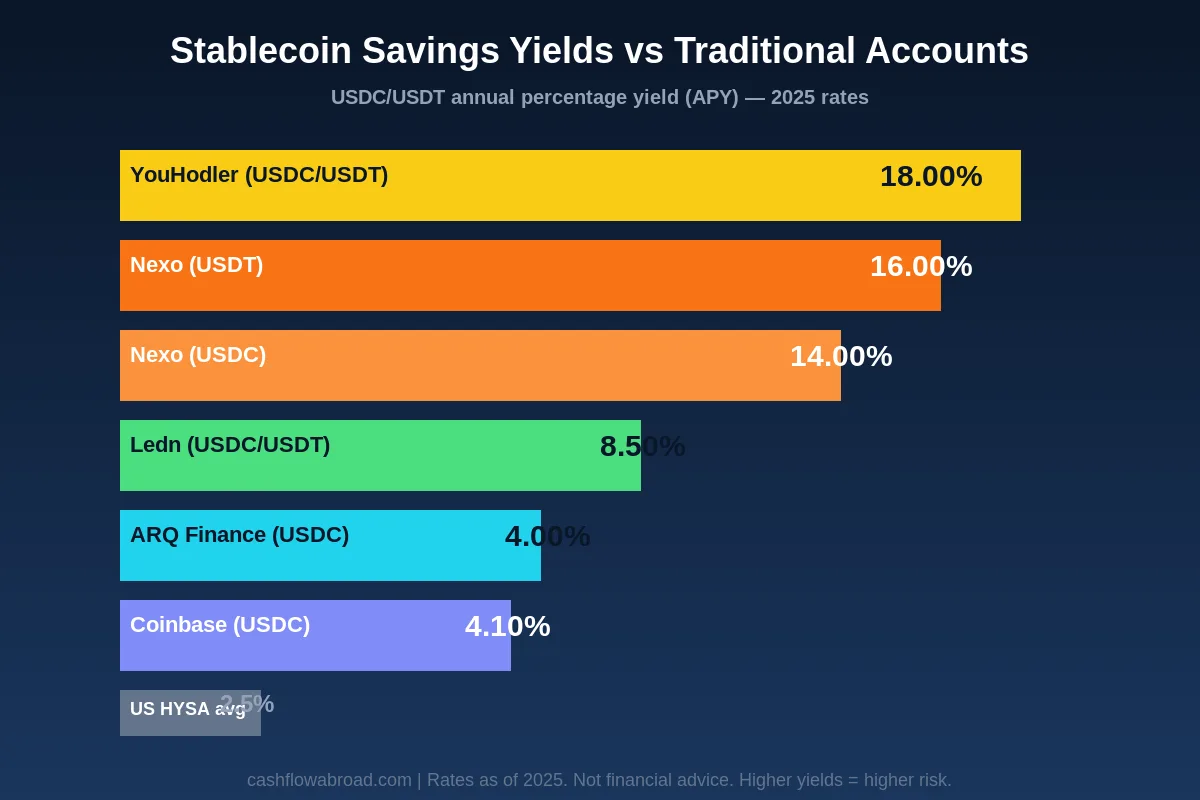

| Platform | Asset | APY (2025) | Risk Level |

|---|---|---|---|

| YouHodler | USDT/USDC | 18.00% | Higher |

| Nexo | USDT | 16.00% | Medium-High |

| Nexo | USDC | 14.00% | Medium-High |

| Ledn | USDC/USDT | 8.50% | Medium |

| Aave (DeFi) | DAI | 11.64% | Medium (smart contract) |

| Aave (DeFi) | USDC | 7.33% | Medium (smart contract) |

| Coinbase (onchain) | USDC | Up to 10.8% | Medium |

| Coinbase (standard) | USDC | 4.10% | Lower |

| ARQ Finance | USDC/EURc | Up to 4.00% | Lower |

| US HYSA (average) | USD cash | ~2.50% | Lowest (FDIC insured) |

The higher-yield platforms (YouHodler, Nexo at those rates) carry counterparty risk — you're lending your stablecoins to the platform which then lends them out. If the platform goes under, you can lose funds. This is not hypothetical: Celsius, BlockFi, and Voyager all collapsed during the 2022 crypto winter. The lesson isn't to avoid yield — it's to understand what you're holding and choose platforms with transparent operations and solid reserves.

The lower-end options (Coinbase, ARQ Finance at 4%) involve significantly less counterparty risk. Coinbase's standard USDC yield comes from Circle's reserve earnings, essentially passing through Treasury bill returns. ARQ Finance is specifically built for the LATAM expat and local use case — it lets you hold balances in USDC or EURc, earn up to 4% annually, swap seamlessly to local currencies (Mexican pesos, Colombian pesos, Argentine pesos, Brazilian reais), and even use a Mastercard with cashback for daily spending. You can deposit USDC or USDT from external wallets directly.

The Expat Stablecoin Stack: A Practical Setup

Theory is fine. Here's how to actually implement this.

Step 1: Maintain a US Anchor Account

Your first line of defense is keeping a US-based account that doesn't punish you for living abroad. Charles Schwab International is the gold standard here — free worldwide ATM withdrawals with full reimbursement, no foreign transaction fees, and no account minimums. It's the account most long-term expats refuse to leave home without.

Mercury works well for expat entrepreneurs needing a US business banking presence — especially if you're running an online business or consulting practice from abroad. Mercury integrates smoothly with crypto on-ramps and off-ramps, which becomes relevant when you're moving money between the dollar stack and your stablecoin holdings.

Related: money transfer guide

Step 2: A Regulated Exchange for On-Ramping

You need a way to convert dollars to USDC efficiently. Kraken is one of the most trusted and longest-running regulated exchanges. It supports USDC, USDT, and dozens of other assets, has solid compliance infrastructure, and is available in most countries. Coinbase is the other obvious choice for US persons — and its base USDC yield of 4.1% means you can earn immediately after converting.

The process: wire or ACH from Schwab → buy USDC on Kraken or Coinbase → send to your yield account or LATAM-focused platform. The whole thing takes under 30 minutes once accounts are set up.

Step 3: For LATAM Expats — The Local Dollar Layer

If you're in Colombia, Mexico, Argentina, or Brazil, ARQ Finance solves the last-mile problem. It lets you hold dollars in USDC, earn 4% on those balances, and swap to local currency whenever you need to pay for rent, groceries, or a restaurant. The Mastercard makes it spendable anywhere. You're not maintaining two separate financial lives — you're living in the local economy while your savings stay in dollar-denominated assets.

This is particularly useful in Colombia, where banking as a foreigner can be frustratingly slow to set up. While you're working through the process of opening a local bank account in Colombia, ARQ Finance bridges the gap entirely.

Step 4: Yield Optimization Without Recklessness

The simple rule: don't chase the highest yield with your core savings. Here's a reasonable allocation framework:

| Allocation | Where It Goes | Target Yield | Purpose |

|---|---|---|---|

| 6-month emergency fund | Coinbase standard USDC or US HYSA | 4–4.5% | Liquidity + safety |

| Medium-term savings (1–3 years) | Ledn, Coinbase onchain, Aave | 7–10% | Better yield, moderate risk |

| Speculative yield (5–10% of savings) | YouHodler, Nexo higher-tier | 14–18% | High yield, accept risk of loss |

| Daily spending buffer | ARQ Finance (LATAM) or Coinbase | 4% | Spendable dollars with basic yield |

Keep your long-term investment portfolio separate — in a PFIC-compliant brokerage like Schwab or tastytrade — and think of the stablecoin stack as your operating capital and medium-term savings vehicle, not your retirement account.

The Tax Reality for US Persons Holding Stablecoins

This section matters enormously and is frequently glossed over. The IRS treats cryptocurrency — including stablecoins — as property. Not currency. Property.

What this means in practice:

- Converting USD to USDC: Generally not a taxable event if done at a 1:1 rate with no gain.

- Converting USDC to local currency: This is a disposal of property. If you bought USDC at $1.00 and it's worth $1.00 when you spend it, there's no gain. But if you received USDC as yield (interest income) and later spend it, the yield itself was ordinary income at the time of receipt.

- Yield earned on stablecoins: This is ordinary income in the year received, reportable on your US tax return regardless of whether you're claiming the Foreign Earned Income Exclusion (FEIE). Passive income — interest, yield — is generally not excluded by FEIE.

- FBAR and FATCA: If you hold stablecoins on foreign exchanges and your aggregate foreign financial account balances exceed $10,000, FBAR reporting may be required. FATCA thresholds vary by filing status. This is covered in detail in the complete US expat banking and tax guide.

The good news for US expats: if you're using platforms domiciled in the US (Coinbase, Kraken), the reporting infrastructure is already there. They issue 1099 forms. The complication arises with foreign platforms (Nexo, YouHodler, offshore DeFi), where you're entirely responsible for self-reporting.

CoinTracking is the tool most serious expat crypto users rely on — it aggregates across exchanges and wallets, calculates gains/losses automatically, and generates tax reports compatible with US, German, UK, and dozens of other tax jurisdictions. If you're holding stablecoins across multiple platforms, this removes the headache.

For a full breakdown of crypto tax reporting obligations as a US expat, including how staking, lending, and yield income is classified, see the crypto taxes for US expats guide.

Risks You Need to Take Seriously

The stablecoin play works — but it's not without real risks that deserve honest acknowledgment.

De-Pegging Risk

Stablecoins have lost their peg before. The most dramatic example was TerraUSD (UST) in May 2022, an algorithmic stablecoin that collapsed from $1.00 to near zero in days, destroying approximately $40 billion in value. USDC itself briefly de-pegged to $0.87 in March 2023 when Silicon Valley Bank — which held $3.3 billion of Circle's reserves — failed. It recovered to $1.00 within 48 hours, but the scare was real.

USDT and USDC are the most battle-tested stablecoins. Neither has permanently lost its peg. But the risk exists, particularly in stress scenarios.

Platform Counterparty Risk

Celsius, BlockFi, Voyager, Genesis — all major yield platforms that failed in 2022. If you're holding stablecoins on a yield platform rather than in your own wallet, you're exposed to that platform's solvency. Higher yield almost always means higher counterparty risk. The 18% APY platforms are not paying you that yield out of charity — they're taking on leverage and risk to generate it.

Regulatory Risk

Stablecoin regulation is evolving rapidly. In the US, new legislation is moving through Congress that would establish federal oversight of stablecoin issuers. In the EU, MiCA regulations are already in effect. In some countries, stablecoins face restrictions or outright bans. Know your local regulatory environment — most countries haven't moved to restrict them, but stay informed.

Self-Custody Risk

If you hold stablecoins in a self-custodied wallet (a hardware wallet like Ledger, or a software wallet like MetaMask), you're immune to platform failure — but you're entirely responsible for your private keys. Lose the seed phrase and the funds are gone permanently. There is no recovery. No customer support. No insurance.

Related: expat investing playbook

The Bigger Picture: Geographic Arbitrage + Dollar Stability

The entire premise of geographic arbitrage — living in a lower-cost country while earning in a stronger currency — depends on protecting the currency advantage you're exploiting.

It's not enough to move to a place where rent is $400/month instead of $2,000. If your savings are denominated in a currency losing 40% per year, the cost-of-living advantage disappears. You need to stay in dollars (or another stable currency) while living in a lower-cost peso or lira or naira economy.

The geographic arbitrage playbook outlines the country selection framework in detail. The stablecoin layer is what makes the financial side of that playbook actually work in practice.

The expats winning this game are running what amounts to a two-layer financial system:

- Income and savings layer: Earned in USD, held in USDC or US-denominated accounts, earning 4–10% yield

- Spending layer: Converted to local currency at point of need, via a card like ARQ Finance's Mastercard or via a zero-fee international account like Schwab

The gap between these two layers — strong dollar savings growing at yield, spending at local prices — is where the wealth is built.

Moving Money: Getting Funds Into and Out of Your Stablecoin Stack

One friction point is moving money between traditional banking and stablecoin infrastructure. A few tools that handle this efficiently:

For international wire transfers: Remitly offers competitive rates for moving money into local currencies. If you need to cash out stablecoins to a local bank account, convert on a major exchange first, then transfer the fiat internationally.

For on/off ramp in LATAM: ARQ Finance handles this natively for Mexico, Colombia, Argentina, and Brazil — deposit USDC directly from your crypto wallet and withdraw to local bank accounts in local currency.

For tracking everything: When you're running a multi-country, multi-platform financial operation, visibility matters. CoinTracking handles the crypto portfolio side. For a comprehensive look at moving money internationally — including the fees that most services hide — the expat money transfer guide covers everything from wire fees to corridor-specific rates.

If you're based in Colombia specifically and looking for local employment or freelance opportunities to supplement your income, Trabajo Colombia is a free job and services board specifically for expats in Colombia — worth bookmarking.

Is This Right for You?

The stablecoin stack isn't for everyone. If you're living in Western Europe, Japan, or Singapore — places with stable currencies and functioning financial systems — the urgency is much lower. You might still benefit from stablecoin yield versus a traditional savings account, but the currency preservation angle doesn't apply the same way.

But if you're in, or considering, any of the following situations:

- Living in Argentina, Turkey, Nigeria, Egypt, or other high-inflation economies

- Countries with capital controls or USD access restrictions

- Colombia, Mexico, Peru, Brazil, or other LATAM countries where dollar-denominated savings are practical

- Any country where your local bank account can't hold foreign currency easily

...then the stablecoin layer is one of the highest-leverage financial moves available to you.

The numbers are unambiguous. A dollar kept in a US savings account earning 2.5% is a dollar doing moderately well. A dollar converted to USDC, earning 4–8%, while you live in a country where that same dollar buys 3–5x as many goods as it would at home — that's the geometric arbitrage these expats have been quietly running for years.

Conclusion: The Dollar Wins, But Only If You Hold It Right

The expats who came out ahead in Argentina's 211% inflation year, Turkey's lira collapse, and Nigeria's naira devaluation weren't necessarily smarter than their neighbors. They just understood one thing: when the local currency is failing, stop holding the local currency for anything beyond daily spending.

Stablecoins solved the practical problem of accessing dollar-denominated savings without a US address. Yield platforms solved the problem of those dollars sitting idle. Apps like ARQ Finance solved the last-mile problem of converting and spending those dollars in local economies.

Put it all together and you have a financial stack that lets you live on local prices while your savings appreciate in the world's reserve currency. That's the whole game.

Start simple: get a Schwab or Mercury account anchored to the US, open a Coinbase or Kraken account for on-ramping to USDC, and experiment with ARQ Finance if you're in LATAM. Scale the yield layer as you get comfortable with the infrastructure.

The wealth destruction from inflation is silent and gradual. The defense against it is equally quiet — until you look at the numbers a year later and realize you're the one who stayed whole.

Financial Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or investment advice. Stablecoins carry risks including de-pegging, platform insolvency, smart contract vulnerabilities, and regulatory changes. Cryptocurrency is treated as property by the IRS and may create taxable events. US persons must comply with FBAR, FATCA, and applicable tax reporting requirements for foreign financial accounts and cryptocurrency holdings. Consult a licensed financial advisor and tax professional before making any investment decisions. Past performance of yield rates does not guarantee future returns. ARQ Finance is not an investment advisor.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Investing & Wealth BuildingJuly 3, 2026

Investing & Wealth BuildingJuly 3, 2026

REITs for US Expats: Income, Tax Rules, and PFIC Traps

US expats can earn 4%+ REIT yields at a 29.6% effective rate with the permanent Section 199A deduction. Know which funds are PFICs and which are not.

Investing & Wealth BuildingJune 26, 2026

Investing & Wealth BuildingJune 26, 2026

Options Trading for US Expats: Tax Rules and Traps

Section 1256 contracts cap US expat options traders at a 26.8% blended rate. Understand wash sales, NIIT traps, mark-to-market, and Form 6781 rules.

Investing & Wealth BuildingJune 24, 2026

Investing & Wealth BuildingJune 24, 2026

W-8BEN: How Expats Cut US Withholding on Dividends

Nonresident aliens can halve 30% US dividend withholding with Form W-8BEN. See treaty rates by country, the portfolio interest exemption, and REIT