Panama Residency: Live on $2,000/Month, Zero Local Tax

Panama offers zero local tax on foreign income, dollar-denominated living, and permanent residency for just $1,000/month. Here's the full breakdown.

Panama taxes zero on foreign income and runs on the US dollar. Full guide to visas, costs, banking, and Pensionado discounts for expats.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

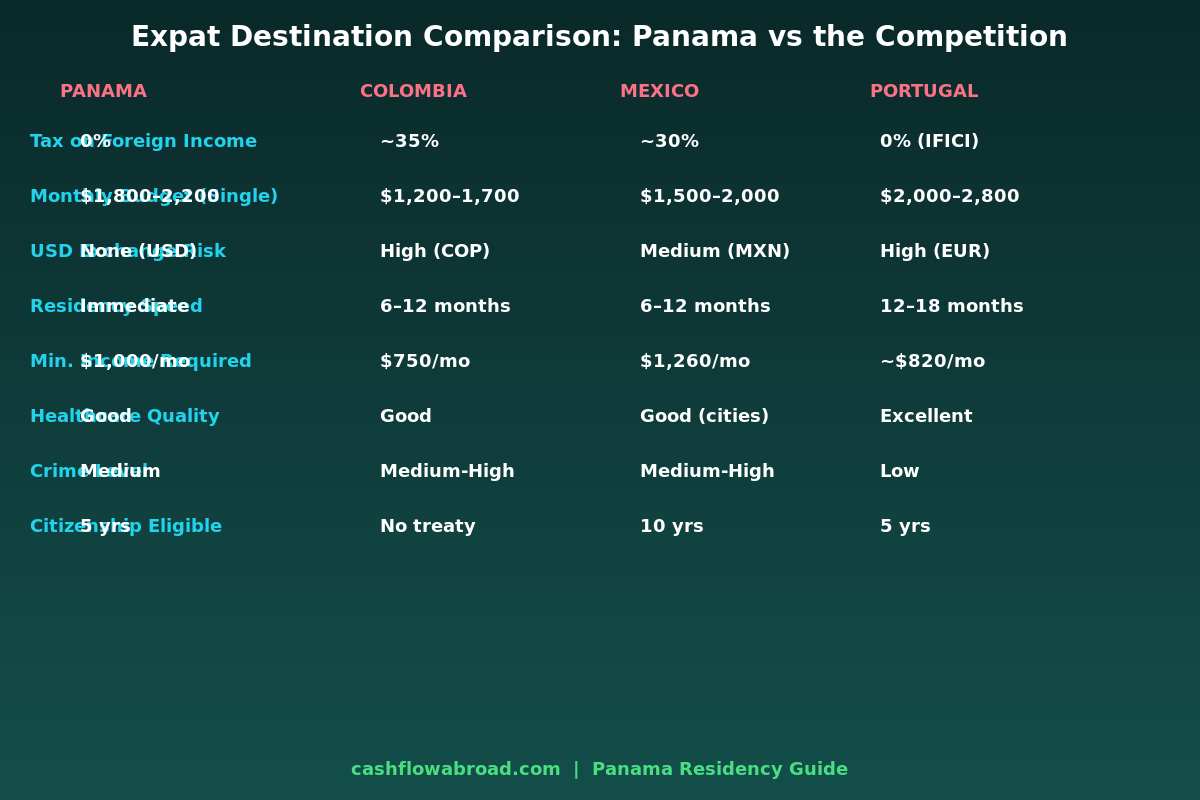

Most expats shopping for a low-tax base in Latin America spend months comparing Colombia, Mexico, and Costa Rica. They almost never look seriously at Panama — and that's a mistake that costs them thousands every year in currency losses alone.

Panama is the only country in the Americas where the US dollar is the official currency, every ATM dispenses dollars, and foreign-sourced income faces zero local tax. No exchange rate erosion. No currency conversion fees on your income. No Panamanian income tax on your US dividends, pension, or freelance contracts. Just a low cost of living, world-class banking infrastructure, and one of the most generous retirement visa programs on the planet.

There's a catch — there's always a catch — and we'll cover it. But first, let's look at the numbers.

Panama's Territorial Tax System: What It Actually Means

Panama taxes only income generated inside Panama. If your income comes from outside the country — US dividends, a remote job paid by a foreign company, a US pension, Social Security, rental income from a US property — Panama doesn't touch it. None of it. That's not a loophole or an incentive program with a sunset clause. It's the foundational design of Panama's tax code, and it applies whether you're a resident or not.

The practical impact: a digital nomad earning $6,000/month from US clients pays $0 in Panamanian income tax. A retiree drawing $3,500/month from a 401(k) plus Social Security pays $0 in Panamanian income tax. An investor collecting $12,000/month in US dividends pays $0 in Panamanian income tax.

There's also no tax on foreign income when you bring it into Panama. You can deposit your US income directly into a Panamanian bank account — no remittance tax, no deemed local income. This is explicitly different from countries like Thailand that tried (briefly) to tax foreign income upon remittance.

The Catch: You Still Owe the IRS

Here's where Panama diverges from a true zero-tax outcome for US citizens: Panama and the United States have no bilateral income tax treaty. That means the usual treaty protections that eliminate double taxation don't apply. As a US citizen, you're still subject to worldwide taxation by the IRS regardless of where you live.

The path forward isn't the treaty — it's the Foreign Earned Income Exclusion (FEIE), which lets you exclude up to $126,500 (2024 figure) in earned income from US taxable income, and the Foreign Tax Credit (FTC). Since Panama taxes almost nothing, you'll have very little foreign tax paid to credit — but the FEIE alone eliminates most of the earned income tax burden for most expats. Here's a full breakdown of how the FEIE works.

Unearned income (dividends, capital gains, rental income) doesn't qualify for the FEIE, so US expats in Panama still owe US tax on investment income at normal US rates. That's the real tradeoff: Panama's territorial system saves you from local tax, but it doesn't eliminate your US obligations the way a true treaty country might.

The Three Residency Paths (and Which One You Should Use)

Panama offers more paths to legal residency than almost any country in the Americas. Here are the three most relevant for North American expats:

| Visa Type | Key Requirement | Residency Granted | Stay Requirement | Total Cost |

|---|---|---|---|---|

| Pensionado | $1,000/month pension income | Immediate permanent | 1 visit per year | $2,500–4,000 |

| Friendly Nations | $200k real estate or bank deposit | 2 yrs temp → permanent | None specified | $3,000–5,000 |

| Qualified Investor | $300k real estate (rising to $500k Oct 2026) | Immediate permanent | None | $4,000–7,000 |

The Pensionado Visa: Still the Best Deal in Latin America

If you have any pension income — Social Security, a 401(k) distribution, a corporate pension, even a small annuity — the Pensionado Visa is almost certainly your best option. The income threshold is just $1,000/month. If you own property in Panama worth $100,000 or more, that drops to $750/month.

On approval, you receive immediate permanent residency — not a temporary permit that you then have to convert after two years. Panama grants it outright. After five years of legal residency, you're eligible to apply for Panamanian citizenship and a Panamanian passport, which carries visa-free access to more than 140 countries.

The minimum maintenance requirement: visit Panama at least once per calendar year. That's it.

The Qualified Investor Deadline You Can't Ignore

If you're considering the Qualified Investor route for real estate, the clock is running. The current threshold is $300,000 — but Panama has officially announced it rises to $500,000 after October 2026. If you're planning to buy property anyway and want to lock in the lower threshold for immediate permanent residency, you need to move before that deadline.

The Qualified Investor Visa also has zero minimum stay requirement, making it the choice for people who want a Panama residency card for banking and tax purposes but plan to split time across multiple countries.

The Pensionado Discount Stack: Real Money

The Pensionado program's discounts often get dismissed as small perks, but the math is more interesting than most people realize. Under Panama's Law 6 of 1987, businesses nationwide are legally required to honor these discounts. They're not promotional offers that can be revoked:

| Category | Discount | Monthly Value (estimate) |

|---|---|---|

| Hotels (Mon–Thu) | 50% off | $100–300/trip |

| Hotels (Fri–Sun) | 30% off | $60–150/trip |

| Flights (domestic + most intl) | 25% off | $75–300/ticket |

| Restaurants | 25% off | $40–100/month |

| Utility bills | 25% off | $25–60/month |

| Medical consultations | 20% off | $10–50/month |

| Hospitals/procedures | 15% off | Varies |

| Entertainment | 50% off | $20–80/month |

A retiree couple who travels regionally four times a year and eats out regularly could easily save $3,000–6,000/year on Pensionado discounts alone. That's not trivial when your total monthly budget is $2,500.

What It Actually Costs to Live in Panama

Panama City is no longer dirt-cheap — it's a genuine financial hub and that's reflected in housing. But outside the premium coastal neighborhoods, it remains far more affordable than any major US city.

Single Person: $1,800–$2,200/Month (Comfortable)

- Rent (1BR, mid-range area like El Cangrejo): $800–$1,200

- Utilities + internet (AC usage matters here): $120–$200

- Groceries: $300–$400 (imported goods cost more; local produce is cheap)

- Transport (Metro + Uber): $50–$100 (Metro is $0.35/ride; Uber runs $3–5 cross-city)

- Dining out (2–3x/week): $150–$250

- Health insurance: $100–$200/month (see below)

- Misc/entertainment: $150–$250

Total: $1,670–$2,550/month for a comfortable single-person lifestyle in Panama City. Premium areas like Costa del Este — popular with expat professionals — start at $2,200/month for rent alone.

Couple: $2,500–$3,200/Month

Couples don't pay double on rent or utilities, so the per-person cost drops significantly. A couple in a solid mid-range neighborhood can live comfortably on $2,500–3,200/month, including one or two restaurant meals per week, occasional day trips, and modest entertainment spending.

If you're based in Boquete (mountain town, cooler climate, large expat community), David, or a beach area like Pedasi, subtract $400–700/month from those numbers. Several thousand expats live well outside Panama City on $1,500–1,800/month total.

Panama Banking: The FATCA Reality

Panama's banking sector is large, sophisticated, and historically private — which is precisely why it attracts expats. Over 80 banks operate under Panama's banking system, including major international institutions.

The problem: FATCA. Most Panamanian banks are FATCA-compliant, meaning they report US account holders to the IRS. Some have decided the compliance burden isn't worth it and refuse American clients outright. Others accept US clients willingly — including Banistmo, Banesco, BAC, Unibank, Scotiabank, and Banco Nacional.

As a non-resident, opening an account is nearly impossible — minimum deposits of $250,000 are common. Once you have residency, that number drops to $500–$5,000 depending on the bank and account type.

The smart move: keep your US banking infrastructure intact while you establish Panamanian accounts. Charles Schwab's international account gives you a US debit card with zero ATM fees worldwide, making it an ideal bridge account while you navigate local banking. Since Panama runs on USD, you'll never pay an ATM conversion fee — you're withdrawing dollars from dollar machines.

Also critical: maintain a legitimate US mailing address for your US bank, IRS filings, and brokerage accounts. A virtual mailbox service like Traveling Mailbox gives you a real US street address in 50+ cities for $15/month, with mail scanning and check deposits — exactly what you need to keep your US financial infrastructure intact after your move. See our full guide on expat banking and taxes for the complete account stack.

The Dollar Economy Advantage: A Bigger Deal Than It Looks

Most expat destinations quietly drain your savings through exchange rate erosion. If you earn in dollars and your local currency appreciates against the dollar, your real purchasing power shrinks. The Colombian peso, Mexican peso, Costa Rican colon — they all fluctuate. Some dramatically.

Panama eliminated this problem by adopting the US dollar (called the "balboa" locally, but physically the same bill) as its official currency in 1904. Your rent is quoted in dollars. Your grocery receipt is in dollars. Your utility bill is in dollars. A $2,000 monthly budget is a $2,000 monthly budget — not "$2,000 equivalent, depending on this week's rate."

For a long-term retiree receiving a fixed dollar pension, this is not a minor convenience — it's fundamental financial stability. Compare it to the expat who moved to Medellín in 2020 when $1 = 4,000 pesos, only to watch the peso strengthen by 20% in some quarters, silently inflating their real costs. That can't happen in Panama.

Healthcare in Panama

Panama's healthcare is genuinely good by regional standards. Panama City has multiple internationally accredited hospitals — Hospital Nacional, Hospital Punta Pacífica (affiliated with Johns Hopkins), and Clínica Hospital San Fernando among them. Many doctors trained in the US or Europe and speak English.

Private healthcare is a fraction of US costs. A specialist consultation runs $50–$100. An MRI costs $300–$500 versus $1,500–$3,000 in the US. A night in a private hospital room averages $200–$400.

International private health insurance through providers like SafetyWing typically runs $100–$200/month for expats under 60, giving you coverage that works both in Panama and on international travel. Panama Pensionado holders also receive a 15–20% discount on hospital procedures and medical consultations by law. For a deeper comparison of expat health insurance options, see our complete expat health insurance guide.

The Downsides Nobody Advertises

Panama earns its reputation as an expat hub, but it's not perfect. Here's what you actually need to know before committing:

Heat and humidity: Panama City sits at sea level near the equator. Temperatures stay in the 86–93°F (30–34°C) range year-round with high humidity. Air conditioning is not optional for most people — budget $80–$150/month just for electricity if you run AC regularly. Boquete in the highlands (elevation 3,900 ft) runs 60–75°F year-round and is far more comfortable, but it's a 7-hour drive from Panama City.

Crime in certain areas: Panama City has safe neighborhoods and genuinely dangerous ones. Areas like Punta Pacifica, El Cangrejo, Costa del Este, and Miraflores are solidly expat-friendly. San Miguelito and certain Colón neighborhoods are not. Do your neighborhood research before signing a lease.

No US-Panama tax treaty: As discussed, this means no treaty protections to simplify your dual-filing situation. FEIE and FTC still do most of the work, but you'll want a CPA who knows expat taxes — not your local H&R Block franchise.

FATCA banking friction: Some banks still turn away Americans. Getting your first account can involve multiple bank visits, more paperwork than you'd expect, and occasionally a flat rejection. Budget 2–4 weeks for the process once you have residency in hand.

Infrastructure outside the capital: Panama City is modern and functional. Outside of it, roads, internet reliability, and medical access drop off noticeably. If you're planning to live rurally, verify infrastructure before committing.

How to Get Your Panama Residency: The Process

The Pensionado process is the most straightforward. Here's the typical sequence:

- Gather documentation: Pension award letter or benefit statement showing $1,000+/month income, certified copy of passport, police clearance from your home country (FBI check for Americans), marriage certificate if applicable. All documents must be apostilled.

- Hire a Panamanian immigration attorney: Not optional — immigration law is processed by licensed attorneys here. Expect to pay $1,000–$2,500 in legal fees. Total government fees add another $800–$1,200.

- File in Panama in person: You must appear in person at the Servicio Nacional de Migración in Panama City. The initial filing takes a full day.

- Receive provisional carnet: You'll get a provisional ID card (carnet) while the application processes, typically within a few weeks. This allows you to open bank accounts, sign leases, and access services as a legal resident.

- Full approval: Complete processing typically takes 3–6 months. You'll then receive your permanent residency card (cédula).

Total cost: $2,500–$4,500 all-in for the Pensionado path, covering attorney, government fees, apostille costs, and document translation. For Friendly Nations ($200k investment path), budget closer to $3,500–$5,500 plus the investment capital itself.

For sending money to Panama during the application process or once you're established, Remitly offers competitive rates on USD transfers with transparent fee structures.

For more on geographic arbitrage destinations and how Panama compares to the full field, that guide covers 10 countries side-by-side with specific cost and tax data.

Bottom Line: Who Panama Is Really For

Panama works best for three types of expats: retirees with a pension above $1,000/month who want instant permanent residency and legally mandated discounts; digital nomads or remote workers who want a dollar-denominated base in the Americas with real banking infrastructure and low friction; and investors who want a territorial tax country with direct US dollar access and strong property rights.

It's not the right move for someone trying to escape IRS obligations entirely — that requires renouncing citizenship, which is a separate and permanent decision. But for reducing your total tax burden, eliminating exchange rate risk, and landing in a place with competent healthcare, fiber internet, and direct flights to Miami in 2.5 hours, Panama is as practical as it gets.

The Qualified Investor real estate deadline of October 2026 is real — if you're buying property and want immediate permanent residency at the $300k threshold instead of the future $500k requirement, the window is closing. For everyone else, the Pensionado at $1,000/month remains one of the best residency-to-cost ratios in the world.

Financial Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Tax laws and immigration regulations change frequently. Consult a qualified immigration attorney and a CPA with international expertise before making any residency or financial decisions. US citizens remain subject to worldwide US taxation regardless of residency status abroad.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageMay 19, 2026

Geographic ArbitrageMay 19, 2026

Panama for US Expats: Dollar Economy, Territorial Tax, Visa Reality

Panama uses the US dollar, taxes zero foreign income, and has 53 international banks. Full guide to visas, costs, and banking for US expats.

Geographic ArbitrageJune 1, 2026

Geographic ArbitrageJune 1, 2026

Paraguay Tax Residency: Earn Globally, Pay Zero

Paraguay taxes 0% on foreign income. Get legal residency for under $2,000, visit once every 3 years. Complete 2026 guide for US expats.

Geographic ArbitrageMay 24, 2026

Geographic ArbitrageMay 24, 2026

Costa Rica Expat Guide: $2,100/Month, 0% Foreign Tax

Costa Rica taxes zero on foreign income. Live on $2,100/month and qualify with $1k/month SS. Complete visa, tax, banking, and cost of living guide.