Moving Abroad Mid-Year: Maximize Your Tax Benefits

Moving in December instead of January can cost you $30,000 in FEIE exclusions. Here's how the pro-rated formula works—and how to maximize it.

Moving in Q4 instead of Q1 costs you up to $30K in FEIE exclusions. Learn how pro-ration works, state tax traps, and FBAR obligations in year one.

Most people who move abroad in October or November are shocked when their accountant tells them they owe $20,000–$30,000 in taxes that a February move would have eliminated. The Foreign Earned Income Exclusion (FEIE) is the most powerful tax tool available to US expats—but it's ruthlessly pro-rated based on the number of days you spend abroad in the tax year. Move on December 1 and you're entitled to exclude just $11,041. Move on January 2 and you're looking at nearly the full $130,000 (2025 limit). That difference is worth up to $30,000 in federal income tax for someone in the 37% bracket.

This guide covers exactly how the FEIE calculation works for mid-year movers, which qualifying test to use, how to legally maximize your exclusion even when you move partway through the year, and what to do about state taxes, FBAR obligations, and health insurance during the transition period.

How the FEIE Works When You Move Mid-Year

The Foreign Earned Income Exclusion lets qualifying US citizens and residents exclude up to $130,000 (tax year 2025) or $132,900 (tax year 2026) of foreign-earned income from federal income tax. But the exclusion isn't binary—you don't just qualify or not qualify for the full amount. It scales with the number of days you have a foreign tax home during the calendar year.

The IRS calculates your maximum exclusion using this formula:

Your Max FEIE = ($130,000 × Qualifying Days) ÷ 365

"Qualifying days" are any days within the calendar year that you spent abroad while meeting one of two tests: the Physical Presence Test or the Bona Fide Residence Test. Every day counts—weekends, holidays, the day you land.

Physical Presence vs. Bona Fide Residence

Most mid-year movers default to the Physical Presence Test because it's objective: you need to be present in a foreign country for 330 full days within any consecutive 12-month period. The calendar year is irrelevant—you can use any 12-month window that contains your qualifying days.

The Bona Fide Residence Test is harder to use in your first year. It requires being a bona fide resident of a foreign country for an uninterrupted period that includes an entire calendar year (January 1 to December 31). If you move abroad in May 2025, you can't qualify under the Bona Fide Residence Test for 2025—only for 2026 and beyond, once you've been there continuously through the full calendar year. The upside: once you qualify, the Bona Fide Residence Test is simpler to maintain than counting 330 days.

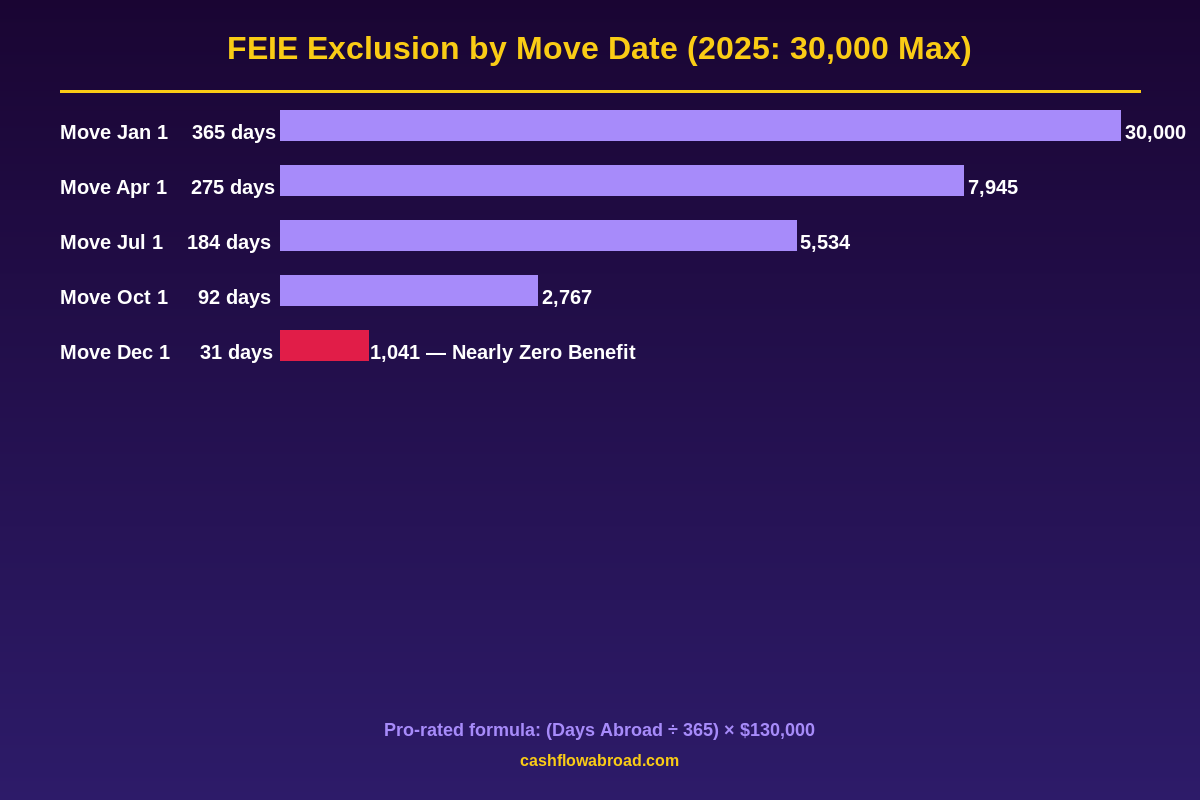

What Your Move Date Actually Costs You

The impact of your move date is dramatic. Here's how the FEIE exclusion breaks down for tax year 2025 under the Physical Presence Test (assuming you stay abroad through December 31):

| Move Date | Days Abroad in 2025 | Max FEIE Exclusion | Tax Saved (37% bracket) |

|---|---|---|---|

| January 2 | 363 | $129,288 | $47,837 |

| April 1 | 275 | $97,945 | $36,240 |

| July 1 | 184 | $65,534 | $24,248 |

| October 1 | 92 | $32,767 | $12,124 |

| December 1 | 31 | $11,041 | $4,085 — nearly zero |

The tax impact of moving in April versus December is $32,000. This is why tax professionals urge clients to plan their departure date—not just their destination.

There's also the question of which income qualifies. The FEIE only excludes foreign-earned income: wages, salaries, or self-employment income you earn while physically living abroad and doing work abroad. Passive income (dividends, interest, capital gains, rental income) never qualifies for the FEIE regardless of how long you've been abroad. See our complete FEIE guide for a breakdown of what counts and what doesn't.

The 12-Month Period Workaround

Here's where mid-year movers get a legitimate advantage that most don't know about. The Physical Presence Test's 330-day requirement doesn't have to fit inside a calendar year. You can use any 12-month period that starts from the date you arrive abroad.

Scenario: You move to Medellín on July 1, 2025. By June 30, 2026, you've spent 330+ days in Colombia. Your qualifying period is July 1, 2025 – June 30, 2026.

For tax year 2025, your qualifying days are July 1 – December 31 = 184 days, giving you a maximum FEIE of $65,534. That's real money excluded in your first partial year—money you would have owed at full US rates if you hadn't structured the claim correctly.

For tax year 2026, your qualifying days include the entire calendar year, so you'd exclude the full $132,900. The key insight: you don't need to re-qualify from January 1. Your 12-month window carries over.

This also means that if you move abroad in December 2025 but stay through the following November, you can still claim FEIE on foreign income earned from December onward using that 12-month window—even though your 2025 tax return will show minimal exclusion for that first partial year. Whether it's worth filing an amended return later using that December-through-November period depends on how much foreign income you earned in that time. An expat CPA can run the numbers in about 15 minutes.

State Taxes in Your Departure Year

The FEIE is a federal tool. State income taxes operate on completely separate rules, and several states actively pursue former residents who moved abroad.

Most states stop taxing your income as of your domicile-change date—the day you establish permanent legal residence in a foreign country and sever significant ties with your home state. For a clean break, this means: close local bank accounts, relinquish your driver's license, file a notice of intent to leave (required in some states), and establish a documented foreign address.

Three states are notoriously aggressive:

- California: Uses a "closest connection" test. Moving abroad doesn't automatically end CA residency unless you've severed all safe-harbor ties—no CA business, no minor children at CA schools, no CA real property you own and could return to.

- Virginia: Presumes you're still a resident if you return for visits totaling more than 183 days per year. The state will also scrutinize whether you maintained a permanent place of abode.

- South Carolina: Will continue taxing you if you maintain any significant SC contacts after departure.

For states like Florida, Texas, Nevada, or South Dakota—which have no state income tax—this is a non-issue. This is one of the reasons many expats elect to establish domicile in a no-income-tax state before leaving the US. Our guide on state taxes for expats walks through domicile strategy in detail.

One practical issue: once you move abroad, you need a physical US mailing address to maintain banking, receive IRS correspondence, and keep your state domicile clean. A virtual mailbox service like Traveling Mailbox gives you a real US street address in 50+ cities for around $15/month—mail is scanned and forwarded digitally. This is particularly important during the transition year when you're still managing accounts tied to your old address.

FBAR and FATCA: What Triggers in Year One

The day you open a foreign bank account, the US reporting clock starts. This catches new expats off guard because the thresholds are lower than people expect, and the penalties for missing them are severe.

FBAR (FinCEN Form 114)

If the aggregate maximum balance of all your foreign financial accounts exceeds $10,000 at any point during the calendar year—even on a single day—you must file an FBAR. The threshold applies to the total across all accounts, not per account. Open a local checking account with $5,000 and a savings account with $6,000 and you've crossed the threshold.

The FBAR is filed electronically through FinCEN's BSA E-Filing system (not with your tax return), with a deadline of April 15 and an automatic extension to October 15. No application required—the extension is automatic.

Non-willful failure to file now carries a maximum penalty of $16,536 per form per year (not per account), following the 2023 Supreme Court ruling in Bittner v. United States. Before that ruling, the IRS was assessing $10,000 per account per year—the case that prompted the ruling involved a $2.72 million penalty against a Romanian-American for five years of missed filings covering 272 accounts. The per-form cap limits annual non-willful exposure to $16,536. Willful violations still carry penalties of $165,353 or 50% of the account balance—whichever is greater—plus potential criminal prosecution.

FATCA (Form 8938)

Form 8938 is filed with your IRS tax return (Form 1040) and covers a broader range of foreign financial assets, including accounts, directly-held foreign stocks, and interests in foreign entities. The thresholds for expats living abroad are significantly higher than for US residents:

| Filing Status (Abroad) | Year-End Threshold | Any-Time-During-Year Threshold |

|---|---|---|

| Single | $200,000 | $300,000 |

| Married Filing Jointly | $400,000 | $600,000 |

FBAR and Form 8938 are completely separate filings with independent thresholds—exceeding one doesn't automatically trigger the other. Both can be required in the same year. Most new expats in their first year trigger only the FBAR threshold; Form 8938 typically becomes relevant once you've built up significant foreign savings or transferred investment accounts abroad.

Foreign Housing Exclusion: The Add-On Most People Miss

Most FEIE discussions skip the Foreign Housing Exclusion (FHE), which can add another $15,000–$40,000+ in excluded income on top of the FEIE limit. If you're renting in a high-cost city like Zurich, Singapore, London, or Tokyo, this exclusion can cover a substantial portion of your rent.

Like the FEIE, the FHE is pro-rated by your qualifying days abroad. The base housing amount is 16% of the FEIE limit ($20,800 for 2025). The FHE covers your actual housing expenses above that base, up to a city-specific cap set by the IRS. If you pay $30,000 in annual rent in Singapore, you can potentially exclude $9,200 in housing costs (the amount above the $20,800 base)—pro-rated by qualifying days.

The FHE is claimed on the same Form 2555 as the FEIE. In a high-rent city, working with a tax professional who optimizes both exclusions can save you an additional $3,000–$12,000 per year that most DIY filers leave on the table. See how both exclusions interact with the Foreign Tax Credit in our FEIE vs. FTC comparison.

Setting Up Banking During the Transition Year

In your first year abroad, income hits US accounts while you're building local banking infrastructure. This creates cash management complexity that can turn into a tax headache.

For expats who need a US brokerage, Charles Schwab International is the default recommendation: it explicitly serves Americans abroad, offers a checking account with fee-free ATM withdrawals worldwide, and won't close your account when you update your address to a foreign country. Most other major US brokers—Fidelity, Vanguard, E*TRADE—restrict or close accounts once they detect a foreign address.

For US business banking, Mercury operates entirely online and works well for expat freelancers and business owners who need to receive USD payments and pay US contractors without maintaining a US physical presence.

For international transfers between your US accounts and local foreign accounts, Remitly offers competitive exchange rates with significantly lower fees than bank wire transfers—useful during the first year when you're regularly moving money while building up local savings.

Moving Back to the US Mid-Year

The same math works in reverse. If you've been abroad for years and return to the US mid-year, you can still claim a pro-rated FEIE for the portion of the year you were abroad.

Under the Bona Fide Residence Test: if you return on August 1, 2025, and had established bona fide residence abroad before January 1, 2025, your qualifying days are January 1–August 1 = 212 days. Maximum exclusion: (212 ÷ 365) × $130,000 = $75,562.

Under the Physical Presence Test: same calculation, but your qualifying period looks back to the 12-month window ending before your return date. If you had 330+ days abroad in the preceding 12 months before returning, you can claim the pro-rated exclusion for your days abroad in the calendar year.

One trap returning expats hit: if you come back and start a US job on August 1, that US-source income earned while physically in the US is not eligible for the FEIE regardless of how many qualifying days you had earlier in the year. The FEIE only applies to foreign-earned income earned while your tax home was abroad.

Missed Year One? The Streamlined Fix

Many expats don't realize they owe anything in their first year abroad—they assume moving abroad means they're off the US tax grid. Others know about income taxes but don't realize FBAR exists. The IRS has a specific amnesty program for this situation: the Streamlined Foreign Offshore Procedures (SFOP).

If your failure to file was non-willful (you simply didn't know), SFOP lets you:

- File amended returns for the 3 most recent tax years you missed

- File delinquent FBARs for the 6 most recent years

- Pay any taxes owed plus interest—but with all penalties waived, including FBAR penalties

To qualify, you must meet the non-residency test (you were outside the US for at least 330 days in one of the 3 covered tax years) and the IRS must not have already contacted you about those years. The SFOP is documented at the IRS website and requires a signed non-willfulness certification—essentially a statement that you didn't know about the requirements, not that you chose to ignore them.

The window matters. Once the IRS opens an examination of your returns, SFOP eligibility disappears. If you're behind, the cost of acting now is just taxes owed plus interest. The cost of waiting is potentially $16,536 per year in FBAR penalties on top of the taxes. Our expat banking and taxes guide covers additional compliance options in detail.

Health Insurance During the Transition Year

Most employer health insurance ends on your last day of employment in the US. If you're leaving a job to move abroad, you'll have a coverage gap unless you plan ahead. COBRA extends US employer coverage for up to 18 months but costs $500–$800/month for an individual—you're paying the full premium your employer was subsidizing, plus a 2% administrative fee.

For most expats, international health insurance makes more sense from day one abroad. SafetyWing offers nomad health insurance starting around $56/month with worldwide coverage including limited US coverage. It's month-to-month with no annual commitment—ideal for people in their first year who may still be figuring out which country they'll settle in. For a more comprehensive plan with higher limits and better hospital network access, our expat health insurance guide covers SafetyWing, Cigna Global, and Allianz Care side by side.

Year-One Tax Action Checklist

| Task | Deadline | Notes |

|---|---|---|

| Establish foreign tax home | Day you move | Keep records: signed lease, utility bills, foreign ID |

| Start tracking qualifying days | Ongoing | Use a spreadsheet or app; you need 330 for Physical Presence Test |

| Notify US employer of foreign tax home | Before year-end | May reduce withholding via Form W-4 adjustment |

| Sever state domicile ties | Before Dec 31 | Critical for CA, VA, SC residents |

| File Form 2555 with 1040 | April 15 (Jun 15 auto-ext) | Claims both FEIE and Foreign Housing Exclusion |

| File FinCEN 114 (FBAR) | April 15 (Oct 15 auto-ext) | Separate from tax return; filed via BSA E-Filing system |

| File Form 8938 if FATCA threshold hit | With 1040 | Attached to your tax return; separate from FBAR |

The Bottom Line

The FEIE is powerful but not automatic. Moving abroad in Q4 instead of Q1 can cost you $30,000 in exclusion value—not because the rules changed, but because the math works against late-year movers. If you're planning a move, target January or early February for maximum exclusion in year one. If you've already moved mid-year, understand the 12-month rolling period strategy to ensure you're capturing every qualifying day you're entitled to.

Year one abroad is also when most compliance mistakes happen. The FBAR clock starts the moment you open a foreign account over $10,000, and the first-year complexity of dual-country income, state tax severance, and health insurance transitions is enough to justify hiring an expat tax professional for at least your first two returns. The cost of a specialist ($500–$2,500) is trivial compared to missing $50,000+ in exclusions or accruing $16,536 per year in FBAR penalties from a form you didn't know existed.

For a full picture of the ongoing FEIE strategy—not just year one—see our guide to zero federal income tax as a US expat and the FEIE vs. Foreign Tax Credit comparison to understand when the FTC might serve you better than the FEIE.

Disclaimer: This post is for informational purposes only and does not constitute tax or legal advice. Tax rules change frequently and individual circumstances vary significantly. Consult a qualified expat tax professional (CPA or enrolled agent) before making decisions based on this information. This post may contain affiliate links; we may earn a commission at no additional cost to you if you purchase through links in this article.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMarch 31, 2026

Expat Tax & FinanceMarch 31, 2026

How to Pay Zero Federal Tax (Legally) as a US Expat

Every year, thousands of US expats legally pay $0 in federal income tax on up to $130,000+ of earned income. The IRS can and will audit this.

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.

Expat Tax & FinanceJune 23, 2026

Expat Tax & FinanceJune 23, 2026

FBAR vs Form 8938: Expat Reporting Guide

US expats with foreign accounts over $10,000 must file FBAR. Learn how Form 8938 differs, current penalty amounts, and how to catch up.