Mexico's 183-Day Tax Trap: What Expats Miss

Over 1.6M Americans live in Mexico. Most don't know that staying 183 days triggers worldwide income tax at up to 35%. Here's how fiscal residency actually works.

Staying 183 days in Mexico makes you a fiscal resident taxed on worldwide income at up to 35%. Learn how ISR works and how to stay compliant.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Over 1.6 million Americans live in Mexico — more than in any other country on earth. Most chose it for the obvious reasons: $1,200–$2,200 a month covers a comfortable life, the food is genuinely excellent, and CDMX has better co-working infrastructure than most US cities. What almost none of them knew before moving: staying 183 days flips a legal switch that makes Mexico's tax authority, SAT, consider you a fiscal resident — and suddenly your worldwide income is on the table for taxes up to 35%.

That's not a hypothetical. It's Mexico's Impuesto Sobre la Renta (ISR) law, and it applies whether you arrived on a tourist visa, a temporary residency card, or a digital nomad permit. The income you earned from clients in Austin or a Shopify store you run from a Condesa café — SAT wants its share of all of it.

How the 183-Day Rule Actually Works

Mexico's Tax Code (Código Fiscal de la Federación, Article 9) sets out two ways you can become a Mexican fiscal resident:

- The day-count test: Spend 183 or more days in Mexico in any calendar year.

- Center of vital interests: Mexico is where your primary home is, your family lives, or more than 50% of your income originates — regardless of how many days you're physically present.

The 183-day trigger gets all the attention, but the vital interests test is quieter and more dangerous. An expat who splits time 60/40 between Mexico City and Miami could still qualify as a Mexican fiscal resident if their spouse and kids stayed in CDMX full-time.

Days are counted on a calendar-year basis: January through December. Partial days count as full days. A weekend trip to Tulum from your CDMX apartment counts. Business travel within Mexico counts. There's no "grace period" once you cross the threshold — you're a fiscal resident for the entire tax year.

What Fiscal Residency Actually Costs You

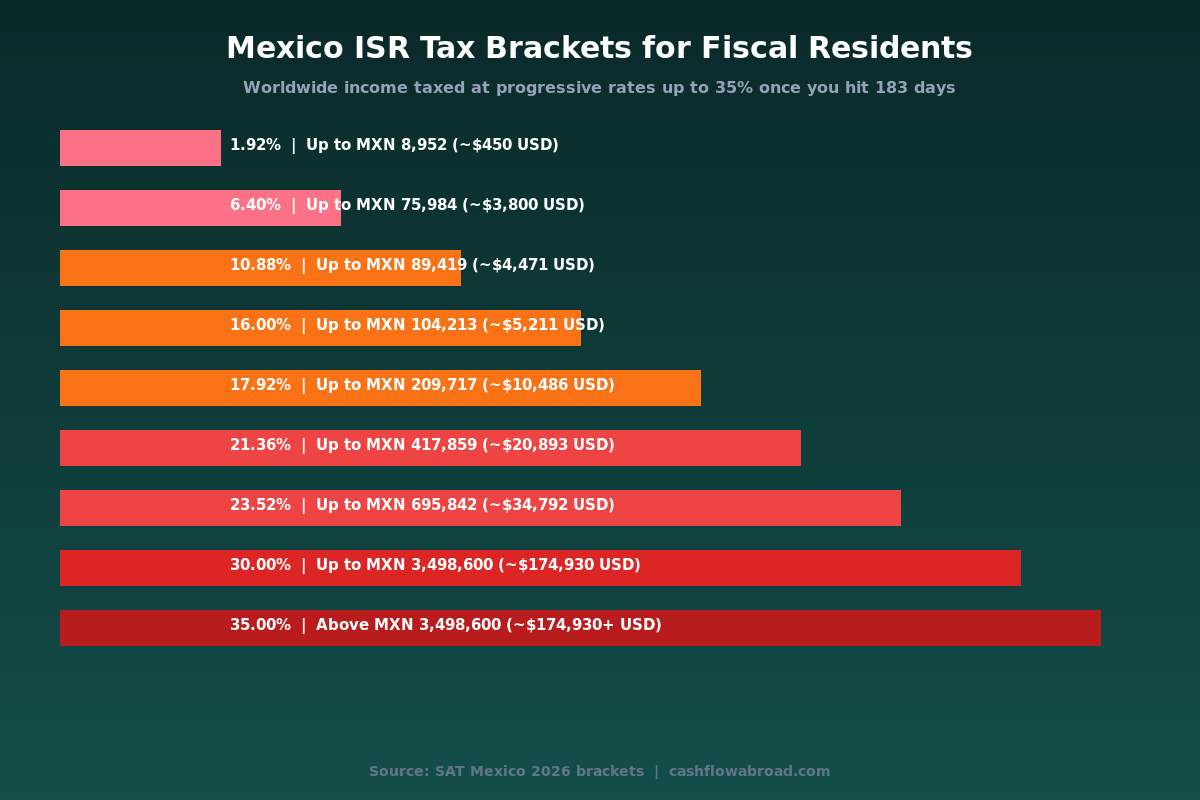

Once you cross the threshold, Mexico taxes your worldwide income under ISR's progressive brackets. Here's what the 2026 rate schedule looks like against real income scenarios:

| Annual Income (USD equiv.) | Mexico ISR Rate | US FEIE Coverage? | Net Double-Tax Risk |

|---|---|---|---|

| Under $4,500 | 1.92–6.40% | Yes (full exclusion) | Low |

| $4,500–$20,000 | 10.88–17.92% | Yes (full exclusion) | Moderate — ISR owed to Mexico |

| $50,000–$100,000 | ~21–23% | Partial (FEIE caps at $132,900) | High — FTC needed |

| Above $175,000 | 30–35% | Partial | Very High — specialist required |

At $80,000 of freelance income — a typical figure for a US remote worker relocating to Mexico City — you're looking at an effective ISR rate of roughly 21–23%. The Foreign Earned Income Exclusion (FEIE) lets you shield up to $132,900 from US taxes in 2026, but FEIE does nothing for what you owe to SAT. Mexico and the US each apply their own calculation to your worldwide income independently.

The FEIE Problem Nobody Talks About

Most expat tax advice treats the FEIE as the golden ticket: exclude foreign earned income from US taxes, live tax-free in a low-cost country, call it geographic arbitrage. That logic holds in territorial-tax countries like Panama or Paraguay. Mexico is different.

The US-Mexico Tax Treaty (signed 1992, updated 2003) provides credit relief under Article 24: you can claim a Foreign Tax Credit for taxes paid to the other country, preventing true double taxation on the same dollar. But the credit only offsets the US tax you owe — and if you're using FEIE to zero out your US tax liability, the FTC credit may provide limited benefit. You still pay ISR to Mexico.

The other silent landmine: there is no US-Mexico Totalization Agreement in force as of 2026. A bilateral agreement was signed in 2004 but has never been ratified by the US Senate. That means self-employed Americans in Mexico can owe both US self-employment tax (15.3% on net self-employment income) and Mexican IMSS contributions simultaneously. For a freelancer earning $70,000, that's a potential $10,700 in US SE tax that no treaty provision eliminates.

Who Gets Caught — and Who Doesn't (Yet)

SAT's enforcement is selective. The agency concentrates on Mexican-source income, domestic employers, and rental property. A remote worker earning in USD, banking abroad, and filing nothing in Mexico often operates under the radar for years. But "not yet caught" is a poor tax strategy.

Three situations dramatically increase your risk of SAT scrutiny:

- Opening a Mexican bank account. Banks report to SAT. Once you have an RFC and a Mexican account showing regular large deposits, the data trail exists.

- Owning Mexican property. Fideicomiso (trust) ownership triggers property registration, which links to SAT records and flags you as a long-term resident.

- Hiring locally. If you employ a Mexican housekeeper, assistant, or any IMSS-enrolled worker, you've created a paper trail of domestic economic activity.

Even without those triggers, the global push toward CARF and automatic tax data sharing means invisible expats are becoming visible. Mexico joined the Common Reporting Standard (CRS) framework; your foreign bank accounts increasingly get reported back to SAT once it identifies you as a resident.

The RFC Question: To Register or Not

The RFC (Registro Federal de Contribuyentes) is Mexico's taxpayer ID. You cannot open a Mexican business bank account, issue invoices, or file Mexican tax returns without one. Here's the paradox:

You cannot register for an RFC as a tourist — it requires legal residency status (Temporary or Permanent Resident card). But if you're legally resident long enough to qualify for an RFC, you've almost certainly crossed the 183-day fiscal residency threshold anyway.

The RFC is not what creates tax liability. Fiscal residency does. But obtaining an RFC is simultaneously acknowledgment that you're operating within Mexico's tax system and your entry point to compliant operation within it.

| Scenario | Visa Type | Days in Mexico | Fiscal Resident? | RFC Required? |

|---|---|---|---|---|

| Short-stay tourist | FMM Tourist | Under 183 | No | No |

| Long-stay tourist (accidental overstay) | FMM Tourist | 183+ | Technically Yes | Cannot get one — no residency card |

| Temporary resident, year 1 | Residente Temporal | 183+ | Yes | Yes — mandatory |

| Permanent resident | Residente Permanente | Any | Yes (presumed) | Yes — mandatory |

Four Practical Strategies to Stay Compliant

1. The 182-Day Calendar

The simplest solution for lifestyle expats who aren't trying to root in Mexico permanently: count your days rigorously and exit before day 183. This works for people who genuinely travel — a month in Colombia, a few weeks in Europe — but it's operationally demanding and increasingly hard to sustain as Mexico becomes "home."

Use a day-counting app (TaxBird or DaysAbroad both work well) and build exit trips into your schedule before September. Most calendar-year fiscal residency problems occur because people arrive in January, love CDMX, and don't count days until October.

2. Stack FEIE with the Foreign Tax Credit

If you become a Mexican fiscal resident, your US filing strategy matters significantly. For 2026, the FEIE excludes up to $132,900 of foreign earned income from US tax. For income above that amount, the Foreign Tax Credit (Form 1116) lets you offset US taxes with ISR already paid to Mexico.

Most CPAs recommend a hybrid approach: FEIE for the first $132,900, FTC for everything above. The math gets complex — ISR's 30-35% rate at high incomes often exceeds the US rate, generating excess FTC credits that carry forward 10 years. Get a CPA who files both US and Mexican returns. A specialist costs $800–$2,000 per year; an unexpected ISR assessment costs far more.

3. RESICO for Freelancers and Solopreneurs

If you're legally resident, actively earning, and want to operate compliantly, Mexico's RESICO (Régimen Simplificado de Confianza) is the most underused tool in the expat tax playbook. RESICO offers dramatically simplified rates of 1%–2.5% on gross monthly revenue for individuals earning up to MXN 3.5 million per year (~$175,000 USD).

Monthly payments are final — no annual return required. For a freelancer billing $8,000/month (~$96,000/year), RESICO means roughly $1,920–$2,400 in annual Mexican tax versus $18,000–$22,000 under standard ISR progressive brackets. The trade-off: you must be legally registered, obtain your RFC, and run all income through Mexico's formal invoicing system (facturas).

4. Maintain Your US Financial Infrastructure

Regardless of where you physically live, a legitimate US postal address is non-negotiable for IRS correspondence, banking continuity, and state domicile purposes. A service like Traveling Mailbox gives you a real US street address in 50+ cities with mail scanning and check deposits — starting at $15/month. It's the easiest way to prevent any disruption to your US banking while you sort out Mexican compliance.

For US banking abroad, Charles Schwab's international account remains the benchmark: no foreign transaction fees, unlimited ATM fee reimbursements worldwide, no minimum balance. Mexican banks charge foreign card fees of 3–5% per withdrawal; Schwab eliminates that entirely. For a full comparison, see our expat banking and tax guide.

Mexico's Cost of Living: The Real 2026 Numbers

Here's what a comfortable single-person expat life actually costs by city in 2026:

| City | Monthly Budget (USD) | 1BR Rent (USD) | YoY Rent Change |

|---|---|---|---|

| Mexico City (Roma/Condesa) | $1,800–$2,500 | $800–$1,400 | +9% |

| Mexico City (Narvarte/Del Valle) | $1,400–$1,900 | $450–$700 | +8% |

| Guadalajara | $1,200–$1,800 | $500–$900 | +12% |

| Mérida | $1,000–$1,500 | $400–$700 | +7% |

| Puerto Vallarta / Riviera Maya | $1,500–$2,200 | $600–$1,100 | +11% |

Rents across popular expat neighborhoods have climbed 8–12% year-over-year as of early 2026, driven by continued remote worker inflows and limited new supply in desirable areas. The $1,500/month life is increasingly concentrated in second-tier cities; Mexico City proper now runs $1,600–$2,200 for a comfortable setup. That rising baseline makes the tax picture more consequential — an unexpected $15,000–$20,000 ISR liability materially changes the geographic arbitrage math.

Moving Money Between Mexico and the US

Expats typically move money in both directions: USD salary into Mexican pesos for daily expenses, and savings back to US accounts. For international transfers, Remitly offers competitive USD-MXN exchange rates with low fees. For day-to-day peso withdrawals, Schwab's zero-fee ATM reimbursement covers any ATM worldwide.

One operational note: large inbound transfers to Mexican accounts trigger CNBV reporting. Transfers above MXN 15,000 (~$750) per month from a single source to a personal account are reported to SAT. This is a vector through which SAT can identify previously undisclosed fiscal residents — another reason to get ahead of compliance rather than hoping to stay invisible.

The Bottom Line

Mexico is still one of the best geographic arbitrage plays available — the cost savings are real, the infrastructure for remote work is genuinely good, and the quality of life is hard to replicate at the price. But it is not a tax-free destination. The 183-day rule is not obscure; it is actively enforced, and enforcement is becoming more systematic as CRS data sharing expands.

The expats who navigate Mexico well do four things: they count days deliberately, they work with a CPA who understands both US and Mexican tax law (not just one or the other), they maintain their US financial infrastructure, and they either commit to full compliance or commit to the 182-day calendar. What they don't do is assume that operating on a tourist visa makes them permanently invisible to SAT.

For a broader look at how US expat taxes interact with foreign residency, read our complete US expat banking and tax guide. And if you're weighing Mexico against other low-tax bases, our geographic arbitrage playbook breaks down 10 countries by tax structure, cost, and quality of life.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax or legal advice. Tax laws change frequently and individual situations vary significantly. Consult a qualified CPA or tax attorney with experience in both US and Mexican tax law before making decisions about fiscal residency, RFC registration, or ISR compliance. Cross-border tax situations are complex; the cost of professional guidance is almost always lower than the cost of non-compliance.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 31, 2026

Expat Tax & FinanceMay 31, 2026

The 183-Day Tax Rule: What Expats Get Wrong

Most expats misunderstand the 183-day tax rule. Learn how it actually works country by country and why it is irrelevant for US citizens abroad.

Expat Tax & FinanceJuly 16, 2026

Expat Tax & FinanceJuly 16, 2026

FBAR for US Expats: FinCEN 114 Rules, Deadlines & Penalties

Who files the FBAR, 2026 penalties up to $16,536/year, the July 2026 closure of the late-filing lane, and what to do if you have missed years.

Expat Tax & FinanceJuly 16, 2026

Expat Tax & FinanceJuly 16, 2026

UK Workplace Pension for US Citizens: The Hidden Tax Traps

UK employer pension contributions are taxable to US citizens as they vest. The 25% lump sum is fully taxable in the US. Know what to report and what