Malaysia MM2H: The $32K Visa That Cuts Your Tax Bill to Zero

10 min read · 2,425 words

Most Americans building their expat shortlist run straight to the usual suspects — Portugal, Panama, Colombia, Georgia. Malaysia rarely shows up. That’s a mistake. The country offers something almost no other jurisdiction on earth can match: a long-term residency visa, one of the lowest costs of living in Southeast Asia, a world-class private healthcare system, and a foreign income tax rate of exactly 0% — by law, until 2036.

The Malaysia My Second Home (MM2H) program has been running for over two decades. It’s been revised multiple times, but the 2025 overhaul brought structure: three clear tiers, a Special Economic Zone pathway that gets the entry cost down to $32,000 for applicants over 50, and a renewed government commitment to attracting foreign capital and retirees. This is one of the most underrated residency plays available today.

What Is Malaysia My Second Home?

MM2H is Malaysia’s long-term residency program for foreign nationals. It’s not citizenship — you don’t get a Malaysian passport — but it’s a renewable visa that lets you live in Malaysia indefinitely. Depending on the tier, you get a 5-, 10-, or 20-year renewable pass with the right to bring dependents, own property, and participate fully in Malaysian economic and social life.

The program has attracted over 50,000 participants from more than 130 countries since its launch. The top applicant countries have historically been China, Japan, South Korea, and the UK, with Americans increasingly entering the mix as word spreads about Malaysia’s favorable tax treatment for foreign-sourced income.

Unlike some residency-by-investment programs, MM2H doesn’t let you simply write a check and disappear. You must meet income requirements, place a fixed deposit with a Malaysian bank, and — under the newer rules — purchase qualifying property in Malaysia. The upside: you have a real base in a functional, modern country with excellent infrastructure.

The Zero Tax Angle That Changes Everything

Here’s the hook most coverage glosses over: Malaysia extended its exemption on foreign-sourced income through December 31, 2036. If you’re a tax resident in Malaysia and your income comes from outside the country — a US S-corp, freelance clients overseas, dividends from foreign investments, rental income from property back home — Malaysia does not tax it.

There’s a condition: the foreign income should have been taxed in the jurisdiction where it was earned. But for most US expats, this plays out simply: you’ve paid US taxes on domestic business income, you claim the Foreign Tax Credit, and Malaysia takes zero. For income already sheltered under the Foreign Earned Income Exclusion (FEIE), the calculus gets more nuanced, but the point stands — Malaysia’s effective rate on offshore earnings for MM2H participants can be 0%.

Compare this to the other popular Southeast Asian options. Thailand’s LTR visa taxes certain foreign remittances; the rules changed in 2023 and keep evolving. Vietnam taxes worldwide income for residents. Indonesia’s territorial system has exemptions but the residency process is complicated. Malaysia is the cleanest, most established foreign-income exemption in the region.

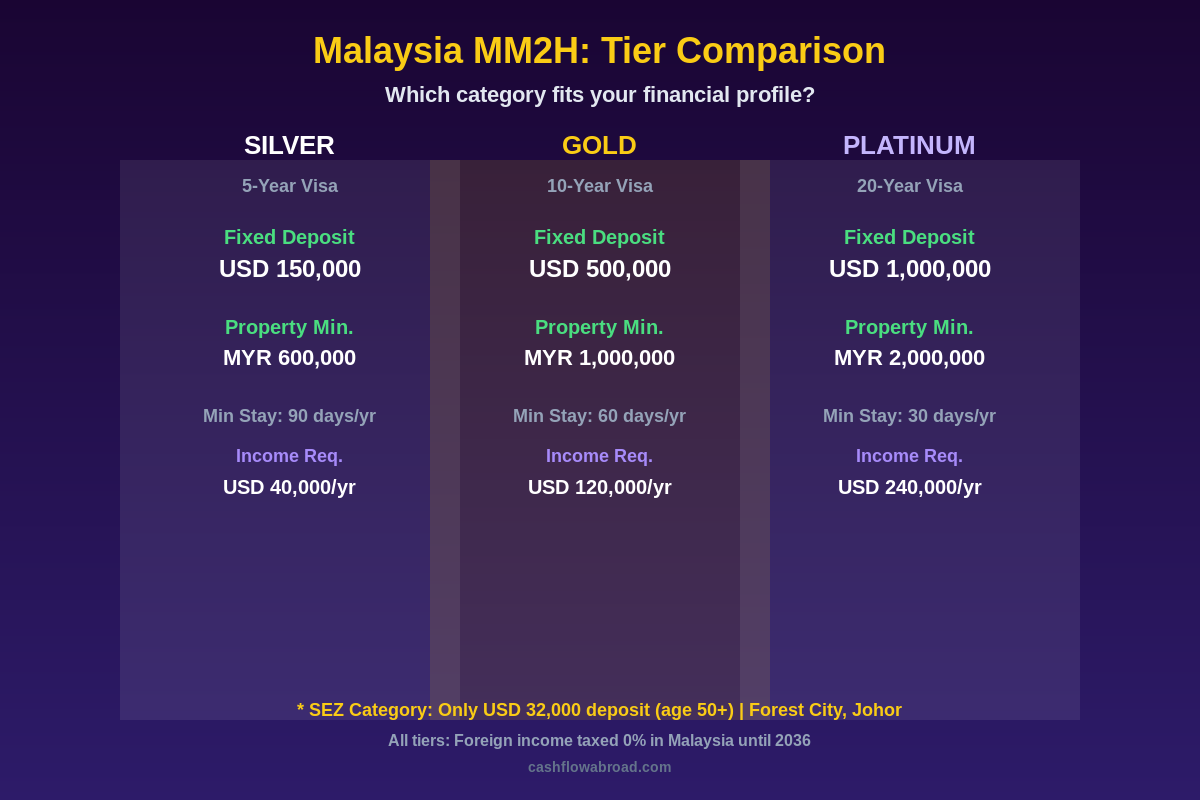

The Three Tiers: Silver, Gold, and Platinum

The 2025 restructuring replaced the old MM2H framework with three distinct tiers. Each requires a fixed deposit placed with a participating Malaysian bank, a minimum property purchase, and demonstrated offshore income.

| Category | Fixed Deposit | Property Min. | Income Req. | Min. Stay | Visa Term |

|---|---|---|---|---|---|

| Silver | USD 150,000 | MYR 600,000 (~$136K) | USD 40,000/yr | 90 days/yr | 5 years |

| Gold | USD 500,000 | MYR 1,000,000 (~$227K) | USD 120,000/yr | 60 days/yr | 10 years |

| Platinum | USD 1,000,000 | MYR 2,000,000 (~$454K) | USD 240,000/yr | 30 days/yr | 20 years |

| SEZ/SFZ | USD 32,000–65,000 | MYR 500,000 (~$114K) | Varies | Varies | 10 years |

Key insight on the fixed deposit: Malaysian banks currently pay roughly 3.5–4.2% interest on fixed-term deposits. On a $150,000 Silver deposit, that’s $5,250–$6,300 per year sitting in a Malaysian bank account — partially offsetting the cost of holding that capital. The deposit isn’t lost; it’s still yours, earning interest.

The SEZ Backdoor: Get In for $32,000

This is the detail that makes MM2H accessible to a much wider audience. The Special Economic Zone (SEZ) — also called the Special Financial Zone (SFZ) — was introduced in 2025 and is currently limited to Forest City in Johor, a massive development on Malaysia’s southern coast directly adjacent to Singapore.

The SEZ tier cuts the entry bar dramatically:

- Ages 21–49: USD $65,000 fixed deposit + MYR 500,000 property purchase

- Ages 50 and above: USD $32,000 fixed deposit + MYR 500,000 property purchase

- Visa term: 10 years, renewable

The catch is the location constraint — you must buy property in Forest City specifically, and purchases must be made directly from Forest City’s development companies. No secondary market, no loans, cash only. For buyers who want a turnkey condo in a Singapore-adjacent hub, this can actually make sense. For buyers who want to live primarily in Kuala Lumpur, it’s more of a paper requirement with a second property.

Forest City has been criticized for slow occupancy, but it’s grown substantially since 2022 and the proximity to Singapore — 30 minutes away — creates real value for anyone doing business in Singapore while wanting to live in a lower-cost environment. Condos in Forest City currently run MYR 300,000–600,000, well within the SEZ minimum property requirement.

What It Actually Costs to Live There

Malaysia’s cost advantage is real but varies significantly by city. Kuala Lumpur (KL) is the most popular choice for MM2H holders — English is the default language of business, the infrastructure rivals any developed country, and the food scene is genuinely extraordinary.

| Expense | Budget | Comfortable | Luxury |

|---|---|---|---|

| 1BR apartment (KL) | $450–550/mo | $600–750/mo | $900–1,400/mo |

| 2BR apartment (KL) | $700–800/mo | $850–1,000/mo | $1,200–2,000/mo |

| Groceries (1 person) | $90–120/mo | $150–200/mo | $250–350/mo |

| Dining out | $180–250/mo | $300–450/mo | $600–900/mo |

| Transport (Grab/public) | $50–80/mo | $100–150/mo | $200–400/mo |

| Health insurance | $80–120/mo | $150–250/mo | $300–500/mo |

| Total monthly | $850–1,100 | $1,400–1,800 | $2,500–4,000+ |

A single expat living comfortably in Kuala Lumpur — nice condo, regular dinners out, occasional weekend travel, private health insurance — can do it for $1,500–$1,800 per month. A couple in a 2BR in Mont Kiara or Bangsar (the primary expat neighborhoods) might spend $2,500–$3,200. At those numbers, geographic arbitrage pays for itself in under two years compared to most US cities.

Penang is the alternative for those who want a slower pace, lower costs, and arguably better food. A 1BR in Penang’s George Town runs $300–$400/month. Retirees love it; the island has the most developed English-speaking expat community outside of KL and a long history of attracting Western residents.

Healthcare: The Underrated Advantage

MM2H requires participants to carry private health insurance from a Malaysian provider — this isn’t optional. That requirement comes with a silver lining: Malaysia’s private hospital system is excellent, and prices are a fraction of what you’d pay in the US.

A private room at Gleneagles Kuala Lumpur or Pantai Hospital — both internationally accredited — runs $100–$200 per night. A specialist consultation is $30–$60. A cardiac bypass that costs $120,000 in the US? Around $8,000–$12,000 in KL. Malaysia consistently ranks among the top medical tourism destinations globally, attracting patients from Indonesia, Singapore, and increasingly the Middle East.

For international coverage that works across Asia with evacuation protection, SafetyWing’s Nomad Health plan is worth comparing against Malaysian local plans — particularly for those who travel frequently. Full options breakdown in our expat health insurance guide.

Banking and Moving Money

MM2H holders can open accounts at Malaysian banks — CIMB, Maybank, and Public Bank are the main choices. You’ll need your MM2H pass and proof of address. MYR fixed deposits are hitting 3.5–4.2%, and savings accounts earn 2.5–3.5% — decent by developed-country standards.

For your US-side banking, Charles Schwab’s international checking account remains the gold standard for expats: no foreign transaction fees, unlimited ATM fee rebates worldwide, and no minimum balance. Withdraw ringgit from any ATM in KL with zero fees — conversion happens at interbank rates.

When moving significant sums between US and Malaysian accounts, Remitly covers the Malaysia corridor with competitive rates and fast delivery, often same-day to MYR accounts. The spread on USD/MYR is thin compared to standard bank wire rates.

One critical piece of infrastructure for US expats: you need a US address for banking, IRS correspondence, and state domicile purposes. Traveling Mailbox gives you a real US street address in 50+ cities starting at $15/month, with mail scanning so you can manage everything from KL. Essential for keeping a US bank account or brokerage active while living abroad. Full breakdown in our virtual mailbox guide for expats.

Connectivity and Digital Infrastructure

Malaysia’s internet infrastructure is solid, particularly in KL and Penang. Fiber to the apartment is standard in most expat-grade condos — CelcomDigi and Maxis offer 1Gbps home fiber for under $35/month. Mobile data is cheap: an unlimited data SIM runs $10–$15/month.

For travel connectivity when you’re hopping to Bali, Bangkok, or Singapore, a Saily eSIM covers Southeast Asia without the hassle of buying a local SIM in each country. If you’re accessing US streaming or financial platforms that restrict based on Malaysian IP addresses, NordVPN runs cleanly in Malaysia without throttling.

Your US Tax Obligations Don’t Disappear

Clear-eyed disclosure: Malaysia’s zero tax on foreign income solves Malaysia’s side of the ledger. It does nothing for your US obligations. Americans owe US taxes on worldwide income regardless of where they live. Malaysia and the US have no income tax treaty (one of the notable gaps), so you can’t use Malaysian taxes paid to offset US liability the way you can in France or Germany.

The strategies that matter for US expats in Malaysia are the same ones that matter everywhere: the Foreign Earned Income Exclusion, the Foreign Tax Credit, and — if you’re running offshore business structures — careful PFIC and CFC compliance. Full breakdown in our US expat banking and taxes guide.

FBAR and FATCA reporting apply to your Malaysian bank accounts once balances exceed the filing thresholds. Track these from day one — the penalties for late filing are disproportionately severe.

Who Should Actually Do This?

MM2H isn’t for everyone. Here’s an honest breakdown of who gets the most value from it:

Strong candidates:

- Remote workers and digital entrepreneurs earning $60,000–$200,000 in offshore income who want a stable Asian base with a real 10-year visa and simple tax treatment

- Retirees on Social Security and investment income — your SS isn’t earned in Malaysia, your dividends aren’t earned in Malaysia; Malaysia doesn’t touch any of it under the exemption

- Singapore workers or business owners — the Johor corridor is booming; living in Forest City or Johor Bahru while working in Singapore is a legitimate arbitrage play given Singapore’s sky-high rents

- Medical tourists turning long-term — if you’re already going to KL for procedures, MM2H lets you stay and pay Malaysian rates indefinitely

Less suitable if:

- You want eventual citizenship — MM2H doesn’t lead to a Malaysian passport on its own

- You want to work locally for a Malaysian employer — MM2H generally prohibits local employment

- You’re unwilling to commit capital to a fixed deposit and property purchase — this isn’t a tourist visa, it’s a lifestyle commitment with real financial requirements

The Application Process

The MM2H process runs through Malaysia’s Ministry of Tourism, Arts and Culture (MOTAC). Simplified steps:

- Gather documents — valid passport (18+ months validity), police clearance from country of origin, bank statements showing the required income, private health insurance, medical report

- Apply through a licensed MM2H agent — MOTAC requires applications through registered agents; agent fees run MYR 3,000–5,000 ($680–$1,130 USD)

- Conditional approval — MOTAC typically processes in 90–120 days

- Place fixed deposit — 30 days after conditional approval to place the deposit at a participating bank

- Purchase qualifying property — within 6 months of conditional approval (or 6 months before endorsement for SEZ)

- Pass endorsement — your renewable visa gets stamped; the clock starts

Total government fees are modest — around MYR 5,000–8,000 ($1,100–$1,800) including visa fees, medical exams, and administrative costs. The real financial commitment is the fixed deposit and property.

What the Brochures Leave Out

Property purchase is mandatory and illiquid. Unlike the old MM2H where property was optional, the new framework requires you to buy. If you buy in KL, the MYR 600,000 minimum for Silver (~$136K) buys a decent but not lavish condo. The Malaysian property market has been flat to modestly appreciating — don’t go in expecting a real estate windfall.

The foreign income exemption has conditions. Malaysia’s 2024 budget reaffirmed the exemption to 2036, but it requires that the income was taxed at source. If you’re earning from a 0%-tax jurisdiction — say, a Dubai-based company that pays no corporate tax — Malaysia’s exemption may not apply cleanly. Get a local tax attorney to sign off on your specific structure before committing.

The ringgit is volatile. MYR has weakened against the dollar over the past decade, which is good for dollar earners converting to ringgit — your money goes further. But it also means your MYR-denominated fixed deposit and property lose dollar value when the ringgit weakens. Factor currency risk into your planning.

MM2H holders can’t vote, can’t access public healthcare subsidies, and can’t own agricultural land. Standard limitations for long-term residents who aren’t citizens.

The Geographic Advantage

Kuala Lumpur is a genuinely underrated global city. The Petronas Twin Towers anchor a business district packed with co-working spaces, investment banks, and multinational headquarters. The food culture is exceptional: Malay, Chinese, and Indian cuisines interlace in hawker centers where a full meal costs $2–$4. The city has excellent international schools, world-class malls, and a surprisingly vibrant arts scene.

From KL: Singapore is 5 hours by car or 40 minutes by plane. Bangkok is 2 hours. Bali is 2.5 hours. Tokyo is 7 hours. You’re within a 3-hour flight of 2 billion people in one of the fastest-growing economic regions on earth — relevant if your income depends on Asian clients, contacts, or business exposure.

For a broader look at how Malaysia stacks up against other destinations offering cost-of-living leverage, check the geographic arbitrage playbook and our ranked guide to digital nomad visas.

Bottom Line

Malaysia MM2H is one of the most structurally sound expat residency programs available. The foreign income tax exemption is real, documented, and extended to 2036. The cost of living makes $2,000/month feel like $5,000. The infrastructure works. The healthcare is excellent and affordable. And the SEZ pathway gets you in for $32,000 if you’re over 50, making it accessible to a demographic that has traditionally had fewer low-friction options for legally restructuring their tax burden abroad.

The tradeoffs are real: you’re committing capital to a fixed deposit and property, your US tax obligations don’t change, and local employment is restricted. For retirees, remote workers, and business owners who’ve already optimized their US tax profile, those tradeoffs are easy to accept. If you’re doing serious due diligence on Southeast Asia, Malaysia should be near the top of your list.

Financial disclaimer: This article is for informational and educational purposes only. It does not constitute tax, legal, immigration, or financial advice. Tax laws and visa regulations change frequently. Consult a qualified tax attorney, CPA, and immigration specialist licensed in the relevant jurisdictions before making any residency or financial decisions. Exchange rates and program requirements cited reflect conditions as of the time of writing and may have changed.

Liked this article?

Get the next one delivered straight to your inbox — plus a free Expat Tax Cheat Sheet.

Join our subscribers. No spam — just expat finance intel and new post notifications.