Ecuador's Dollar Advantage: The Expat's Best-Kept Secret

Ecuador runs on the US dollar — no currency risk, no conversion fees. Visa from $482/month. $25 doctor visits. $1,400/month lifestyle. Full US expat guide.

Ecuador runs on the US dollar — zero currency risk. Visa from $482/month, $25 doctor visits, $1,400/month lifestyle. The complete US expat guide.

Most expats moving abroad spend weeks building currency-risk spreadsheets. Modeling peso devaluations, hedging against inflation, timing wire transfers. In Ecuador, that spreadsheet has exactly zero rows. The country has run on the US dollar since January 9, 2000 — and 26 years later, your Social Security check, investment dividends, and freelance income all land in the same currency you spend at the supermarket.

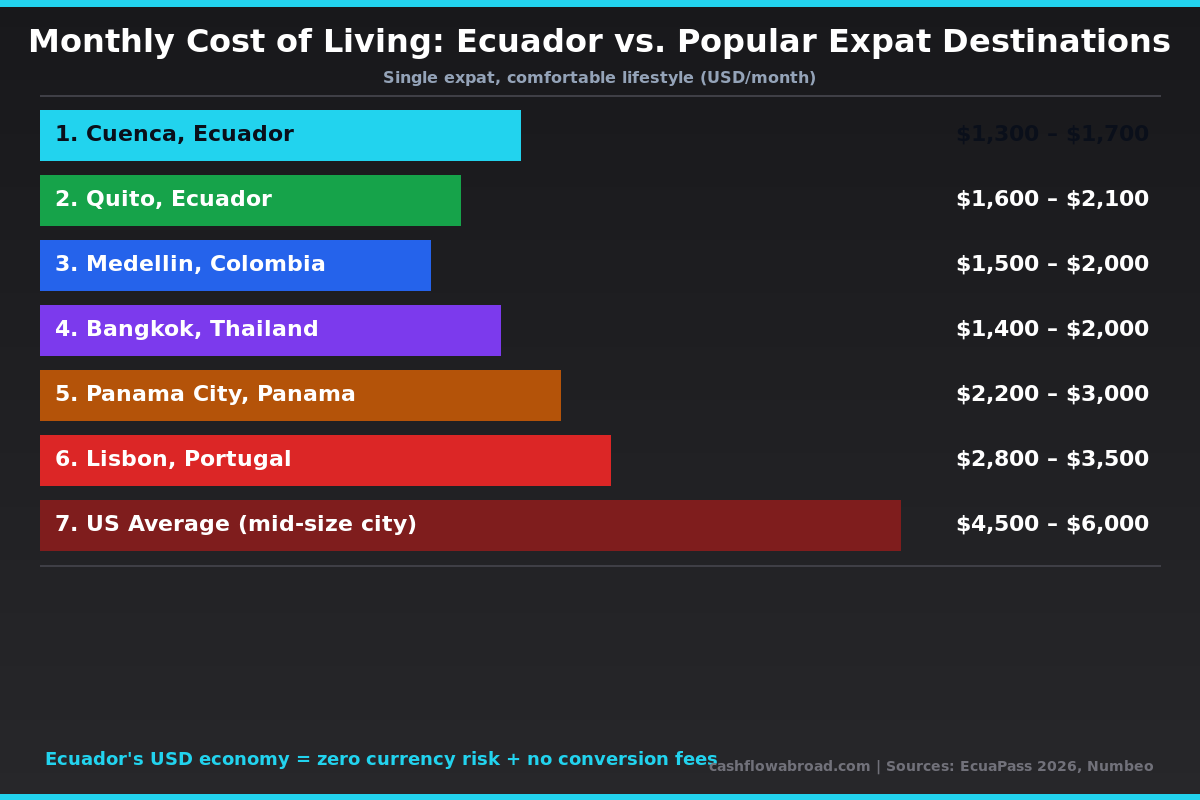

That single fact puts Ecuador in a category no other low-cost Latin American country occupies. Panama also uses dollars, but costs more. The rest of the region forces you to live inside a currency that may halve in purchasing power overnight. Ecuador doesn't. And because the cost of living in Cuenca — its most popular expat city — runs $1,300 to $1,800 per month for a comfortable single lifestyle, the arithmetic gets very interesting very fast.

Here's what most expat guides bury: Ecuador quietly changed its tax rules in late 2021, and understanding that change is the difference between a brilliant relocation and an expensive surprise from the SRI.

The Dollar Advantage Nobody Talks About

Dollarization isn't just convenient — it's structurally different from other expat plays. When you retire to Mexico or Colombia, every time the peso weakens, your dollar-converted income buys more. When it strengthens, you feel the squeeze. Your monthly budget becomes a variable you can't control.

In Ecuador, there's no conversion. Your US bank wires dollars. You withdraw dollars. You pay rent in dollars. The US Social Security Administration's International Direct Deposit program sends payments directly into approved Ecuadorian banks — no conversion fee, no middleman skimming 1.5% off the top. A retiree receiving $2,200/month in Social Security lands $2,200 in their Ecuadorian account, not $2,134 after forex costs.

For remote workers, the math is similarly clean. Client invoices in USD, expenses in USD. No mental overhead, no currency app on your phone, no checking exchange rates before buying a couch. After a few weeks, you genuinely stop thinking about it — and that cognitive relief compounds over a decade of expat life in a way that most relocation guides never quantify.

Ecuador Cost of Living: Real Numbers

The most popular expat city is Cuenca, a 500-year-old colonial city at 8,400 feet elevation with spring-like weather year-round (65–72°F average). It consistently ranks among the cheapest comfortable cities in the Western Hemisphere for USD earners.

| Expense Category | Cuenca (Budget) | Cuenca (Comfortable) | Quito |

|---|---|---|---|

| 1BR apartment (central) | $350–$450 | $550–$800 | $600–$1,000 |

| Utilities (electricity, water, internet) | $60–$80 | $80–$120 | $90–$140 |

| Groceries (1 person/month) | $150–$200 | $200–$300 | $220–$350 |

| Eating out (1 person/month) | $100–$150 | $200–$350 | $250–$400 |

| Healthcare (private insurance) | $85 (IESS public) | $120–$200 | $150–$250 |

| Transport | $30–$50 | $60–$120 | $80–$150 |

| Monthly Total (single expat) | $775–$1,010 | $1,290–$1,890 | $1,490–$2,290 |

Quito runs 20–30% more expensive than Cuenca and sits higher (9,350 feet vs. Cuenca's 8,400), which new arrivals notice in their lungs the first week. Manta, on the Pacific coast, is warmer and costs roughly the same as Cuenca — popular with retirees who want beach access without Bali prices or Southeast Asia visa complications.

For geographic arbitrage context, see the full geographic arbitrage playbook comparing 10 countries — Ecuador stacks up well on currency-risk-adjusted purchasing power, which is where most comparisons go wrong.

Visa Options: Your Path to Legal Residency

Ecuador overhauled its visa system and released updated 2026 income thresholds tied to its Unified Basic Salary ($482/month). Every route leads to the same destination: temporary residency first, permanent residency after 21 months, citizenship eligibility after 3 more years.

| Visa Type | Income or Investment Requirement | Government Fees | Who Qualifies |

|---|---|---|---|

| Professional Visa | $482/month + any bachelor's degree | $50 apply + $270 approve | Remote workers, graduates |

| Digital Nomad Visa | $1,446/month (foreign-sourced income) | $50 apply + $400 issue | Freelancers, remote employees |

| Retirement Visa | $1,446/month pension or Social Security | $50 apply + $270 approve ($135 if 65+) | Retirees with fixed income |

| Investor Visa | $48,200 (real estate, bank CD, or company equity) | $50 apply + $270 approve | Property buyers, capital investors |

The Professional Visa is the sleeper option most guides ignore. If you have any bachelor's degree — in any field, from any accredited university — and earn at least $482/month from foreign clients, you qualify for a 2-year renewable residency. That's the lowest income bar of any formal residency visa in Latin America.

The Investor Visa at $48,200 is smarter than it looks: place that money in an Ecuadorian bank CD earning 7–9% annual interest ($3,374–$4,338/year) and your deposit works while your 21-month residency clock runs simultaneously. Total government fees: under $400. Your investment keeps earning returns rather than sitting dormant as a locked government deposit.

The 2021 Tax Rule That Changed Everything

Here's the section most "Ecuador is a tax haven!" articles skip: Ecuador was a territorial tax country until November 2021. Only income earned inside Ecuador was taxed. Then the COVID fiscal recovery law — Ley Orgánica para el Desarrollo Económico y Sostenibilidad Fiscal — changed the framework. Ecuador now taxes residents on worldwide income.

The definition of "resident" for Ecuadorian tax purposes: spending more than 183 days in Ecuador in any rolling 12-month period. If you hit that threshold, Ecuador treats your global income — US dividends, foreign rental income, remote consulting earnings — as taxable at progressive rates from 0% (on the first $12,081) up to 37% (on income above $108,810).

If you spend fewer than 183 days/year in Ecuador, you're classified as a non-resident for Ecuadorian tax purposes. Non-residents pay a flat 25% withholding only on Ecuador-sourced income — nothing on US or third-country income. Some expats deliberately structured their first year or two around sub-183-day stays before deciding to commit.

The practical reality for full-time residents: Ecuador's progressive rates are manageable when combined with US tax tools — particularly because there is no US-Ecuador tax treaty, which changes which weapons you deploy. More on that next.

Your US Tax Obligations Don't Disappear

The US taxes citizens on worldwide income regardless of where they live. Moving to Ecuador changes the composition of your taxes but not the obligation to file. What it gives you are two powerful levers:

Foreign Earned Income Exclusion (FEIE): If you qualify under the Physical Presence Test (330 full days outside the US in a 12-month period) or the Bona Fide Residence Test, you can exclude up to $132,900 of foreign earned income from US federal taxes in 2026. This applies to wages and self-employment income — not passive income like dividends or pension distributions. See the complete FEIE guide for how the physical presence test actually works in practice.

Foreign Tax Credit (FTC): For any income taxes you pay to Ecuador, you can claim a dollar-for-dollar credit against your US tax liability. No treaty required — the FTC works unilaterally. It covers earned and passive income, making it the primary shield against double taxation once you're a full Ecuadorian tax resident. See the FEIE vs. Foreign Tax Credit breakdown for when to use each and when to layer both.

Practical example: remote worker earning $90,000/year. FEIE eliminates US federal tax on up to $132,900 of that earned income. Ecuador taxes the same $90,000 at its progressive rates — rough resident liability around $14,000–$16,000 depending on deductions. The FTC covers that Ecuadorian tax against any residual US federal liability. Net result: total tax significantly below what a US-based earner would pay, with no currency risk on purchasing power.

FBAR and FATCA filings still apply. Any Ecuadorian bank account exceeding $10,000 in aggregate at any point during the calendar year requires FinCEN 114 reporting. Accounts above $50,000 trigger FATCA Form 8938. These are reporting requirements, not additional taxes — but the penalties for non-filing start at $10,000 per account per year. The US expat banking and taxes guide covers the full compliance stack.

For maintaining a real US street address while living in Ecuador — for IRS correspondence, state domicile management, and US banking requirements — Traveling Mailbox provides a physical US address in 50+ cities, digitizes incoming mail, and handles check deposits for $15/month. The virtual mailbox guide covers setup and state domicile strategy.

Healthcare: $25 Doctor Visits and $85/Month Insurance

Ecuador runs one of the most underrated healthcare systems for expats in Latin America. The price differential versus US care is so large it sounds exaggerated until you experience it:

- GP consultation (private clinic): $25–$40

- Specialist visit: $40–$80

- MRI scan: $200–$400 (vs. $1,500–$3,000+ in the US)

- IESS public health insurance: approximately $85/month with no pre-existing condition exclusions

Legal residents can enroll in IESS (Instituto Ecuatoriano de Seguridad Social) — Ecuador's public health system — for around $85/month. It covers hospitalizations, surgeries, specialist care, and prescriptions. Quality varies by city and clinic, but for routine care it's solid. Most expats layer IESS with a private supplement or carry international evacuation coverage for emergencies.

SafetyWing is the standard flexible option for nomads and expats — plans covering international medical emergencies start around $40–$80/month depending on age and home country. The full expat health insurance guide walks through how to layer IESS, private Ecuadorian plans, and international coverage for complete protection.

Banking and Moving Money

Since everything in Ecuador is already USD, wire transfers from your US account skip the conversion step entirely. Your bank still charges a wire fee ($25–$45 at most US banks), but services like Remitly significantly reduce that cost for regular US-to-Ecuador transfers. For a full breakdown of what international transfers actually cost, see the expat money transfer guide.

Banco Pichincha and Produbanco are the two largest private banks with decent ATM networks and online banking portals. Opening an account requires your cedula (local ID issued once residency is approved). Most branches in Cuenca and Quito have English-speaking staff familiar with expat onboarding.

For your main US banking infrastructure, Charles Schwab International is the expat gold standard — zero foreign ATM fees worldwide, no monthly minimums, and no account closure threats for clients with foreign addresses. Most US brokerages eventually terminate accounts of clients living abroad; Schwab explicitly supports expat clients and reimburses all foreign ATM fees. For alternatives, see the expat brokerage guide.

If you manage stablecoin balances or want dollar-denominated investment tools across Latin America, ARQ Finance holds USDc/EURc balances, swaps to local currencies (MXN, COP, ARS, BRL), and earns up to 4% on dollar balances — useful for a multi-country financial setup.

Best Cities for US Expats

Cuenca is the default choice and for good reason. Colonial architecture, a UNESCO World Heritage historic district, a large English-speaking expat community (estimated 5,000–8,000 Americans), and the lowest costs in the country. Year-round spring climate at 65–72°F. The altitude (8,400 ft) takes a week or two to adjust to but is manageable for most healthy adults.

Quito offers more: more international flights (direct to Miami, JFK, Houston, Amsterdam), a larger economy, more urban amenities. Costs run 20–30% above Cuenca. The altitude at 9,350 feet is harder on newcomers and on cardiovascular conditions. If your income requires regular travel or client meetings, Quito's connectivity advantage is real.

Manta sits on the Pacific coast, warmer and lower-altitude, with costs comparable to Cuenca. Direct flights to Panama City and Lima. Growing expat community, especially among retirees who want beach access without the visa complexity of Southeast Asia or the cost of Costa Rica's coastal towns.

Loja in the southern highlands is cheaper than Cuenca by 15–20% with a growing university presence and a quieter pace. Less developed expat infrastructure but exceptional value for those who don't need a large English-speaking community around them.

The Verdict on Ecuador

Ecuador's dollar economy isn't just a convenience — it's a structural advantage that compounds over years. No currency hedging, no conversion friction, no watching exchange rates before major purchases. Your Social Security, pension, or remote income arrives in your Ecuadorian account exactly as it left the US.

The 2021 tax change means Ecuador isn't a zero-tax play for full-time residents anymore. But between the FEIE (eliminating up to $132,900 of earned income from US tax), the Foreign Tax Credit (covering Ecuadorian tax dollar-for-dollar against US liability), and Ecuador's own 0% band on the first $12,081 of income, the effective burden is manageable for most income profiles.

The Investor Visa at $48,200 placed in a 7–9% CD may be the cleanest setup available: your deposit earns real returns, your 21-month residency clock starts, and you get permanent residency without proving monthly income or owning a business. Total government fees: under $400. For a full relocation checklist covering documentation, banking setup, and state domicile, the Relocation Kit covers the full Ecuador move process. For a broader comparison including countries that still operate on territorial taxation, the geographic arbitrage playbook ranks 10 destinations across tax, cost, and residency access.

This article is for informational purposes only and does not constitute tax, legal, or immigration advice. Ecuador's tax rules changed in November 2021 and may continue to evolve — confirm the current 183-day residency threshold and applicable rates with a qualified cross-border tax professional before making any relocation decisions. FEIE and FTC rules are US federal tax provisions; state tax obligations may vary. Affiliate links in this post may earn a commission at no additional cost to you.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJune 6, 2026

Geographic ArbitrageJune 6, 2026

Vienna Expat Guide: RWR Card, Taxes, and Living Costs

Vienna ranks #1 in livability. Complete guide to Austria's Red-White-Red Card, the 30% expat tax deduction, income brackets, and real monthly living

Geographic ArbitrageMay 28, 2026

Geographic ArbitrageMay 28, 2026

Vietnam Expat Guide: $1,200/Month, Zero Foreign Tax

Vietnam costs ~$1,200/month for a comfortable expat life and taxes foreign income at 0% if you stay under 183 days. Complete guide for US expats.

Geographic ArbitrageMay 28, 2026

Geographic ArbitrageMay 28, 2026

Panama Residency: Live on $2,000/Month, Zero Local Tax

Panama taxes zero on foreign income and runs on the US dollar. Full guide to visas, costs, banking, and Pensionado discounts for expats.