Cambodia Expat Guide: Dollar Economy, $800/Month, No Foreign Tax

Cambodia runs on US dollars, costs under $1,200/month, and taxes zero foreign income. Here's the full expat guide with real numbers and IRS obligations.

Cambodia uses US dollars, costs under $1,200/month, and exempts foreign income from local tax. Full guide for US expats with real numbers and IRS rules.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Cambodia is the only country in Southeast Asia where you can buy street food, pay rent, tip a tuk-tuk driver, and wire money to your US account — all without touching foreign currency. The US dollar is Cambodia's de facto official currency. No conversion fees, no exchange rate math, no watching the daily rate on your phone. You just live in dollars.

That alone makes Cambodia unusual. But combine it with a territorial tax system (foreign-sourced income is untaxed locally), sub-$1,200/month living costs in the capital, and visa rules so relaxed that Americans have been renewing the same business visa for over a decade — and you start to understand why Cambodia flies under the radar while everyone else argues about Bali and Chiang Mai.

This guide covers the real numbers, the IRS situation, and the things the "top expat destinations" listicles never mention.

Why Cambodia Actually Works for US Expats

Most Southeast Asian expat destinations come with a hidden tax: currency volatility. The Thai baht, Vietnamese dong, and Indonesian rupiah all fluctuate — sometimes significantly — against the dollar. Your purchasing power can shift 10–15% in a year without you changing a single habit.

Cambodia solved this by accident of history. After decades of economic instability following the Khmer Rouge era, Cambodians lost confidence in the riel and spontaneously dollarized the economy. Today, the US dollar accounts for an estimated 80–90% of all financial transactions in Phnom Penh. Rent is quoted in dollars. Salaries are paid in dollars. Even most ATMs dispense dollars. The riel exists mainly for small change (anything under $1).

For a US expat, this is strikingly convenient. There's no "I got burned on the exchange rate" story here.

Cambodia's Territorial Tax: Zero on Foreign Income

Cambodia taxes residents only on Cambodia-sourced income. If your employer, clients, or investments are based outside Cambodia, that income is completely outside the Cambodian tax authority's reach — regardless of whether you've been in-country for 30 days or 300.

The tax residency threshold is the standard 182-day rule. Spend more than 182 days in Cambodia in a calendar year, and you're technically a Cambodian tax resident. But since territorial taxation applies, this doesn't change much for remote workers or those with purely foreign income. Cambodia has no mechanism to tax what flows in from abroad.

Cambodia's progressive income tax rates on locally-sourced income run from 0% on the first approximately $1,250/month to 20% above roughly $3,125/month. For digital nomads and remote employees whose income originates outside Cambodia, these rates are irrelevant.

Important: No Cambodia-US Tax Treaty

Cambodia and the United States have no bilateral tax treaty. There's also no totalization agreement, meaning self-employed Americans in Cambodia cannot escape US self-employment tax (15.3% on the first ~$168,600 of net self-employment income in 2025) the way they could in treaty countries like the UK or Germany.

This is one of Cambodia's real hidden costs for self-employed expats. If you're freelancing or running a solo business while in Cambodia, factor in that SE tax — it's payable regardless of the FEIE or Foreign Tax Credit.

Your IRS Obligations Don't Vanish

The US taxes citizens on worldwide income, full stop. Cambodia's territorial system protects you from Cambodian taxes on foreign income. It does nothing about the IRS.

The primary tool for US expats is the Foreign Earned Income Exclusion (FEIE), which allows you to exclude up to $130,000 of foreign earned income from US federal income tax in 2025 (the amount adjusts for inflation annually). To claim it, you must pass either the Bona Fide Residence Test or the Physical Presence Test (330 days outside the US in any 12-month period).

What FEIE does NOT cover: passive income. Dividends, rental income, capital gains, and interest remain fully taxable by the IRS at standard rates, regardless of where you live. A remote employee or freelancer under $130K/year may owe zero US federal income tax. An investor with significant portfolio income still faces a full US tax bill.

For more on stacking the FEIE correctly, see our zero federal income tax expat guide.

FBAR and FATCA: Still Required

If your Cambodian bank account balance exceeds $10,000 at any point during the year, you must file FinCEN 114 (FBAR) by April 15, with automatic extension to October 15. FATCA reporting thresholds apply if aggregate foreign financial assets exceed $200,000 abroad (or $50,000 if filing while in the US).

The good news: Cambodia's major banks — ABA Bank, ACLEDA, and Canadia Bank — are FATCA-compliant and report US account holders to the IRS. Opening accounts as a US citizen is generally straightforward, unlike in many European countries where FATCA compliance is used as an excuse to deny Americans accounts entirely.

For the full FBAR/FATCA framework, read our US expat banking and taxes guide.

Visa Options for Americans

Cambodia's visa situation is refreshingly uncomplicated compared to most expat destinations.

| Visa Type | Duration | Cost | Renewability | Work Permitted? |

|---|---|---|---|---|

| e-Visa (Tourist) | 30 days | $37 ($30 + $7 processing) | One extension to 30 days | No |

| Business Visa (EB/EG) | 30 days on arrival, extendable | $35 on arrival + extension fees | Indefinitely — 1 or 12 months at a time | De facto yes |

| Retirement Visa (ER) | 12 months | ~$290–$300/year | Indefinitely | No |

| Ordinary Residence | Ongoing | Requires investment or employment | Annual renewal | Yes |

The Business Visa (EB or EG) is what most long-term expats use. It requires no proof of employment or business registration — just a passport, $35, and a local "sponsor" (typically handled by the guesthouse, apartment complex, or a visa agent for a small fee). Extensions of 1 month, 3 months, 6 months, or 12 months are available and routinely renewed. Many expats have maintained the same business visa for 5+ years without issue.

The Retirement Visa (ER) requires you to be 55 or older. There's no minimum income or asset threshold in law, though immigration may ask for evidence you can support yourself. At approximately $290–$300/year, it's one of the cheapest official long-stay options in Asia.

Cambodia has no digital nomad visa category. The business visa effectively fills that role.

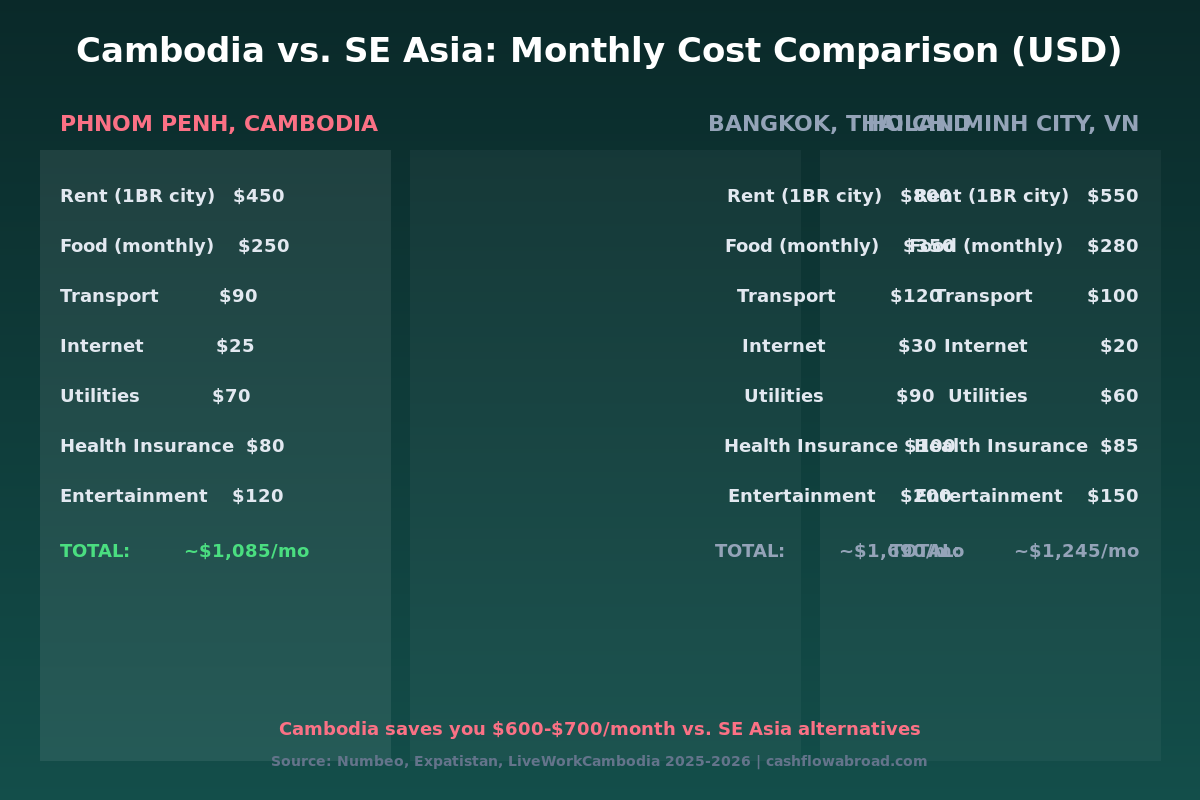

Real Monthly Costs in Phnom Penh

Here's what a realistic single-person budget looks like in Phnom Penh's main expat neighborhoods (BKK1, Tonle Bassac, Daun Penh):

| Expense | Budget Tier | Mid-Range Tier | Comfortable Tier |

|---|---|---|---|

| 1BR Apartment | $270–$350 | $400–$550 | $600–$900 |

| Food (groceries + dining) | $150–$200 | $250–$350 | $400–$600 |

| Transportation | $50–$80 | $90–$150 | $150–$300 |

| Utilities + Internet | $50–$70 | $70–$100 | $100–$130 |

| Health Insurance | $50–$80 | $80–$130 | $150–$200 |

| Leisure & Social | $80–$120 | $150–$250 | $300–$500 |

| Monthly Total | $650–$900 | $1,040–$1,530 | $1,700–$2,630 |

Street food — banh mi, fried rice, noodle soups — runs $1–$3 per meal. A sit-down local restaurant meal is $3–$6. Western restaurant meals cost $8–$15. A cold local beer in a bar is $1–$2. Internet at $15–$25/month gets you fiber speeds across the BKK1 neighborhood. Tuk-tuk rides within Phnom Penh run $1–$3; motorbike rentals for those who want independent mobility run $80–$150/month.

Siem Reap (home to Angkor Wat) and the beach town of Kampot run 20–35% cheaper than Phnom Penh on comparable amenities. Many expats use Phnom Penh as a base and make weekend trips to both.

Compare this to neighboring capitals: Bangkok mid-range runs approximately $1,690/month, Ho Chi Minh City approximately $1,245/month. Phnom Penh delivers comparable infrastructure and an active expat scene at a meaningful discount — and in dollars the whole way through.

Banking in Cambodia as a US Citizen

Opening a local bank account in Cambodia is one of the easier processes in Southeast Asia. Unlike in Europe — where FATCA compliance is routinely used as grounds to refuse American customers — Cambodian banks actively court foreign depositors.

ABA Bank is the most popular choice among expats and digital nomads. Its mobile app is well-designed, supports fast international transfers, and processes incoming SWIFT wires efficiently. ACLEDA and Canadia Bank are solid alternatives with nationwide branch networks. You'll typically need your passport, visa, and a local address to open an account — some accounts open in under an hour.

For your US banking needs, Charles Schwab's international checking account remains the gold standard for expats — it refunds all ATM fees worldwide with no foreign transaction fees, making it ideal for withdrawing dollars from Cambodian ATMs. Cambodia's ATMs widely dispense USD.

For maintaining a US business address and receiving IRS mail while abroad, a virtual mailbox like Traveling Mailbox gives you a real US street address in 50+ cities with mail scanning and check deposit — essential for keeping your banking, IRS correspondence, and state domicile intact from Phnom Penh.

For international money transfers — sending dollars from Cambodia to the US or paying US bills — Remitly typically offers competitive rates and fast delivery times on USD corridors.

Healthcare: What Expats Actually Need

Cambodia's public hospital system is basic — limited resources, chronic underfunding. Expats use private hospitals exclusively.

Phnom Penh's private sector is decent for routine care. Royal Phnom Penh Hospital — affiliated with Bangkok Dusit Medical Services — offers English-speaking staff, modern imaging, and direct insurance billing. A general consultation runs $60; add a blood panel and CT scan and you're looking at $120–$200. Sunrise Japan Hospital is Singaporean-managed and strong on specialist care.

The caveat: Cambodia is not where you want to be for complex surgery, cancer treatment, or cardiac emergencies. Medical evacuation to Bangkok (a one-hour flight) is standard practice for serious conditions — Bumrungrad and Samitivej hospitals handle most regional evacuations. This makes evacuation coverage non-negotiable.

SafetyWing's Nomad Insurance starts at approximately $56/month for adults under 40 and includes emergency evacuation coverage — workable for healthy expats on a budget. Comprehensive international plans with higher annual limits run $80–$200/month depending on age and coverage tier.

For a full framework on comparing international health plans, see our expat health insurance guide.

Connectivity for Remote Workers

Phnom Penh's fiber internet infrastructure has improved substantially. Speeds of 100–200 Mbps are standard in modern apartments and most coworking spaces at $15–$30/month. Mobile data is cheap — local SIMs from Cellcard or Smart offer 30-day packages for $5–$10. Coverage is reliable in Phnom Penh and Siem Reap; expect spottier service in rural areas.

For short-term stays or while getting a local SIM sorted, Saily eSIM provides immediate data coverage in Cambodia without a physical SIM card swap. A VPN like NordVPN is standard practice for accessing US streaming services, US banking portals that block foreign IPs, and general privacy on shared networks.

The Honest Downsides

Cambodia doesn't get the same expat press as Bali or Bangkok partly because it has real friction points other countries don't.

Visa insecurity. The business visa system operates on informal rules. There's nothing explicitly illegal about a remote worker holding one, but there's also no legal framework protecting it. Policy can shift without notice. Most long-term Cambodia expats accept this as a calculated risk and keep contingency plans.

Air quality. Phnom Penh ranks among the more polluted Asian capitals, particularly during dry season (November–April) when agricultural burning worsens particulate levels. Not a dealbreaker but worth factoring in if you have respiratory issues.

US account friction. Some US banks close accounts or flag transactions when they detect long-term foreign residency. Having a robust US setup before you leave — Schwab, a maintained credit card, a virtual mailbox — prevents the most common account closure scenarios.

No retirement account contributions from excluded income. If the FEIE excludes all your earned income, you'll have $0 of earned income for Roth IRA contribution purposes. Self-employed expats using a Solo 401(k) have more flexibility here. See our expat investing playbook for details.

Self-employment tax still applies. Without a US-Cambodia totalization agreement, self-employed Americans pay full 15.3% SE tax on net earnings. No treaty exemption exists.

Who Cambodia Is (and Isn't) For

Cambodia makes the most sense for:

- Remote employees and freelancers earning under $130K/year in foreign-sourced income — FEIE can zero out US federal income tax while Cambodia's territorial system zeros out local tax

- Retirees 55+ on fixed income who want Southeast Asia's dollar economy without Thailand's complexity or Vietnam's bureaucracy

- Geographic arbitrage practitioners maximizing the gap between a US-dollar income and local spending — the math at $800–$1,200/month all-in is compelling

- First-time expats who want a forgiving, low-bureaucracy entry point before moving to a more complex jurisdiction

It's a harder fit for high earners with significant passive income, those needing specialized medical care, or expats who need ironclad legal residency. For a broader geographic arbitrage framework across 10 countries with different cost-tax profiles, see our geographic arbitrage playbook.

Bottom Line

Cambodia is quietly one of the most financially efficient expat destinations in Southeast Asia. The dollar economy removes currency risk. The territorial tax system removes local income tax on foreign earnings. The visa system — while informal — is forgiving and cheap. And roughly $1,100/month covers a genuinely comfortable life in a city with a growing expat infrastructure, fast internet, and Bangkok a short flight away for anything Cambodia can't provide.

The IRS still finds you. Self-employment tax still applies without a totalization agreement. Go in clear-eyed about the visa informality and healthcare limitations. But for remote workers optimizing the gap between US-dollar income and local spending, Cambodia delivers the arbitrage math better than almost anywhere else in the region.

Financial Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Tax laws change frequently and affect individuals differently based on their specific circumstances. Consult a qualified CPA or tax attorney experienced in US expat taxation before making decisions based on this information. The FEIE exclusion amount, visa regulations, and cost figures cited reflect data available as of mid-2026 and are subject to change.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageMay 28, 2026

Geographic ArbitrageMay 28, 2026

Vietnam Expat Guide: $1,200/Month, Zero Foreign Tax

Vietnam costs ~$1,200/month for a comfortable expat life and taxes foreign income at 0% if you stay under 183 days. Complete guide for US expats.

Geographic ArbitrageJune 3, 2026

Geographic ArbitrageJune 3, 2026

Retire in the Philippines: SRRV, Costs, and Setup

SRRV deposit from $15K, Cebu life from $1,200 monthly, Philippine law exempts foreign pension remittances from local tax. Full relocation setup guide.

Geographic ArbitrageMay 24, 2026

Geographic ArbitrageMay 24, 2026

Costa Rica Expat Guide: $2,100/Month, 0% Foreign Tax

Costa Rica taxes zero on foreign income. Live on $2,100/month and qualify with $1k/month SS. Complete visa, tax, banking, and cost of living guide.