Airbnb Hosting Abroad: The US Tax Guide You Actually Need

FEIE won't save you on Airbnb income—it's passive, not earned. Here's how expat hosts use depreciation, Schedule E, and the FTC to cut their US tax bill to near zero.

FEIE won't cover Airbnb income. Learn how expat hosts use Schedule E, depreciation, and the Foreign Tax Credit to legally cut their US tax bill.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

The average Airbnb host worldwide earns $13,800 a year. For most, that's a nice side income. For US expat hosts, it's an IRS blind spot that costs them thousands — because nearly every expat assumes their Foreign Earned Income Exclusion covers short-term rental earnings. It doesn't. Rental income is passive income. The FEIE, which shields up to $132,900 of earned income in 2026, doesn't touch a single dollar of what Airbnb pays you.

That's the bad news. The better news: with the right filing structure, most expat Airbnb hosts reduce their US tax liability to near zero using deductions, depreciation, and the Foreign Tax Credit. Here's the full breakdown.

How the IRS Actually Classifies Your Airbnb Income

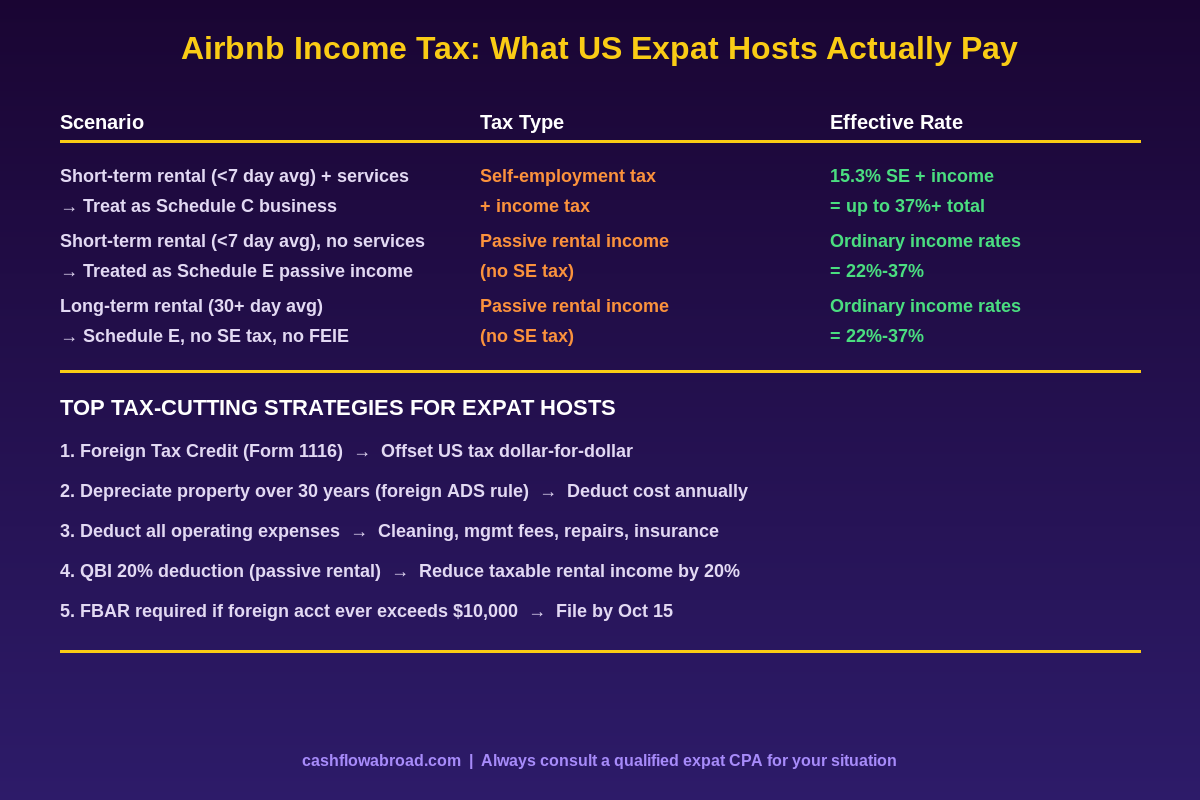

This distinction is worth understanding before anything else, because it determines whether you owe 15.3% self-employment tax on top of your regular income tax — or nothing of the sort.

The IRS looks at two factors: average rental period and whether you provide "substantial services."

- Schedule C — Business income (SE tax applies): Your average rental period is 7 days or fewer and you provide substantial services — daily maid service, meals, guided tours, concierge-level management. This turns your rental into a hospitality business. You owe 15.3% self-employment tax on net earnings, plus income tax. Most expat hosts don't fall here.

- Schedule E — Passive rental income (no SE tax): Your average rental period is 7 days or fewer but you don't provide substantial services (standard cleaning between guests doesn't count), or your average stay is longer than 7 days. You file on Schedule E. No SE tax, but rental income is taxed at your ordinary income rate.

Nearly all typical Airbnb setups — listing your Medellín apartment or Lisbon flat by the night or week without providing concierge services — land on Schedule E. That's where this guide focuses.

What You Can Deduct on Schedule E

Schedule E lets you subtract real expenses from rental income before taxes hit. The IRS is generous here — and most expat hosts leave money on the table by not tracking everything.

Deductible Expenses

| Expense Category | What Qualifies | Note |

|---|---|---|

| Platform fees | Airbnb's 3% host service fee | Deduct directly from gross receipts |

| Cleaning | Cleaning fees paid to third parties | Keep invoices/receipts |

| Property management | Co-host fees, property management companies | Common for remote expat hosts |

| Repairs & maintenance | Broken fixtures, painting, maintenance | Capital improvements must be depreciated |

| Insurance | Home/rental insurance premiums | Pro-rate if mixed personal/rental use |

| Utilities | Electricity, internet, water | Pro-rate for rental days only |

| HOA/condo fees | Association fees for the rental unit | Fully deductible if rental-only |

| Foreign property taxes | Local property taxes paid abroad | Deduct on Schedule E, not as FTC |

| Mortgage interest | Interest on a foreign mortgage | Deductible if used to acquire rental property |

Depreciation: The Silent Deduction

Depreciation is the deduction most expats forget to take — and it's often the biggest one. Foreign residential rental property must be depreciated over 30 years using the straight-line ADS method (versus 27.5 years for US domestic rentals). The building value only — land doesn't depreciate.

Example: You purchased a Medellín, Colombia apartment for $95,000. After apportioning land value at $20,000, your depreciable building basis is $75,000. Divide by 30: you deduct $2,500/year automatically — whether you remember to claim it or not. (If you forget to take it, the IRS still assumes you did when you sell, so always claim it.)

For a higher-value property — say a $280,000 Lisbon flat with $50,000 in land value — that's $230,000 ÷ 30 = $7,667/year in depreciation deductions. Against $25,000 in gross rental income, that's a meaningful reduction before other expenses even factor in.

The Foreign Tax Credit: Your Double-Tax Shield

The Foreign Tax Credit (FTC) is the mechanism that prevents you from paying full tax on the same income to two governments. You file Form 1116 with your US return and claim a dollar-for-dollar credit for taxes paid to the country where the property sits.

It works like this: If you earned $20,000 gross Airbnb income from a property in Portugal and paid €3,200 (~$3,400) in Portuguese rental tax, your US tax liability on that income drops by $3,400. For most expat hosts operating in countries with meaningful rental tax rates — Portugal (28%), Spain (19%), France (30%), Germany (25%) — the FTC eliminates US tax entirely on that income.

Countries with lower or zero rental taxes (Colombia, Mexico, Panama) create a different situation: you'll owe more US tax, but the deductions above still do heavy lifting.

One important distinction: foreign property taxes paid on your rental property are not creditable via Form 1116 — you deduct them on Schedule E instead. Only income taxes paid on rental earnings get the FTC treatment.

For a deeper look at managing your US banking while hosting abroad, see our full expat banking guide — particularly the section on keeping US accounts active while living overseas.

FBAR and FATCA: When Rental Income Triggers Reporting

Here's where expat hosts get surprised. Your Airbnb hosting income triggers separate reporting requirements if it flows through foreign financial accounts.

FBAR (FinCEN Form 114): Required if the aggregate value of all your foreign financial accounts exceeds $10,000 at any point during the calendar year. This includes checking accounts, savings accounts, foreign PayPal or payment processor accounts, and any account holding rental deposits. The penalty for non-willful failure starts at $10,000 per violation. Filing is due April 15 with an automatic extension to October 15.

FATCA (Form 8938): Higher thresholds apply for expats — $200,000 aggregate for joint filers, $100,000 for single filers. If you're receiving substantial rental income, this could apply.

The practical fix: have Airbnb pay directly to a US bank account. Mercury is excellent for this — it's a US business bank account with no monthly fees and solid wire/ACH support, keeping your rental income in a clean US account with no FBAR implications. You then transfer funds internationally as needed using Remitly, which consistently beats bank exchange rates on international transfers.

You'll also want a real US mailing address for IRS correspondence and to maintain your US banking relationships. Traveling Mailbox ($15/month) gives you a real US street address in 50+ cities, scans your mail digitally, and can deposit checks — essential for any expat running a rental business from abroad. We cover this in more detail in our virtual mailbox guide.

For a full walkthrough of FBAR and FATCA requirements, see our FBAR and FATCA filing guide.

Country-Specific Rules That Catch Expat Hosts Off Guard

Your local country's rental regulations matter just as much as your IRS filing. Here's where several popular expat destinations stand in 2026:

| Country | Local Rental Tax Rate | Key 2026 Development | FTC Usable? |

|---|---|---|---|

| Spain | 19% non-resident withholding | 86,000+ illegal listings removed; national STR registry voided by Supreme Court — local regulations now vary by region | Yes |

| Portugal | 28% on rental income | 40% of Alojamento Local permits revoked; Lisbon and Porto heavily restricted | Yes |

| France | 30% flat tax (PFU) | New EU sustainability regulations effective May 2026; registration required in all cities | Yes |

| Colombia | 0–35% income tax + possible IVA | SAT-equivalent DIAN registration required if revenue exceeds annual threshold; IVA (19% VAT) may apply | Partial |

| Mexico | 25% flat on gross, or 35% on net | Airbnb now withholds and remits Mexican ISR automatically for hosts on the platform | Yes |

| Thailand | 5–35% personal income tax | Condo rentals technically require hotel license; enforcement increasing in Chiang Mai, Phuket | Yes |

European markets have seen the most dramatic crackdowns. If you're hosting in Spain or Portugal, verify your local municipal registration is current — operating without it now triggers heavy fines, and Airbnb is actively removing non-compliant listings under government orders.

For expats thinking about the Colombia Airbnb market, the cost-of-living advantage remains compelling. Medellín and Cartagena properties can generate $1,200–$2,800/month in Airbnb income at nightly rates far below what comparable US properties command. See the full cost of living breakdown for Medellín for context on why this market attracts expat investors.

The QBI Deduction: One More Tool in the Box

Under legislation making the Qualified Business Income (QBI) deduction permanent, eligible expat hosts filing Schedule E may deduct up to 20% of their qualified rental income before calculating US income tax — on top of the expense deductions and FTC already described.

The deduction phases out at higher income levels ($197,300 for single filers, $394,600 for joint filers in 2026), but many expat hosts fall well below these thresholds because the FEIE already removes most of their wage income from the US-taxable equation. For a host earning $20,000 in rental income with no other US-taxable income, the QBI deduction reduces taxable rental income to $16,000 — saving $440–$880 in tax depending on their bracket.

Depreciation Recapture: The Deferred Bill to Plan For

When you sell the property, the IRS recaptures all the depreciation you claimed — at a 25% tax rate. On a property depreciated for 10 years at $2,500/year, that's $25,000 in accumulated depreciation, triggering a $6,250 tax bill at sale.

This isn't a reason to skip depreciation (the IRS assumes you took it whether or not you did, so skipping it just means paying recapture with no corresponding deduction benefit). But it does affect how you model exit scenarios. Factor depreciation recapture into any property investment analysis, particularly for high-appreciation markets like Medellín or Lisbon where sale gains can be substantial. Our full guide to buying and renting property abroad covers exit tax strategy in detail.

The Practical Setup: 6 Steps Before Your First Guest Checks In

- Determine your Schedule C vs. E classification. Count your average stay length and assess your service level. Nightly or weekly stays with no daily housekeeping or meals = Schedule E. Document your cleaning policy in writing.

- Open a US bank account for Airbnb payouts. Route rental income to a US account to avoid FBAR complications and keep funds in dollars. Mercury is free, works well for this, and has no foreign transaction fees.

- Track every expense from day one. Management fees, cleaning invoices, repair receipts, and Airbnb's own fee statements (downloadable from your host dashboard). A simple spreadsheet by month is enough to start.

- Get a virtual US address. Required for IRS mail, US banking, and maintaining your state domicile. Traveling Mailbox at $15/month is the practical standard among expat hosts and remote landlords.

- Register locally where required. Spain, Portugal, France, and Mexico all have registration requirements for short-term rentals. Operating without registration exposes you to fines and potential removal from Airbnb — don't skip this step.

- Hire an expat CPA for year one. Specifically someone who has filed Schedule E for foreign properties. The depreciation schedule for foreign property (30-year ADS), the FTC on rental income, and the FBAR interplay are not things a domestic accountant sees regularly. The cost ($500–$1,500 for year one) typically recovers itself in deductions they identify that you'd otherwise miss.

The Bottom Line

Airbnb hosting from abroad is one of the cleanest ways to build passive income while living on geographic arbitrage. The IRS bill that most expats dread rarely materializes in practice — because depreciation, operating expenses, and the Foreign Tax Credit, properly applied, neutralize most of it. What kills expat hosts isn't the tax rate; it's not filing at all, or filing on the wrong form without claiming what they're owed.

Know your classification (almost certainly Schedule E), document your expenses from day one, and use the FTC to offset the local taxes you're already paying. That combination typically brings your US liability close to zero — while the rental cash flows in.

For more on managing money across borders as an expat, see our guides on cutting international transfer fees and the expat investing playbook for building wealth abroad without triggering PFIC rules.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute tax, legal, or financial advice. Tax rules for US expats are complex and fact-specific. Consult a qualified expat CPA or tax attorney before making any filing decisions. Rental income rules, foreign tax credit eligibility, and country-specific regulations may change. All figures referenced are based on information available as of 2026.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJune 17, 2026

Expat Tax & FinanceJune 17, 2026

Form 1116: How to Recover Foreign Taxes as a US Expat

Learn how Form 1116 works: income baskets, the credit limitation formula, dividend withholding recovery, FEIE interaction, and the 10-year

Expat Tax & FinanceJune 10, 2026

Expat Tax & FinanceJune 10, 2026

Norway Wealth Tax and Income Tax: A US Expat's Guide

Norway levies a 1.0% annual wealth tax on assets above $174,000 plus income tax reaching 47.5%. US expats learn what they owe, FTC strategy, and visa

Expat Tax & FinanceJune 5, 2026

Expat Tax & FinanceJune 5, 2026

Foreign Pensions and US Tax: UK, Canada, Germany

UK state pension is taxable in US. Canadian RRSP defers automatically. German pension triggers US tax. Country-by-country expat pension tax guide.