Greece's 7% Flat Tax: Pay Less Than Your US State

Greece's 7% flat tax on all foreign pension income lasts 15 years. A California retiree earning $60K saves up to $15,000/year by moving. Here's exactly how it works.

Greece's 7% flat tax on all foreign pension income lasts 15 years. A California retiree earning $60K saves up to $15,000/year by moving.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

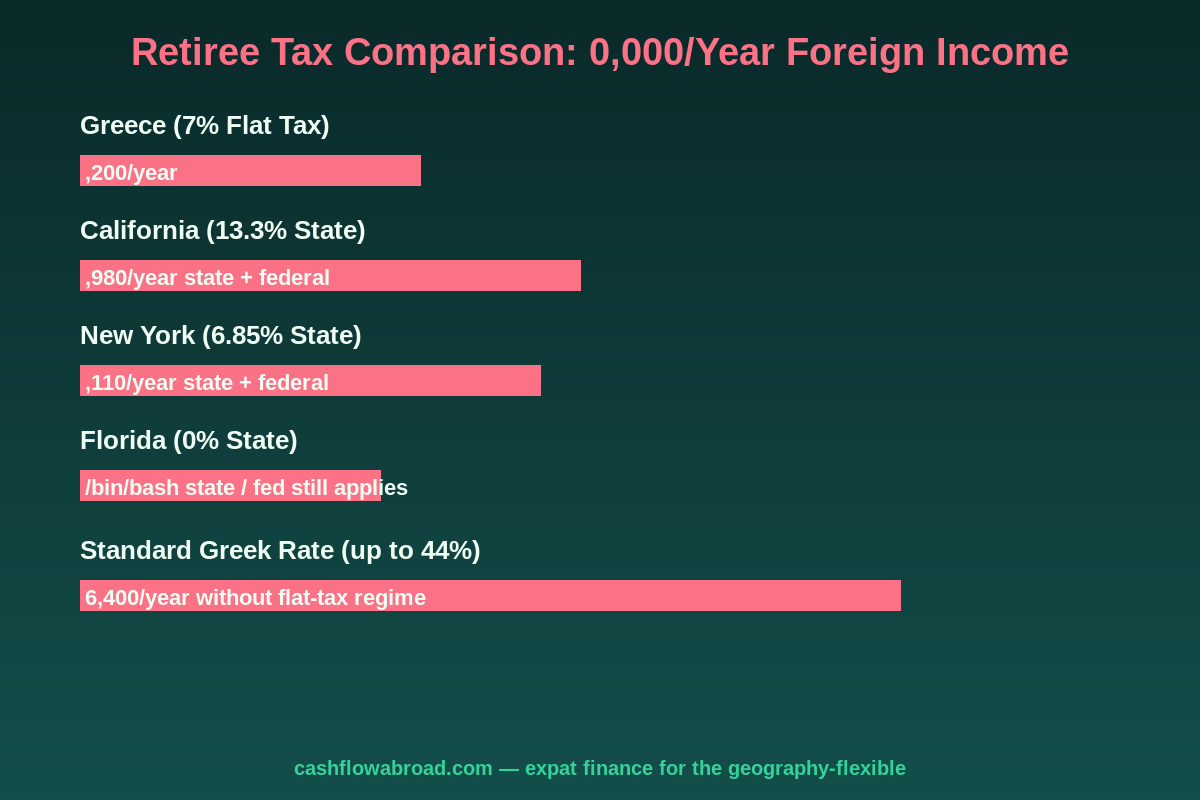

Here's a number that should make every American retiree stop scrolling: if you retire to California earning $60,000 a year from your pension, IRA distributions, and investment dividends, you hand Sacramento $7,980 — just in state taxes. Move that same income to Greece under their 7% flat-tax regime, and you owe €4,200 (~$4,600) to the Greek government. Total. Because Greece has no state-level income tax.

That's not a loophole or a gray area. It's a formal program Greece introduced in 2020 specifically to lure foreign retirees with their checkbooks intact. More than 5 years in, it's still running, still underused by Americans, and still one of the most favorable retiree tax structures in any developed country. Here's exactly how it works — and what they don't put in the brochure.

What Is Greece's 7% Flat Tax?

Greece created a special retiree tax regime under Article 5B of the Greek Income Tax Code. It allows foreign pensioners who transfer their tax residency to Greece to pay a flat 7% on all foreign-source income — for up to 15 years. After 15 years, you're taxed at standard Greek rates (9%–44%), unless you've planned ahead.

What counts as "foreign income" under this regime is unusually broad:

- Foreign pension payments (including US Social Security)

- IRA and 401(k) distributions

- Dividends from foreign stocks and funds

- Interest from foreign bank accounts

- Capital gains from foreign-asset sales

- Rental income from property outside Greece

Income earned inside Greece is taxed at standard Greek rates, which start at 9% and climb to 44% above €40,000. So the strategy is simple: keep your income-generating assets abroad and live off them in Greece.

Who Can Actually Qualify

The requirements are specific, and one of them trips up more applicants than you'd expect:

- Not a Greek tax resident for 5 of the last 6 years. If you've been living in Greece already, you likely don't qualify. This regime is for new arrivals.

- You receive a pension from a recognized source. This means a pension tied to prior employment — Social Security, a private employer pension, a government pension, or income from an IRA/401(k) connected to work history. Pure investment income with no pension component is harder to qualify with, though some advisors have made it work via structured arguments.

- You transfer your tax residency to Greece. This means spending 183 days per year there, registering with the Greek tax authority (AADE), and obtaining a Greek tax number (AFM). You can't "visit for tax purposes" — Greece actually wants you there.

- You come from a country with a tax information exchange agreement with Greece. The US qualifies. Most EU countries, UK, Canada, and Australia do as well.

Applications open January 1st and close March 31st each year. Miss that window and you wait 12 months. This is not a rolling admission process — it's calendar-bound, which catches people off guard when they move in October thinking they can apply immediately.

The Tax Math: What You Actually Save

Let's run real numbers. A retired couple drawing $80,000 a year total — $30,000 Social Security, $35,000 IRA distributions, $15,000 in dividends:

| Location | State/Local Tax Rate | Annual State Tax | Federal Tax (Estimated) | Total Tax Burden |

|---|---|---|---|---|

| Greece (7% Flat) | 7% flat on all foreign income | $5,600 | $0 (Greek tax credits offset US liability) | ~$5,600 |

| California | Up to 13.3% | ~$9,000 | ~$9,000–$12,000 | ~$18,000–$21,000 |

| New York | Up to 10.9% | ~$7,200 | ~$9,000–$12,000 | ~$16,200–$19,200 |

| Florida / Texas | 0% (no state income tax) | $0 | ~$9,000–$12,000 | ~$9,000–$12,000 |

The Greece number assumes you use the foreign tax credit to offset Greek taxes paid against your US federal liability — which you can do since the US–Greece tax treaty allows for this. US citizens always owe the IRS something, but Greek taxes paid generally wipe most of it out at these income levels. The net result: you often end up paying roughly what you'd pay in Greece, plus a small residual US amount, rather than double-taxing yourself.

This is why Greece actually beats Florida for high-income retirees drawing heavily from taxable accounts. Florida has no state tax, but you still face full US federal rates. Greece's 7% flat tax, combined with the foreign tax credit, caps your total obligation dramatically.

Getting There Legally: The FIP Visa

To live in Greece as a non-EU citizen, you need the Financially Independent Person (FIP) visa — the Greek equivalent of Portugal's D7 or Spain's non-lucrative visa. Requirements as of 2026:

- Minimum income: €3,500/month net from passive sources (pension, dividends, rental income). Add 20% for a spouse (€4,200/month) and 15% per child.

- Alternative: €126,000 in a Greek or international bank account demonstrating you can self-fund for the 3-year visa duration.

- Private health insurance: Required. This is where SafetyWing becomes relevant — their Remote Health plan provides comprehensive international coverage accepted in Greece, with premiums significantly lower than US COBRA or domestic equivalents.

- No working in Greece: The FIP visa is explicitly for passive-income retirees. Take on Greek-source work and you violate the terms.

- Clean criminal record + standard documentation.

The FIP visa is valid for 3 years, renewable. After 5 years of continuous legal residence, you can apply for permanent residency. After 7 years, you're eligible for Greek citizenship — which means EU citizenship, full freedom of movement, and a passport that opens 186 countries visa-free.

One practical note: €3,500/month is €42,000/year. That's the income threshold to get the visa, not the amount you need to live on. Greece is substantially cheaper than that threshold. You could pocket a meaningful surplus even after Greek costs.

Greece vs Portugal vs Italy: The Honest Comparison

| Factor | Greece | Portugal | Italy |

|---|---|---|---|

| Retiree Tax Regime | 7% flat on foreign income | NHR closed Jan 2025; IFICI excludes retirees | 7% flat for southern villages under 20K population |

| Duration | 15 years | N/A for new retirees | 10 years |

| Visa Income Requirement | €3,500/month | €920/month (D7) | €31,000/year (Elective Residence) |

| Monthly Cost of Living (Single) | €1,100–€1,800 | €1,200–€2,000 (rising) | €1,200–€2,200 |

| Path to EU Citizenship | 7 years | 5 years | 10 years |

| English Widely Spoken | Yes (especially coastal and tourist areas) | Yes (Lisbon, Porto) | Limited outside tourist zones |

Portugal was the obvious answer for expat retirees until January 2025, when the NHR regime closed and was replaced by IFICI — a program designed for tech workers and researchers, not retirees drawing Social Security. That shift handed Greece a significant competitive advantage it hadn't previously had. Italy's version of the 7% regime exists but comes with a major catch: you must move to a municipality with fewer than 20,000 residents in a southern region (Calabria, Sicily, Sardinia, etc.). Greece applies the rate nationally — Athens, Thessaloniki, Crete, wherever you land.

What It Actually Costs to Live in Greece

The FIP visa requires €3,500/month but most retirees spend considerably less. Real monthly budgets by city in 2026:

| City | Rent (1BR) | Groceries/Month | Total Monthly Budget |

|---|---|---|---|

| Athens (city center) | €600–€900 | €250–€350 | €1,500–€2,300 |

| Thessaloniki | €450–€700 | €220–€300 | €1,200–€1,700 |

| Crete (Heraklion) | €400–€650 | €200–€280 | €1,100–€1,600 |

| Aegean Islands (off-season) | €350–€500 | €230–€330 | €1,000–€1,500 |

Athens has gotten more expensive — rents jumped 20–30% between 2022 and 2025 partly due to short-term rental saturation. But Thessaloniki, Greece's second-largest city with a thriving food scene, Byzantine history, and a large international university population, remains dramatically cheaper than comparable European capitals. A couple can live very comfortably there on €1,800–€2,200/month.

Healthcare is a significant variable. Expats on the FIP visa need private coverage. The public system (ESY) is technically accessible once you pay Greek social contributions, but that typically requires Greek-source income or employment. Most retirees use a combination of private Greek health insurance (€150–€300/month for an older retiree) and supplemental international coverage. See our full expat health insurance guide for a breakdown — and SafetyWing's Remote Health plan is one of the more cost-effective global options that works in Greece.

The 15-Year Cliff You Need to Plan For

Year 16 is where Greece gets uncomfortable. The 7% flat rate expires, and you drop into standard Greek tax brackets: 9% up to €10,000, 22% from €10,001 to €20,000, 28% from €20,001 to €30,000, 36% from €30,001 to €40,000, and 44% above €40,000. On an $80,000 income, that's a jump from roughly $5,600/year to over $20,000/year in Greek taxes alone.

The strategies retirees are using to handle Year 16:

- Move before the clock runs out. Spend 15 years in Greece, then relocate to another territorial-tax country (Panama, Georgia, Malaysia) before Greek standard rates kick in. You've preserved wealth for 15 years and exit cleanly.

- Reclassify income sources. By year 16, some retirees have converted enough assets to Roth accounts or structured income differently. This requires years of advance tax planning.

- Apply for the HNW non-dom regime. If your income has grown substantially, the €100,000/year lump-sum option caps your Greek tax at that fixed amount regardless of income. At incomes above ~€1.4M/year, it becomes the math winner.

The honest reality: 15 years is long enough that most retirees in their 60s won't be optimizing for Year 16 on day one. But if you move at 55, you should be planning this from the start.

The US Expat Angle: What the IRS Still Wants

Nothing about this regime eliminates your US tax filing obligation. US citizens owe the IRS regardless of where they live — and Greece's 7% rate, while low, still generates a foreign tax credit you can apply against your US liability. At $60,000–$80,000 in income, the foreign tax credit often wipes out most or all of what you'd owe federally, leaving a small residual that varies based on income composition.

A few mechanics worth knowing:

- Social Security: The US–Greece tax treaty allows Social Security benefits to be taxed only in Greece, not the US. That means Social Security income covered under the 7% flat tax is effectively not double-taxed.

- Roth IRA distributions: These are tricky. Roth distributions are tax-free in the US, but Greece may tax them since the treaty doesn't explicitly exempt Roth income the same way. Clarify this with a bilingual tax advisor before drawing down a Roth from Greece.

- FBAR and FATCA: Opening Greek bank accounts triggers standard foreign account reporting requirements. Any account over $10,000 at any point in the year goes on your FBAR. FATCA Form 8938 applies if your foreign holdings exceed $200,000 while abroad.

- Brokerage access: Many US brokerages restrict accounts for non-residents. Charles Schwab International is the most expat-friendly option — it allows US citizens living abroad to maintain investment and checking accounts with free ATM withdrawals worldwide. Set this up before you leave.

You'll also want to maintain a valid US mailing address for IRS correspondence and state domicile management. A Traveling Mailbox virtual address (~$15/month) gives you a real US street address that scans physical mail and handles check deposits — essential for maintaining financial continuity abroad. We cover this in detail in our virtual mailbox expat guide.

For sending money between your US accounts and a Greek bank, Remitly handles USD-to-EUR transfers with competitive rates and transparent fees — useful for funding monthly expenses from US retirement accounts without getting slaughtered on conversion.

How to Apply: The Actual Steps

- Establish Greek residency first. Rent a long-term apartment (not Airbnb), get a utility bill in your name, and apply for your AFM (Greek tax number) at the local tax office (DOY). This is the foundation for everything else.

- Obtain the FIP visa. Apply at the Greek consulate in your home country before you move, or apply for a national visa to enter and then convert within Greece. Process times vary: 30–90 days from a US consulate is realistic.

- File the Article 5B application. Submit to the AADE (Greek tax authority) between January 1 and March 31 of the year you want the regime to begin. You'll need your AFM, proof of foreign pension income (SSA letter, 1099s, pension statements), proof you weren't a Greek tax resident in 5 of the last 6 years, and a certificate from your home country tax authority.

- Pay your first year's tax. On approval, you're assessed 7% on your declared foreign income and pay by the standard Greek filing deadline (typically July).

- File annually in both countries. You file a Greek income tax return each year declaring foreign income and paying 7% on it. Simultaneously, you file your US return and claim the foreign tax credit for Greek taxes paid.

The bureaucratic friction is real. Greece is not known for fast or digital immigration processes. Budget 3–6 months for everything to come together, work with a local Greek accountant (bilingual ones in Athens typically charge €800–€2,000/year for expat returns), and don't try to DIY the Article 5B application on a first attempt.

The Bottom Line

Greece's 7% flat tax is a legitimate, treaty-compliant regime that lets qualifying foreign retirees slash their income tax bill for 15 years while living in one of the most beautiful countries in Europe. The eligibility rules are real, the application window is narrow, and the bureaucracy is Greek. But for retirees escaping California, New York, or any other high-tax state — particularly those drawing $60,000+ in combined retirement income — the financial case is difficult to argue against.

Portugal closed its NHR door in January 2025. Italy buried its version in rural southern villages. Greece left the door open, available nationally, accessible to anyone with a qualifying pension and 183 days a year to spend on the Mediterranean. That window won't stay open indefinitely. Tax regimes this favorable tend to attract attention and get revised once enough people use them. The five-year window between 2020 and now has been significantly underutilized by American retirees who simply didn't hear about it.

For more on how far your Social Security stretches abroad, the full geographic arbitrage playbook, and the FEIE and foreign tax credit mechanics, explore the related guides.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual circumstances vary. Consult a qualified tax advisor familiar with both US expat tax law and Greek tax regulations before making any relocation or financial decisions. The US–Greece tax treaty and Greek domestic law governing the Article 5B regime should be reviewed with a licensed professional for your specific situation.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Retirement AbroadMay 31, 2026

Retirement AbroadMay 31, 2026

Social Security for Expats: Collect Full Benefits from Abroad

US expats can collect Social Security in 186+ countries. The 2025 WEP repeal restored hundreds per month for expats with foreign pensions.

Retirement AbroadJuly 13, 2026

Retirement AbroadJuly 13, 2026

Rule 72(t) Early IRA Withdrawals: The Expat Guide

How expat early retirees use Rule 72(t) SEPP to access traditional IRA funds before 59½: calculation methods, 2026 AFR rates, FEIE limits, and

Retirement AbroadJune 4, 2026

Retirement AbroadJune 4, 2026

Required Minimum Distributions for US Expats Abroad

RMDs apply no matter where you live. Covers SECURE 2.0 age rules, expat withholding, Roth conversions, and the 25% penalty for missed distributions.