The $39,870 Expat Bonus: Foreign Housing Exclusion Explained

You are claiming the FEIE and still leaving up to $39,870 more tax-free on the table. The Foreign Housing Exclusion stacks directly on top of Form 2555.

Most US expats who claim the Foreign Earned Income Exclusion feel like they've done the work. They've filed Form 2555, excluded up to $132,900 of earned income, and saved several thousand dollars in federal tax. They're leaving another $39,870 completely untouched.

There's a second exclusion built into the same form—Part VI of Form 2555—called the Foreign Housing Exclusion (FHE). It stacks on top of the FEIE, applies to your rent, utilities, and several other housing costs, and requires no additional forms beyond what you're already filing. In expensive cities like Singapore or London, the combined ceiling jumps well past $200,000 in total excluded income per person. Yet IRS data consistently shows the housing exclusion is claimed at a fraction of the rate of the FEIE itself. The gap is almost entirely explained by taxpayers who simply didn't know it existed.

What Is the Foreign Housing Exclusion?

The FHE lives in IRC Section 911(a)(2). It lets qualifying US expats exclude the portion of their foreign housing costs that exceeds a base floor—the IRS's assumption of what housing "would cost" in the US—from their federal taxable income. Whatever you spend on rent and qualifying expenses above that floor, up to a city-specific cap, comes off your gross income.

The mechanism works on top of the FEIE, not instead of it. The IRS applies the housing exclusion first, then calculates the FEIE on the remaining foreign earned income. Both amounts reduce your taxable income on the same return.

There's also a Foreign Housing Deduction, which covers the same expenses for self-employed expats who can't take an exclusion against earned income (more on that distinction below).

The 2026 Numbers You Need

Three figures govern the FHE for the 2026 tax year:

- Base housing amount: $21,264 — this is 16% of the $132,900 FEIE limit, and it's subtracted from your qualified expenses before you get any benefit. Think of it as the IRS's assumed US housing cost. Nothing below this threshold is excludable.

- Standard cap: $39,870 — the maximum housing exclusion for most countries (30% of the FEIE limit). Your net standard-location benefit is $39,870 − $21,264 = $18,606.

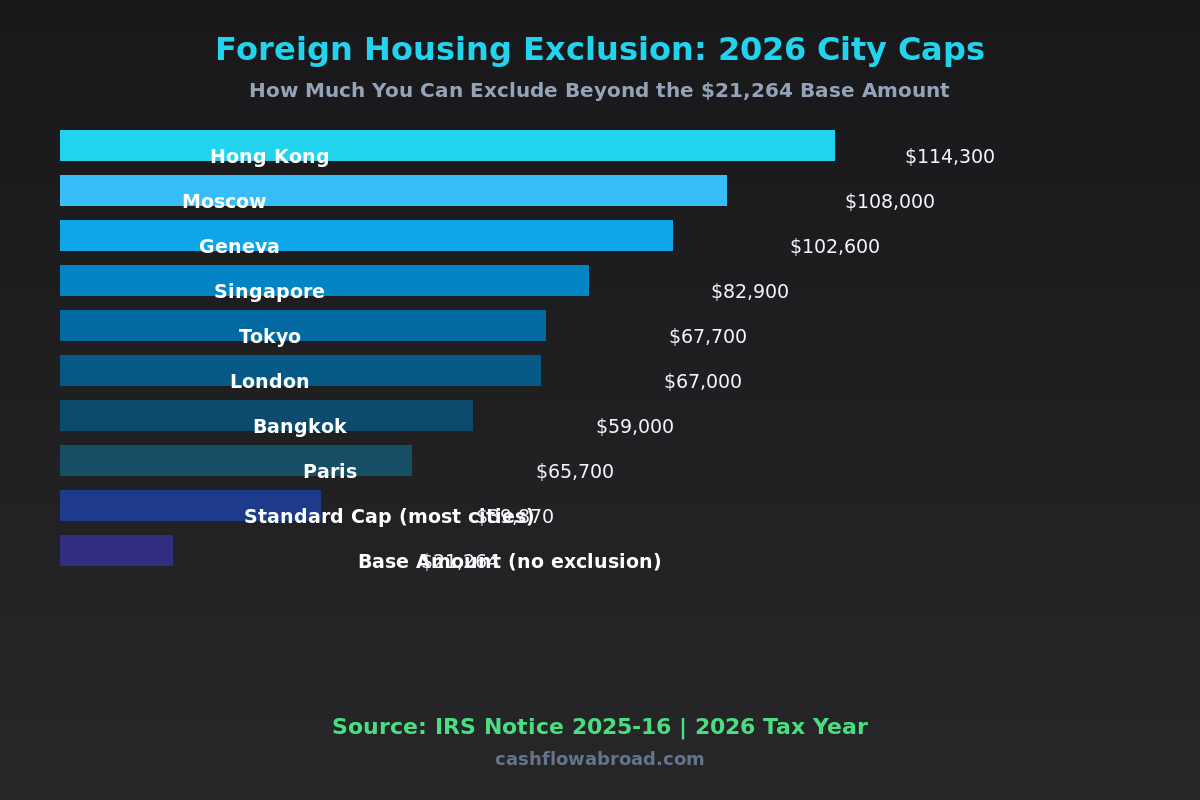

- High-cost city caps: For 137 cities with above-average rents, IRS Notice 2025-16 sets higher limits. In the most expensive markets, these caps can exceed $100,000.

| Location | 2026 FHE Cap | Net Excludable (Above Base) |

|---|---|---|

| Hong Kong | $114,300 | $93,036 |

| Moscow | $108,000 | $86,736 |

| Geneva | $102,600 | $81,336 |

| Singapore | $82,900 | $61,636 |

| Tokyo | $67,700 | $46,436 |

| London | $67,000 | $45,736 |

| Paris | $65,700 | $44,436 |

| Bangkok | $59,000 | $37,736 |

| Most other countries | $39,870 (standard) | $18,606 |

An expat renting in Singapore for $4,500/month ($54,000/year) would clear the $21,264 floor by a wide margin and could exclude up to $61,636 in housing costs. Paired with the $132,900 FEIE, their total exclusion reaches $194,536 per person before the first dollar of US federal income tax applies.

What Housing Expenses Qualify

The IRS definition is broader than most people expect, and narrower in a few specific ways.

Qualifying expenses:

- Rent

- Utilities — electricity, gas, water, sewer (telephone and internet do not qualify)

- Renter's or property insurance on the dwelling

- Nonrefundable fees paid to obtain a lease (common in Japan, Korea, and parts of Europe)

- Rental of furniture and accessories

- Residential parking

- Household repairs

What doesn't qualify:

- Telephone and internet bills

- Purchased furniture or appliances

- Property improvements that extend the life or value of the home

- Housing costs paid by your employer that weren't included in your taxable income

- "Lavish or extravagant" expenses—an undefined IRS standard, but worth noting for high-end markets

If your employer pays your housing directly and excludes it from your W-2, you cannot claim those same costs under the FHE. The exclusion only applies to amounts you actually paid—or that appear in your taxable income—not employer benefits that bypassed your return entirely.

FHE + FEIE: How the Math Actually Works

This is where most people's understanding breaks down. The housing exclusion does not simply add $18,606 to your FEIE cap. The IRS runs it on a separate track first, and then the FEIE applies to the remaining income. The order matters.

Here's the walkthrough for an employee earning $160,000 in 2026, renting in a standard-cap country for $30,000/year in qualified housing costs:

| Step | Amount |

|---|---|

| Foreign earned income | $160,000 |

| Qualified housing expenses | $30,000 |

| Minus base housing amount | −$21,264 |

| Housing exclusion claimed | $8,736 |

| Foreign earned income after housing exclusion | $151,264 |

| FEIE applied (capped at $132,900) | −$132,900 |

| Remaining taxable income | $18,364 |

Without the housing exclusion, the same person would have $27,100 in taxable income after the FEIE—$8,736 more. At the 22% marginal bracket, the FHE saves them roughly $1,922 in federal tax on a $2,500/month apartment. If that same person is in London paying $5,500/month ($66,000/year), and London's cap is $67,000, their net housing exclusion is $44,736—a federal tax saving of $9,842 per year.

Those aren't trivial numbers. For a couple with both spouses earning abroad and both paying rent, they multiply again.

Employee vs. Self-Employed: A Critical Distinction

The Foreign Housing Exclusion is for employees—W-2 earners or foreign employer equivalents. Self-employed expats who earn through Schedule C file a Foreign Housing Deduction instead, reported on Schedule 1, Form 1040. The qualifying expenses are identical; the tax mechanics differ.

For self-employed expats, the housing deduction reduces earned income before the SE tax calculation, which can interact with how much FEIE you can then claim. The deduction also flows through differently on the standard deduction vs. itemized deduction analysis. If you're a freelancer or running a one-person LLC abroad, don't assume the housing exclusion works the same way as it does for employed expats—run both scenarios before filing.

How to Claim It on Form 2555

The FHE requires no separate form. It lives in Part VI of Form 2555—the same form you already file for the FEIE. Adding the housing exclusion is incremental work on an existing filing, not a new return.

The eligibility tests are identical to the FEIE:

- Physical Presence Test: 330 full days in a foreign country during any consecutive 12-month period, OR

- Bona Fide Residence Test: Established bona fide residence in a foreign country for an uninterrupted tax year

For Part VI, you'll need: total qualified housing expenses for the year, your location's housing limit (from IRS Notice 2025-16 or the standard $39,870), number of qualifying days, and whether any employer-provided housing was included in your W-2 Box 1 income.

If you split the year between two countries—say, six months in Medellín and six in Bangkok—you must pro-rate the housing limit: (city cap ÷ 365) × days in that location. Keep housing expense records separated by location for the year. The IRS won't ask for them upfront, but an audit will.

Three Cases Where the FHE Doesn't Help You

The FHE is not universally beneficial. Analyze carefully—or skip entirely—in these situations:

1. Your housing costs are below $21,264/year. If you're renting in Tbilisi, Medellín, or Chiang Mai for $800–$1,200/month, you're paying $9,600–$14,400 annually. You never clear the base amount, and no exclusion benefit exists. This is actually fine: it means you're living cheaply enough that the FEIE alone probably wipes out your US tax anyway.

2. You're using the Foreign Tax Credit instead of the FEIE. The FHE pairs with the FEIE; you can't claim FEIE and FTC on the same income. If you're in a high-tax country like Germany, France, or Australia where local tax already exceeds your US liability dollar-for-dollar via the Foreign Tax Credit, switching to the FEIE + FHE route may not be optimal. The FHE also reduces your foreign earned income available for FTC purposes, which could shrink your FTC pool and create unexpected US tax on passive income. Get a professional analysis before changing elections.

3. Your employer fully pays your housing as an excluded benefit. If your company pays rent directly on your behalf and it never appears in your W-2, there's nothing to exclude. The FHE only runs on costs that either came out of your pocket or are included in your taxable compensation.

Married Expat Households

Married expats filing jointly get one housing exclusion for the household—they don't each get the full cap. However, if both spouses earn foreign income and each maintains a separate foreign household (for example, working in different countries), each can claim their own FHE on their own Form 2555.

If filing separately (which some high-income dual-expat couples do for FEIE optimization), each spouse calculates their own FHE independently at the full city-specific limit. A high-earning couple in Singapore filing separately, each paying $4,000/month in qualifying housing costs, could each claim up to $61,636 in housing exclusion, plus $132,900 each in FEIE—a combined total exclusion of $389,072 before any US federal income tax applies.

Record-Keeping That Actually Holds Up

The IRS doesn't require receipts attached to Form 2555, but you need documentation for potential audits. Maintain:

- Lease agreements for every year claimed

- Monthly rent receipts or bank wire confirmations

- Utility statements with your name and address

- Insurance premium statements

- Any nonrefundable lease fees or furniture rental agreements

Keep these organized by tax year. Cloud storage with date-stamped scans works well. If you're keeping a US address for IRS correspondence—which you should—a virtual US mailbox ($15/month, real street address in 50+ cities, mail scanning, check deposits) handles IRS notices, brokerage statements, and state domicile requirements without needing a US family member's address on every account.

For your US financial stack while abroad, Charles Schwab International provides fee-free banking with unlimited ATM rebates worldwide and no foreign transaction fees. Keep it paired with a Mercury account for USD business invoicing if you're earning abroad as a contractor or running an online business.

The Full Picture: Combined FEIE + FHE by Location

| Scenario | FEIE | FHE (Net) | Total Excluded | Est. Tax Saved* |

|---|---|---|---|---|

| Standard city, $25K rent | $132,900 | $3,736 | $136,636 | ~$822 |

| Standard city, $45K rent | $132,900 | $18,606 | $151,506 | ~$4,093 |

| Bangkok, $50K rent | $132,900 | $37,736 | $170,636 | ~$8,302 |

| London, $66K rent | $132,900 | $45,736 | $178,636 | ~$10,062 |

| Singapore, $70K rent | $132,900 | $61,636 | $194,536 | ~$13,560 |

| Hong Kong, $100K rent | $132,900 | $93,036 | $225,936 | ~$20,468 |

*Estimated federal tax saved on FHE portion only, at 22% marginal rate. Actual savings depend on your full tax picture.

These are per-person figures. A dual-income couple in Singapore, both earning foreign income and both paying qualifying housing costs, could collectively exclude north of $389,000 before owing a single dollar in US federal income tax—on the same Form 2555 every qualifying expat is already supposed to file.

For context on the full expat tax toolkit, the FEIE strategy guide covers the eligibility tests and physical presence rules in depth. If you're weighing the FEIE against the Foreign Tax Credit for your specific country situation, the FEIE vs. FTC comparison walks through the decision logic. And for setting up the financial and banking infrastructure to support an expat life, the US expat banking guide covers the full stack.

Bottom Line

The Foreign Housing Exclusion has been sitting in Section 911 since 1978. It requires no extra forms, no special registration, and no new eligibility tests beyond what FEIE claimants already meet. The only reason to not claim it is not knowing it exists—or living somewhere cheap enough that your housing costs fall below $21,264/year, in which case you've already solved the problem a different way.

If you're paying rent abroad and haven't been filing Part VI of Form 2555, pull your last three returns. Amended returns are available for three years back (Form 1040-X), and the statute of limitations generally allows you to reclaim refunds from 2023 and 2024 returns as well. The math is straightforward; the money is already there.

Financial disclaimer: This article is for informational purposes only and does not constitute tax or legal advice. US tax rules for expats are complex and situation-specific. Consult a qualified tax professional familiar with international tax law before making any filing decisions. IRS limits referenced reflect the 2026 tax year and are subject to annual adjustment.

Related guides

Expat Tax & FinanceMay 6, 2026

Expat Tax & FinanceMay 6, 2026

The Foreign Housing Exclusion Most Expats Forget to Claim

The IRS Foreign Housing Exclusion stacks on top of FEIE. In Hong Kong, it can exclude another $93,500. Here are the 2025 city limits and how to claim

Expat Tax & FinanceMay 1, 2026

Expat Tax & FinanceMay 1, 2026

The $75K Tax Break US Expats Leave on the Table

Most US expats claim the FEIE and stop — missing a second IRS shelter that can shield up to $93K more in cities like Hong Kong or Singapore.

Expat Tax & FinanceMay 29, 2026

Expat Tax & FinanceMay 29, 2026

Self-Employment Tax: The Expat Freelancer’s Hidden Bill

FEIE zeroes your income tax abroad—but SE tax still applies. See the exact numbers and legal ways to reduce your bill as a US expat freelancer.