GILTI Tax: Why Your Foreign Company Still Owes the IRS

US citizens who own foreign corporations face GILTI tax on undistributed profits — even in zero-tax countries like Dubai or Panama. Here is how it works and how to reduce it.

Own a foreign company as a US expat? GILTI tax means you owe the IRS annually — even in Dubai or Panama. Learn how to legally reduce your bill to zero.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

You move to Dubai. Pay zero corporate tax. Set up a local LLC. Then your US accountant calls with news that ruins your afternoon: you still owe the IRS thousands of dollars on profits you never even touched.

This is GILTI — Global Intangible Low-Taxed Income — and it has quietly become the single biggest tax surprise for US citizens who own foreign companies. Since 2018, the IRS has required US shareholders of foreign corporations to report and pay tax on their company's profits annually, regardless of whether a single dollar was distributed. The zero-tax country you chose? Irrelevant. The profits sitting untouched in a foreign bank account? Taxable now.

Roughly 1–2 million Americans own or co-own foreign businesses. Most of them don't know GILTI exists until they file their first Form 5471 — or until the IRS sends a notice with a $10,000 penalty attached.

What GILTI Is and Why Congress Created It

The 2017 Tax Cuts and Jobs Act (TCJA) introduced GILTI as an anti-deferral mechanism. Before 2018, US shareholders of foreign corporations could let profits accumulate offshore indefinitely, paying no US tax until money came home. Congress decided this was unacceptable and created a rule that taxes the "excess" profits of foreign companies every single year.

The logic: a normal return on tangible business assets (equipment, buildings) is fine. But "intangible" profits — income from software, services, intellectual property, consulting — should face US tax even in a zero-tax country.

A Controlled Foreign Corporation (CFC) is any foreign corporation where US persons collectively own more than 50% of the shares, counting only those with 10%+ stakes each. If you're a US citizen who owns 100% of a company in Panama, Paraguay, or the UAE, you have a CFC and GILTI applies to you.

The GILTI Calculation: Real Numbers

The formula sounds complex but the result is simple to understand:

GILTI Inclusion = Tested Income − (10% × QBAI)

Where:

- Tested Income = the CFC's net income (roughly)

- QBAI = Qualified Business Asset Investment — the average adjusted tax basis of the CFC's depreciable tangible assets

- 10% × QBAI = the "routine return" excluded from GILTI

For most expat-owned online businesses, consulting firms, agencies, and service companies: QBAI is zero. No equipment, no machinery, no buildings. That means 100% of profits are GILTI.

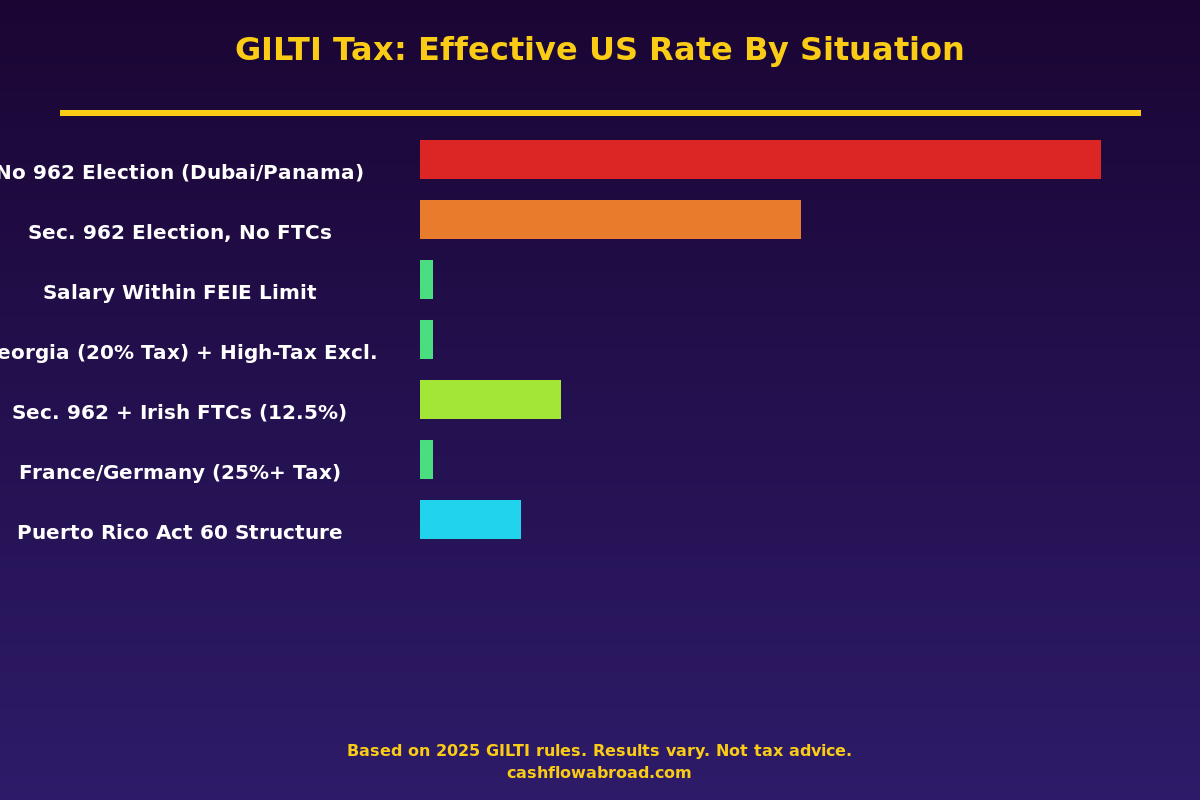

Example: US Consultant in Dubai, $100,000 Profit

| Scenario | Calculation | US Tax Owed |

|---|---|---|

| No Section 962 election (worst case) | $100,000 × 37% ordinary rate | $37,000 |

| Section 962 election (corporate treatment) | $100,000 → 50% deduction → $50,000 × 21% | $10,500 |

| Salary paid = $100,000 within FEIE limit | CFC profit reduced to $0 / FEIE excludes salary | $0 |

| Company in Georgia (country), 20% local tax | High-tax exclusion elected (20% > 18.9% threshold) | $0 |

| Company in Germany, ~30% local tax | High-tax exclusion elected, all GILTI excluded | $0 |

The Dubai consultant without a 962 election pays $37,000 in US tax on income the UAE never touched. That's not a planning failure — it's the default outcome for expats who don't actively structure around GILTI.

The Section 962 Election: Your First Defense

Section 962 allows an individual US shareholder to elect to be taxed as if they were a domestic C corporation on their GILTI inclusion. This unlocks two major benefits:

- The Section 250 deduction — reduces your GILTI inclusion by 50% before calculating tax. Effective rate drops from up to 37% down to 10.5%.

- Indirect foreign tax credits — you can claim 80% of the foreign taxes paid by the CFC as a credit against your GILTI liability.

The 962 election is made annually on your Form 1040. It's not permanent — you choose it each year based on your situation.

The catch: When the company later distributes dividends, there's a second layer of tax on previously-taxed earnings that weren't fully offset. You need to track a "962 offset account" carefully. For businesses that reinvest heavily, this is manageable. For businesses that distribute everything, the math gets messier.

The 18.9% Rule That Changes Everything

If a CFC's income is already subject to a foreign effective tax rate of at least 18.9% (= 90% of the US 21% corporate rate), you can elect to exclude that income from GILTI entirely. This is called the GILTI High-Tax Exclusion.

| Country | Typical Corporate Rate | Above 18.9% Threshold? | GILTI Exposure |

|---|---|---|---|

| UAE / Dubai | 0–9% | No | Full exposure |

| Panama (foreign-source income) | 0% | No | Full exposure |

| Paraguay (foreign-source income) | 0–10% | No | Full exposure |

| Georgia (country) | 15–20% | Borderline / Yes at 20% | Partial to zero |

| Ireland | 12.5% | No | Full exposure |

| Singapore | 17% | No | Full exposure |

| UK | 25% | Yes | Excluded |

| Germany | ~30% | Yes | Excluded |

| France | 25% | Yes | Excluded |

This creates a counterintuitive dynamic: US expats in higher-tax European countries often owe less GILTI than those in zero-tax jurisdictions. Paying 25% in Germany to exclude all GILTI makes sense if the alternative is paying 10.5% GILTI on top of complex structures in a nominally zero-tax country.

One key restriction: the exclusion is applied item-by-item at the "tested unit" level — you can't blend high-tax and zero-tax income streams within one CFC to manufacture an artificial average above 18.9%.

Who Gets Hit Hardest

The profile of a high-GILTI-exposure expat: a US citizen who left the country, set up a local company in a zero-tax jurisdiction, runs a service business (agency, consulting, SaaS, freelancing through a corp), and pays themselves via distributions rather than salary. Every one of those choices maximizes GILTI exposure.

Most exposed business types:

- Digital agencies and consultancies — no tangible assets, pure service income, zero QBAI exclusion

- Online course creators and content businesses — all intangible income

- Software companies and SaaS — IP-based income, minimal depreciable assets

- E-commerce operators — often structured through foreign corps with minimal local inventory

Least exposed: manufacturers, construction companies, equipment-heavy operations where QBAI can meaningfully offset tested income. A CFC with $2,000,000 in depreciable equipment gets a $200,000 QBAI exclusion annually — meaningful for capital-intensive businesses, completely irrelevant for a laptop-based consultant.

Five Strategies That Actually Work

1. Pay Yourself a Salary Within FEIE Limits

The FEIE (Foreign Earned Income Exclusion) excludes up to $130,000 of foreign-earned income from US federal tax in 2025 (indexed annually). Salary paid by your CFC reduces the company's retained profit — which reduces GILTI.

If your CFC earns $100,000 and you pay yourself $100,000 as salary, GILTI income drops to $0. The FEIE then excludes that salary from US tax. Net federal income tax: $0.

Limitation: The FEIE only covers earned income up to the cap. Above $130,000, you're paying ordinary income rates on excess salary — potentially worse than the 10.5% GILTI rate on a 962 election. Run the numbers both ways. Self-employment tax (15.3% on roughly the first $170,000) also applies regardless of FEIE for self-employed US citizens, so large salaries create SE tax drag. Our full FEIE guide covers the mechanics in detail.

2. Make the Section 962 Election Annually

For business owners in zero-tax countries who can't use salary + FEIE efficiently — because income exceeds the FEIE cap or because they need corporate-level cash management — the 962 election cuts the effective GILTI rate from up to 37% down to 10.5%. That's still a tax bill, but it's a fraction of the worst-case outcome.

Work with a CPA who specializes in international tax to track your 962 offset account. This prevents surprise bills when you eventually take distributions.

3. Elect the GILTI High-Tax Exclusion

If your CFC operates in a country where the effective corporate rate hits 18.9%+, file the high-tax exclusion election on Form 8992. This is why Georgia's tax structure matters: the standard 20% corporate rate can clear the threshold, while the 1% micro-business regime definitely doesn't.

4. Use a US S-Corporation Instead

An S-corp is a US domestic entity — CFC rules and GILTI don't apply. Income flows through to your personal return at ordinary rates, but only your reasonable salary faces payroll tax. S-corp distributions escape SE tax.

Trade-offs: you lose foreign corporate deferral ability (which GILTI was eliminating anyway), and you must maintain a legitimate US business address. A virtual mailbox through Traveling Mailbox handles the US address requirement for ~$15/month — a real US street address with mail scanning, forward, and check deposit. Best for expats whose clients are primarily US-based and who want simpler compliance than Form 5471 + GILTI calculations.

5. Relocate to Puerto Rico Under Act 60

Puerto Rico is a US territory. Bona fide Puerto Rico residents who qualify under Act 60's Export Services chapter pay 4% Puerto Rico rate on qualifying service income, with no federal income tax. Because a Puerto Rico entity is domestic for federal purposes, GILTI doesn't apply.

The non-negotiable requirements: 183+ days per year physically in Puerto Rico, pass three-part tax home and closer connection tests, $5,000 annual decree fee, $10,000+ annual charitable contributions to Puerto Rico nonprofits, plus IRS scrutiny that has intensified significantly. The IRS has named Act 60 compliance a named audit priority. This is not a paper relocation — Puerto Rico residency must be genuine. See our full Act 60 guide.

The Penalty Problem: $10,000 Per Year, Per Company

GILTI requires two forms most expats have never heard of:

- Form 5471 — ownership information return for each CFC (filed annually with your 1040)

- Form 8992 — the GILTI calculation

Miss Form 5471? The penalty is $10,000 per year, per corporation. Ignore an IRS notice and it adds $10,000 per 30-day period, up to $50,000 additional per failure. The statute of limitations doesn't start running until the form is actually filed. An unfiled Form 5471 from 2019 is still open to examination today.

Expats who've owned foreign companies for multiple years without filing 5471s are sitting on penalty exposure that can dwarf the actual tax owed. The IRS Streamlined Procedures for taxpayers living abroad typically waive most penalties for non-willful non-filers — but you need to act before the IRS finds you first.

The 2026 Change You Need to Know About

The One Big Beautiful Bill Act (signed July 4, 2025) renamed GILTI to Net CFC Tested Income (NCTI) starting January 1, 2026, with material changes:

- Section 250 deduction drops from 50% to 40% — effective rate rises from 10.5% to 12.6%

- QBAI is eliminated entirely — all tested income subject to NCTI, no tangible asset exclusion

- FTC haircut improves: you can now use 90% of foreign taxes as credits (was 80%)

- High-tax exclusion threshold drops to approximately 14% (was 18.9%) — significantly more countries now qualify

The QBAI elimination is significant for capital-intensive businesses that previously benefited from large exclusions. But the lower 14% threshold opens the high-tax exclusion to more expats — including many in Eastern European and Southeast Asian countries that previously fell between the cracks. For 2025 tax year returns (filed in 2026): the legacy GILTI rules still apply.

Keep Your Financial Infrastructure in Order

Running a foreign company as a US expat requires banking infrastructure that works across borders. Mercury offers fee-free US business banking with wire capabilities suited to expat-owned operations. For investments, Charles Schwab International is one of the few US brokerages that doesn't close expat accounts, offering free ATMs worldwide and full brokerage access. For moving money between your foreign company and US accounts, Remitly consistently offers competitive rates without the spread markups common with bank wires.

For the broader picture on US expat investing rules — particularly PFIC rules that apply when you hold foreign mutual funds or ETFs — see our expat investing playbook. GILTI and PFIC rules together are the two biggest compliance traps for US expats with foreign business and investment income.

Bottom Line

GILTI is not a niche edge case. If you're a US citizen who owns 10%+ of a foreign corporation, you have annual reporting obligations — and likely a tax bill — from the day that company was formed. The tax can be reduced to zero with the right structure, but none of the planning strategies kick in automatically.

Three immediate steps:

- Determine if your foreign company is a CFC. US persons collectively own >50%? You have GILTI exposure.

- Audit your Form 5471 filing history. Every missing year is a $10,000 penalty that hasn't been assessed yet.

- Model the planning scenarios — salary + FEIE, Section 962, high-tax exclusion, S-corp restructuring — against your specific income level, distribution needs, and country. The right answer varies significantly by situation.

The IRS has more visibility into foreign accounts and entities than at any point in history. CARF, FATCA, and AI-assisted audit matching have ended the era of expats quietly running foreign companies with no US consequence. The planning window is open — but only for those who act before the notice arrives.

This article is for educational purposes only and does not constitute tax, legal, or financial advice. GILTI and NCTI rules are complex and highly fact-specific. Consult a qualified international tax professional — specifically one experienced with CFCs, Form 5471, and Form 8992 — before making any structural decisions about your foreign company or business.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJune 14, 2026

Expat Tax & FinanceJune 14, 2026

Form 5471 for Expats: CFC Reporting and Penalty Guide

Own a foreign corporation with 10% US ownership? Form 5471 is mandatory — missing it costs $10,000 per entity per year automatically.

Expat Tax & FinanceJune 16, 2026

Expat Tax & FinanceJune 16, 2026

Form 5471: US Expats Who Own Foreign Companies

Filing Form 5471 is required for US expats who own 10% or more of a foreign corporation. Learn the five categories, $10,000 penalties, and how to

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.