FBAR vs FATCA: What Every Expat Must Know

FBAR and FATCA are two separate IRS reporting requirements that catch expats off guard. Here are the thresholds, penalties, and how to catch up without disaster.

The IRS fined a retired teacher $16,536 — not for unpaid taxes, but for failing to check a box on a form. Her tax bill was zero. Her penalty was real. That's FBAR, and it catches more Americans living abroad every year than almost any other compliance rule.

If you have a foreign bank account and you're a US citizen, you almost certainly have two separate reporting obligations that most people confuse, conflate, or skip entirely: FBAR and FATCA. They're different forms, filed with different agencies, carrying different penalties, and triggered by different thresholds. And yes — you might need to file both.

Here's the complete breakdown, with the numbers that actually matter.

What Is FBAR — And Why It Exists

FBAR stands for Report of Foreign Bank and Financial Accounts. The form itself is FinCEN 114, filed with the Financial Crimes Enforcement Network — not the IRS. FBAR has existed since 1970 under the Bank Secrecy Act, originally created to combat money laundering, not to target ordinary expats with savings accounts in their country of residence.

That origin matters. FBAR isn't an income-reporting form. It's a disclosure form. You're not reporting income — you're reporting the existence of accounts. The government wants to know the accounts are there. Whether you earned anything in them is a separate question handled by your tax return.

FBAR: The $10,000 Threshold That Trips Everyone Up

The filing threshold is $10,000 — but not $10,000 per account. It's an aggregate balance across all foreign accounts at any single point during the calendar year. This is where people get burned.

Say you have two foreign accounts: one with $6,000 and one with $5,000. Neither account alone crosses $10,000. But together, on any given day, they totaled $11,000. That triggers an FBAR obligation — and if you didn't file, you're potentially looking at penalties.

The threshold applies to:

- Foreign bank accounts (checking, savings, time deposits)

- Foreign brokerage accounts

- Foreign retirement accounts (including pension funds)

- Foreign mutual funds

- Accounts where you have signature authority (e.g., your employer's overseas account)

The FBAR is due April 15, with an automatic extension to October 15 — no need to request it. You file electronically through the FinCEN BSA E-Filing System. It doesn't cost anything and takes about 20 minutes if you have your account numbers handy.

What Is FATCA — And Why It's Different

FATCA — the Foreign Account Tax Compliance Act — was enacted in 2010 and operates on a completely different level. Where FBAR is a 1970s anti-money-laundering tool, FATCA is a 21st-century enforcement mechanism that turns foreign banks into IRS informants.

Under FATCA, foreign financial institutions are required to identify accounts held by US persons and report them directly to the IRS (or face a 30% withholding penalty on US-sourced payments). This is why Swiss banks started closing American accounts around 2011 and why opening a foreign bank account as a US citizen has gotten harder in the past decade.

From your side as an expat, FATCA compliance means filing Form 8938 (Statement of Specified Foreign Financial Assets) with your regular 1040 tax return. Unlike the FBAR, this form goes to the IRS, not FinCEN.

FATCA Thresholds: Much Higher for Expats

FATCA thresholds are significantly higher than FBAR — and expats living outside the US get even more generous limits than people living stateside.

| Filing Status | Value on Dec 31 | OR — Value at Any Point |

|---|---|---|

| Single or MFS — living abroad | $200,000 | $300,000 |

| Married filing jointly — living abroad | $400,000 | $600,000 |

| Single or MFS — living in the US | $50,000 | $75,000 |

| Married filing jointly — in the US | $100,000 | $150,000 |

Congress built in the higher expat thresholds deliberately — recognizing that people living overseas often maintain larger foreign account balances simply to cover rent, payroll, and daily expenses in local currency. A $250,000 balance in a Colombian bank account for someone running a business there is operationally normal, not suspicious.

FATCA also covers a broader range of assets than FBAR. Where FBAR is strictly about accounts, Form 8938 captures:

- Stocks and securities in foreign companies (held directly, not through a US broker)

- Interests in foreign partnerships, trusts, or corporations

- Foreign pension and retirement plans

- Any financial instrument or contract with a foreign counterparty

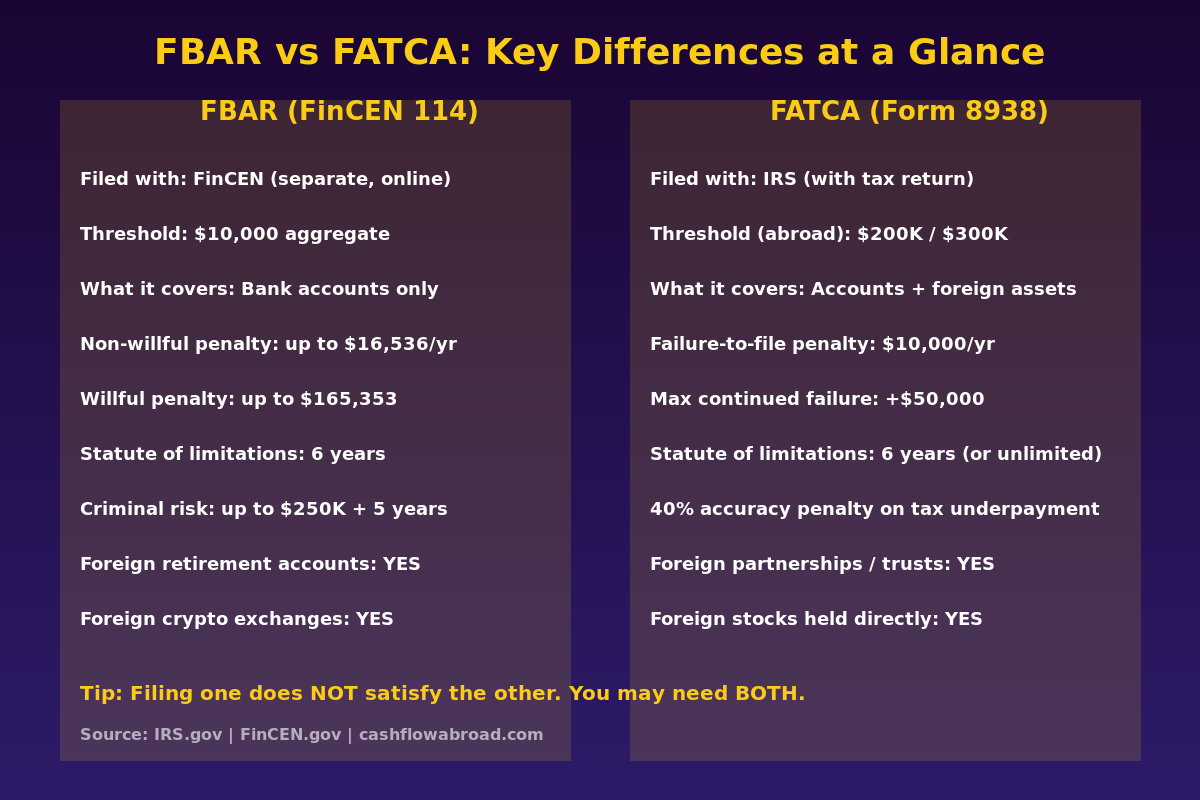

FBAR vs FATCA: The Key Differences at a Glance

| Feature | FBAR (FinCEN 114) | FATCA (Form 8938) |

|---|---|---|

| Filed with | FinCEN (not IRS) | IRS (with your 1040) |

| Trigger threshold | $10,000 aggregate (any day) | $200K–$400K on Dec 31 (abroad) |

| Assets covered | Foreign financial accounts only | Broader — includes stocks, pensions |

| Deadline | April 15 (auto ext. to Oct 15) | Same as your 1040 filing deadline |

| Non-willful penalty | Up to $16,536/year | $10,000 base |

| Willful penalty | Up to $165,353 or 50% of balance | $10,000 + $10K/30 days (max $50K) |

| Can both apply? | Yes — same accounts can trigger both | |

That last row is the part that surprises most expats. You're not choosing between FBAR and FATCA. You may be required to file both, reporting the same accounts on two separate forms to two separate government entities. The overlap is intentional — it creates redundancy in the government's information network.

The Penalties Are Not a Joke

FBAR penalties are structured in a way that's almost disproportionate to the offense.

Non-willful FBAR penalty: Following the Supreme Court's 2023 ruling in Bittner v. United States, non-willful penalties are assessed per form per year (not per account per year). The current inflation-adjusted cap is up to $16,536 per year. If you had unreported accounts for five years, that's potentially $82,680 — for doing nothing wrong intentionally, just not knowing the form existed.

Willful FBAR penalty: If the IRS determines your failure to file was willful — meaning you knew about the requirement and ignored it — penalties jump to the greater of $165,353 or 50% of the highest account balance per year. On a $500,000 account, that's $250,000 in penalties for a single year.

Criminal exposure: For egregious cases, FBAR violations can bring criminal penalties — up to $250,000 and five years imprisonment. If the violation involves more than $100,000 in a 12-month period, those numbers double to $500,000 and ten years.

FATCA penalties are less dramatic but persistent: $10,000 base penalty, plus an additional $10,000 for every 30 days you fail to file after receiving an IRS notice, maxing out at $50,000. A 40% accuracy penalty can stack on top if there's also unreported income.

Five Mistakes Expats Make Every Year

1. Thinking a small balance means no filing requirement

The $10,000 FBAR threshold is aggregate and historical. Even if your accounts are now empty, if they crossed $10,000 at any point during the calendar year, you had a filing obligation for that year.

2. Assuming FEIE exempts you from these reports

The Foreign Earned Income Exclusion reduces or eliminates your income tax. It does nothing for FBAR or FATCA. These are disclosure forms, not income forms. See our complete FEIE guide for how income exclusions actually work — they're a different mechanism entirely.

3. Missing the signature-authority trap

You need to file an FBAR for any foreign account over which you have signature authority — even if you have no ownership interest. If you're a signatory on your employer's foreign operating account and it exceeded $10,000 at any point, you have an FBAR obligation. Most employees working abroad for foreign companies don't know this.

4. Forgetting foreign retirement accounts

Retirement accounts in the country where you live — national pension plans, employer retirement schemes, private pension funds — are typically reportable on FBAR and may be reportable on Form 8938. The treatment varies significantly by country and account type. Don't assume a retirement account is exempt without verifying.

5. Waiting too long to catch up

The IRS has an amnesty-style program for expats who fell behind without fraudulent intent. It's called the Streamlined Foreign Offshore Procedures — and it has a critical eligibility window: you must apply before the IRS contacts you. Once they reach out, that path closes.

How to Catch Up: The Streamlined Procedures

If you've been living abroad and haven't been filing FBAR or Form 8938, the Streamlined Foreign Offshore Procedures (SFOP) are your best path back — assuming the IRS hasn't already initiated contact.

What SFOP requires:

- 3 years of back tax returns (or amended returns)

- 6 years of FBARs (FinCEN Form 114)

- Form 14653 — a certification that your non-compliance was non-willful

- Non-residency test: outside the US for at least 330 full days in at least one of the three delinquent tax years, with no US abode

The outcome: Qualified SFOP participants pay zero offshore penalty. No failure-to-file penalties, no FBAR penalties, no accuracy-related penalties. You pay any back taxes owed plus interest — that's it. For someone with six years of unreported accounts, this can mean the difference between $0 in penalties and $100,000.

If you're US-based or spend significant time stateside, the Streamlined Domestic Offshore Procedures (SDOP) apply instead — same catch-up structure, but with a 5% miscellaneous penalty on the highest aggregate balance of unreported accounts. Still far better than the alternative.

For comprehensive guidance on the banking and account management side of expat compliance, the US expat banking and taxes guide covers how to structure accounts to minimize both reporting complexity and penalty exposure going forward.

The Annual Compliance Checklist

Each year, before October 15, run through this list:

- Total all foreign account balances — at any single point during the year. If aggregate ever exceeded $10,000, file FBAR.

- File FinCEN 114 electronically through the BSA E-Filing System. Free. 20 minutes.

- Check Form 8938 thresholds — for single expats living abroad, $200,000 on December 31 or $300,000 at any point. If exceeded, attach 8938 to your 1040.

- List signature-authority accounts — even if you don't own them.

- Include foreign retirement accounts — verify whether each qualifies for an FBAR exclusion based on tax treaty or account classification.

- Keep records for 6 years — the FBAR statute of limitations is 6 years, not 3.

Keeping a solid US address on file matters for IRS correspondence, state domicile, and maintaining US banking relationships while abroad. A virtual mailbox gives you a real US street address in dozens of cities for around $15/month. Traveling Mailbox handles mail scanning, check deposits, and keeps your IRS correspondence reachable regardless of where you're based. See our virtual mailbox guide for expats for the full breakdown.

For the banking stack itself — which accounts to keep, which ones survive expat life without getting closed — the zero-fee expat banking stack guide covers the right US account setup. Charles Schwab International remains the gold standard for expats who need free ATM access worldwide and a brokerage that won't close accounts for living overseas.

Why This Matters More Now Than Ever

FATCA has fundamentally changed the information landscape. More than 100 countries have signed automatic information-exchange agreements with the US government. The Common Reporting Standard (CRS) means foreign banks are actively reporting US account holders whether you file or not. The era when unreported foreign accounts stayed invisible ended years ago — and penalties for past non-compliance don't disappear just because the violations weren't discovered.

The compliance process is manageable. FBAR is a free electronic filing that takes less time than a state tax return. Form 8938 is an attachment to a form you're already filing. For expats who've fallen behind, the Streamlined Procedures offer genuine amnesty — one with clear entrance requirements and a zero-penalty outcome for those who qualify.

The cost of getting this right is low. The cost of ignoring it is not.

For a deeper look at how the global data-sharing landscape has shifted — including CARF and AI-driven IRS audits — see the end of expat invisibility. If crypto accounts are part of your picture, the crypto taxes for expats guide covers FBAR and Form 8938 treatment for cryptocurrency held on foreign exchanges.

The Bottom Line

FBAR and FATCA are not the same thing. They cover overlapping but distinct assets, report to different agencies, carry different penalties, and have different thresholds. You may need both. Most expats with a local bank account need at least one.

The $10,000 FBAR threshold is low enough that virtually any expat with a local bank account triggers it. The consequences for non-compliance — even unintentional — can be severe. But the Streamlined Foreign Offshore Procedures exist precisely for ordinary people abroad who didn't know about these requirements, and they provide a structured path back into compliance without catastrophic penalties.

File the forms. Keep records for six years. And if you've been missing filings, move on Streamlined before the IRS moves on you.

This post is for informational purposes only and does not constitute tax or legal advice. FBAR and FATCA rules are complex and fact-specific. Consult a qualified US international tax professional for guidance on your individual situation.

Proximo paso

Turn reporting risk into a checklist

After comparing FBAR and FATCA, use the checklist to separate filing obligations, account inventory, state domicile, and tax strategy.

Guias relacionadas

Expat Tax & FinanceJune 2, 2026

Expat Tax & FinanceJune 2, 2026

FBAR vs Form 8938: The $10,000 Expat Filing Trap

US expats with foreign accounts must file both FBAR and Form 8938. Learn the exact thresholds, account types, and penalties before you miss a

Expat Tax & FinanceMay 17, 2026

Expat Tax & FinanceMay 17, 2026

FBAR Filing Guide: How Expats Dodge $165K Penalties

FBAR penalties can hit $165K even if you paid zero tax. Learn who must file FinCEN 114, what accounts qualify, and how to catch up penalty-free.

Expat Tax & FinanceMay 5, 2026

Expat Tax & FinanceMay 5, 2026

Australian Super & US Taxes: The Trap Nobody Warns You About

The US-Australia treaty gap exposes your super to annual IRS taxation and 0,000/yr penalties. What every US expat in Australia must know.