FBAR Filing Guide: How Expats Dodge $165K Penalties

The FBAR penalty has nothing to do with your tax bill. A single missed filing can cost 65K. Here's exactly who must file, what accounts qualify, and how to catch up.

FBAR penalties can hit $165K even if you paid zero tax. Learn who must file FinCEN 114, what accounts qualify, and how to catch up penalty-free.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

You paid every dollar you owed. Your tax returns were clean. Yet the IRS can still assess a $165,353 penalty — because you forgot to file a four-page form about a foreign savings account that earned $800 in interest. That's the FBAR trap. It has nothing to do with how much tax you owe and everything to do with disclosure.

Roughly 9 million Americans live outside the U.S. Most hold at least one foreign bank account. Only a fraction understand that a single missed filing can trigger penalties that dwarf the account balance itself. Here's exactly what the FBAR requires, how the penalties work, and what to do if you've missed years.

What Triggers the FBAR Filing Requirement

The Report of Foreign Bank and Financial Accounts (FBAR), filed on FinCEN Form 114, is required when two conditions are simultaneously true:

- You are a U.S. person — citizen, permanent resident (green card holder), or a domestic entity such as a trust, estate, or corporation

- At any point during the calendar year, the aggregate value of all your foreign financial accounts exceeded $10,000

"Aggregate" is the word most people miss. It is not $10,000 per account — it's $10,000 combined across every foreign account you hold anywhere in the world, even briefly. If you had $6,000 in a German checking account and $5,000 in a Mexican savings account on the same day, you must file. The threshold captures the summer you parked cash between apartments in two countries.

"Financial interest" is equally broad. You must file if you own the account directly, but also if:

- A foreign company in which you own more than 50% holds foreign accounts

- You have signature authority over a foreign business account held by your employer

- The beneficial owner of the account is a trust for which you are the grantor or a beneficiary

That last point catches expats who work for foreign subsidiaries. You can have signature authority over an account you've never personally deposited a cent into, and the FBAR obligation still applies.

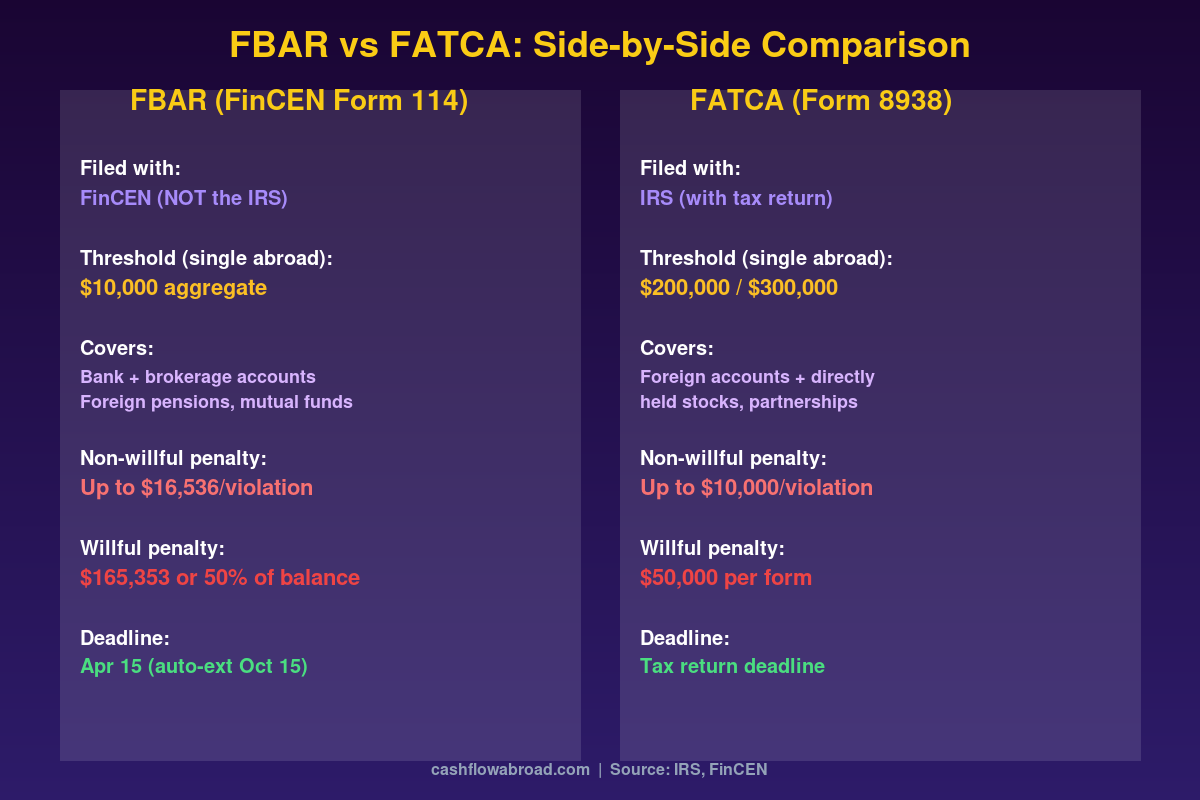

FBAR vs. FATCA: Not the Same Obligation

Confusing FBAR with FATCA is the second most common mistake. They are two entirely separate reporting requirements run by two different agencies — and filing one does not substitute for the other.

| FBAR (FinCEN 114) | FATCA (Form 8938) | |

|---|---|---|

| Filed with | FinCEN — electronically, never attached to tax return | IRS — attached to your Form 1040 |

| Threshold (abroad, single) | $10,000 aggregate at any point during year | $200,000 at year-end or $300,000 at any point |

| Threshold (abroad, married filing jointly) | $10,000 aggregate at any point during year | $400,000 at year-end or $600,000 at any point |

| What it covers | Foreign bank and financial accounts only | Foreign accounts + stocks, partnerships, other assets |

| Non-willful penalty (2026) | Up to $16,536 per annual report | Up to $10,000 per year |

| Willful penalty (2026) | $165,353 or 50% of account balance, whichever is higher | Up to 40% of undisclosed asset value |

| Criminal exposure | Up to $500,000 fine + 10 years imprisonment | Civil penalties only (criminal handled separately) |

A married expat abroad may owe FBAR at $10,000 combined balances but not Form 8938 until their year-end balance reaches $400,000. Both thresholds operate independently. If you meet both, file both — there's no overlap credit.

Your overall expat tax strategy ties these obligations together. A solid expat banking and taxes framework covers how FBAR, FATCA, the FEIE, and foreign tax credits all interact in a single annual filing.

The Supreme Court Ruling That Saved One Man $2.67 Million

In February 2023, the Supreme Court issued one of the most taxpayer-friendly FBAR decisions in history: Bittner v. United States (598 U.S. 2023), decided 5-4.

Alexandru Bittner, a Romanian-American businessman, failed to file FBARs for five years. During those years, he held more than 50 foreign accounts annually. The government argued each missed account per year was a separate violation — assessing $10,000 × 272 accounts = $2.72 million in total penalties. The Supreme Court disagreed.

The Court held that for non-willful failures, the $10,000 penalty applies per annual report, not per account. Bittner's penalty was reduced to $50,000 — $10,000 for each of the five missed annual FBARs.

This ruling matters enormously for expats with multiple foreign accounts who missed filings due to genuine unawareness. It does not help willful violators: the per-account penalty structure still applies to knowing or reckless failures, where the 2026 amount reaches $165,353 or 50% of account balance per account per year — whichever is greater.

Accounts You're Probably Not Reporting

Beyond the obvious checking and savings accounts, these commonly-missed categories have generated significant penalty assessments:

Foreign Pension Plans

The Australian Superannuation, Canadian RRSP, Singapore CPF, UK SIPP, German Riester — all are generally reportable on the FBAR if they meet the $10,000 threshold. The IRS published guidance that created confusion over the years, but the current position is clear: defined contribution foreign pensions are reportable. For defined benefit plans, the IRS recommends using a reasonable estimate of present value. When in doubt, report.

Foreign Brokerage Accounts

A brokerage account held at a foreign financial institution counts even if it holds U.S.-listed ETFs. The institution's physical location determines whether it's a "foreign financial account," not the nationality of the assets inside it.

Crypto on Foreign Exchanges

FinCEN has signaled that cryptocurrency held on foreign exchanges may be subject to FBAR reporting requirements, though final rules are still pending. Given the IRS's aggressive posture on crypto compliance, the conservative approach is to report digital assets on non-U.S. platforms if the aggregate value reaches $10,000. For a full breakdown of how crypto intersects with U.S. expat obligations, the expat crypto tax guide covers reporting, capital gains treatment, and the FATCA interaction.

Employer Signature Authority Accounts

If your foreign employer granted you signature authority over any corporate account — payroll, operating, or otherwise — you may have an FBAR obligation for that account even with zero personal financial interest. The common exception applies when you have no financial interest and the employer-owner already reports the account. Get written documentation if you're relying on that exception.

How to File the FBAR: Step-by-Step

The FBAR is filed electronically only — there's no paper option. The process:

- Go to the BSA E-Filing System at bsaefiling.fincen.gov. You can file as a guest without creating a FinCEN account.

- Complete FinCEN Form 114. For each foreign account, you need: financial institution name and address, account number, maximum value during the calendar year (in USD), and account type (bank, securities, other).

- Convert maximum balances to USD. Use the highest balance the account reached at any point during the year — not the year-end balance. Convert using the U.S. Treasury's official exchange rates, published each December for that calendar year at Treasury.gov.

- File by April 15. An automatic extension to October 15 applies if you miss the April deadline — no separate extension request is needed.

If you hold more than 25 foreign accounts, you may file on a summary basis rather than listing each account individually. You must still maintain full records in case the IRS requests them.

Maintaining a U.S. banking anchor while living abroad simplifies FBAR compliance by keeping your core finances on domestic ground. Charles Schwab International actively welcomes expat clients and offers free ATM withdrawals worldwide — a strong domestic anchor alongside any foreign accounts. For U.S. business banking, Mercury is built for remote entrepreneurs and doesn't close accounts simply because you live overseas.

One piece of infrastructure that most expats underestimate: a real U.S. mailing address. The IRS, banks, and brokerages all require one for correspondence. Traveling Mailbox provides a real U.S. street address in 50+ cities with mail scanning and check deposits for about $15/month — essential for maintaining state domicile, IRS correspondence, and banking relationships. The full breakdown is in our virtual mailbox guide for expats.

Penalties, Deadlines, and Record-Keeping

The 2026 penalty amounts, adjusted for inflation under the Federal Civil Penalties Inflation Adjustment Act:

| Violation Type | Penalty (2026) | Per What? |

|---|---|---|

| Non-willful (unaware or negligent) | Up to $16,536 | Per annual FBAR (per Bittner 2023) |

| Willful (knew and didn't file) | $165,353 or 50% of account balance — whichever is greater | Per account, per year |

| Criminal (willful) | Up to $500,000 fine | Plus up to 10 years imprisonment |

"Willful" in FBAR law doesn't require proof of intent to evade taxes — it includes "willful blindness." Courts have found willfulness where taxpayers signed returns with Schedule B's foreign account question (line 7a: "Did you have a financial interest in or signature authority over a financial account in a foreign country?") and checked "No" without actually verifying the answer. That signature creates a presumption of awareness of the question.

The IRS statute of limitations to assess FBAR penalties is six years from the filing deadline. A 2019 FBAR (due April 2020) remains open through April 2026. Keep foreign account statements showing maximum balances, institution names, and account numbers for at least seven years.

Missed Years? The Penalty-Free Catch-Up Path

If you've missed FBAR filings and your failure was genuinely non-willful, the IRS offers a legitimate amnesty program: the Streamlined Foreign Offshore Procedures (SFOP) for expats who meet the non-residency test.

Under SFOP, you:

- File the past 3 years of delinquent or amended federal tax returns

- File the past 6 years of missing FBARs (FinCEN Form 114)

- Pay any unpaid tax owed on those returns plus interest

- Submit a signed certification that the failure to file was non-willful

The result: zero FBAR penalties, zero failure-to-file penalties, zero accuracy-related penalties. For expats who genuinely didn't know about FBAR — which is extraordinarily common among long-term expats who left before FATCA's 2010 passage — SFOP is the correct and legally protected path.

Non-residency eligibility: you must have been outside the U.S. for at least 330 days in at least one of the three tax years covered by the amended returns. Most long-term expats pass this easily.

The non-willfulness certification requires honesty and care. If the IRS later determines the original failure was willful, the streamlined submission becomes a paper trail and full willful penalties can still apply. Work with a tax attorney or CPA experienced in FBAR compliance before submitting if there's any question about intent. The combination of FEIE and foreign tax credits often reduces past tax liability to near zero, making SFOP both financially and legally manageable for most expats.

Why "Quiet Disclosures" Are Dangerous

A quiet disclosure — simply filing late FBARs on your own, outside the streamlined program — might feel like the simpler path. It isn't. The IRS has specifically flagged quiet disclosures as a pattern it examines. When examiners identify one, they can investigate whether the original failure was actually willful, potentially pulling open years that would otherwise have been protected under the streamlined program.

Worse, a quiet disclosure provides none of the penalty protection that streamlined filing does. You've now told the IRS you had unreported foreign accounts — without the legal shield.

The correct path for non-willful failures is always the IRS's formal program. Do not improvise this one.

FBAR Compliance as Part of Your Banking Stack

Good FBAR compliance starts with knowing what you have. Keep a simple spreadsheet: institution name, country, account number, and approximate maximum balance for each calendar year. Update it quarterly. The actual FBAR filing takes about 30 minutes once the data is organized.

Minimize foreign accounts to what you actually need. For most expats, a single local-currency account for day-to-day spending plus a U.S. anchor account covers 95% of transactions. Moving money between them efficiently — without the markup that most bank transfers embed in exchange rates — matters. Remitly offers transparent fee structures and mid-market rate pricing for regular international transfers, without the inflated spreads hidden inside most bank wires.

For expats in Latin America who need dollar-denominated savings with local currency access, ARQ Finance offers USDC/USDT-based accounts with local currency conversion for Mexico, Colombia, Argentina, and Brazil. Worth understanding from a reporting standpoint: stablecoin balances on non-U.S. platforms may eventually fall under FBAR requirements once FinCEN finalizes its crypto guidance.

The zero-fee expat banking stack covers the full infrastructure — which accounts to keep, how to maintain them compliantly, and how to minimize both fees and reporting complexity across multiple jurisdictions.

FBAR in Perspective

The FBAR generates no tax liability on its own. Filing it doesn't mean you owe anything. It is a disclosure instrument — a mechanism for the U.S. government to track where American capital sits. Most expats who understand that reframe stop treating FBAR as a threat and start treating it as a 30-minute annual exercise.

The risk is not in filing. It's in not knowing you're required to. Add up the peak balances across every foreign account you hold. If the aggregate crossed $10,000 on any single day during the calendar year, file FinCEN 114. If you've missed years, use the streamlined procedures. The penalty exposure from non-compliance dwarfs the inconvenience of getting compliant.

For a complete picture of your U.S. expat tax obligations — FBAR, FEIE, FATCA, self-employment taxes, and the state tax traps that follow Americans overseas — the U.S. expat banking and taxes guide is the starting point.

Financial and Tax Disclaimer: This article is for informational and educational purposes only and does not constitute legal, tax, or financial advice. FBAR rules are complex and fact-specific. Consult a qualified tax attorney or CPA experienced in U.S. international tax law before making filing decisions, particularly if you have missed prior-year FBARs or are uncertain whether your conduct was willful or non-willful. Penalty amounts are for calendar year 2026 and adjusted annually for inflation.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Next step

Build the tax file before filing

FBAR is only one part of the annual abroad tax file. Keep account records, tax elections, and state domicile evidence in one place.

Related guides

Expat Tax & FinanceJune 23, 2026

Expat Tax & FinanceJune 23, 2026

FBAR vs Form 8938: Expat Reporting Guide

US expats with foreign accounts over $10,000 must file FBAR. Learn how Form 8938 differs, current penalty amounts, and how to catch up.

Expat Tax & FinanceJune 14, 2026

Expat Tax & FinanceJune 14, 2026

FBAR: The $10,000 Trap Every Expat Must Understand

The $10,000 FBAR threshold is aggregate across all foreign accounts, not per account. Who must file, what counts, and the penalty math after Bittner.

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

FBAR vs FATCA: What Every Expat Must Know

FBAR and FATCA are two separate foreign account reporting requirements with different penalties and thresholds. Learn what every US expat must file.