Andorra Tax Residency: Europe's Hidden 10% Tax Haven

Andorra's 10% income tax, zero inheritance tax, and 4.5% VAT make it Europe's most underrated tax haven — but Americans face a critical catch.

In January 2025, the Andorran passive residency quota for the entire year was exhausted in 22 days. Sixty applicants who had been waiting for months were handed rejection letters and given 8 days to leave the country — with their €50,000 deposits suddenly reclassified as non-refundable fees. Welcome to Europe's least-covered tax haven.

Andorra doesn't appear on most expat shortlists. It's not a Caribbean offshore bank with a questionable reputation, not a trendy digital nomad beach destination, and not a massive EU jurisdiction like Portugal or Spain. It's a mountain microstate between France and Spain with 77,000 residents, no train service, no airport, and a 10% flat income tax that makes its neighbors' rates look extortionate.

For the right profile of expat, it might be the most underrated residency in Europe. For Americans specifically, there's a critical asterisk — and most articles glossing over it are written by people who don't pay US taxes.

What Makes Andorra Different

Andorra's tax structure is deceptively simple. Personal income tax tops out at 10%, with the first €24,000 exempt and a graduated 5% band from €24,000–€40,000 (with an €800 relief credit). The first €3,000 of savings income is fully exempt. Capital gains tax starts at 15% if you sell an asset within the first year of ownership, drops by roughly 2% per year, and hits zero after 12 years. There is no inheritance tax, no wealth tax, and a VAT equivalent (called IGI) of just 4.5% versus the 20%+ standard VAT rates in France and Spain next door.

That IGI rate is not a footnote — it's why hundreds of thousands of French and Spanish residents drive into Andorra every month to buy electronics, alcohol, tobacco, and luxury goods. Residents benefit from this permanently. Your daily cost of living is structurally cheaper than in any neighboring country.

Corporate tax matches the personal rate: flat 10%. Dividends paid by Andorran companies to Andorran residents are fully exempt. For anyone with a business that can be structured locally, the combination is genuinely powerful.

Residency Options in 2026

There are three paths to Andorran residency, and they are not equally accessible.

Passive Residency (By Investment)

This is the route marketed to high-net-worth individuals. As of January 2026, the requirements are:

- Minimum investment: €1,000,000 in Andorran assets — real estate, financial instruments, shares in local companies, or collective investment funds. (If you go pure real estate, the minimum property value is €800,000.)

- AFA deposit: €50,000 paid to the Andorran Financial Authority. As of 2026, this is officially non-refundable. It is an admission fee, not a deposit. Add €12,000 per dependent.

- Minimum stay: 90 days/year — the main appeal vs. active residency's 183-day requirement.

- Income requirement: ~€54,912/year (300% of Andorran minimum wage), plus ~€18,304 per dependent.

- Annual quota: 200 slots for the entire country. In 2025, these filled in January. Applications open October 1 for the following year.

The investment threshold doubled in 2026 (from €600,000 to €1,000,000) and the AFA deposit went from refundable to non-refundable in the same legislative package. If you were planning to do this on 2024's terms, those terms no longer exist.

Non-residents purchasing property face an additional 6% foreign investment surcharge on a first property and 10% on any subsequent purchase — a deliberate cooling measure. Foreign nationals may also own only one detached house or a maximum of two apartments in Andorra.

Active Residency (For Workers and Self-Employed)

If you work in Andorra — for an Andorran employer or as a registered self-employed person — you qualify for active residency:

- Minimum stay: 183 days/year

- Government bond deposit: €15,000 (refundable on departure)

- Immigration fee: €2,500 + €500 per dependent

- Must register a self-employed activity or hold an employment contract with an Andorran entity

Active residents pay into CASS, Andorra's social security system. For self-employed residents, minimum monthly CASS contributions run approximately €563/month. In return, you get public healthcare coverage (75–90% reimbursement after paying upfront).

Digital Nomad Visa

Introduced in 2022 under Andorra's Digital Economy Law, this is theoretically the most accessible path — but the caps make it effectively a lottery:

- Only 50 slots per year for the entire country, all nationalities combined

- Minimum income: €3,858/month (~$4,200), or 300% of Andorran minimum wage

- No €50,000 AFA deposit required

- Minimum stay: 90 days/year

- Must work exclusively for non-Andorran clients via remote/digital means

- Private health and disability insurance mandatory (€100–€300/month depending on age)

- New as of 2024: Basic Catalan (A1/A2 level) required — a real barrier for most English-first applicants

The visa is valid for 2 years and renewable. With 50 total slots for the world, treat this as a long-shot application — not a reliable plan.

Cost of Living: The Real Numbers

Andorra is often described as "expensive" by people comparing it to Southeast Asia, and "cheap" by people who just came from Monaco. The reality sits closer to Madrid or Lisbon — livable at a mid-range budget, with consumer goods notably cheaper due to the 4.5% IGI.

| Expense | Monthly Cost (Approx.) |

|---|---|

| 1-bedroom apartment, Andorra la Vella center | €1,100–€1,400 |

| 2-bedroom apartment, central | €1,300–€1,600 |

| Utilities (single person, efficient home) | €30–€70 |

| Groceries (couple) | €350–€500 |

| Restaurant meal (mid-range, 2 people) | €30–€50 |

| Private health insurance (passive/nomad residents) | €100–€300 |

| Total — single, comfortable lifestyle | €1,200–€1,700/month |

| Total — couple, comfortable lifestyle | €2,000–€3,500/month |

Housing inventory is tight — the entire urban core occupies a single mountain valley, and the rental market has tightened as Andorra's profile has risen. The consumer goods savings are persistent: electronics, wine, perfume, and clothing are all meaningfully cheaper than in France or Spain. Most residents take regular shopping trips across the border — in reverse, compared to what their neighbors do.

Banking in Andorra

Andorra has exactly three banks: Andbank, Creand, and Morabank. This concentration means serious scrutiny on every account opening.

Opening an account as a non-resident is technically possible but practically difficult. Most account types aren't available to non-residents; those who qualify typically need minimum private banking deposits of €250,000+. Expect to appear in person, produce a full financial paper trail, and wait 4–8 weeks. Hire a local gestoria (licensed Andorran advisor) — the internal rules vary by bank and nationality, and this is not a process to navigate blind given the stakes involved.

The operational upside: despite not being in the EU, Andorra participates in SEPA. Euro transfers to and from EU banks work exactly like domestic EU transfers — same fees, same speed. Your day-to-day banking works seamlessly with the eurozone.

For US expats managing multi-currency finances, Mercury handles US dollar banking remotely, and Charles Schwab International gives you fee-free ATM withdrawals globally plus a brokerage that doesn't immediately close expat accounts — both worth holding alongside your Andorran account.

The American Asterisk: What US Expats Actually Owe

Here is where every Andorra article written for a European audience becomes actively misleading for Americans.

A French citizen who establishes tax residency in Andorra is, by law, no longer a French tax resident. They pay Andorra's 10% maximum on income. Their prior country loses its claim. The system works as advertised for them.

A US citizen does the same move and still owes the IRS. The United States taxes its citizens on worldwide income regardless of where they live or what they pay in foreign taxes. Moving to Andorra does not change your US filing obligations — it adds Andorran ones on top.

Two additional facts compound this:

No US-Andorra Tax Treaty. Andorra has signed 17 Double Taxation Agreements — with France, Spain, Luxembourg, Portugal, UAE, Malta, and others. The US is not on that list. This means no reduced withholding on US-source income, no treaty-based double taxation protections, and no tie-breaker provisions to claim non-US residency for tax purposes.

No US-Andorra Totalization Agreement. No coordination between US and Andorran social security systems. Self-employed Americans who qualify as active residents and pay into CASS could face both Andorran CASS contributions and US self-employment tax (15.3%) on the same income. The totalization agreement list does not include Andorra.

The Foreign Earned Income Exclusion (FEIE) still applies for Americans in Andorra — if you meet the Physical Presence Test (330 days outside the US in a 12-month period), you can exclude up to $130,000 (2025) of foreign earned income. But the FEIE does not cover investment income, capital gains, or passive income. And because Andorra's max income tax is 10% while US rates for many taxpayers are higher, claiming a Foreign Tax Credit may still leave a meaningful US balance owed after the credit.

The practical upshot: Andorra can meaningfully reduce total tax burden if your income is primarily earned income, you'd otherwise pay high-rate state taxes, and investment income is modest. It will not reduce US liability to near zero without substantially more structure. Hire a US expat CPA before any application. This is not a situation for DIY software.

For a full picture of the US compliance stack, the US expat banking and taxes guide covers everything from FBAR to state tax exposure.

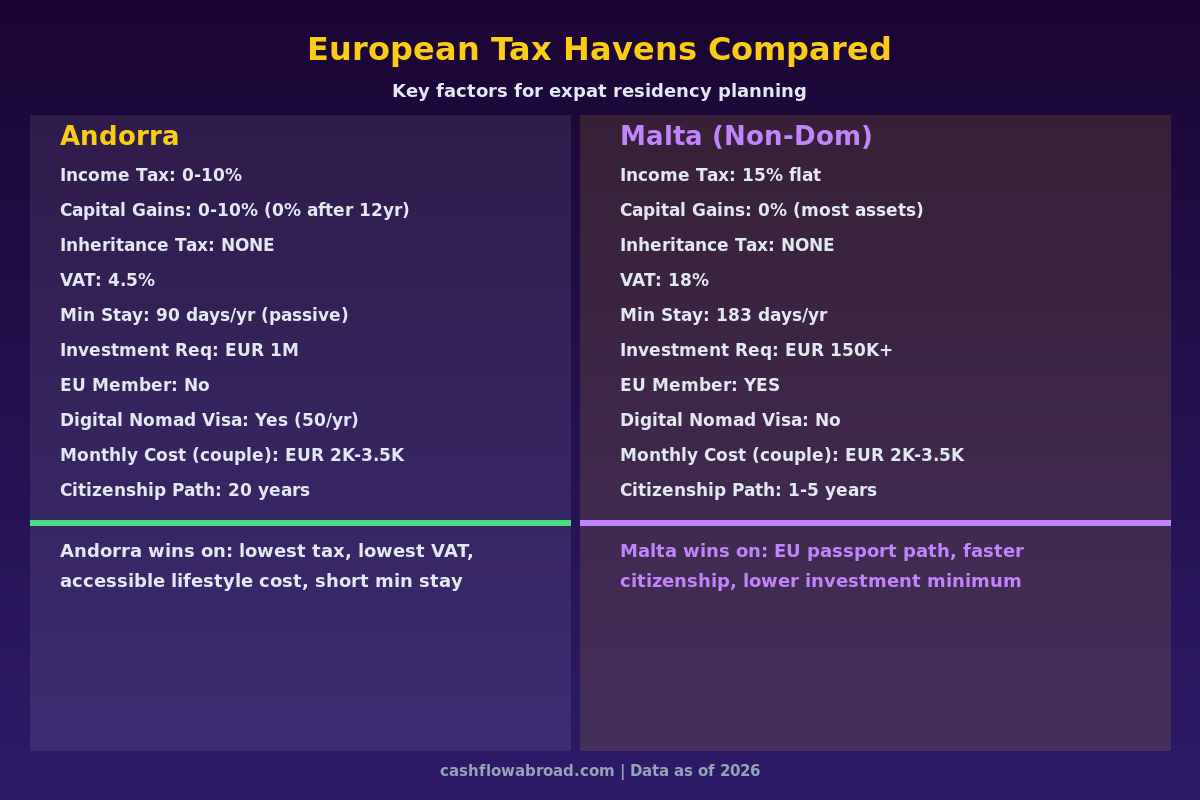

Andorra vs. Other European Tax Havens

| Factor | Andorra | Monaco | Malta (Non-Dom) | Cyprus (Non-Dom) |

|---|---|---|---|---|

| Max income tax | 10% | 0% | 15% (remittance) | 0% on foreign income |

| Capital gains | 0% after 12 years | 0% | 0% (most assets) | 0% |

| Inheritance tax | None | None | None | None |

| VAT equivalent | 4.5% | 20% (French) | 18% | 19% |

| Residency investment req. | €1M (passive) | €500K deposit + property | €150K+ (GRP) | €300K+ |

| Monthly cost (couple) | €2K–€3.5K | €6K–€20K+ | €2K–€3.5K | €2.5K–€4K |

| EU member | No | No | Yes | Yes |

| Path to citizenship | 20 years, no dual | 5+ years, very selective | 1–5 years | 7 years |

For non-Americans, Andorra wins on net effective tax rate combined with accessible cost of living. Monaco is better on income tax but costs 4–10x more to actually live there. Malta and Cyprus offer EU membership and faster citizenship paths — if a second passport matters, those routes compete on different dimensions. See the full citizenship by investment guide for that comparison.

The pending EU Association Agreement — concluded in negotiations in late 2023 but awaiting ratification by all 27 EU member parliaments and an Andorran referendum — would change this substantially. If ratified, Andorran residents would gain free movement rights to live and work across all EU states without giving up Andorra's tax structure. This remains theoretical, but it's the most significant potential upside to the Andorra proposition in decades.

Practical Realities Nobody Mentions

No airport, no train. Barcelona is 3–3.5 hours by road; Toulouse is 2 hours. Direct bus services to both airports exist, but your travel days are long. For frequent travelers, this is a meaningful quality-of-life cost that doesn't show up in budget spreadsheets.

Catalan is the official language. Spanish and French are widely spoken, and English is common in business, but government documents, official communications, and the digital nomad language requirement are all in Catalan. It's achievable at A1/A2 level — but it requires actual effort.

No dual nationality. Andorran citizenship requires 20 years of residency and renouncing your prior nationality. For Americans, that means surrendering the US passport. Nobody realistically does this. Andorra is a tax residency play, not a second passport play.

The quota situation is genuinely unpredictable. Applications for the following year's passive residency slots open October 1. With 200 total slots and global demand, prepare as early as September. Missing the window means waiting another full year — with your €50,000 AFA fee at risk if you're in process when quotas close. A local gestoria is not optional.

For maintaining US banking, IRS correspondence address, and state domicile during a multi-month application process, a Traveling Mailbox virtual US address — real street address in 50+ US cities, mail scanning, check deposits, ~$15/month — keeps your US financial infrastructure intact while you're building European residency. See the full virtual mailbox guide for how to use it properly.

Who Andorra Is Actually For

Andorra makes the most sense for:

- High-earning non-Americans currently paying 40–50%+ income tax in France, Spain, Germany, or the UK who want a legitimate low-tax European base without leaving the continent

- Entrepreneurs and business owners who can structure an Andorran entity and generate income locally — the 10% corporate rate and full dividend exemption compound well for reinvested business profits

- Retirees with substantial investment portfolios (non-American) for whom zero inheritance tax and 0% long-term capital gains is the primary objective

- Americans with primarily earned income who would otherwise pay high-rate state taxes, can claim FEIE, and have modest investment income — the savings versus California or New York can still be meaningful

Andorra is not ideal for anyone seeking near-zero total US tax liability without more comprehensive international tax planning, frequent travelers who can't tolerate the road logistics, or people on a timeline shorter than 2–3 years given quota timelines and application lead times.

For health coverage during and after the move, SafetyWing provides international health insurance that works across borders — standard for expats in the gap between leaving their home country system and establishing local coverage. Passive and digital nomad residents in Andorra who don't access CASS are legally required to hold private health insurance. The expat health insurance guide breaks down what different plan types cover and what they don't.

Conclusion

Andorra is the most legitimate, lowest-tax European residency that doesn't require Monaco-level wealth or a compromised lifestyle. A 10% income tax ceiling, zero inheritance tax, 0% long-term capital gains, and a 4.5% VAT rate don't coexist anywhere else in Europe at a cost of living a normal professional can sustain.

The caveats are real: investment thresholds jumped to €1 million in 2026, the €50,000 AFA "deposit" is now a non-refundable fee, quotas fill in days, and Americans still owe the IRS regardless of where they live. The 2025 quota debacle — 60 people rejected and told to leave in 8 days — is a useful reminder that Andorra's residency system prioritizes the country's interests, not applicants' convenience.

If you fit the profile, the math works. If you're American and hoping Andorra eliminates your IRS relationship, it won't. Go in with both eyes open, engage a local gestoria at least 6 months before you intend to apply, and treat the €50,000 AFA payment as the irreversible commitment it now is.

This article is for informational purposes only and does not constitute tax or legal advice. US expat tax situations are highly individual and fact-specific. Consult a qualified US expat CPA and a licensed Andorran immigration advisor before making any residency or tax decisions. Tax laws, residency requirements, and investment thresholds change frequently — verify all figures with official sources before acting.

Guias relacionadas

Geographic ArbitrageMay 15, 2026

Geographic ArbitrageMay 15, 2026

Andorra's 10% Flat Tax: Europe's Best-Kept Expat Secret

Andorra offers a 10% max income tax, 4.5% VAT, and zero inheritance tax. Full guide: residency types, costs, and the US expat catch.

Geographic ArbitrageJune 1, 2026

Geographic ArbitrageJune 1, 2026

Argentina for US Expats: Costs, Visas, Banking

US dollar earners can live comfortably in Buenos Aires for $1,500/month. Complete guide to Argentina visas, banking, taxes, and healthcare for US

Geographic ArbitrageMay 24, 2026

Geographic ArbitrageMay 24, 2026

Costa Rica Expat Guide: $2,100/Month, 0% Foreign Tax

Costa Rica taxes zero on foreign income. Live on $2,100/month and qualify with $1k/month SS. Complete visa, tax, banking, and cost of living guide.