Andorra's 10% Flat Tax: Europe's Best-Kept Expat Secret

Andorra caps income tax at 10%, charges 4.5% VAT, and levies zero inheritance or wealth tax. Here's the full guide for expats — including the US catch.

Andorra offers a 10% max income tax, 4.5% VAT, and zero inheritance tax. Full guide: residency types, costs, and the US expat catch.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Seventy-seven thousand people live in a country sandwiched between France and Spain, pay a maximum 10% income tax, and enjoy zero inheritance tax, zero wealth tax, and one of Europe's lowest VAT rates at 4.5%. The country: Andorra. The conversation about it in expat circles: almost nonexistent.

That silence is partly earned — Andorra has real friction points, especially for American citizens stuck with the US's citizenship-based tax system. But for European passport holders, non-US remote workers, and certain high-net-worth retirees, Andorra sits quietly in the Pyrenees as one of the most tax-efficient residency options in the world. It's overdue for a serious look.

What Makes Andorra Different

Andorra is not an EU member state. It's not in the Schengen Area. It is, however, in a customs union with the EU, which means goods move freely across its borders — you just can't use it as a Schengen base for 90-day visa-free travel (you enter Andorra through France or Spain, and Schengen days still count).

The principality is co-governed by two princes: the President of France and the Bishop of Urgell in Spain. It's a constitutional monarchy with a parliament (Consell General). The official language is Catalan. The currency is the euro, though Andorra issues its own euro coins.

The economy runs on three things: tourism (~10 million visitors per year for a population of 77,000), duty-free retail, and banking. Tobacco, alcohol, and electronics are significantly cheaper than in Spain or France, making cross-border shopping tourism a genuine economic pillar. That structural setup — heavy reliance on external spending and banking privacy — drove Andorra to build an unusually attractive tax regime to compensate for its physical isolation and tiny domestic market.

Andorra la Vella, the capital, sits at 1,023 meters above sea level — one of Europe's highest capitals — and is surrounded by ski resorts that draw 3–4 million winter visitors annually. If you're optimizing for both tax efficiency and a mountain lifestyle, the combination is hard to replicate anywhere else in Western Europe.

The Tax Structure, Explained

Andorran income tax (IRPF) is progressive in name but barely so in practice:

| Annual Income (€) | Tax Rate | Tax Owed on That Band |

|---|---|---|

| €0 – €24,000 | 0% | €0 |

| €24,001 – €40,000 | 5% | Up to €800 |

| €40,001 and above | 10% | 10% on everything over €40K |

Someone earning €100,000 pays roughly €7,000 in income tax — an effective rate of 7%. In France or Germany, the same earner pays 40–45%. The headline is 10%, but thanks to the €24,000 tax-free band, the real effective rate on most incomes lands between 5–9%.

The broader picture:

- Wealth tax: None

- Inheritance tax: None

- Capital gains tax: 0% on most assets (10% applies only to real estate capital gains, and only on the appreciation portion)

- Corporate tax: 10% flat

- VAT (IGI): 4.5% standard rate, compared to 20–25% in neighboring countries

- CASS contributions: Social security for active residents — roughly 5–8% combined employer/employee; self-employed pay approximately 5.5%

That 4.5% VAT is a daily lifestyle benefit you feel on every purchase. Restaurant meals, hotel stays, electronics, and fuel all cost materially less than across the border. For high-spending retirees or frequent diners, it compounds into thousands per year.

Two Paths to Andorran Residency

Andorra doesn't let you just show up and claim tax residency. There are two primary pathways, and they serve very different profiles.

Active Residency (For Business Owners and Remote Workers)

Active residency is for people who will work in Andorra — either employed by an Andorran company or running their own business there. Requirements:

- Own at least 20% of an Andorran company AND hold a management position (managing director or board member)

- Register and pay into CASS (Andorra's social security system)

- Physically present in Andorra for at least 183 days per year

- Pay a €50,000 non-refundable deposit to the AFA (Andorran Financial Authority) — returned when you leave in good standing

Active residency is the practical route for remote workers and entrepreneurs who want to genuinely relocate. The 183-day requirement means you're actually living there, not passing through. Andorran law firms that specialize in relocation regularly help applicants set up compliant company structures. Budget €5,000–€15,000 in legal fees to establish the company and navigate the application.

Passive Residency (For Investors and Retirees)

This is Andorra's version of a golden visa. Following updated legislation enacted in January 2026 (the Omnibus 2 law), requirements are:

| Requirement | Amount / Detail |

|---|---|

| Investment in Andorran assets | €1,000,000 minimum (real estate, financial instruments, company shares, government bonds) |

| Alternative: Housing Fund investment | €400,000 (reduced threshold for this specific route) |

| Non-refundable AFA payment | €50,000 per applicant + €12,000 per dependent |

| Minimum annual income proof | ~€54,912 (300% of Andorran minimum wage) |

| Minimum physical stay per year | 90 days |

| Private health insurance | Required, valid in Andorra |

The investment threshold rose from €600,000 to €1,000,000 in January 2026 — a significant jump that has filtered out mid-level applicants. However, the 90-day minimum stay is genuinely rare among European residency programs. Most require 183 days to establish tax residency; Andorra's passive program lets you maintain legal residency with just three months per year on the ground.

Private health insurance is mandatory for passive residents. SafetyWing's international coverage is a starting point for comparison, though Andorra-specific compliance requirements typically mean sourcing a local Andorran insurer or an internationally licensed plan that explicitly covers the principality.

Cost of Living: The Real Numbers

Andorra is not cheap in absolute terms — this is Western Europe with mountain real estate dynamics — but the combination of low income tax and low VAT makes the effective cost of living significantly lower than France or Spain for high earners whose savings rate matters.

| Expense Category | Monthly Cost (Single) | Notes |

|---|---|---|

| Rent (1-bed furnished) | €650–€850 | Andorra la Vella central; newer buildings run higher |

| Utilities | ~€90 | Electricity 68% cheaper than Spain |

| Groceries | €300–€450 | Alcohol, tobacco, and some packaged goods are duty-free |

| Dining out (mid-range) | €200–€350 | 4.5% VAT keeps restaurant bills lower than France |

| Health insurance | €80–€200 | CASS for active residents; private for passive |

| Transport | €50–€150 | No public transit — car or taxi; fuel is duty-free |

| Total moderate lifestyle | €2,000–€2,500/month | — |

Property purchase prices start around €3,000–€5,000/m² in Andorra la Vella — comparable to mid-tier Spanish cities but well below Paris or Geneva. Foreigners have historically needed government authorization to purchase, but this has been progressively liberalized; consult a local property lawyer for current restrictions.

One real friction point: no airport. The nearest are Barcelona-El Prat (roughly 3 hours by car or bus) and Toulouse–Blagnac (~2.5 hours). If you fly regularly, build that transfer time into your lifestyle calculus before committing.

The US Expat Catch

Here's where Andorra's story gets complicated for American passport holders — and most expat content glosses over this entirely.

The United States taxes citizens on their worldwide income regardless of where they live. Moving to Andorra does not eliminate your US tax obligation. And unlike 21 countries that have signed tax treaties with Andorra (including the UK, as of February 2025), the US has no tax treaty with Andorra.

In practice, this means:

- You pay Andorran income tax (up to 10%) on Andorran-source and global income once you're a resident

- You still file a US tax return reporting all worldwide income

- You can claim the Foreign Tax Credit (FTC) for Andorran taxes paid — but since Andorra's 10% cap is below most US marginal rates, you'll typically owe the rate differential to the IRS

- You can claim the Foreign Earned Income Exclusion (FEIE) — currently around $130,000 annually — on qualifying earned income, which eliminates US tax on that portion entirely. Read the full FEIE vs. Foreign Tax Credit comparison

A concrete example: a US freelancer earning $180,000/year in Andorra.

- FEIE excludes ~$130,000 from US income tax → IRS only sees the remaining $50,000

- Andorra taxes the full income at roughly 7% effective → ~$12,000 in Andorran tax

- That $12,000 FTC offsets much of the US liability on the excess $50,000

- Total effective burden: well under 20% — far better than the US's 37% marginal rate, but not zero

For US earners below the FEIE threshold: pay Andorra's tax, pay little to nothing additional to the US on that earned income. For passive income (dividends, capital gains), the FTC is your mechanism — the FEIE doesn't cover passive income. Andorra's favorable capital gains treatment helps here, but the IRS still wants its share of your investment returns.

Self-employment tax is the remaining sting: the US levies 15.3% SE tax on the first ~$160,000 of self-employment income regardless of where you live. Andorra has no totalization agreement with the US, meaning Andorran CASS contributions don't offset this. Compare that to countries like the UK or Germany, where totalization agreements eliminate the double social security hit — a real advantage those destinations hold over Andorra for self-employed Americans.

Who Andorra Is (and Isn't) For

Andorra works well for:

- EU/EEA passport holders earning remote income — they get the full benefit of a 10% cap with no US tax complexity layered on top

- Entrepreneurs building Andorran companies who want proximity to EU markets without EU corporate tax rates

- Retirees with investment income, particularly those whose passive income falls mostly within the €24,000 tax-free band or can be structured to stay in the 5% band

- High-net-worth individuals where a €1M investment is a rounding error against the long-term tax savings — even at €7,000 annual tax vs. €45,000 in France, the math recalibrates within a few years

- Anyone relocating from France, Germany, or Spain, where 40–45% marginal rates make even a partial exit immediately worthwhile

Andorra struggles for:

- US citizens with primarily US-source income — you're paying US tax regardless; Andorra adds legal structure cost without proportional benefit

- Digital nomads who need Schengen mobility — Andorra is not Schengen, and your 90/180 day clock continues to run on every trip to France or Spain

- Low-to-mid income earners — the €50,000 AFA deposit, legal setup fees, and Andorra's cost of living only justify the move at incomes where the effective tax savings are substantial

- Anyone needing EU freedom of movement or a pathway to EU citizenship — Andorra's passport, while respected, doesn't open EU borders

The five-flag strategy framework is useful context here: Andorra works best as a tax residency flag when paired with a business registered in a low-overhead jurisdiction, investments held at an international brokerage, a second passport from a travel-friendly country, and physical assets elsewhere. Treating Andorra as a one-stop solution limits its effectiveness, especially for Americans who need the FEIE and FTC framework to make the numbers work.

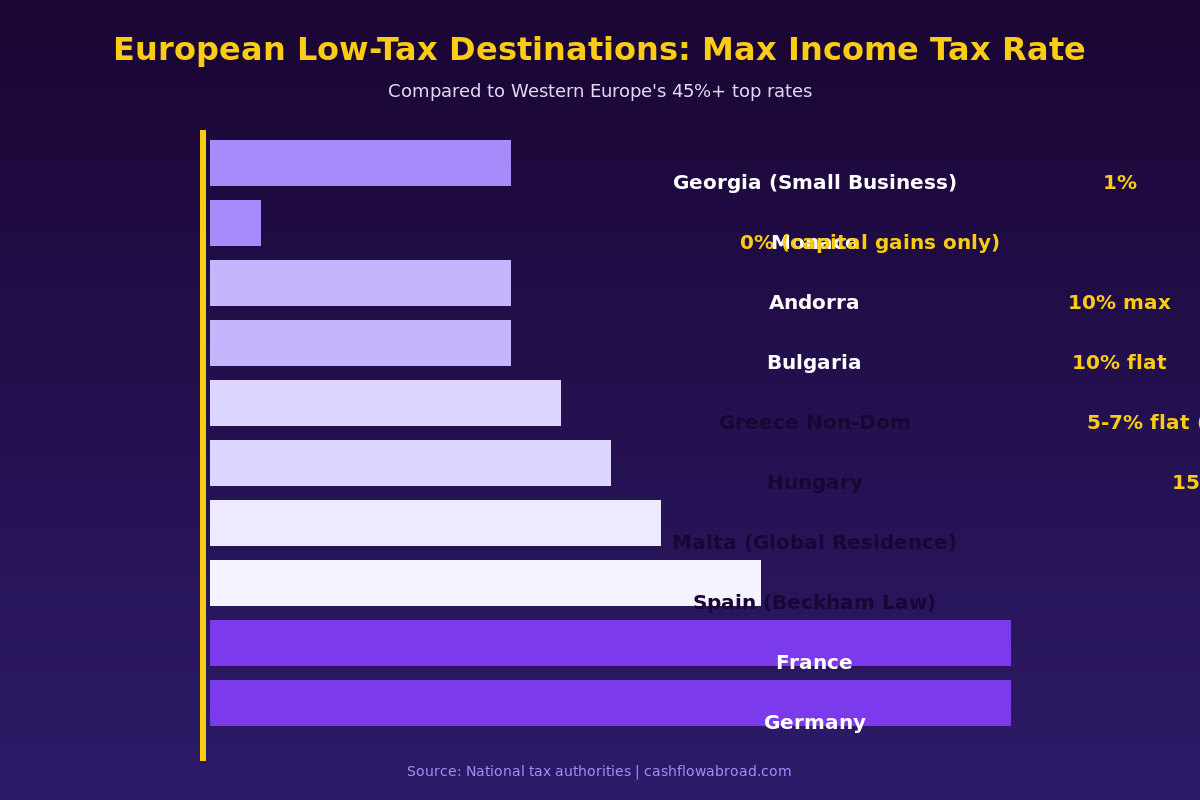

How Andorra Compares to Competitors

If you're shopping for a European low-tax residency, here's how Andorra stacks up against the realistic alternatives. See the full geographic arbitrage playbook for in-depth country analysis.

| Jurisdiction | Max Income Tax | Investment Required | Min Stay/Year | EU Member | US Tax Treaty |

|---|---|---|---|---|---|

| Andorra | 10% | €1M (passive); €50K deposit (active) | 90 days (passive) / 183 (active) | No | No |

| Bulgaria | 10% flat | None | 183 days | Yes | Yes |

| Georgia | 1% (small biz) | None | 183 days | No | No |

| Cyprus Non-Dom | 0% on dividends | None formal | 60–183 days | Yes | Yes |

| Greece Non-Dom | 7% flat (retirees) | None | 183 days | Yes | Yes |

| Malta Global Residence | 15% flat | €275K+ property | None | Yes | Yes |

| Hungary | 15% flat | None | 183 days | Yes | Yes |

For non-US expats, Bulgaria is the hardest competitor to dismiss: same 10% rate, EU membership, no investment requirement, and 183-day residency that grants EU freedom of movement. Andorra's advantages are the lower VAT, the mountain lifestyle, and the privacy/stability of a principality banking system that operates outside EU regulatory frameworks — meaningful to some high-net-worth individuals.

For territorial tax countries — where foreign-source income is simply exempt from local tax — Georgia and Paraguay often make stronger structural sense for Americans because they remove a layer of complexity entirely. Andorra taxes global income once you're resident, which still requires FTC/FEIE management for US citizens.

Practical Steps to Establish Andorran Residency

- Choose your residency type — Active (run a business, 183+ days) vs. Passive (invest €1M+, 90 days minimum)

- Engage a local law firm — Andorran immigration attorneys handle the company setup (active) or investment structure (passive). Budget €5,000–€15,000 in professional fees

- Secure accommodation — A lease or property purchase is required before the application; most applicants rent first

- Gather documents — Apostilled criminal background check, medical certificate from an Andorran-licensed physician, proof of income or investment, valid health insurance

- Submit to Servei d'Immigració — Andorra's immigration authority; processing takes 2–4 months

- Open an Andorran bank account — Crèdit Andorrà, BancSabadell d'Andorra, and Mora Banc are the main options; expect thorough KYC/AML documentation requirements

- Register with CASS if active — Social security registration is mandatory for active residents and must be done before you begin operating your business

For international money transfers to fund your setup costs or ongoing living expenses, Remitly offers competitive EUR transfer pricing versus traditional bank wire fees of $25–$45 per transaction. For your US banking foundation — which you'll want to maintain — Charles Schwab International remains the gold standard: free global ATM withdrawals, no foreign transaction fees, and a brokerage that doesn't close your account when you move abroad.

To maintain a US address for IRS correspondence, state domicile, and domestic financial accounts while living in Andorra, Traveling Mailbox provides a real US street address in 50+ cities with digital mail scanning and check deposit for $15/month — the site owner uses this personally and it's covered in the virtual mailbox expat guide.

The Verdict

Andorra's 10% flat tax is one of Europe's cleanest — but it's not a cheap or frictionless option. The passive residency investment threshold jumped to €1,000,000 in January 2026, pricing out most middle-income earners. Active residency requires 183 days and a real business presence in a country with no airport and a tiny domestic market.

What Andorra does deliver — for the right profile — is a legitimate, stable, and internationally recognized residency anchored by a genuinely low tax code. No wealth tax, no inheritance tax, capital gains mostly untaxed, and a 4.5% VAT that makes neighboring countries feel gouged every time they buy a coffee.

If you hold a European passport, earn high remote income, and want to split time between ski slopes and a growing Pyrenean entrepreneurial community without surrendering 40% of your income to a national government, Andorra deserves serious due diligence — not as a loophole, but as a legitimate small-country advantage that's been available for decades while most expats looked elsewhere.

If you're American and expecting Andorra to make your IRS problem disappear, start with the FEIE vs. Foreign Tax Credit breakdown first. The math still works at higher income levels — it just requires more planning than the brochures suggest.

Financial Disclaimer: This article is for informational and educational purposes only. It does not constitute tax, legal, or financial advice. Tax laws and residency requirements change frequently — the January 2026 Omnibus 2 changes to Andorran passive residency thresholds are one example. Always consult a qualified CPA experienced in US expat tax law and a licensed Andorran attorney before making any residency or investment decisions. Individual tax situations vary significantly.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageMay 28, 2026

Geographic ArbitrageMay 28, 2026

Vietnam Expat Guide: $1,200/Month, Zero Foreign Tax

Vietnam costs ~$1,200/month for a comfortable expat life and taxes foreign income at 0% if you stay under 183 days. Complete guide for US expats.

Geographic ArbitrageMay 3, 2026

Geographic ArbitrageMay 3, 2026

Andorra Tax Residency: Europe's Hidden 10% Tax Haven

Andorra offers 10% max income tax, zero inheritance tax, and 4.5% VAT. Full 2026 guide to residency options, costs, and the US expat catch.

Geographic ArbitrageJune 1, 2026

Geographic ArbitrageJune 1, 2026

Paraguay Tax Residency: Earn Globally, Pay Zero

Paraguay taxes 0% on foreign income. Get legal residency for under $2,000, visit once every 3 years. Complete 2026 guide for US expats.