You filed your FEIE, zeroed out your federal tax bill, and felt like a genius. Then your accountant calls. California wants $17,290 — on the same income you just excluded from federal taxes.

This is the state tax domicile trap. Moving abroad does not automatically end your US state tax obligations. Several states — particularly California and New York — actively pursue their former residents who live overseas, sometimes for years after they've left. Understanding how state domicile works, which states are aggressive, and how to cut ties correctly is one of the most valuable financial moves you can make before relocating.

Your FEIE Won't Save You From This

The Foreign Earned Income Exclusion is a federal benefit. It lets you exclude up to $130,000 of foreign-earned income (2025 figure) from your federal taxable income. It does exactly nothing for state taxes.

States calculate income tax independently. If California considers you a domiciliary — a legal resident for tax purposes — it taxes your worldwide income at rates up to 13.3%, regardless of what happened on your federal return. That $130,000 you excluded federally? California sees it in full.

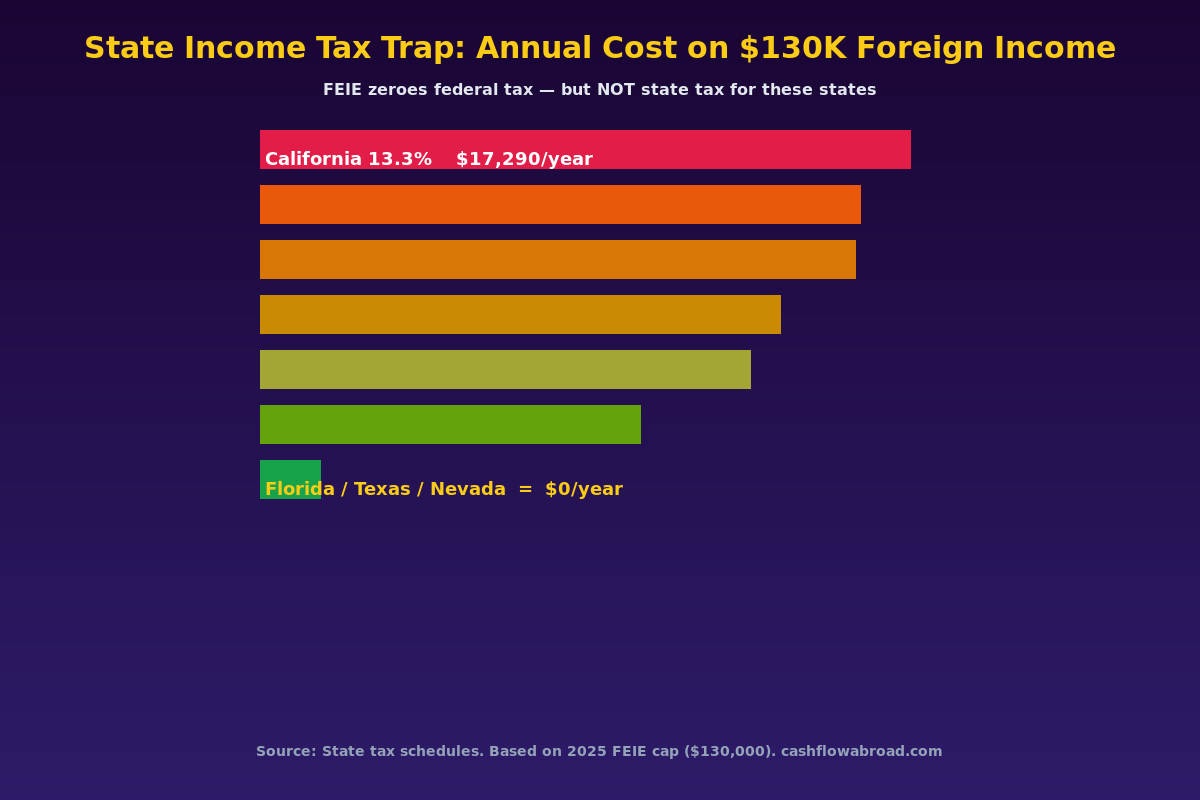

The math is punishing:

| State | Top Rate | Annual Tax on $130K | 5-Year Exposure |

|---|---|---|---|

| California | 13.3% | $17,290 | $86,450+ |

| New York | 10.9% | $14,170 | $70,850+ |

| New Jersey | 10.75% | $13,975 | $69,875+ |

| Oregon | 9.9% | $12,870 | $64,350+ |

| Minnesota | 9.85% | $12,805 | $64,025+ |

| Virginia | 5.75% | $7,475 | $37,375+ |

| Florida / Texas / Nevada | 0% | $0 | $0 |

These numbers assume income at the FEIE cap. At higher income levels, the exposure is steeper. California's standard late-payment penalty rate is 5% per year on unpaid balances — and audits can land years after you've left.

Domicile vs. Residency: The Distinction That Costs Expats Money

Most people conflate these terms. They're legally different, and that difference is expensive.

Residency is where you physically live. You can be a resident of Portugal, Colombia, or Thailand while still being a domiciliary of California.

Domicile is your "permanent home" — the place where you intend to return when you've finished your time abroad. Under California law, you can only have one domicile at a time, and you don't change it simply by leaving the country. You change it by establishing a new permanent home somewhere else with the genuine intent to remain there indefinitely.

Here's where the trap snaps shut: if you moved from San Francisco to Medellín without formally establishing a new domicile first, California presumes you're still a California domiciliary. The longer you wait to fix it, the more back taxes, interest, and penalties accumulate.

The Most Aggressive States (And What They Look For)

California: The Hardest State to Escape

California's Franchise Tax Board is notoriously aggressive about auditing former residents who claim to have moved. The FTB uses a totality-of-circumstances test that weighs dozens of factors:

- Where your spouse and minor children live

- Location of your "most prized possessions" — art, collections, family heirlooms

- Where you maintain your principal bank accounts

- Location of your doctors, dentists, lawyers, and accountants

- Where you're registered to vote

- Where your vehicles are registered

- Whether you maintain a California storage unit, gym membership, or club membership

Moving abroad actually works against you in California's analysis. If you left the US rather than moving to another state, the FTB tends to assume you intend to return to California eventually. Renting out your old California home while abroad? That's evidence you plan to return.

California audits can arrive years after you left. A former San Diego resident living in Vietnam might receive an audit notice covering three prior tax years — which is why getting this right before you leave is far cheaper than fixing it afterward.

New York: Two Traps in One

New York has a two-track trap. Even if you've broken domicile, you can still be taxed as a "statutory resident" if you:

- Maintain a "permanent place of abode" in New York (even if you're rarely there), AND

- Spend more than 183 days per year in New York

If your spouse kept the Manhattan apartment and you visit for extended periods, you could trigger statutory residency. New York defines "day" broadly — any part of a day counts, including transit time spent in JFK or LaGuardia with a connection delay.

Breaking New York domicile requires demonstrating change across five objective factors (the PORCH test): Place of abode, Objects of value, Revenue sources, Connections, and time Here. New York's Division of Tax Appeals has rejected domicile changes from people who moved abroad but didn't document their break thoroughly.

Other States That Pursue Expats

| State | What Makes It Difficult | Top Rate |

|---|---|---|

| New Jersey | Presumes NJ domicile for anyone who lived there; tracks voter registration and driver's license | 10.75% |

| Virginia | 183-day presence test; audits former military and federal employees claiming domicile change | 5.75% |

| South Carolina | Broadly defines "resident"; pursues expats who maintain SC driver's licenses | 6.4% |

| New Mexico | Taxes income from all sources for domiciliaries; limited reciprocity agreements | 5.9% |

The Easy Exit States

Nine states have no individual income tax: Florida, Texas, Nevada, Washington, Wyoming, Alaska, South Dakota, Tennessee, and New Hampshire (NH taxes investment income but is phasing that out). These states do not audit departing residents for income tax purposes.

The most popular expat move: establish Florida domicile before leaving the US. What that requires:

- Filing a Florida Declaration of Domicile at the county courthouse ($10 fee)

- Getting a Florida driver's license

- Registering to vote in Florida

- Updating your IRS address (Form 8822) to a Florida address

- Changing bank account and brokerage addresses to Florida

- Spending at least 31 days in Florida before departure

You need a physical Florida address — not a P.O. box. This is where a virtual mailbox becomes essential. Traveling Mailbox provides real street addresses in 50+ US cities (including several Florida cities) starting at about $15/month. Mail gets scanned digitally and forwarded on request. It satisfies the IRS, state DMVs, and financial institutions that require a physical US address. The site owner personally uses this service for exactly this purpose — more detail in the full virtual mailbox guide for expats.

How to Break Domicile Before You Leave

The domicile change needs to happen before your last day in your high-tax state. Once you're abroad, it's harder to execute the steps cleanly — and easier for your former state to argue you didn't fully commit.

The documented sequence that works:

- Choose your new domicile state. Florida, Texas, and Nevada are most popular. South Dakota is useful for expats who want favorable trust laws and simple residency documentation requirements.

- Get a physical address in that state. Rent an Airbnb for a week, stay with family, or use a virtual mailbox with a real street address. You need this address to start updating documents.

- File the Declaration of Domicile (Florida) or equivalent. Texas and Nevada have no formal filing, so you need comprehensive documentation instead.

- Surrender your old driver's license and get a new one. This is one of the most heavily weighted factors in domicile audits. A California DL while claiming Florida domicile is a red flag.

- Update all financial accounts. Banks, brokerages, credit cards, insurance. Charles Schwab's international account is popular among expats — it supports expat clients explicitly, rebates all ATM fees worldwide, and doesn't require you to close your account when you move abroad.

- File your last high-tax state return as a part-year resident. Your last California return should show you left mid-year. Filing as a full-year resident in your departure year is a mistake that locks in domicile for that year.

- File your new state's return showing you established residency there (even if only for a few weeks before departing).

- Keep a domicile file. Document everything: receipts, DMV records, the Declaration of Domicile filing, bank statements, utility bills. If audited three years later, this file is your entire defense.

If You Already Left Without Breaking Domicile

This is fixable — but requires prompt action. The longer you wait, the more years of potential liability accumulate.

First, assess whether your former state is actually tracking you. California is most likely to if you: earned income reportable to the state (1099s, K-1s with California-source income, rental income from California property), filed California returns in prior years, or maintained any California-connected accounts or business entities.

One critical nuance: if you have California-source income (a California LLC, rental property, clients in California), you may owe taxes regardless of domicile. California taxes California-source income even for non-residents. That's a separate issue from the domicile question — and one that requires its own planning.

To fix a missed domicile change after departure:

- Establish domicile in a no-tax state now, even while abroad — use a virtual mailbox, update documents, get a new driver's license

- File amended returns for years where you mistakenly filed as a California or New York resident when you qualified as a nonresident

- Consult an expat CPA who specializes in state tax, not just federal — the full expat banking and tax guide has guidance on finding the right professional

Keeping US Banking Intact While Abroad

There's a practical challenge that intersects with domicile: US banks frequently close accounts when you update to a foreign address. This is why the virtual mailbox + no-tax state strategy works hand-in-hand with expat banking setup.

With a Florida street address through Traveling Mailbox, you keep your existing US accounts by maintaining a domestic address on file. Charles Schwab International explicitly supports US expat clients and rebates 100% of ATM fees worldwide — so you can withdraw local currency anywhere without getting hit with fees. For US business banking abroad, Mercury doesn't require a US residential address for its business accounts.

The Geographic Arbitrage Math

Expats pursuing geographic arbitrage typically focus on cost-of-living differences. But the tax geography matters just as much — and state domicile is the piece most people miss.

Consider an American earning $130,000 remotely, living in Medellín (cost of living roughly $1,800–2,500/month versus $5,000+ in San Francisco):

- Living expense savings vs. San Francisco: ~$36,000/year

- Federal tax savings via FEIE: ~$25,000/year (estimated at this income level)

- California state taxes — if domicile isn't broken: -$17,290/year

Breaking California domicile before leaving — a one-time process — saves $17,290 per year in perpetuity. Professional help typically runs $1,500–3,000 in CPA and attorney fees. Payback period: under five weeks of state tax savings.

What to Do Before You Leave

If you're planning to move abroad within the next 12 months:

- Identify your state's domicile rules now. California and New York require the most lead time — start the domicile break 60–90 days before departure, not the week before.

- Hire a CPA who specializes in expat state taxes. The federal piece is mostly standardized; state domicile strategy is where the real money is saved.

- Secure a no-tax state address. A virtual mailbox in Florida or Texas anchors your domicile. Traveling Mailbox at $15/month provides a real street address — not a P.O. box — plus mail scanning and check deposit forwarding.

- Update every document in sequence. Driver's license → voter registration → bank accounts → IRS Form 8822 → investment accounts. Order matters; auditors look for consistency.

- File your departure year returns correctly. Part-year resident in your high-tax state, resident in your new no-tax state. This is the year most people make errors.

- Keep your domicile file forever. There's no statute of limitations on unfiled California returns. The documentation you build now protects you for decades.

The FEIE is powerful. Living in a territorial-tax country takes things further. But neither fully works if your former state is still quietly tallying what you owe. Fix domicile first — everything else in your expat financial strategy is built on top of that foundation.

For the full expat estate planning picture, including how domicile interacts with inheritance and trust structures, see our expat estate planning guide.

Financial Disclaimer: This article is for informational purposes only and does not constitute legal or tax advice. State domicile law is complex and varies by jurisdiction. Tax rates and thresholds cited reflect 2025 published schedules and may change. Consult a licensed CPA or tax attorney with expertise in US expat state taxation before making decisions about your domicile status or tax filing obligations.