Spain's Beckham Law: Pay 24% Tax for 6 Years as an Expat

Spain taxes income at up to 47%—but new arrivals can lock in 24% flat and exempt all foreign income for six years under the Beckham Law.

Spain's Beckham Law locks in a 24% flat tax rate and exempts foreign income for 6 years. Full guide: eligibility, application, US citizen pitfalls.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Spain is the country where people go to pay 47% income tax and feel good about the weather. At least, that's the assumption. The reality for new arrivals is radically different: under the Beckham Law, you can lock in a flat 24% rate on Spanish-sourced income—and exempt virtually all your foreign income from Spanish tax entirely—for six consecutive years. On a €150,000 salary, that's a difference of roughly €21,000 per year compared to the standard IRPF scale. Over six years, that compounds to over €126,000 in tax you keep.

Most people searching for low-tax expat destinations immediately think of Dubai, Paraguay, or Georgia. Spain rarely comes up. That's the arbitrage opportunity hiding in plain sight.

What Is the Beckham Law?

Officially called the Régimen Especial para Trabajadores Desplazados (Special Tax Regime for Inbound Workers), the law was introduced in 2005 largely to attract high-earning foreign professionals and, yes, footballers like David Beckham—hence the nickname. The Startups Act of 2022 (Law 28/2022) dramatically expanded eligibility to include digital nomads, remote workers, and startup founders, making it relevant to a much broader expat audience.

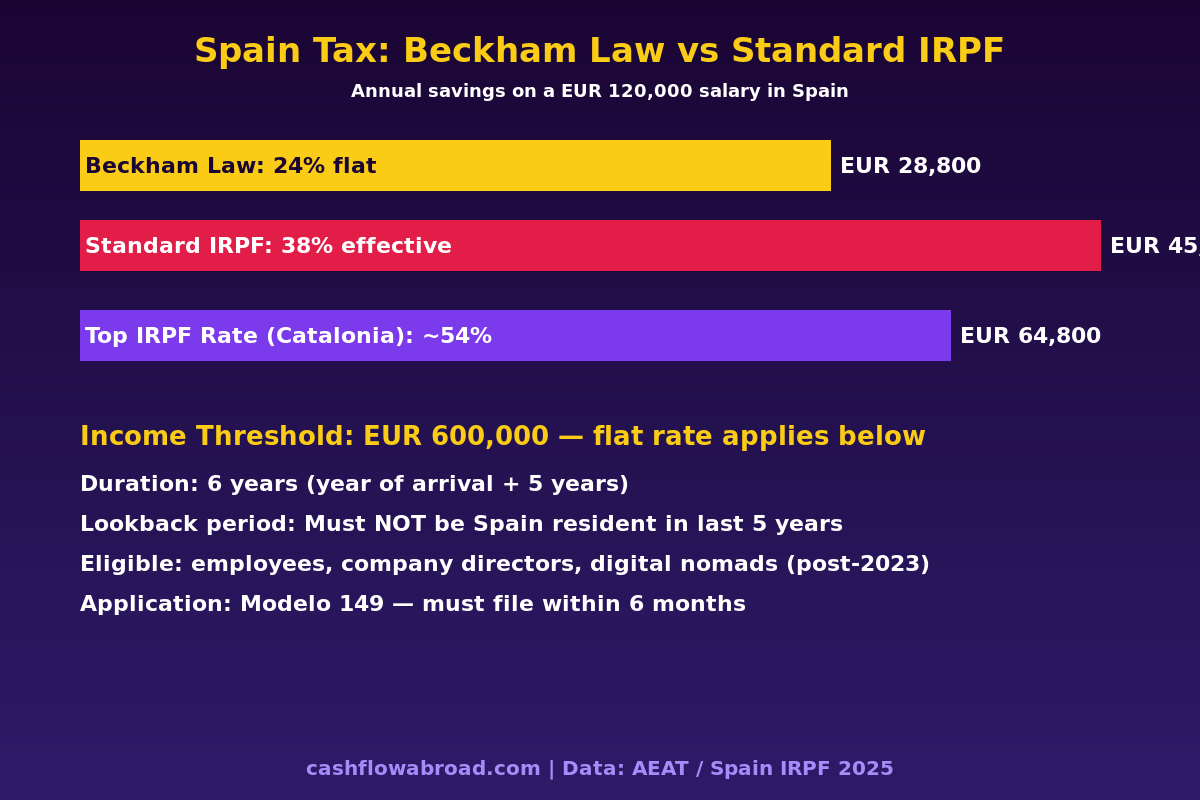

Under the standard Spanish income tax (IRPF), residents face progressive rates from 19% on the first €12,450 up to 47% on income above €300,000. Factor in regional surcharges in places like Catalonia and the effective marginal rate can hit 54%. The Beckham Law replaces all of this with a single flat rate: 24% on Spanish-sourced income up to €600,000. Above that threshold, the rate is 47%—but very few people earn more than €600k from Spanish sources.

The foreign income exemption is where it gets genuinely powerful. Dividends, interest, rental income, and capital gains from assets held outside Spain are generally not taxed in Spain at all during the Beckham period. If you run a US-based S-corp, own rental properties in Texas, or earn dividend income from a US brokerage, Spain won't touch it.

How Much Do You Actually Save?

The numbers below compare tax liability under the Beckham Law versus the standard IRPF regime, based on Spanish-sourced employment income only. Actual effective rates vary slightly by region due to autonomous community surcharges.

| Annual Income (EUR) | Beckham Law (24% flat) | Standard IRPF (est.) | Annual Saving | 6-Year Total Saving |

|---|---|---|---|---|

| €50,000 | €12,000 | ~€16,000 | ~€4,000 | ~€24,000 |

| €80,000 | €19,200 | ~€28,000 | ~€8,800 | ~€52,800 |

| €120,000 | €28,800 | ~€46,000 | ~€17,200 | ~€103,200 |

| €150,000 | €36,000 | ~€57,000 | ~€21,000 | ~€126,000 |

| €200,000 | €48,000 | ~€76,000 | ~€28,000 | ~€168,000 |

The regime also shields you from Spain's Wealth Tax on foreign assets. Spanish residents normally pay up to 3.5% annually on net assets above €700,000. Under the Beckham Law, that tax applies only to assets physically located in Spain—so your US brokerage account, US real estate, and offshore savings are outside the scope.

Who Qualifies for the Beckham Law?

There are five eligibility categories under the expanded 2022 rules. You need to fall into at least one:

- Employee of a foreign company — You're hired by a non-Spanish employer and relocate to Spain to work.

- Digital nomad visa holder — You work remotely for non-Spanish clients or an employer outside Spain while physically based in Spain on the Digital Nomad Visa (International Telework Authorization).

- Startup founder or director — You're a director or key employee at a startup or innovative company recognized under Law 28/2022.

- Highly qualified professional — You hold a postgraduate degree and work in a qualifying field, including R&D, science, and technology.

- Investor (qualified) — Active investor managing or acquiring stakes in Spanish ventures under certain criteria.

The universal requirements regardless of category:

- You must not have been a Spanish tax resident in the five years before arriving. Spent a summer in Malaga in 2020? That probably doesn't disqualify you, but being formally tax-resident does.

- You must perform at least 85% of your work from within Spain.

- You must become a Spanish tax resident—meaning you spend 183+ days per year in Spain.

Traditional autónomos (self-employed freelancers) without a qualifying digital nomad visa or startup connection are generally excluded. If you're a freelancer planning to move to Spain, the Digital Nomad Visa route is the cleaner path to Beckham eligibility.

The Digital Nomad Visa Connection

Spain launched the International Telework Visa in 2023 under the Startups Act. It's designed specifically for remote workers employed by or contracting with companies outside Spain. The visa explicitly qualifies holders for the Beckham Law, confirmed by Spanish court rulings in 2025—removing prior ambiguity about whether remote workers could access the regime.

Key requirements for the Digital Nomad Visa:

| Requirement | Detail |

|---|---|

| Minimum income | €2,762/month (200% of Spain's minimum wage, confirmed through 2026) |

| Income source | Must come from entities outside Spain; no more than 20% from Spanish clients |

| Health insurance | Full coverage in Spain required for the duration of stay |

| Clean criminal record | Certificate from home country (must be apostilled) |

| Application fee | ~€80 consular fee + ~€73 residence card fee (~€300–700 total) |

| Processing time | Officially 10–45 days; budget 2–4 months end-to-end |

| Validity | 1 year initial; renewable up to 5 years total |

For health insurance, SafetyWing's Nomad Health plan covers Spain and satisfies the visa requirement. Premiums run $100–$180/month depending on age—far cheaper than most private expat health plans. Compare this to other European digital nomad visas in our full digital nomad visa rankings.

Step-by-Step: Applying for the Beckham Law

This is where applicants lose the benefit most often—not by being ineligible, but by missing a filing deadline or using the wrong form. The sequence matters.

- Arrive and register your address — Get your empadronamiento (municipal registration) at your local town hall within 30 days of arriving.

- Get your NIE — Your Número de Identidad de Extranjero is your Spanish tax ID. Cost: approximately €9.84.

- Register with Social Security — This is the critical clock-starter. The 6-month Beckham Law filing window begins from this date—not from visa approval, not from when you landed.

- File Modelo 030 — Registers you with the Spanish tax authority (Agencia Tributaria).

- File Modelo 149 — The formal opt-in election for the Beckham Law. Must be filed within 6 months of Social Security registration. Missing this deadline is permanent.

- Receive confirmation — The Agencia Tributaria issues an acknowledgment, which can take up to 2 months. File Modelo 149 early to give yourself runway.

- File annual returns using Modelo 151 — Instead of the standard Modelo 100, Beckham participants use Modelo 151 to report Spanish income at the 24% flat rate.

The most common failure point: applicants assume the deadline runs from visa approval or physical arrival. It runs from Social Security registration. Once registered, file Modelo 149 immediately—don't wait until you understand every detail of Spanish tax law.

US Citizens: What Beckham Does and Doesn't Fix

If you're American, the Beckham Law delivers real tax savings in Spain. It does not eliminate your US filing obligations.

The IRS taxes US citizens on worldwide income regardless of residence. Under Beckham, your Spanish income is taxed at 24%. You can generally claim a Foreign Tax Credit (FTC) on your US return for Spanish taxes paid, which reduces your US bill dollar-for-dollar. For most earners, this eliminates most additional US tax owed on the Spanish portion.

The complication is your foreign income that Spain exempts under Beckham. If Spain doesn't tax it, there's no foreign tax to credit against the US tax owed on that same income. The Foreign Earned Income Exclusion (FEIE) can shelter up to $130,000 (2025 figure) of foreign-earned income from US tax, but you can't claim both FEIE and FTC on the same dollars—and using FEIE creates complications with IRA contributions.

The standard approach for US expats under Beckham:

- Use the Foreign Tax Credit on Spanish employment income—Spain taxes it at 24%, you credit that against your US liability.

- For foreign-source income Spain doesn't tax (dividends, capital gains), evaluate FEIE or FTC from other treaty partners. This requires a dual-qualified tax professional.

- FBAR still applies: Spanish bank accounts above $10,000 trigger FinCEN 114. Foreign assets above $200,000 (married abroad) trigger Form 8938.

See our full guide to US expat banking and taxes for the foundational framework that applies in every expat jurisdiction.

Banking and Financial Setup in Spain

You'll need a Spanish bank account for rent, utilities, and Social Security contributions. Opening one requires your NIE and proof of address. CaixaBank, Banco Santander, and Sabadell all offer English-language service in major cities. For lower fees, N26 and Revolut operate in Spain with Spanish IBANs and no monthly fees for basic accounts.

Keep your US accounts intact. The Charles Schwab International account continues to work from Spain—no account closures, no ATM fees globally, and you can hold US-domiciled funds without triggering the PFIC rules that catch expats who invest in local foreign funds. See our expat investing guide for why protecting your US brokerage access is critical.

For maintaining a US mailing address—required to keep US bank accounts functional and satisfy IRS correspondence requirements—Traveling Mailbox provides a real US street address in 50+ cities with mail scanning and check deposits for $15/month. This is a standard piece of infrastructure for every American expat.

What Spain Actually Costs

The tax advantage compounds when set against Spain's cost of living, which runs meaningfully below Northern Europe or comparable US metros.

| Expense | Madrid | Barcelona | Valencia / Málaga |

|---|---|---|---|

| 1-bed apartment (city center) | €1,200–1,800/mo | €1,300–2,000/mo | €800–1,300/mo |

| Monthly food (couple) | €400–600 | €400–650 | €300–500 |

| Transport (monthly metro pass) | €55 | €80 | €40–50 |

| Utilities (electricity, gas, water) | €80–130/mo | €90–140/mo | €70–110/mo |

| Health insurance (private, expat) | €100–200/mo | €100–200/mo | €80–180/mo |

| All-in monthly budget (single) | ~€2,500–3,500 | ~€2,700–3,800 | ~€1,800–2,800 |

Valencia and Málaga are the standout value plays—significantly cheaper rent than Madrid or Barcelona, excellent infrastructure, warm climate, and growing international communities. Málaga in particular has seen Google, Vodafone, and Oracle establish major operations since 2022, making it increasingly viable for tech workers beyond pure remote freelancers.

Five Mistakes That Kill the Beckham Benefit

1. Missing the Modelo 149 deadline

The 6-month clock starts at Social Security registration, not arrival or visa approval. Once registered, file immediately. The approval takes up to 2 months—you want that window cushioned.

2. Assuming the Digital Nomad Visa auto-enrolls you

The visa grants legal residence. The Beckham tax regime requires a separate opt-in via Modelo 149. Having the visa and not filing Modelo 149 means you pay standard IRPF rates. This is a surprisingly common and expensive mistake.

3. Thinking standard autónomo status qualifies

Traditional self-employed freelancers without the Digital Nomad Visa are excluded from the Beckham regime. The visa is the bridge. Apply for the DNV first; then Beckham.

4. Misreading the 5-year residency lookback

You cannot have been a Spanish tax resident in any of the five calendar years before your arrival year. Studying in Spain years ago, a prior work stint, or even a long summer with registered residency can disqualify you. Check your history carefully before applying.

5. Skipping the dual tax professional

Americans in Spain under the Beckham Law are navigating two sophisticated systems simultaneously. Budget for a US CPA familiar with international taxation and a Spanish gestor (tax advisor) who knows the Beckham regime. The coordination between IRPF, FTC, FBAR, and FEIE requires specialist knowledge that generalists on either side often lack.

When the Six Years End

At the end of year six, you revert to standard IRPF. This is a predictable cliff that requires planning well before it arrives. The main options:

- Leave Spain strategically — Six years of tax savings can fund a move to a territorial tax jurisdiction like Paraguay or Georgia, where foreign income isn't taxed indefinitely.

- Restructure income — Under standard IRPF, shifting income from employment to dividends or capital gains (taxed at 19–28%) becomes more valuable. Plan the transition structure while still in the Beckham period.

- Optimize within IRPF — Spanish pension contributions, mortgage deductions in some autonomous communities, and family allowances reduce the IRPF burden more than most expats realize once they start working within the system.

The Beckham years should be treated as a concentrated wealth-building window—invest the difference, not just spend it. The broader framework in our geographic arbitrage playbook applies: the biggest gains come from combining lower taxes with lower costs and higher savings rates simultaneously.

Bottom Line

Spain's Beckham Law is the most underrated tax structure in Europe for expats. At 24% flat on Spanish income and zero on foreign income for six years, it outperforms most territorial tax regimes—and it comes packaged with EU legal stability, a first-world healthcare system, and cities that people genuinely want to live in. The administrative requirements are real: you need the Digital Nomad Visa, Modelo 149 filed within 6 months of Social Security registration, and a tax professional who knows both Spanish and US law. Those three things, handled correctly, unlock six years of compounding at rates most Americans only pay in their lowest tax bracket.

Financial and tax disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Spanish tax law and visa requirements change regularly; individual circumstances vary significantly. Consult a qualified Spanish gestor and/or US CPA with international experience before making any decisions about Spanish residency or the Beckham Law regime.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 3, 2026

Expat Tax & FinanceMay 3, 2026

The FEIE Retirement Trap: Why Your Tax Break Costs More

Claiming the FEIE can zero out your Solo 401(k) and IRA contribution limits. Learn how the 5-year lock-in affects self-employed expats.

Expat Tax & FinanceAugust 7, 2026

Expat Tax & FinanceAugust 7, 2026

Use a 529 at Foreign Universities

Use 529 funds abroad safely: verify foreign school eligibility, document qualified costs, and avoid taxable withdrawal mistakes.

Expat Tax & FinanceAugust 4, 2026

Expat Tax & FinanceAugust 4, 2026

Form 8833 For Expats: Treaty Disclosure

Learn when expats use Form 8833 for treaty disclosure, common exceptions, dual-resident risks, and how to avoid $1,000 penalties.