For decades, the US government quietly docked the Social Security checks of millions of Americans who had the audacity to also earn a foreign pension. No announcement. No clear explanation. Just a silent formula — the Windfall Elimination Provision — that could cut your monthly benefit by up to $587 without most people understanding why. An American nurse who spent 15 years in the UK before retiring in Florida got less Social Security than her neighbor who never left the country, because her NHS pension was treated as a strike against her.

That changed on January 5, 2025, when President Biden signed the Social Security Fairness Act (HR 82). It repealed both the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO), effective retroactively to January 2024. For US expats with foreign pensions — UK National Insurance, Canadian CPP, Australian Super, German Rentenversicherung — this is one of the most consequential policy wins in decades. Here's exactly what it means for your money.

What the WEP Was (And Why It Was Infuriating)

Social Security's benefit formula is deliberately progressive. Low lifetime earners get back a higher percentage of their wages than high earners — 90% of the first "bend point" in earnings versus 32% and 15% at higher tiers. The idea: protect people who spent their working lives in low-wage jobs.

The Windfall Elimination Provision exploited a quirk in this formula. If you worked partly in jobs that didn't withhold Social Security taxes — foreign employers, many state and local government jobs — your Social Security earnings record looked sparse. The formula saw you as a low earner and applied the generous 90% factor to your first bend point. The WEP assumed that was a windfall you didn't deserve, and it slashed that 90% factor down to as low as 40%.

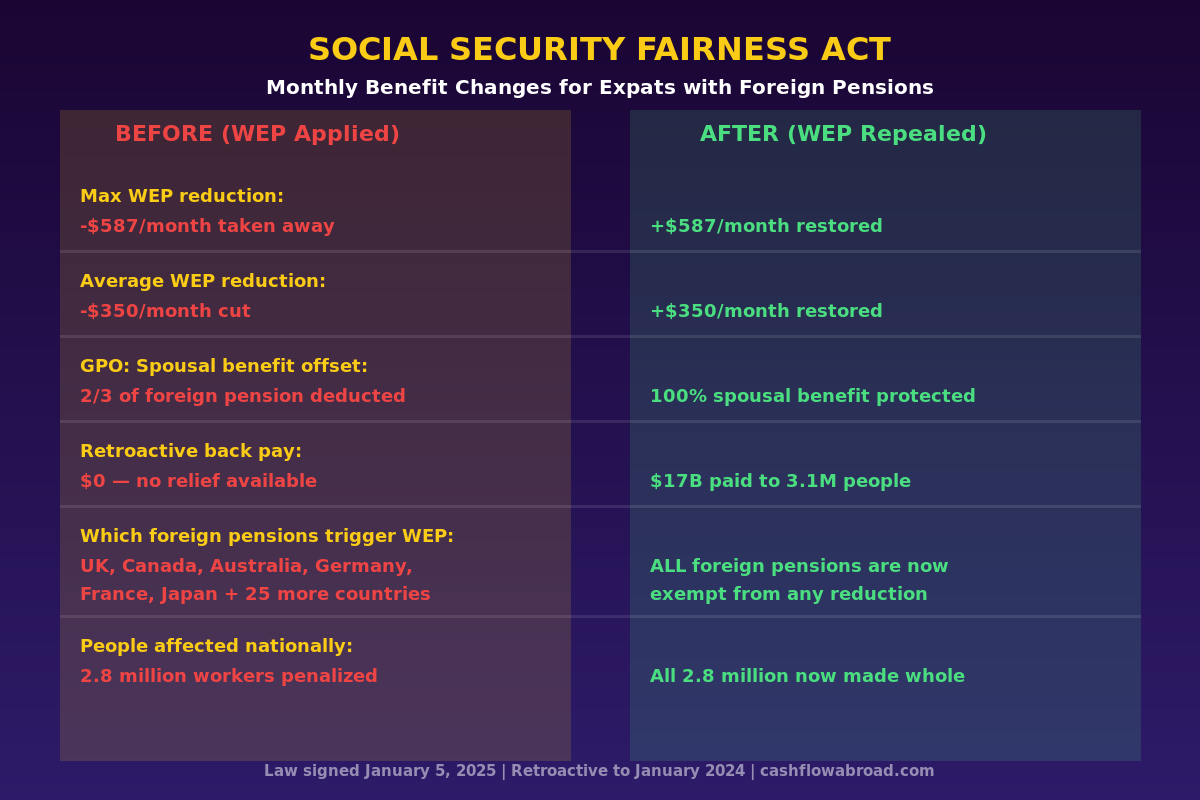

In practice, that meant a reduction of up to $587/month in 2024 — the exact amount depending on how many years of "substantial" US Social Security-covered earnings you had. Fewer than 20 qualifying years: maximum penalty. More than 30 years: no WEP at all. Each year between 20 and 30 reduced the penalty by 5 percentage points.

The "substantial earnings" threshold for 2024 was $31,275 in Social Security-covered income per year — meaning only years where you earned above that threshold counted. Expats often had gaps in their US earnings record precisely because they were working abroad during prime earning years.

The average WEP reduction was approximately $350/month. Over a 20-year retirement, that's $84,000 lost — silently, without most affected retirees fully understanding the cause.

The GPO: When Spouses Got Hit Even Harder

The Government Pension Offset was worse for surviving spouses and dependents. Under GPO, if you received any pension from non-covered employment — including a foreign government pension — your Social Security spousal or survivor benefit was reduced by two-thirds of your pension amount.

There was no cap. A widow with a $3,000/month UK State Pension would lose $2,000 from any Social Security survivor benefit she'd otherwise claim based on her late husband's record. For those with large enough foreign pensions, this wiped out the spousal benefit entirely.

GPO affected roughly 800,000 people nationally — primarily women, since spousal and survivor benefits skew female. Many didn't discover the offset until they applied for benefits and saw a number dramatically lower than expected.

The New Law: What Changed on January 5, 2025

Both provisions are now gone. The Social Security Fairness Act repealed WEP and GPO completely, effective for benefits paid for months after December 2023. That retroactive date matters: if you were receiving a reduced benefit in 2024, you're owed a lump-sum back payment covering every month you were shortchanged.

The SSA began processing retroactive payments on February 24, 2025. By July 7, 2025, the agency had completed 3.1 million payments totaling $17 billion — finishing five months ahead of the statutory deadline. For most affected beneficiaries, the back payment landed as a one-time deposit in March or April 2025, with the higher ongoing monthly amount starting in April 2025 (for March 2025 benefits).

What the Numbers Look Like Now

| Scenario | Old Monthly Benefit (with WEP/GPO) | New Monthly Benefit | Monthly Increase |

|---|---|---|---|

| Max WEP reduction (fewer than 20 qualifying years) | Reduced by $587 | Full amount restored | +$587/month |

| Average WEP case | Reduced by ~$350 | Full amount restored | +$350/month |

| GPO: widow with $3,000/month foreign pension | Lost $2,000 from spousal benefit | Full spousal benefit | +$2,000/month |

| GPO: total elimination of spousal benefit | $0 spousal/survivor benefit | Full entitlement restored | Varies |

The average monthly increase post-repeal is approximately $360/month. Annualized, that's $4,320 per year in restored benefits — significant for retirees on fixed incomes.

Which Foreign Pensions Were Affected (And Now Aren't)

The WEP applied to any pension from employment that didn't withhold US Social Security taxes — which includes virtually all foreign employers. If you worked abroad for a foreign company or government, your salary wasn't subject to FICA. If you also qualified for that country's state pension, that pension triggered WEP when you applied for US Social Security.

This is now completely irrelevant. Your foreign pension has zero effect on your US Social Security calculation. Here's the country-by-country picture:

| Country | Pension System | US Totalization Agreement? | WEP Status Now |

|---|---|---|---|

| United Kingdom | UK State Pension / National Insurance | Yes | No reduction — fully protected |

| Canada | CPP / QPP | Yes | No reduction — fully protected |

| Australia | Superannuation | Yes | No reduction — fully protected |

| Germany | Rentenversicherung | Yes | No reduction — fully protected |

| France | Régime Général | Yes | No reduction — fully protected |

| Japan | Kosei Nenkin | Yes | No reduction — fully protected |

| Thailand / Philippines / UAE / India | Various national pensions | No | No reduction — fully protected |

The critical point for expats in countries without US totalization agreements: WEP repeal helps you whether or not a totalization agreement exists. Under the old rules, non-totalization countries were the worst of both worlds — your foreign pension triggered WEP, and you couldn't even combine foreign work credits with your US record to meet the 40-quarter eligibility threshold. The WEP repeal fixes the penalty half of that equation.

Totalization Agreements: Still Useful, Now Better

The US has totalization agreements with 31 countries as of 2025 (UK, Canada, Australia, Germany, France, Japan, Ireland, Italy, Netherlands, Spain, Switzerland, and more). These serve two functions that remain fully in force:

- Eliminate dual Social Security taxation — if you're working in Germany for a German employer, you pay into German social insurance, not simultaneously into US Social Security

- Allow combining work credits — if you have 28 US Social Security quarters and worked 8 years in the UK, those UK credits can be combined with your US quarters to meet the 40-quarter eligibility requirement

WEP repeal doesn't affect totalization agreements — they continue to work exactly as before. What changed is that if you used a totalization agreement to qualify for US Social Security, your foreign pension no longer reduces the benefit you receive. Previously, you could use the UK-US agreement to qualify, then watch WEP slash your monthly check anyway. That absurdity is gone.

For more on how totalization agreements work in practice, see our guide to US totalization agreements.

What Expats Should Do Right Now

If You're Already Receiving Benefits

Verify your contact information at ssa.gov/myaccount. This is the single most important step for expats. If SSA has an outdated mailing address or foreign bank account information on file, your retroactive payment and new monthly amount may be delayed or misdirected. The SSA sends notices about the changes by mail to the address on record — if you moved since applying for benefits, update it immediately.

Maintaining a reliable US address is essential for SSA correspondence. A virtual mailbox service like Traveling Mailbox gives you a real US street address in 50+ cities, scans your mail digitally, and deposits any checks — critical infrastructure for expats who need to receive government correspondence without physical US presence. See our full virtual mailbox guide for expats for setup details.

Check whether your payment came through. If you haven't received a retroactive lump sum by mid-2025, contact SSA directly. Expats can reach the international SSA office at 1-410-965-2160 or through the nearest US Embassy or Consulate, many of which have dedicated SSA staff.

If You Haven't Applied Yet

Apply as soon as you're eligible — there's a six-month retroactivity limit on new applications for retirement and survivor benefits that hasn't changed with the SSFA. Every month of delay in applying is a month of the higher, unreduced benefit you won't get back.

One worthwhile strategy: if you have a foreign pension and plan to delay Social Security to age 70 to maximize the delayed retirement credits (8% per year between full retirement age and 70), that calculation just became more valuable. You're now maximizing a larger base benefit. Run the numbers with an expat financial planner who understands both US Social Security and foreign pension systems.

The Tax Trap Nobody Mentions: Your Lump Sum

The retroactive back payment — covering 12-13 months of restored benefits — landed as a single lump sum for most recipients in early 2025. For many, this created a tax problem: a windfall large enough to push them into a higher bracket for the 2025 tax year.

The IRS provides partial relief through the "lump-sum election" method, which lets you calculate taxes as if the back pay had been received in the prior years it covers. This is calculated using Form SSA-1099 and IRS Publication 915 — it doesn't eliminate tax, but can reduce it for the year you received the lump sum.

Key tax facts that haven't changed:

- Social Security benefits are not foreign earned income and cannot be shielded by the Foreign Earned Income Exclusion (FEIE)

- Up to 85% of your Social Security is taxable at ordinary income rates depending on your "combined income" (provisional income) — your increased benefit may push more of your SS into the taxable range

- Canada taxes US Social Security benefits for non-residents at 15% withholding under the US-Canada tax treaty

- Germany may also tax your US Social Security depending on your treaty position

If you're managing investment accounts alongside Social Security as part of your retirement picture, Charles Schwab International remains one of the few US brokerages that genuinely serves expats — with free ATM reimbursements worldwide and no foreign transaction fees on the Schwab Bank account, useful for accessing your Social Security income wherever you are.

Complex Cases: Who May Still Be Waiting

As of early 2026, a subset of affected retirees hadn't received full retroactive payments. SSA acknowledged from the start that cases involving foreign pension documentation, non-standard earnings histories, or non-citizen beneficiaries require case-by-case manual processing. If your situation involves:

- A pension from a country without a US totalization agreement

- Earnings records spanning multiple countries

- A spousal or survivor claim where GPO previously applied

- Benefits routed through a foreign bank account

...contact SSA directly rather than waiting for automatic processing. For receiving your increased Social Security payments internationally with minimal fees, Remitly can transfer USD Social Security deposits to your local bank account abroad at competitive exchange rates.

What WEP Repeal Doesn't Fix

Eligibility gaps remain. If you don't have 40 US Social Security quarters, you may not qualify for US benefits at all — regardless of WEP repeal. Totalization agreements can help you combine credits with the 31 agreement countries, but there's no fix for expats in countries without agreements who have fewer than 40 quarters. For a detailed look at how Social Security interacts with retirement abroad, see our guide to retirement abroad and Social Security.

The FEIE still doesn't cover Social Security income. This hasn't changed, and it's a common misconception among expats who think their entire income is shielded abroad.

Social Security's solvency timeline is slightly worse. The CBO estimated the SSFA will cost approximately $195-200 billion over ten years, moving the Social Security trust fund depletion date roughly six months earlier. This doesn't change anything in the near term but adds to the long-running debate about Social Security reform — which expats with decades of retirement ahead should track.

The Bottom Line

The Social Security Fairness Act is a genuine, meaningful win for US expats who spent years working across borders. WEP and GPO were complex provisions that quietly penalized globally mobile workers — the exact people a modern economy should be rewarding. With both now gone, the playing field is leveled.

If you were subject to WEP or GPO: verify your SSA contact information, confirm your retroactive payment processed, and check that your new monthly amount reflects the full, unreduced benefit. If you're approaching retirement with a mix of US Social Security credits and a foreign pension: remove WEP from your projections entirely and recalculate what you're actually owed.

For the full picture of how Social Security, foreign pensions, and expat tax planning interact, our US expat banking and taxes guide and expat estate planning guide cover the adjacent issues in depth.

Financial disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Social Security rules are complex and individual circumstances vary significantly. Benefit calculations depend on your personal earnings record, which only the SSA can officially determine. Consult a qualified expat tax professional or financial advisor before making decisions based on this information. Affiliate links in this post may earn the site owner a commission at no extra cost to you.