Philippines SRRV: Permanent Residency for $15,000

The Philippines SRRV gives you permanent residency from $15,000 — and you get the deposit back. Here's the full breakdown for US retirees.

The Philippines SRRV offers refundable-deposit permanent residency from $15,000. Full breakdown: costs, taxes, healthcare, and city budgets for US expats.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Most people shopping for residency visas overseas are looking at minimum six-figure deposit requirements, multi-year waiting periods, or citizenship programs that demand a million dollars in real estate. The Philippines offers something genuinely unusual: a permanent-residency visa backed by a deposit you get back in full when you leave, starting at just $15,000. That's not a typo. And unlike most retirement residency programs, it came with a surprise upgrade in September 2025 — the minimum age dropped from 50 to 40, opening it to a whole new generation of semi-retired professionals and early retirees.

What the SRRV Actually Is (and Isn't)

The Special Resident Retiree's Visa (SRRV) is issued by the Philippine Retirement Authority (PRA), a government agency under the Department of Tourism. It is a non-immigrant visa with indefinite multiple-entry privileges — functionally permanent residency, though not citizenship. You can leave and re-enter as many times as you want without reapplying.

The mechanism that makes it accessible is simple: instead of a one-way investment, you deposit money into a PRA-accredited Philippine bank or investment vehicle. That deposit earns returns while you're there, and you retrieve it when you decide to surrender the visa. You're not spending it — you're parking it.

Two categories matter most for Western retirees:

- SRRV Classic — For the general public, ages 40 and up.

- SRRV Courtesy — Preferential rates for retired diplomats, military personnel, and a category called "high achievers." Deposits as low as $1,500–$6,000 apply here, but this guide focuses on Classic.

The Deposit Requirements in Full

The September 2025 restructure changed both the minimum age and the deposit tiers. Here's the current breakdown for SRRV Classic:

| Age | Pension Holder | Non-Pension Holder |

|---|---|---|

| 50 and above | $15,000 | $30,000 |

| 40–49 | $25,000 | $50,000 |

To qualify for the lower "pension holder" tier, you need to demonstrate a lifetime pension of roughly $800/month for a single applicant. Social Security income qualifies. A pension from a former employer qualifies. A provable annuity qualifies.

On top of the deposit, you pay a $1,500 application fee for the principal applicant, plus $300 per dependent (spouse and children under 21). The initial annual PRA fee is also due at approval. This fee structure is non-refundable — it's the actual program cost. The deposit itself is not.

What the SRRV Gets You

The practical benefits go beyond just a right to stay:

- Multiple-entry, indefinite stay — No expiration, no annual renewal with immigration, no visa run culture to manage.

- Exempt from BI Annual Report — Most foreign nationals in the Philippines must report annually to the Bureau of Immigration. SRRV holders are exempt.

- One-time duty-free importation — $7,000 worth of household goods and personal effects, importable within 90 days of visa issuance, tax-free. This covers the cost of shipping a substantial amount of belongings.

- Dependent inclusion — Spouse and children under 21 can be added to the visa. Critically, dependent children can enroll in Philippine schools and universities without converting to a student visa.

- Tax exemption on foreign pension and annuities — More on this below, but this is substantial.

Philippines Tax Treatment for SRRV Holders

The Philippines taxes income on a residency-and-source basis. Resident aliens — foreigners who have established domicile in the Philippines — are generally taxed on Philippine-sourced income only. Foreign-sourced income, including pensions and annuities earned abroad, is explicitly exempt from Philippine income tax for SRRV holders.

In plain terms: if your income is a US Social Security payment, a 401(k) distribution, rental income from US property, or dividends from a US brokerage, the Philippines does not touch it. Your Philippine tax liability is zero on that income.

This is a major contrast with countries that tax worldwide income or that have tried to retroactively capture foreign pension income (the Australian Super situation for US expats is a cautionary tale — see our guide on the Australian Super US tax trap).

Capital gains on Philippine assets are subject to Philippine capital gains tax, but most expat retirees are not buying and selling Philippine securities as their primary income strategy. If your portfolio sits in a US brokerage account, it's out of scope for Philippine taxation.

Your US Tax Obligations Don't Change

Moving to the Philippines does not reduce your US tax obligation. The US taxes its citizens on worldwide income regardless of residence. You still file a Form 1040 every year. Your Social Security benefit is still subject to US federal income tax if your combined income exceeds the thresholds. Your IRA distributions still get reported.

The mechanisms for reducing that US tax bill — the Foreign Earned Income Exclusion (FEIE, up to $126,500 in 2024) and the Foreign Tax Credit — still apply. The FEIE covers earned income (freelance work, consulting), not passive income like pensions or investment returns. Since the Philippines doesn't tax your foreign pension, there's no Philippine tax to claim as a credit against that income on your US return — but there's also no double-taxation problem, since the Philippines isn't taxing it to begin with.

The US-Philippines tax treaty exists but contains a "saving clause" that preserves US taxing rights over US citizens, limiting its practical benefit for most American SRRV holders. Our deeper breakdown of how the saving clause works covers this in full.

Bottom line: for a retiree whose income is US Social Security plus IRA distributions, the Philippine tax liability is zero, and the US tax liability is the same as if they'd never left the US. The financial gain from the Philippines is purely on the spending side.

The Real Monthly Numbers

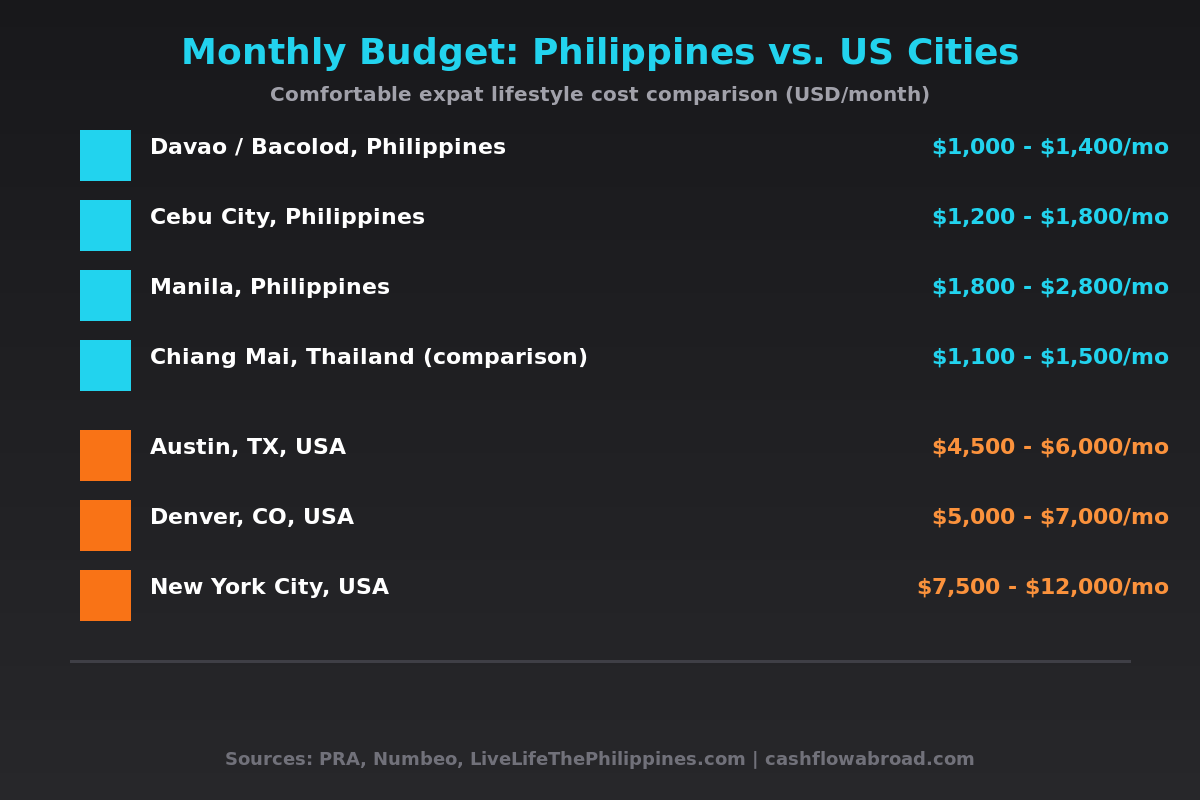

The Philippines is not the cheapest country in Southeast Asia for expats — Chiang Mai and Hanoi often beat it on housing. But it has advantages that matter to American retirees: English is an official language, the dollar exchange rate is favorable (roughly ₱56–58 per USD as of 2026), and the culture has deep American roots from the colonial period. You don't need a translator to see a doctor.

City-by-City Budget Breakdown

| City | 1BR Rent/Mo | Comfortable Monthly Budget | Character |

|---|---|---|---|

| Davao City | $180–$300 | $1,000–$1,400 | Calm, safe, rapidly developing, Mindanao's economic hub |

| Bacolod | $175–$310 | $1,000–$1,500 | City of Smiles, strong expat community, low cost |

| Cebu City | $260–$425 | $1,200–$1,800 | Urban hub with beaches, direct international flights |

| Metro Manila | $600–$930 | $1,800–$2,800 | Full world-class amenities, traffic, premium hospitals |

Grocery shopping splits sharply depending on how local you go. Rice is ₱40–60/kilo, chicken is ₱140–180/kilo, and local produce is cheap. A Filipino-style grocery budget in Bacolod runs $80–120/month. Add Western brands, imported wine, and imported cheese and it climbs to $250–400/month. Most expats settle somewhere in between.

Utilities — electricity, water, internet — typically run ₱4,000–8,000/month ($70–140), with fiber internet commonly available in the major cities at speeds of 100–300 Mbps.

Healthcare: The Honest Assessment

The Philippines punches above its weight on private hospital quality in the major cities. Manila has multiple JCI-accredited hospitals — St. Luke's Medical Center, Makati Medical Center, and The Medical City are regularly cited for quality comparable to mid-tier US facilities, but at 60–80% lower cost:

- Private specialist consultation: ₱800–₱2,200 (~$14–$38)

- MRI scan: ₱12,000–₱18,000 (~$210–$310)

- Private hospital room per night: ₱5,000–₱15,000 (~$87–$260), budget to premium

- Cardiac bypass surgery: approximately 20–30% of US prices at top Manila hospitals

Outside major cities, quality drops sharply. If you're in a rural province, expect limited specialist availability. Cebu's Chong Hua Hospital offers tertiary care at 25–40% lower costs than Metro Manila premium facilities — a strong option for expats based in the Visayas.

Health Insurance Options

Philippine local health insurance from providers like Maxicare, Pacific Cross, or Sun Life runs $50–$150/month and covers most major Philippine private hospitals. International plans from Cigna or Allianz run $200–$400/month and offer global coverage including emergency medical evacuation.

For a robust expat setup, many SRRV holders pair a local Philippine plan for day-to-day care with an international plan that includes medevac. Our full expat health insurance guide covers the major providers and what the tiers mean in practice. SafetyWing also offers a Nomad Insurance plan at $45–$80/month depending on age — a reasonable emergency-coverage safety net before setting up a full local policy.

How to Apply: The Step-by-Step

The PRA administers the program directly. A visa agent familiar with the process saves time, but you don't strictly need one. Here's what the process looks like:

- Gather documents in your home country: Passport (6 months validity minimum), police clearance apostilled in your country of origin, medical certificate from a licensed physician dated within 60 days of application, and proof of pension or income if applying as a pension holder.

- Submit to PRA: Either directly at the PRA Manila office or through a PRA-accredited retirement agent. Processing takes 20–30 working days once the full application is accepted.

- Transfer the deposit: Funds go into a PRA-accredited bank or investment vehicle in the Philippines. The bank issues a certificate confirming the deposit, which becomes part of your visa documentation.

- Receive visa endorsement and ACR I-Card: The Alien Certificate of Registration Identity Card is your physical ID. You'll need it for banking, property rental, and government transactions.

The $1,500 application fee and dependent fees are due at submission. They don't come out of the deposit — they're separate, non-refundable costs.

Banking and Moving Money

Opening a Philippine bank account as an SRRV holder is straightforward — your ACR I-Card and passport satisfy most banks' documentation requirements. BDO (Banco de Oro), BPI (Bank of the Philippine Islands), and Metrobank are the most expat-friendly for general banking.

For transferring money from the US to the Philippines, Remitly typically offers competitive USD-to-PHP exchange rates with same-day or next-day delivery. Economy transfers take 3–5 days but minimize fees — the right choice for regular monthly transfers.

For maintaining your US financial infrastructure — keeping a US bank account active, receiving Social Security direct deposits, managing IRS correspondence — you need a valid US mailing address. A Traveling Mailbox virtual mailbox gives you a real US street address in one of 50+ cities with mail scanning and check deposit for $15/month. This matters for keeping US banking relationships intact and satisfying state domicile requirements.

Your US brokerage account is worth protecting. Charles Schwab International is the standard recommendation for expat investors — designed to remain open regardless of your country of residence, with a debit card that reimburses ATM fees globally. Our full breakdown of which US brokerages survive expat moves explains why this matters before you relocate.

What Nobody Tells You

The typhoon question is real. The Philippines sits in one of the most active typhoon corridors on Earth. The central Visayas (Cebu, Bohol) and northern Luzon bear the most hits. Davao, in southern Mindanao, is statistically the least typhoon-exposed major city in the country. If natural disaster risk factors into your decision, it affects your city choice — not the visa itself.

The English advantage is genuine. English is a co-official language of the Philippines and the medium of instruction in schools and business. Most urban Filipinos speak functional to fluent English. This is not the case in Thailand, Vietnam, or most of Latin America. For American retirees, the Philippines stands out on this point.

Power outages still happen. In the provinces and some suburban Manila areas, brownouts of 1–4 hours remain occasional. Newer condo developments typically have generator backup — ask before signing a lease.

The SRRV does not grant work authorization. If you want to work or run a business in the Philippines, you need separate permits. The SRRV is a retirement visa; the PRA is explicit that holders are expected to be living on pension or retirement income.

How the SRRV Compares to Other Asia Retirement Visas

| Program | Country | Min. Deposit/Requirement | Deposit Refundable? | Min. Age |

|---|---|---|---|---|

| SRRV Classic | Philippines | $15,000 | Yes | 40 |

| MM2H (Silver) | Malaysia | ~$65,000 liquid assets | Partial | 35 |

| LTR (Wealthy Pensioner) | Thailand | $80,000 in assets | No | 50 |

| Panama Pensionado | Panama | $1,000/mo pension | N/A | None |

The SRRV wins on deposit size and refundability, and it's the only major Asia retirement visa where English is an official language. Malaysia's MM2H program offers a strong alternative if Southeast Asian infrastructure is the priority. Panama's Pensionado is worth a hard look if you prefer a lower deposit and want Latin America — our geographic arbitrage playbook lays out the full comparison.

Who the SRRV Is Actually For

The profile that makes the most financial sense: a US retiree aged 50+ with Social Security income of $800–$1,500/month, a desire to live comfortably in English on $1,200–$2,000/month in a warm climate, and no interest in paying $4,000–$6,000/month for the same lifestyle in a US city. The all-in cost is $16,500 (deposit + application fee). You get $15,000 back when you leave. The effective cost of the visa is $1,500.

The profile that needs to think harder: someone under 50 without a qualifying pension, facing the $50,000 non-pension deposit tier. At that level, you're tying up meaningful capital at Philippine savings-account rates. The Panama Pensionado or Paraguay's zero-residency-requirement program (see our Paraguay residency guide) may offer better capital efficiency.

If you're planning the full financial mechanics of an overseas move, the complete US expat banking and tax guide covers the pre-departure checklist — which accounts to keep, which to close, and how to handle state tax domicile before you leave.

The Bottom Line

The Philippines SRRV is one of the most pragmatic retirement residency programs in Asia. The deposit structure removes the sunk-cost risk common to other programs. The English advantage is real and underrated. And for retirees willing to live outside Manila, $1,200–$1,500/month delivers warm weather, affordable private healthcare, and a genuinely hospitable culture that is difficult to replicate in the US for under $4,000/month.

The September 2025 age reduction to 40 opened a new chapter. Semi-retirees, freelancers on passive income, and early-retired professionals without a formal pension can now enter at $25,000 (ages 40–49 with qualifying income). The deposit still comes back. The lifestyle math still works.

This article is for informational purposes only and does not constitute legal, tax, or financial advice. Tax rules and visa requirements change — verify current requirements directly with the Philippine Retirement Authority (pra.gov.ph) and consult a qualified tax advisor familiar with US expat tax law before making any residency decisions.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJune 3, 2026

Geographic ArbitrageJune 3, 2026

Retire in the Philippines: SRRV, Costs, and Setup

SRRV deposit from $15K, Cebu life from $1,200 monthly, Philippine law exempts foreign pension remittances from local tax. Full relocation setup guide.

Digital Nomad & Visa GuidesMay 25, 2026

Digital Nomad & Visa GuidesMay 25, 2026

Bali's $130K Visa and the Tax Trap Most Nomads Miss

Indonesia's $130K Second Home Visa sounds ideal — but the 183-day tax rule could expose your worldwide income. Here's what nomads need to know.

Digital Nomad & Visa GuidesMay 15, 2026

Digital Nomad & Visa GuidesMay 15, 2026

Taiwan Gold Card: Asia's Overlooked Expat Tax Break

How Taiwan’s Gold Card gives foreign professionals a 50% income tax cut + tax-free overseas income for 5 years. Step-by-step application guide.