Japan for US Expats: Taxes, Visas & the $2,000/Month Life

Japan's cost of living was supposed to be the deal-breaker. It wasn't. Fukuoka drops that number closer to $1,055. Excludes health insurance and travel.

Japan's cost of living was supposed to be the deal-breaker. It wasn't. Fukuoka drops that number closer to $1,055. Excludes health insurance and travel.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Japan's cost of living was supposed to be the deal-breaker. It wasn't. At JPY159 to the dollar (April 2026), a single American can live comfortably in Osaka for $1,315 per month — less than rent alone in most US cities. Fukuoka drops that number closer to $1,055. Even Tokyo, the city everyone warns you about, clears $1,690 monthly for a decent one-bedroom and a social life. The bigger shock isn't the price — it's how few US expats actually know how the tax system works here, and how dramatically that changes depending on how long you stay.

Japan has quietly become one of the most compelling expat destinations in Asia for Americans who do their homework. It's safe, clean, food-obsessed in the best way, has world-class infrastructure, and offers a digital nomad visa that lets you test the waters without uprooting your life. But stay past the five-year mark and the rules change fast — in ways that can cost you serious money if you're not prepared.

What It Actually Costs to Live in Japan

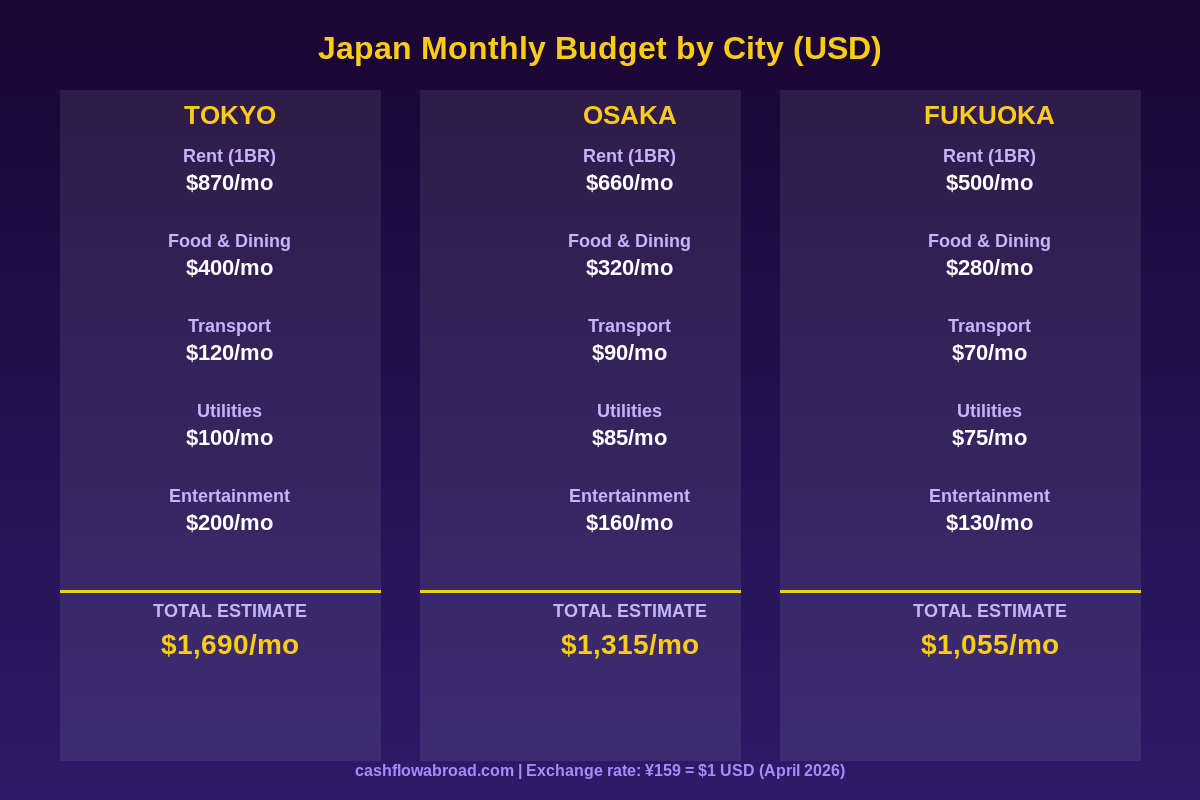

Japan's reputation for being expensive is a Tokyo 2008 problem. Currency depreciation and regional price variation have completely changed the calculus. Here's what real monthly budgets look like in Japan's three main expat hubs at today's exchange rate:

| Expense | Tokyo | Osaka | Fukuoka |

|---|---|---|---|

| 1BR apartment (central) | $870 | $660 | $500 |

| Food & dining | $400 | $320 | $280 |

| Transport (rail pass) | $120 | $90 | $70 |

| Utilities | $100 | $85 | $75 |

| Entertainment | $200 | $160 | $130 |

| Total estimate | $1,690 | $1,315 | $1,055 |

Based on JPY159 = $1 USD, April 2026. Excludes health insurance and travel.

A few things worth knowing: Japan's grocery bills are genuinely low once you eat like a local. A bowl of ramen at a counter shop runs $7–9. Convenience store meals — and they're legitimately good — cost $4–6. International ingredients and imported goods spike your food bill fast. Utilities run high in winter (electric heating) and summer (air conditioning is non-negotiable in July and August). Tokyo's rail system costs money but eliminates the need for a car entirely — that's $400–700/month back in your pocket versus most US cities.

Outside the three main cities, Japan gets dramatically cheaper. Hiroshima, Kanazawa, and secondary Kyoto neighborhoods offer a mix of culture and lower costs, though Kyoto's short-term rental market has tightened due to Airbnb restrictions. The government now actively promotes regional relocation and in some rural areas offers cash grants of up to JPY 1,000,000 (around $6,300) to relocate — it's a real program called the local government settlement grant, though it comes with residency commitments.

Visa Options for Americans

Japan launched its Digital Nomad Visa in 2024, and it's one of the more straightforward options if you already earn well. Here's the full landscape:

| Visa Type | Duration | Income Requirement | Key Restriction |

|---|---|---|---|

| Digital Nomad Visa | 6 months (non-renewable) | ~$67,328/year (¥10M) | Must earn income outside Japan; no Japanese employer |

| Engineer/Humanities/Intl Services | 1–5 years (renewable) | Job offer required | Must be employed by a Japanese company |

| Highly Skilled Professional (HSP) | 5 years | Points-based system | Fast-tracks permanent residency (1–3 years) |

| Business Manager | 1–3 years (renewable) | ¥5M+ investment | Must operate a real business in Japan |

| Spouse Visa | 1–3 years (renewable) | None | Married to Japanese national or permanent resident |

| Permanent Residency | Indefinite | Stable income required | Generally 10 years; HSP holders qualify in 1–3 years |

The Digital Nomad Visa is clean but comes with a hard wall: it's not renewable. Once your 6 months is up, you need to spend at least 6 consecutive months outside Japan before reapplying. No Residence Card is issued, which means no Japanese bank account, no standard mobile contract, and no access to the National Health Insurance system. You'll need private coverage — more on that below.

The HSP visa is the sleeper pick. Japan awards points for salary, academic background, age, and Japanese language ability. Hit 70 points and you qualify for 5-year status; hit 80 points and permanent residency eligibility drops to just 1 year instead of 10. If you're a tech or finance professional in your 30s with a Japanese employer, the HSP track can get you permanent residency faster than almost any other country in Asia.

One 2026 update: Japan raised its departure tax to JPY 2,000 ($12.60) and increased visa processing fees across the board. Modest costs, but worth knowing before you budget your first trip to scope things out.

The Tax Situation: What US Expats Actually Owe

Japan's tax system has a built-in five-year grace period for foreigners that most Americans don't realize exists — and it's the most important number in this whole guide.

Non-Permanent Resident Status (Years 1–5)

If you've spent five years or fewer as a Japanese resident within the past 10 years, you're classified as a non-permanent resident. In that status, Japan only taxes your Japan-source income plus any foreign-source income you remit to Japan. Your US brokerage dividends, your online income deposited into a US account, your rental income from a US property — none of that is taxed in Japan as long as you don't transfer it into a Japanese bank account.

Combined with the Foreign Earned Income Exclusion ($130,000 for the 2025 tax year, filed in 2026), many US remote workers in Japan for under five years can effectively eliminate double taxation. You exclude your foreign earned income on the US side via Form 2555; Japan doesn't tax it because you're not remitting it. This is a genuinely favorable setup that almost no mainstream expat content accurately explains. See the FEIE guide for the mechanics.

What Happens After 5 Years

Once you cross the five-year threshold, Japan treats you as a permanent tax resident — distinct from immigration permanent residency — and taxes your worldwide income. Japanese income tax is progressive: 5% on the first ¥1.95M, scaling to 45% on income above ¥40M. Add the 10% resident tax (prefectural plus municipal) and the effective top rate hits 55% — one of the highest in the developed world.

The US-Japan Tax Treaty provides a dollar-for-dollar credit mechanism to avoid double taxation, but high earners will still face meaningful Japan-side tax bills on investment income and business profits. Plan your residency duration the same way you'd plan a financial position: with a clear time horizon and an exit plan.

The Inheritance Tax Trap

Japan's inheritance tax runs 10–55% on a progressive scale, and it can reach foreign assets in ways expats don't expect. The key threshold is 10 years of Japanese residency. Short-term residents (under 10 years) are taxed only on Japanese-sited assets — your US brokerage and US real estate stays entirely outside Japan's reach. Long-term residents (10+ years) face inheritance tax on worldwide assets.

The US-Japan Estate Tax Treaty provides protection via tax credits and clear residency-based allocation rules, but if you're planning a long-term move with substantial assets, get estate planning advice from a treaty-aware attorney before you hit that 10-year mark. This is not a hypothetical risk — it's caught multiple long-term Japan expats with US-held portfolios completely off guard. The expat estate planning guide covers the cross-border asset protection side in detail.

Banking and Moving Money

Japan remains more cash-dependent than its tech reputation suggests, but Seven Bank ATMs (inside every 7-Eleven) accept international cards around the clock with no 7-Eleven-side fee. Your US bank's foreign transaction fees are the variable. The cleanest setup: a Charles Schwab International checking account — zero foreign transaction fees and full ATM fee reimbursement worldwide — plus a local Japan Post Bank account once you have your Residence Card.

Without a Residence Card, local banking is limited. Most nomads on the Digital Nomad Visa use PayPay for mobile payments and lean on their home bank cards for cash. Once you're on a long-term visa, Shinsei Bank and SMBC have English-language interfaces and are more foreigner-friendly than the major megabanks (Mizuho, MUFG), which still require Japanese for most in-branch processes.

For sending money between Japan and the US, Remitly handles JPY/USD transfers with transparent exchange rates and same-day delivery. Given the yen's current weakness, timing larger transfers matters — a 5-yen swing on a $10,000 transfer is a $300+ difference.

Maintain a real US mailing address for your brokerage, IRS filings, and bank accounts. A Traveling Mailbox virtual mailbox ($15/month) gives you a real US street address with mail scanning — essential for keeping Schwab, your brokerage, and the IRS satisfied while you're living abroad.

Healthcare for US Expats

Japan's healthcare system consistently ranks in the top 10 globally. Once enrolled in National Health Insurance (NHI) — mandatory when you have a Residence Card — you pay 30% of medical costs out-of-pocket with generous annual caps. Premiums are income-based, so your first year in Japan, when your declared Japan income is zero, NHI runs as low as ¥2,000–5,000/month ($12–31). That changes as your declared income rises.

On the Digital Nomad Visa, you're excluded from NHI. The visa requires private health insurance covering at least ¥10 million ($62,893) for injury, illness, and death. SafetyWing Nomad Insurance satisfies this requirement at $60–100/month for most Americans — a fraction of maintaining US coverage from abroad. For a full comparison of expat insurance options, see the expat health insurance guide.

English-speaking doctors are more available in Tokyo and Osaka than most people expect. International clinics in both cities handle English-language appointments without issue. Dental work is notably affordable — a filling runs $30–60 under NHI, compared to $200–400 in the US out-of-pocket.

Practical Details Nobody Puts in One Place

Internet: Japan's fiber infrastructure is world-class. Home internet runs $40–60/month with speeds that embarrass most US ISPs. Rakuten Mobile's unlimited plan works well in major cities. For arrival connectivity, a Saily eSIM activates instantly at the airport — no SIM swap needed.

Apartments: This is the hardest part of Japan for foreigners. Traditional leases require a Japanese guarantor, key money (non-refundable gift to the landlord, often 1–2 months rent), and a formal agency relationship. Key money is fading in younger markets, but you'll still face 2–3 months upfront regardless. Gaijin Pot Housing and Sakura House specifically serve foreign renters without guarantor requirements — useful for your first 6–12 months while you build local credit history.

Crypto taxation: Japan classifies crypto gains as miscellaneous income, taxed at the full progressive rate up to 55%. This is among the harshest crypto tax regimes globally. Your non-permanent resident window may offer some shelter on offshore holdings not remitted to Japan, but this needs specific advice. US obligations stack on top — the crypto taxes US expat guide covers what the IRS expects regardless of where you live.

Language: Japanese bureaucracy — visa renewals, tax filings, apartment contracts — runs in Japanese. Translation apps handle most daily situations, but having a bilingual helper (or hiring a regional immigration lawyer for $200–400 a year) prevents expensive mistakes in official settings.

Who Japan Actually Works For

Japan is a strong fit for: remote workers earning $70,000+ in offshore income who want to exploit the non-permanent resident window; tech and engineering professionals who can get employer sponsorship and ride the HSP track to permanent residency; couples and families who prioritize safety, education quality, and livability over low sticker price; and anyone currently earning in dollars who wants to benefit from the yen's historic weakness.

It's a harder fit for: crypto-heavy portfolios (the tax treatment is punishing), anyone planning an indefinite stay without proactive tax planning (the five-year cliff is real), and people who need immediate banking access — the Digital Nomad Visa's no-Residence-Card limitation creates real friction in month one.

For the broader geographic arbitrage context — comparing Japan to Southeast Asia, Latin America, and Europe — the geographic arbitrage playbook runs the numbers across 10 countries side by side.

Bottom Line

Japan makes far more financial sense for US expats than its outdated reputation suggests — especially right now, with the yen at multi-decade lows and a digital nomad visa that removes the old employer-sponsor barrier. A remote worker earning $80,000/year can live exceptionally well in Osaka for under $1,400/month during their first five years, while Japan's tax system largely stays out of the way. The trade-offs are real: challenging apartment markets for foreigners, a brutal crypto tax regime, and a residency clock that triggers serious tax consequences after year five. But for the right profile — intentional about residency duration, earning in dollars, willing to do the upfront logistics work — Japan is one of the most underrated expat setups in the world.

Plan your residency like a trade: know your entry, know your exit, and let the non-permanent resident window work for you instead of against you.

Financial Disclaimer: This post is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and vary by individual circumstance. Consult a qualified US expat tax attorney and a licensed Japanese tax advisor before making any residency or financial decisions. Exchange rates referenced reflect April 2026 figures and will fluctuate.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJuly 19, 2026

Geographic ArbitrageJuly 19, 2026

Sofia Remote Work Budget Under $2,000

Price rent, transit, utilities, insurance, and visa caveats before using Sofia, Bulgaria as a lower-cost EU base for remote work.

Geographic ArbitrageJune 30, 2026

Geographic ArbitrageJune 30, 2026

Moving Abroad with Kids: School Costs and Family Budget

International school fees change the whole geographic arbitrage math for families. Compare real costs in Medellín, Chiang Mai, Mexico, and Lisbon for

Geographic ArbitrageJune 29, 2026

Geographic ArbitrageJune 29, 2026

Bali for US Expats: Monthly Costs and Permit Guide

How much Bali costs, which Indonesian stay permit suits long-term stays, and what US citizens owe the IRS while living there in 2025.