How the IRS Can Cancel Your Passport Abroad

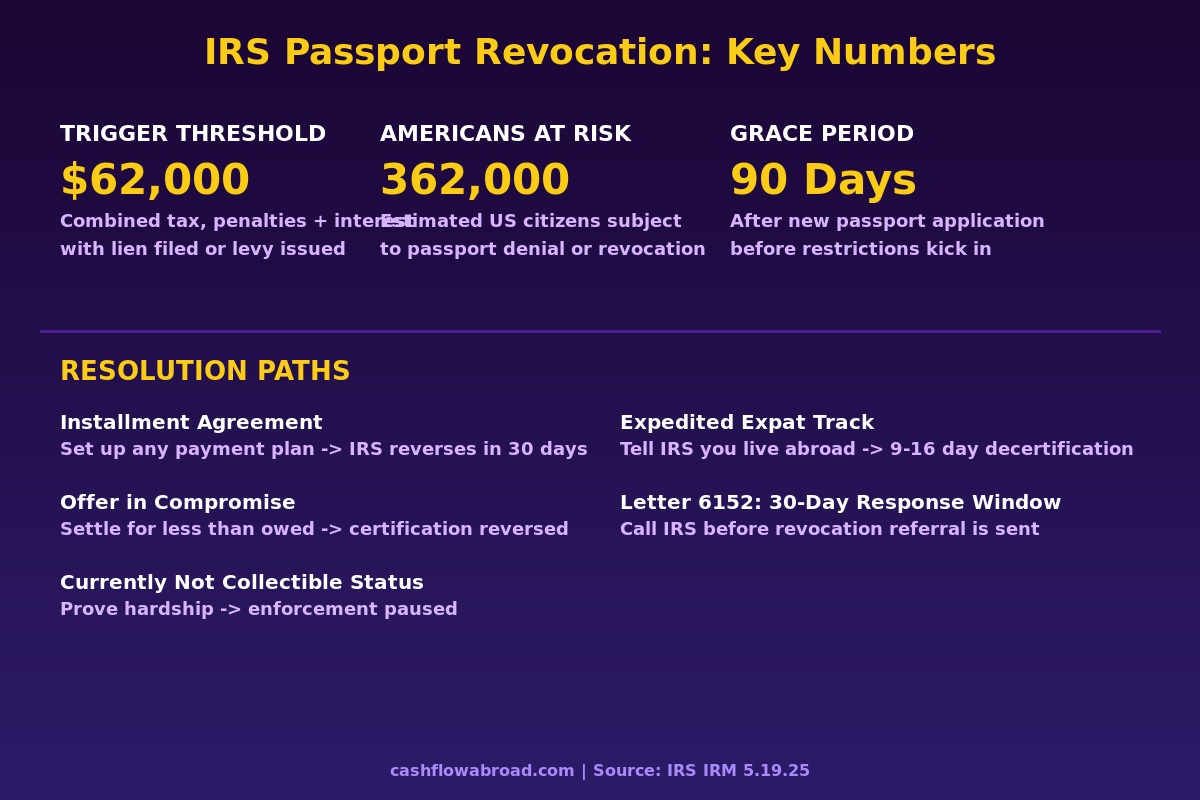

The IRS can revoke your US passport for owing $62,000+ in tax debt — and 362,000 Americans are in scope. Here's how it works and how to stop it.

The IRS can revoke your passport for $62,000+ in unpaid taxes. 362,000 Americans at risk. Learn thresholds, process, and resolution options.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

The IRS doesn't need to arrest you. It doesn't need a court order. Under a law most Americans have never heard of, the agency can quietly notify the State Department that you owe taxes — and within weeks, the document you depend on to live, work, and move freely abroad stops working. Approximately 362,000 US citizens are currently estimated to be in scope for passport revocation or denial under IRC Section 7345. Most of them don't know it.

If you're an expat, this isn't just a financial inconvenience. Your passport is your ID at foreign banks, your credential at border crossings, the anchor for your residency visa. Getting it revoked while you're living in Medellín or Chiang Mai or Tbilisi is a different category of problem than getting it revoked in Kansas City.

What Actually Triggers Revocation

Congress authorized this mechanism through the FAST Act in December 2015. The IRS started enforcing it in January 2018. The program targets what the law calls "seriously delinquent tax debt" — a specific legal status, not just owing money.

To reach seriously delinquent status, you need all three conditions:

- You owe more than the threshold amount in combined federal tax debt, penalties, and interest

- The debt has been assessed (not just proposed)

- Either a Notice of Federal Tax Lien has been filed and all administrative remedies have lapsed, or a levy has been issued

The threshold is adjusted annually for inflation: $62,000 in 2024 and 2025, with a projected increase to approximately $66,000 for 2026. That number sounds high until you remember that IRS penalties and interest compound. A $35,000 tax bill from three years ago can cross the threshold before you've opened the certified mail.

| Year | Threshold | Notes |

|---|---|---|

| 2018 (program launch) | $51,000 | Original threshold at implementation |

| 2020 | $54,000 | First inflation adjustment |

| 2022 | $55,000 | — |

| 2024 | $62,000 | Significant jump due to cumulative inflation |

| 2025 | $62,000 | Held steady |

| 2026 (projected) | ~$66,000 | Expected inflation adjustment |

Some debts are explicitly excluded from certification: debts under an active installment agreement or pending Offer in Compromise, debt in currently-not-collectible status, debt being disputed in Collection Due Process proceedings, and debt discharged in bankruptcy. These exclusions are the off-ramps — and every single one of them can be invoked proactively.

How the Process Actually Works

The sequence is more deliberate than most people expect. The IRS isn't allowed to just notify State and walk away — there are procedural steps, including a formal warning before revocation.

Step 1 — Certification. Once your debt meets the threshold and lien/levy condition, the IRS certifies your name to the US Department of State. Simultaneously, it mails you a CP508C notice to your last known address. This is the first formal notification that certification has happened.

If you're living abroad and haven't updated your IRS address, CP508C may go to a US address you left years ago. This is why maintaining a real US street address is infrastructure, not optional. A virtual mailbox like Traveling Mailbox — which scans and forwards your mail digitally — means you actually see certified IRS notices instead of discovering them when you try to board a flight. File Form 8822 every time you move to keep the IRS address current. See our full guide on virtual mailboxes for expats.

Step 2 — Letter 6152. Before the IRS formally refers your case to State for revocation, it sends Letter 6152. This asks you to call within 30 days to resolve your account. It's the last clear warning before the revocation referral goes out.

Step 3 — State Department action. Once State receives a certified name, it has three options: deny a new passport application, revoke an existing passport, or issue a limited-validity passport allowing return to the United States only. The limited passport means you're not permanently stranded — but you're functionally grounded. No visa renewals, no international banking appointments, no business travel.

Step 4 — 90-day grace on new applications. If you apply for a passport while certified, the State Department grants a 90-day window before enforcing restrictions. This is designed to give you time to contact the IRS and resolve the certification. Use it — it's real runway.

Why the Stakes Are Different If You Live Abroad

For a US-based person, a revoked passport disrupts vacations and international business trips. For an expat, it can unravel the entire structure of your life abroad.

Foreign banks require a valid passport for account maintenance and KYC renewals. Many residency programs require periodic passport-verified check-ins. Your passport may be your primary government ID for landlords, employers, healthcare providers, and local agencies. A limited-validity US-only passport ends your ability to renew a Schengen visa, extend a Southeast Asian residency permit, or apply for any new document in your host country.

Expats are also disproportionately likely to end up among the 362,000. Complex tax situations — the Foreign Earned Income Exclusion, foreign tax credits, FBAR reporting, PFIC investments — create more surface area for IRS disagreements. Many expats underestimate what they owe on US taxes from abroad. Others fall behind during the chaos of relocation with no local CPA and no working mail address.

The IRS built in one accommodation for expats: if you notify the IRS that you reside abroad, the standard 30-day processing window for decertification compresses to 9–16 days. That's meaningful if your visa expires in three weeks. But you have to know to ask for it explicitly when you call.

Resolution Options: You Don't Have to Pay It All

This is the fact most coverage of this topic buries: you do not need to pay the full balance to stop passport revocation. The IRS reverses certification under several conditions, and a modest monthly installment agreement qualifies.

| Resolution Method | Upfront Cost | IRS Reversal Timeline | Best For |

|---|---|---|---|

| Full payment | 100% of balance | Within 30 days of processing | Those who can pay in full |

| Installment Agreement | First payment only | Within 30 days of activation | Most practical for most taxpayers |

| Offer in Compromise | 20% of offer (lump sum OIC) | Once OIC accepted or pending | Those who qualify for reduced settlement |

| Currently Not Collectible | Nothing | Once CNC status granted | Demonstrated financial hardship |

| Collection Due Process hearing | Filing fee ($0–$330) | Enforcement suspended during appeal | Disputing the underlying debt |

| Erroneous certification lawsuit | Legal fees | Court order required | IRS certified in error |

The Installment Agreement is the most important option to understand. You call the IRS, set up a payment plan for whatever amount you can manage monthly, make the first payment, and the IRS is required to notify the State Department within 30 days that you've been decertified. Passport status restored — without paying off years of accumulated debt.

An Offer in Compromise that is merely pending (submitted but not yet decided) also suspends certification, buying significant time. The IRS accepts OICs when there's genuine doubt about collectibility — meaning the agency doesn't realistically expect to recover the full amount given your assets and income. This is a separate track from the emerging CARF global data-sharing regime, but that program makes hiding foreign assets harder — which makes a legitimate, documented OIC more important than trying to wait things out.

The Currently Not Collectible designation pauses all IRS collection activity if you can demonstrate financial hardship. Interest continues accruing during CNC status, but enforcement (including passport referrals) stops. CNC status is reviewed periodically and requires updated financial documentation, but it buys breathing room while you stabilize.

Prevention: The Real Play

The cleanest outcome is never reaching certification. That requires a few habits that most expats don't think about until something goes wrong.

Keep your IRS address current. File Form 8822 whenever you move. Maintain a stable US mailing address — not your parents' house where mail sits unread for months, but a virtual mailbox service that scans and sends you a notification when IRS mail arrives. The $15–$25/month cost of services like Traveling Mailbox is insignificant compared to the cost of missing a CP508C.

Respond to every IRS notice before it escalates. A CP14 (balance due) is not a lien. A CP504 (intent to levy) is not a levy. Calling the IRS in response to either one — even to dispute, request more time, or set up a payment plan — resets the clock and prevents the enforcement action that triggers passport certification eligibility. The IRS actually prefers contact to silence.

Keep a functional US bank account. Paying the IRS from abroad requires ACH capability on a US account. Charles Schwab's international checking account works from anywhere with no foreign transaction fees and worldwide ATM reimbursement. Mercury works well for business accounts. Direct Pay at IRS.gov accepts ACH from US accounts — you can schedule a payment from Bangkok in under five minutes.

File every year, even if you owe zero. Most expats with total income below the Foreign Earned Income Exclusion ($126,500 for tax year 2024) owe nothing federally. But you still need to file Form 1040 and any required information returns — FBAR if your foreign accounts exceeded $10,000 at any point, Form 8938 for FATCA reporting, Form 5471 if you own a foreign corporation. Crypto reporting requirements add another layer. Unfiled information returns generate penalties that can compound toward the certification threshold independent of any underlying tax liability.

Use the IRS Streamlined Compliance Procedures if you're behind. The Streamlined Foreign Offshore Procedures allow expats who fell behind without willful intent to catch up on up to three years of returns and six years of FBARs, with dramatically reduced penalties. Critical rule: you must apply before the IRS contacts you first. Once the agency initiates contact, the window closes.

The Bottom Line

Section 7345 is real, actively enforced, and designed to be hard to ignore — because for most Americans, their passport is their most emotionally and practically irreplaceable document. For expats, that's doubly true. With 362,000 people estimated to be in scope and the program running since 2018, this isn't an edge case risk.

The mechanics are more forgiving than the headline suggests. A modest installment agreement reverses certification without paying off the full debt. The 90-day grace window on new applications gives real runway. The expedited 9–16 day decertification track for overseas residents exists specifically for people in your situation. But you need to know these levers exist — and you need to know about them before the CP508C arrives, not after.

Keep your address current, keep a US bank account, file every year, and treat IRS correspondence as urgent. Your wealth structure abroad is only as stable as your ability to move freely and access your documents.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute legal, tax, or financial advice. IRS thresholds, rules, and procedures change; verify current information at IRS.gov. If you believe you may be affected by IRC Section 7345 or have unfiled US tax returns, consult a qualified tax professional, enrolled agent, or tax attorney before taking action. The author is not a licensed tax advisor.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

FBAR vs FATCA: What Every Expat Must Know

FBAR and FATCA are two separate foreign account reporting requirements with different penalties and thresholds. Learn what every US expat must file.

Expat Tax & FinanceMay 25, 2026

Expat Tax & FinanceMay 25, 2026

State Domicile for Expats: Avoid the States That Chase You Abroad

California can tax your foreign income at 13.3% even after you leave. Learn how to change state domicile and save 5,000+ per year as a US expat.

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.