High-Yield Foreign Savings: Earn 12% While US Banks Pay 4%

US savings pays 4%. Colombian CDTs pay 12.9%. Which foreign savings accounts beat US rates — and the currency risk nobody mentions.

US savings pays 4%. Colombian CDTs pay 12.9%. Learn which foreign savings accounts beat US rates and the currency risk nobody mentions.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

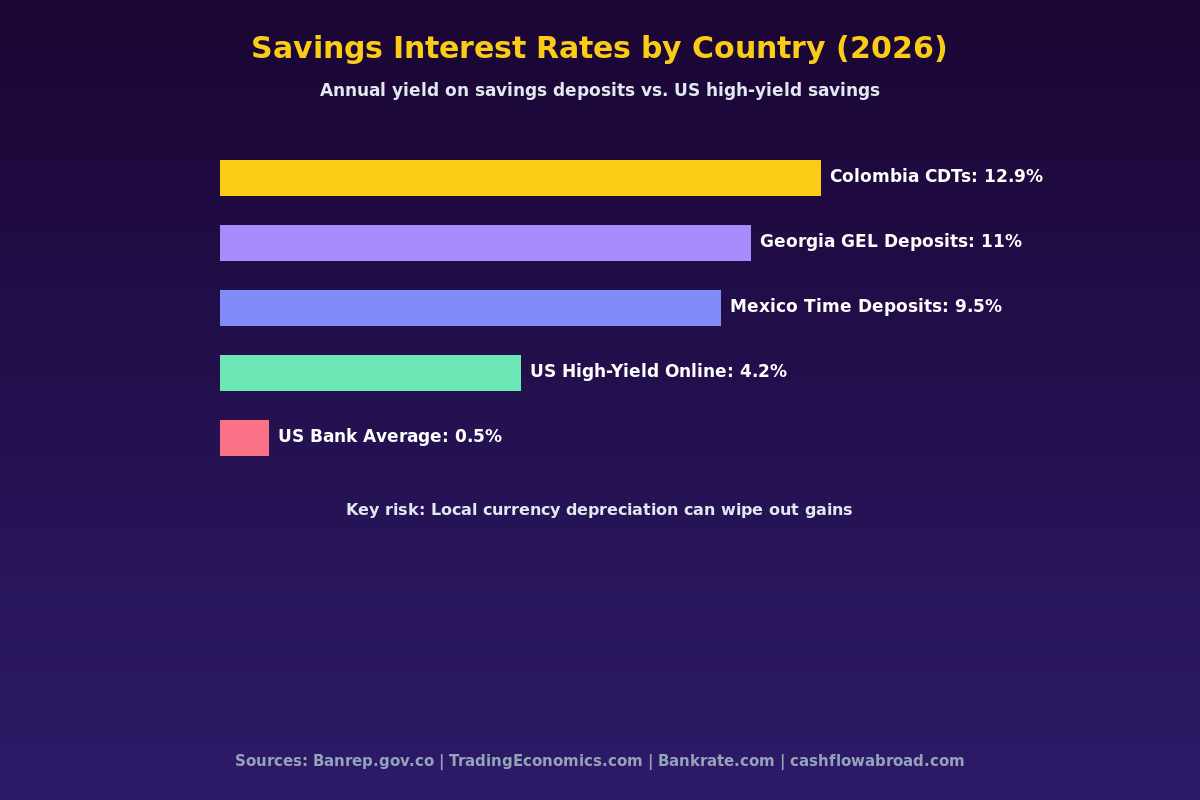

Your US savings account is paying 4.2%. A fixed-term deposit at a Colombian bank is paying 12.9%. That's a 3x difference on money that's just sitting there — and it's completely legal, widely used by expats, and backed by government deposit insurance.

But here's what most guides don't tell you: earning 12% in Colombian pesos while thinking in US dollars is not the same as earning 12% in real terms. The currency risk can erase everything — and then some. This guide gives you the full picture: which countries, which banks, real rates, real risks, and the FBAR obligations the IRS expects you to understand.

Why Foreign Banks Pay More

High interest rates in emerging markets aren't a gift — they're compensation for risk. When Colombia's central bank (Banrep) sets its benchmark rate at 9.25%, commercial banks price savings products above that to attract deposits. When the US Federal Reserve sets rates near 4.25-4.5%, US savings accounts trail that benchmark, typically paying 0.5% at national banks and 4-4.5% at online-only institutions.

Three factors drive the gap:

- Higher inflation targets: Countries like Colombia and Mexico historically run 3-8% inflation, so nominal rates must stay elevated to offer a real (inflation-adjusted) return

- Currency premium: Investors demand extra yield to hold assets in a currency they perceive as riskier than the US dollar

- Competition for deposits: In markets with lower financial inclusion, banks and fintech apps aggressively compete for retail savers with above-benchmark rates

None of this means foreign savings accounts are a scam. It means you're being paid to take on currency risk — and you need to decide whether that's a trade you actually want to make.

Where the Best Rates Actually Are

Colombia: CDTs Paying Up to 12.9%

Colombia's Certificados de Depósito a Término (CDTs) are fixed-term deposits that work like US CDs. In March 2026, rates reach up to 12.9% annual effective rate (E.A.) at regulated financial institutions supervised by the Superintendencia Financiera. Major banks like Bancolombia and Davivienda offer 9-10% E.A. on 180-day terms. Digital platforms push higher: Nu Colombia at 9.7% (180 days), Ualá at 13%, and Rappi Pay at up to 14%.

Deposit insurance (Fogafín) covers up to 50 million Colombian pesos per depositor per institution — roughly $12,000 USD at current exchange rates. That's thin coverage compared to FDIC's $250,000 in the US, which matters if you're moving significant sums.

Opening a CDT as a foreigner requires a Colombian bank account, which in turn requires a cédula de extranjería (foreign ID card), typically available once you have a visa or residency status. If you're just passing through, digital banks like Nu and Ualá have simpler onboarding with a passport — but account opening rules vary and change frequently.

Georgia: 10-11% on GEL, Tax-Free

The country of Georgia has become a legitimate expat banking hub — and for good reason. TBC Bank and Bank of Georgia (together controlling 80% of the Georgian banking market) currently offer 10-11% annual interest on Georgian Lari (GEL) term deposits, with Western institutional investors including JPMorgan Asset Management, Vanguard, and BlackRock as significant shareholders in Bank of Georgia.

The standout advantage: Georgia levies 0% personal income tax on bank deposit income. For Georgian residents, interest compounds tax-free. For US citizens (taxed on worldwide income regardless of where they live), you'll still owe the IRS, but the hosting country won't take a cut.

USD deposits at Georgian banks pay 4-5% — competitive with US online banks but with the added complexity of opening an account abroad. GEL deposits at 10-11% are the headline number, but that's in lari. See the currency risk section below before getting excited.

Account opening for non-residents is generally straightforward at TBC Bank and Bank of Georgia — walk into a branch in Tbilisi with your passport and they'll set you up. The Georgia 1% flat tax program has attracted thousands of expats; read the full Georgia expat tax guide here if you're considering making it a base.

Mexico: CETES and Nu Mexico

Mexico's central bank (Banxico) cut its benchmark rate to 6.5% at its May 2026 meeting, down from a peak of 11.25% in 2023. Time deposits (plazo fijo) at established banks pay around 9.5% on average. Inbursa's InbursaCT product ties its rate directly to CETES and pays the full government rate on balances above 100,000 pesos — accessible via app with instant liquidity.

Nu Mexico offers a savings product that has paid up to 10% annualized on demand deposits with no lock-up period — a remarkable combination of liquidity and yield. The caveat: these rates float with the CETES benchmark, so as Banxico cuts, the yield follows.

Opening a Mexican bank account as a foreigner requires an RFC (Mexican tax ID), which takes time and paperwork. BBVA Mexico has been documented pressuring foreign account holders into unwanted insurance products; Banorte is a cleaner option but stricter on documentation. For expats already living in Mexico with temporary or permanent residency, the banking setup is straightforward.

The Math Nobody Shows You

Here's the calculation that most "12% returns abroad!" articles skip entirely.

Say you move $10,000 USD to Colombia, convert to pesos (roughly 41.5 million COP at current rates), and lock it in a 12-month CDT at 12.9%. At maturity, you have about 46.8 million COP — a clean 12.9% gain in pesos.

Now you convert back to USD. If the exchange rate stayed flat, you'd have $11,272. Profit: $1,272 or 12.7%. But the Colombian peso has historically depreciated against the dollar. In 2023, the peso lost roughly 15% of its value against USD over the year. If that happened to your CDT: your 46.8 million COP converts back at the weaker rate, and you might walk away with $9,600 — a net loss of $400 despite earning 12.9% in local currency.

| Scenario | COP Rate Earned | USD Depreciation | Net USD Return |

|---|---|---|---|

| Best case (peso flat) | 12.9% | 0% | +12.7% |

| Moderate (5% depreciation) | 12.9% | -5% | +7.2% |

| Historical avg (peso -8%/yr) | 12.9% | -8% | +3.9% |

| Bad year (peso -15%) | 12.9% | -15% | -4.0% |

| Worst case (currency crash -40%) | 20%+ | -40% | -28% |

This table doesn't make foreign savings accounts look bad — it makes them look accurate. If you're spending in pesos anyway (because you live in Medellín), the 12.9% is real and the "currency risk" is reversed: you'd actually be hurt if the peso strengthened. But if you're earning in dollars and parking money temporarily, you're genuinely exposed.

Dollar Accounts: The Middle Path

If currency risk is a dealbreaker, there are dollar-denominated foreign savings options worth knowing:

- Georgian banks in USD: TBC Bank and Bank of Georgia both offer USD-denominated term deposits at 4-5% annually — same or slightly better than US online banks, with 0% Georgian income tax on interest and the added benefit of a non-US banking relationship

- HSBC Expat: Offers USD accounts with modest yields and global banking infrastructure — useful if you need cross-border banking more than yield optimization

- Stablecoin savings via ARQ Finance: The most underrated option for dollar savings in Latin America — earn up to 4% on USDc/EURc balances, swap to MXN/COP/ARS/BRL on demand, and use the Mastercard with cashback. No currency conversion required. Available in Mexico, Colombia, Argentina, and Brazil. See ARQ Finance here.

The stablecoin savings angle deserves a pause. A 4% yield on dollar-pegged stablecoins isn't as flashy as 12.9% in Colombian pesos, but it's real dollar yield with no conversion risk — accessible from a smartphone without the bureaucratic friction of opening a physical foreign bank account.

FBAR, FATCA, and What the IRS Wants

This section isn't optional reading. If you open a foreign savings account, the IRS has reporting requirements that carry severe penalties for non-compliance.

FBAR (FinCEN Form 114)

You must file an FBAR if the combined maximum value of all your foreign financial accounts exceeded $10,000 at any point during the calendar year — even for a single day. The 2026 deadline is April 15 with an automatic extension to October 15. File electronically at FinCEN.gov; this form goes to FinCEN, not the IRS.

Non-willful FBAR violations: fines up to $10,000 per violation. Willful violations: up to $100,000 or 50% of the account balance, whichever is greater. A January 2026 Court of Appeals ruling established that "reckless disregard" of the FBAR requirement triggers willful penalties — meaning intentional ignorance is no longer a viable defense.

FATCA (Form 8938)

If your total foreign financial assets exceed $50,000 at year-end (or $75,000 at any point during the year) as a single filer living stateside — thresholds are higher for married couples and for expats living abroad — you must file Form 8938 with your tax return. FBAR and FATCA overlap but are separate obligations filed with different agencies.

Interest Is Taxable Regardless

Interest earned in a foreign savings account is ordinary income taxable by the US, regardless of where it's earned or whether you bring the money home. Convert the interest to USD at the applicable Treasury exchange rate and report it on Schedule B. The Foreign Earned Income Exclusion (FEIE) does NOT cover passive interest income — it only applies to active earned income.

The cost of wiring money abroad to fund these accounts eats into returns. Use Remitly for international transfers — transparent pricing and no hidden $25-$45 bank wire fees. The full breakdown of transfer costs is in the expat money transfer guide.

Who Foreign High-Yield Accounts Actually Work For

Three profiles where this makes clear sense:

- Expats spending locally. If you live in Medellín and your expenses are in pesos, a 12.9% CDT has zero currency risk relative to your cost of living. The peso-dollar exchange rate is irrelevant to your actual purchasing power.

- Geographic arbitrageurs diversifying USD holdings. Georgian USD deposits at 4-5% offer a non-US banking relationship, potential asset protection, and competitive yield without FX exposure. A useful addition to the banking stack covered in the zero-fee expat banking guide.

- Experienced investors sizing currency bets deliberately. If you believe the Mexican peso will hold or appreciate over 12 months (plausible given nearshoring trends and remittance flows), a CETES-linked account at 9.5% is a structured trade — not a savings account mistake.

What it's not suited for: US dollar emergency fund, money needed back in dollars within 12 months, or anyone who hasn't already built a solid US banking base. The US expat banking guide covers the foundation before you go exploring abroad.

Opening a Foreign Savings Account: Practical Guide

| Country | Best Options | Requirements | Time to Open |

|---|---|---|---|

| Colombia | Nu Colombia, Ualá, Bancolombia | Passport + cédula de extranjería (or NIT) | 1-3 days (digital banks faster) |

| Georgia | TBC Bank, Bank of Georgia | Passport only; in-person branch visit in Tbilisi | Same day |

| Mexico | Nu Mexico, InbursaCT | Passport + RFC tax ID + CURP | 1-4 weeks (RFC registration takes time) |

Maintain a US banking anchor in parallel. Charles Schwab International remains the go-to for US expats: no foreign ATM fees worldwide, a brokerage that doesn't close when you move abroad, and a debit card that works everywhere. If you need a US mailing address for banking correspondence and IRS notices while living abroad, Traveling Mailbox provides a real US street address in 50+ cities with mail scanning and check deposit for $15/month — the site owner uses this personally.

For the full geographic arbitrage framework — building income and assets across multiple jurisdictions — the Geographic Arbitrage Playbook lays out the complete strategy.

The Bottom Line

Foreign high-yield savings accounts are real, legal, and genuinely lucrative under the right circumstances. Colombia's CDTs at 12.9%, Georgia's GEL deposits at 10-11%, and Mexico's CETES-linked accounts at 9.5% all beat US rates by a significant margin. But the yield is compensation for currency risk — not free money. An expat spending in Colombian pesos has zero currency risk on a peso CDT. A dollar-denominated American wiring funds for a 12-month lock-up is taking on real FX exposure.

The practical path: use foreign-currency accounts for money you'll spend locally, consider USD-denominated deposits in Georgia for diversification without conversion risk, and explore stablecoin savings platforms like ARQ Finance for 4% dollar yield without the paperwork. Whatever you do, file your FBAR if the balance crosses $10,000 at any point during the year.

Disclaimer: This post is for educational purposes only and does not constitute financial, tax, or legal advice. Interest rates, exchange rates, and banking regulations change frequently. Consult a qualified CPA familiar with expat compliance before moving funds into foreign accounts. All FBAR and FATCA obligations described reflect US law as of May 2026.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

FBAR vs FATCA: What Every Expat Must Know

FBAR and FATCA are two separate foreign account reporting requirements with different penalties and thresholds. Learn what every US expat must file.

Expat Tax & FinanceJune 23, 2026

Expat Tax & FinanceJune 23, 2026

FBAR vs Form 8938: Expat Reporting Guide

US expats with foreign accounts over $10,000 must file FBAR. Learn how Form 8938 differs, current penalty amounts, and how to catch up.

Geographic ArbitrageJune 19, 2026

Geographic ArbitrageJune 19, 2026

Nairobi Expat Guide: M-Pesa Banking and Class N Permit

How US expats use M-Pesa, open Kenyan bank accounts, handle FBAR, and get the Class N permit ($1,200/year) with zero Kenyan tax on foreign income.