GILTI Is Dead: New NCTI Tax Rules for Expat Business Owners

The One Big Beautiful Bill Act renamed GILTI to NCTI and raised the effective rate from 10.5% to 12.6%. Here is what expat business owners must do now.

GILTI became NCTI in 2026 under the OBBBA. The effective rate rose to 12.6%, QBAI was eliminated. US expats with foreign corps need a new plan.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

If you own a foreign corporation and filed your U.S. taxes correctly last year, congratulations — you just learned rules that no longer apply. The One Big Beautiful Bill Act (OBBBA), signed into law in 2025, renamed GILTI — Global Intangible Low-Taxed Income — to Net CFC Tested Income (NCTI) and quietly made the underlying math worse for most expat business owners. The effective federal rate climbed from 10.5% to 12.6%, the asset exclusion that protected tangible businesses was eliminated, and the rules for who gets caught expanded. Most people haven't noticed yet.

This guide is for U.S. citizens and green card holders who own 10% or more of a foreign corporation — whether that's a holding company in Panama, a consulting LLC in Georgia, a Colombian SAS, or an Estonian OÜ. If any of those describe you, read every section.

What GILTI Was — and Why Everyone Hated It

GILTI was introduced in 2018 as part of the Tax Cuts and Jobs Act. The intent was to stop multinationals from parking profits in low-tax jurisdictions indefinitely. The execution caught millions of small expat business owners in its crossfire.

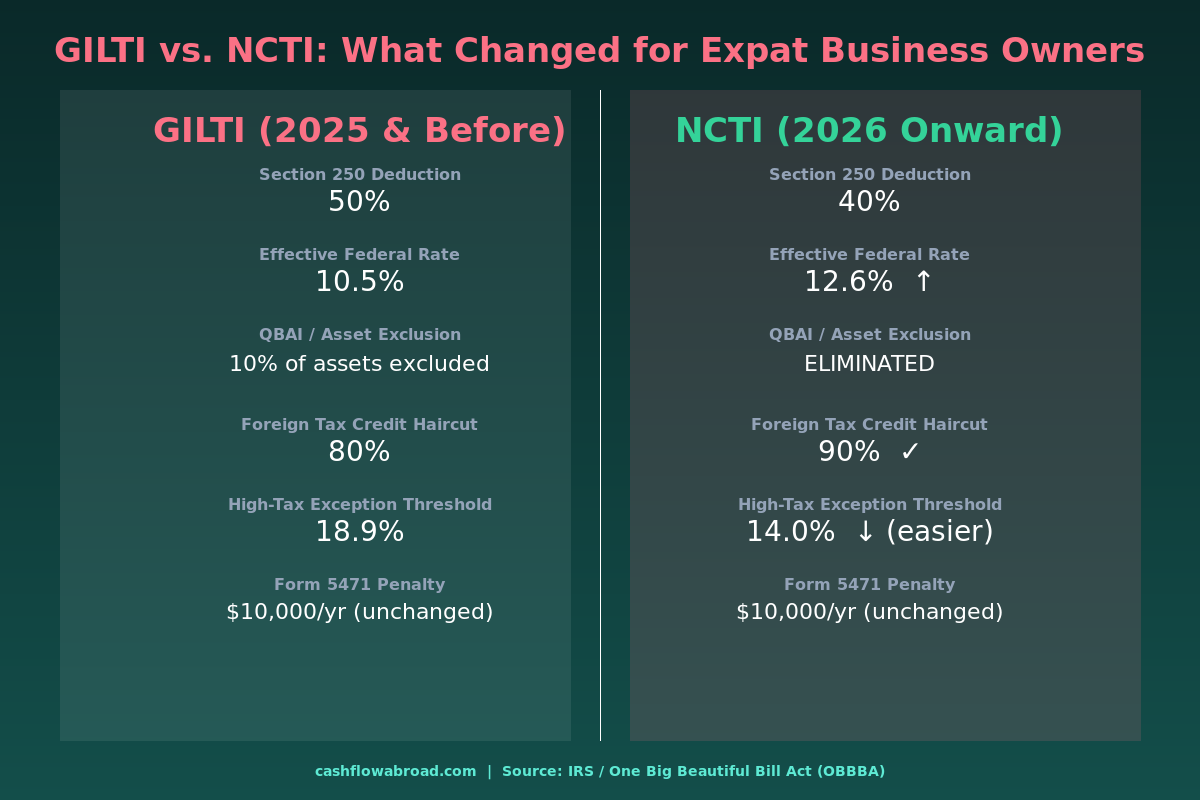

The basic mechanic: if you owned 10% or more of a foreign corporation, you owed U.S. tax on your share of that corporation's profits every year — regardless of whether you took a distribution. Profits stayed offshore, but the tax bill arrived anyway. The effective rate for individual expats using the Section 962 election was 10.5%, after a 50% Section 250 deduction on the 21% corporate rate.

The one saving grace was the QBAI exclusion — the Qualified Business Asset Investment carve-out. Under GILTI, you could subtract 10% of your corporation's tangible assets (property, equipment, physical infrastructure) from the income subject to tax. Businesses with real physical operations — a factory in Vietnam, a hotel in Portugal, a manufacturing facility in Poland — got meaningful relief. Service businesses and software companies got nothing, since they held few qualifying assets.

Then the OBBBA arrived. And the QBAI exclusion disappeared entirely.

What Changed: The GILTI to NCTI Transition

Effective January 1, 2026, GILTI was officially renamed Net CFC Tested Income (NCTI) under Section 951A of the Internal Revenue Code, as amended by the One Big Beautiful Bill Act. Four structural changes came with the rebrand:

1. The Effective Rate Went Up

The Section 250 deduction — the mechanism that reduces the corporate income base before tax is applied — dropped from 50% to 40%. On a 21% corporate rate, the arithmetic produces an effective NCTI rate of 12.6% (21% × 60% = 12.6%). That's a 20% increase in the actual tax owed compared to GILTI's 10.5% rate. On $200,000 in foreign corporate profit, the difference is $4,200 more per year.

2. The QBAI Exclusion Is Gone

Under old GILTI, if your foreign corporation owned $500,000 in qualified tangible assets, you subtracted $50,000 (10% of QBAI) from your tested income before calculating the tax. Under NCTI, that subtraction no longer exists. Your full net tested income is in scope, regardless of how capital-intensive your business is. Businesses that relied on the QBAI exclusion to reduce or eliminate their GILTI liability now face the full rate on 100% of their foreign profits.

3. The Foreign Tax Credit Haircut Improved (Slightly)

The indirect foreign tax credit available on NCTI — the credit you claim for taxes already paid to the foreign jurisdiction — increased from 80% to 90% under Section 960(d). If your foreign corporation paid $30,000 in local taxes, you can now claim $27,000 as a credit against your U.S. NCTI liability, up from $24,000. This partially offsets the rate increase for expats in higher-tax countries but does nothing if your foreign jurisdiction charges little or no corporate tax.

4. The High-Tax Exception Got Easier to Qualify For

The high-tax exception — the cleanest path to avoiding NCTI entirely — now triggers at a 14% local tax rate, down from 18.9% under GILTI. If your foreign corporation faces an effective local tax rate of at least 14%, you can elect to exclude that income from NCTI calculation entirely. Countries including Germany, France, the UK, Japan, Australia, Canada, Spain, and Italy all clear this threshold comfortably. Even some countries with substantial corporate rates — Colombia charges 35%, Mexico 30%, Portugal 21% — qualify easily.

Who Gets Hit: The 10% Ownership Threshold

NCTI applies if you are a U.S. shareholder who owns, directly or indirectly, 10% or more of the total combined voting power or total value of a Controlled Foreign Corporation (CFC). A foreign corporation is a CFC when U.S. shareholders collectively own more than 50% of it. Most expat business structures qualify.

This means a Colombian SAS you own 100% of is a CFC. A Hong Kong limited company you own 70% of with a local partner is a CFC. Even a holding company in a territorial tax jurisdiction like Panama — where the local tax on foreign-source income is zero — is still a CFC if you own 10% or more and it triggers the income thresholds.

What's not a CFC for NCTI purposes: a disregarded entity (single-member foreign LLC treated as a flow-through) and a foreign partnership. These structures are taxed differently, which matters enormously for planning purposes covered below.

One 2026 rule change worth noting: NCTI income is now allocated to U.S. shareholders who own stock at any time during the tax year, not just on the last day. A planning window where some advisors recommended timing ownership transfers near year-end has been closed.

The Math: A $150,000 Profit Example

Consider an expat with a single-member foreign corporation generating $150,000 in net profit in a zero-tax jurisdiction — say, a Panama corp running a remote consulting practice:

| Item | Under GILTI (2025) | Under NCTI (2026) |

|---|---|---|

| Net tested income | $150,000 | $150,000 |

| QBAI exclusion | $0 (service biz) | N/A — eliminated |

| Section 250 deduction | $75,000 (50%) | $60,000 (40%) |

| Taxable income | $75,000 | $90,000 |

| Tax at 21% corporate rate | $15,750 | $18,900 |

| Foreign tax credit (zero-tax jurisdiction) | $0 | $0 |

| Net U.S. tax owed | $15,750 | $18,900 |

Same business, same income, $3,150 more in U.S. taxes owed due solely to the deduction change. Now add the QBAI impact for a business with tangible assets. A Vietnamese manufacturer with $300,000 in qualified equipment could previously exclude $30,000 from GILTI tested income. Under NCTI, that shield is gone entirely — meaning even capital-heavy operations now pay on their full profit.

The Four NCTI Escape Routes

Route 1: High-Tax Exception Election

If your foreign corporation pays effective local taxes of at least 14% on its income, you can elect to exclude that income from NCTI entirely under the high-tax exception. This is an annual election filed on Form 8992. Countries that qualify include virtually all of Western Europe, Japan, Australia, Canada, and most Latin American nations. The 14% threshold is genuinely achievable — and a qualifying election produces a clean $0 NCTI bill.

The catch: some countries have preferential regimes for certain income types — capital gains, intellectual property, dividends — that result in effective rates below 14% even when headline rates are higher. You need to calculate based on what the foreign corporation actually paid, not the statutory rate.

Route 2: Section 962 Election

The Section 962 election is the primary planning tool for expats whose foreign corporations sit in low-tax or zero-tax countries. It allows an individual U.S. shareholder to elect to be treated as a domestic corporation for NCTI purposes, capping the effective rate at 12.6% and allowing you to claim 90% of foreign taxes paid as a credit.

For expats in zero-tax jurisdictions with no local corporate tax to offset, the Section 962 election still applies the 12.6% rate without any FTC benefit. For those paying even modest foreign taxes — 5% to 10% locally — the creditable amount reduces the effective U.S. rate meaningfully. Section 962 only covers the NCTI inclusion; when you eventually repatriate earnings as dividends, a second layer of individual income tax can apply on the distribution. Structure the timing of distributions carefully.

Route 3: Disregarded Entity Election (Check-the-Box)

Single-owner foreign corporations can elect to be treated as disregarded entities for U.S. tax purposes under the "check-the-box" regulations (Form 8832). Once elected, the foreign entity is invisible to the IRS — you report the income directly on your personal return as self-employment income, not as CFC income subject to NCTI rules.

This is powerful because disregarded entity income qualifies for the Foreign Earned Income Exclusion (FEIE). The 2026 FEIE limit is $132,900. If your foreign business generates $120,000 in active service income and you qualify under the bona fide residence or physical presence test, you can exclude the full amount — bringing your U.S. income tax on that income to $0. You'll still owe self-employment tax (15.3% on net earnings), but compared to the 12.6% NCTI rate with no FEIE offset, the math often favors the disregarded entity path for service businesses earning under the exclusion threshold.

The tradeoffs: Form 8858 replaces Form 5471 (simpler, same $10,000 penalty for missing it), and the election is irrevocable for 60 months without IRS permission. Analyze your income level, country, and business type before committing.

For the full mechanics of the FEIE — bona fide residence test, physical presence test, and the housing exclusion add-on — see our guide on how expats legally pay zero federal income tax.

Route 4: Subpart F Income and Passive Structuring

NCTI does not apply to Subpart F income — income that's already taxed currently under separate Subpart F rules, including passive income like dividends, interest, and rents from unrelated parties. If your CFC earns mostly passive income, Subpart F governs at your ordinary income rate (up to 37%), which can be higher than 12.6%. If it earns active business income, NCTI applies. The distinction matters because passive-heavy structures may be better served by different planning than the routes above. For the related issue of passive foreign investment vehicles, our PFIC guide for expat investors covers how investment income in CFCs gets classified and taxed.

Form 5471: The $10,000 You Can't Afford to Miss

Every U.S. shareholder who owns 10% or more of a CFC must file Form 5471 with their annual tax return — attached directly to your personal Form 1040 or 1120. The form reports the CFC's income, assets, distributions, and tax paid. It has five ownership categories, with different schedules required depending on your percentage and income type. NCTI reporting also adds Form 8992 to the package.

Missing Form 5471, filing it late, or filing it incomplete triggers a $10,000 penalty per form per tax year. If the IRS notifies you and you still don't comply, that penalty can escalate to $50,000–$60,000. There is essentially no first-time waiver culture around this penalty, and the IRS has been receiving foreign account data automatically via FATCA since 2014 — the odds of detection have increased every year.

If you elected disregarded entity status (Route 3), you file Form 8858 instead. Still a $10,000 annual penalty for missing it, but the form itself is considerably simpler. Either way, don't skip the compliance filing thinking the IRS won't notice. They will, eventually, and the statute of limitations doesn't run until the form is filed.

How NCTI Plays Out by Country

| Country | Corporate Rate | High-Tax Exception? | NCTI Exposure |

|---|---|---|---|

| Panama | 0% (foreign-source) | No | Full 12.6% — use §962 or disregarded entity |

| Georgia | 0% (virtual zone) / 15% standard | Virtual zone: No; Standard: Yes | Depends on income classification |

| Paraguay | 10% | No (below 14%) | 12.6% less 90% of 10% FTC = ~3.6% net |

| UAE / Dubai | 9% | No (below 14%) | 12.6% less 90% of 9% FTC = ~4.5% net |

| Colombia | 35% | Yes | High-tax exception eliminates NCTI |

| Portugal | 21% | Yes | High-tax exception eliminates NCTI |

| Estonia | 0% retained / 20% distributions | Complex per year | Analyze by distribution year — special rules apply |

| Germany | ~30% combined | Yes | High-tax exception eliminates NCTI |

Dubai is instructive. The UAE's 9% corporate tax is below the 14% NCTI high-tax exception threshold, so you can't elect your way out — but the improved FTC haircut (90%) means you credit 8.1% of that 9% against a 12.6% NCTI bill, leaving a net U.S. rate of roughly 4.5% on Dubai CFC income. Our Dubai expat tax guide covers the full picture including the UAE-U.S. tax treaty situation (there isn't one).

Paraguay is similar: a 10% local rate is below 14%, so no exception, but the 9% creditable FTC (90% of 10%) brings the net NCTI exposure down to about 3.6%. Still real, still requires filing — but manageable.

Your Infrastructure: Banking and Address

Expat business owners navigating NCTI compliance need a functioning U.S. banking stack. Mercury is the clean choice for online businesses — no monthly fees, U.S. routing numbers compatible with every payment processor, and straightforward wire/ACH setup for receiving client payments from abroad.

You'll also need a permanent U.S. mailing address for IRS correspondence, state domicile, and Form 5471 submissions. A Traveling Mailbox virtual address (starting at $15/month) gives you a real U.S. street address in the state of your choice, with mail scanning and check deposit — essential for receiving anything the IRS sends in connection with foreign corporation filings. Choosing the right state matters: some states have no income tax on foreign-source income; others have aggressive residency rules. See our guide to state taxes following expats abroad for the domicile analysis.

NCTI Action Checklist for 2026

- Verify CFC status. If you own 10%+ of a foreign corporation and U.S. shareholders collectively hold 50%+, it's a CFC subject to NCTI.

- Calculate your effective local tax rate. If above 14%, file Form 8992 to elect the high-tax exception. This is an annual election — it doesn't carry forward automatically.

- Evaluate the disregarded entity path. If you own 100% of the foreign corporation and earn active service income under $132,900, the check-the-box election plus FEIE often produces a better result than Section 962. Run the numbers with a CPA.

- Rerun your QBAI math. If you previously relied on the 10% tangible asset exclusion to reduce your GILTI, that's gone. Your NCTI base is now higher by exactly that excluded amount.

- File Form 5471 or Form 8858. Every year, without exception. The $10,000 penalty is assessed per form per year and the IRS is increasingly automated in detecting non-filers via FATCA data.

- Time your distributions carefully. NCTI taxes you on undistributed profits annually. When you eventually distribute, plan for the second-layer individual income tax on the dividend — coordinate with your CPA to avoid surprises.

For the broader picture of running a profitable business from abroad — including entity selection, banking, and the full compliance stack — our guides on running a U.S. business while living in Colombia and offshore company tax traps cover the structural decisions in depth.

The Bottom Line

Renaming GILTI to NCTI is less important than what moved underneath the label. The rate went up 20%, the QBAI buffer is gone, the high-tax exception threshold dropped to 14%, and the foreign tax credit improved modestly. For expat business owners in zero-tax or low-tax jurisdictions, the 2026 math is modestly worse. For those in countries above 14%, it's now easier — not harder — to eliminate the U.S. inclusion entirely.

The common thread across every planning scenario: this tax doesn't manage itself. NCTI elections are annual, Form 5471 is mandatory, and the disregarded entity decision is irrevocable for five years. Getting the structure right once, and maintaining it correctly year after year, is the only way to stay ahead of it.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute tax, legal, or financial advice. U.S. international tax law is complex and highly fact-specific. Consult a qualified CPA or international tax attorney before making any decisions about your foreign business structure, NCTI elections, Form 5471 filing obligations, or disregarded entity elections. All figures reflect 2026 IRS guidance and the One Big Beautiful Bill Act as enacted; verify current thresholds with IRS publications before filing.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJune 16, 2026

Expat Tax & FinanceJune 16, 2026

Form 5471: US Expats Who Own Foreign Companies

Filing Form 5471 is required for US expats who own 10% or more of a foreign corporation. Learn the five categories, $10,000 penalties, and how to

Expat Tax & FinanceJune 14, 2026

Expat Tax & FinanceJune 14, 2026

Form 5471 for Expats: CFC Reporting and Penalty Guide

Own a foreign corporation with 10% US ownership? Form 5471 is mandatory — missing it costs $10,000 per entity per year automatically.

Expat Tax & FinanceJuly 2, 2026

Expat Tax & FinanceJuly 2, 2026

S-Corp vs LLC for US Expats: SE Tax Savings Compared

US expats pay 15.3% SE tax on LLC profits even with FEIE. Learn when an S-corp election saves tax, how GILTI affects foreign corps, and when to use a