Form 3520: The Foreign Gift Trap Most Expats Miss

Your parents wire you $180k from abroad and you owe a $45,000 IRS penalty — on money that isn't taxable. Form 3520 is the form most expats never knew existed.

Miss Form 3520 and owe 25% of your foreign gift amount in IRS penalties — on money that isn't even taxable. Here's what every US expat needs to know.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Your parents sold the family home in Mexico City and wired you $180,000 to help with a down payment in Lisbon. Zero tax owed — it's a gift, not income. Except the IRS wants a form anyway, and if you didn't file it, the penalty is $45,000. Not because you evaded anything. Because you didn't know a form existed.

That's Form 3520 — one of the most commonly missed tax forms in the entire US expat filing stack, and one with some of the sharpest penalties in the tax code. Unlike the FBAR (which lives at FinCEN) or the FEIE (which reduces your taxable income), Form 3520 has nothing to do with what you owe. It's a pure information return — the IRS wants a record of large foreign gifts, inheritances, and transactions involving foreign trusts. File it, no problem. Ignore it, and you're staring at a 5% monthly penalty that caps at 25% of the entire gift amount.

For a $180,000 gift left unreported for five months: $45,000 in penalties on money you never earned, from taxes you never owed.

What Is Form 3520?

Form 3520 is the Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts. It's filed with the IRS and covers three distinct scenarios:

- You received a large gift or bequest from a foreign individual or foreign estate

- You received money or assets from a foreign trust

- You transferred assets to a foreign trust

The form doesn't trigger any tax. Foreign gifts are not taxable income in the US — the recipient never owes gift tax (that's the donor's obligation in most countries, or nobody's in countries without gift tax). But Congress decided in 1996 that it wanted a paper trail on large cross-border transfers, so here we are.

For expats, scenario 1 is by far the most common: aging parents in a foreign country leave you an inheritance, or wealthier family abroad helps with a financial milestone. For expats who have established foreign business structures or retirement arrangements, scenarios 2 and 3 come into play — and carry even steeper penalties.

Who Must File

Any "US person" who received a qualifying foreign gift or distribution must file Form 3520. A US person includes:

- US citizens (regardless of where they live)

- Green card holders

- US resident aliens meeting the substantial presence test

The requirement doesn't go away when you move abroad. A dual citizen living in Canada who receives a $200,000 inheritance from a German grandparent still has a Form 3520 obligation. The passport on your desk doesn't matter — the citizenship does.

What Triggers the Filing Requirement

There are two thresholds, and they apply to different types of senders:

| Source of Gift or Bequest | Reporting Threshold (2026) |

|---|---|

| Foreign individual or foreign estate | Over $100,000 aggregate in the calendar year |

| Foreign corporation or foreign partnership | Over $20,573 aggregate in the calendar year |

The aggregate part is critical. You don't evaluate each transfer separately — you add up all gifts from foreign persons received during the year. Two $60,000 transfers from your parents abroad in the same tax year sum to $120,000 and push you over the threshold. Both transfers combined trigger one Form 3520 filing.

Also worth knowing: the $100,000 threshold applies per family unit. If your parents and grandparents in a foreign country all transfer money to you in the same year and the IRS concludes they're acting in concert, those transfers get aggregated together.

The Traps Expats Actually Fall Into

This isn't a theoretical risk. Form 3520 gets missed constantly, and the IRS has ramped up enforcement on information returns. Here are the most common triggers:

Foreign Inheritances

A parent or grandparent dies abroad and leaves you property, cash, or investments. If the total value exceeds $100,000, you have a Form 3520 obligation even though an inheritance is definitionally not income. Most expat families and their local estate attorneys have never heard of this US requirement — and never raise it.

Family Support Transfers

Parents helping with a home purchase, tuition, or a business is common in many cultures. If foreign family members wire you more than $100,000 in a year — for any reason, a wedding gift, down payment help, startup capital — it's a reportable event. The purpose of the gift doesn't matter; only the threshold does.

Foreign Pension Plans Classified as Trusts

Some foreign retirement accounts — including UK SIPPs, Australian superannuation funds, and certain Canadian pension structures — are classified as foreign trusts under US tax law. Distributions from these vehicles can trigger both the trust reporting provisions of Form 3520 and a separate Form 3520-A (the annual return the foreign trust itself is supposed to file). Failure to file Form 3520-A triggers a 5% penalty on trust assets — per year.

Gifts from Foreign Companies

The $20,573 threshold for foreign corporations is low enough to catch many transactions. If you receive stock, property, or cash from a foreign business — including one in which family members are shareholders — you may cross this threshold faster than you'd expect.

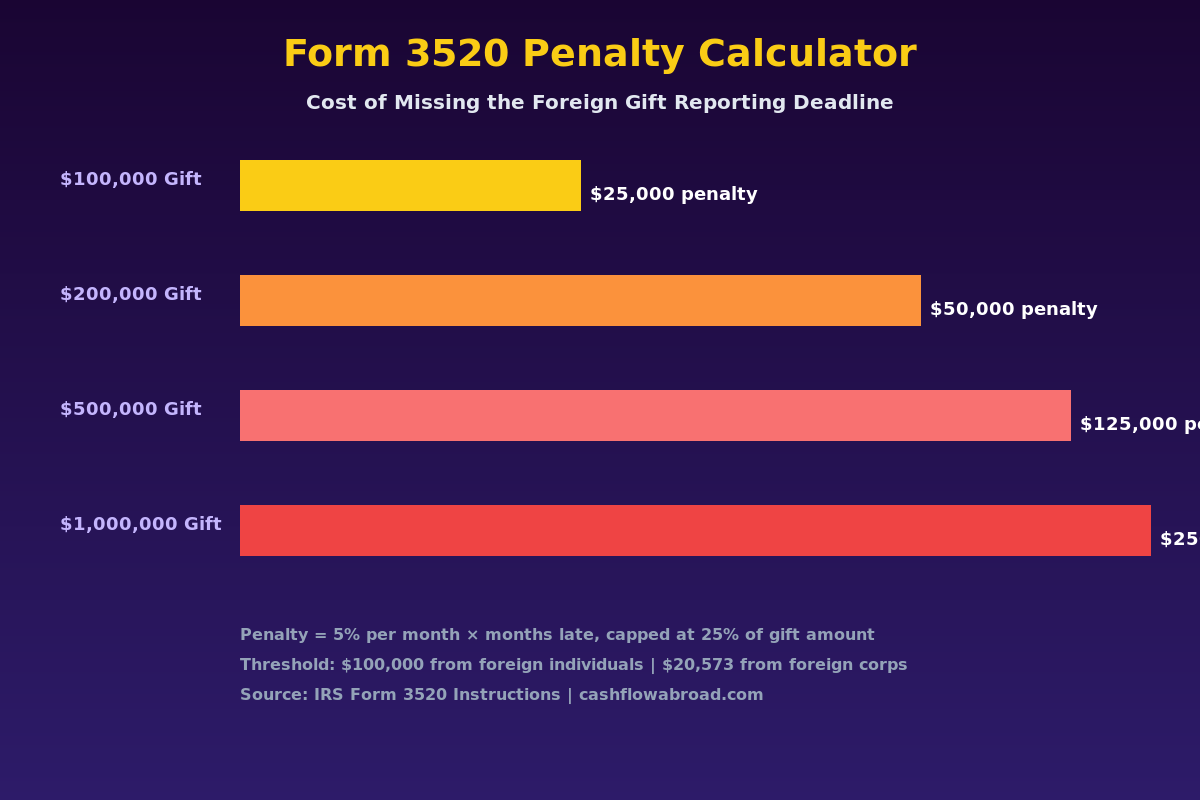

The Penalty Math That Makes This Urgent

The IRS does not treat information return failures gently, and Form 3520 is no exception:

| Violation Type | Penalty |

|---|---|

| Late or incomplete Form 3520 — foreign gifts | 5% of gift amount per month, up to 25% |

| Late or incomplete Form 3520 — trust distributions | 35% of gross distribution amount |

| Late or missing Form 3520-A — foreign trust annual return | 5% of trust assets per year |

| Minimum penalty in any case | $10,000 |

Run the numbers on real scenarios:

- $100,000 gift, 5 months late: $25,000 penalty

- $300,000 inheritance, 5 months late: $75,000 penalty

- $500,000 foreign trust distribution, not reported: $175,000 penalty

None of those penalties involve any tax liability on the underlying money. You received a gift. You owed no income tax. You owe five or six figures anyway — for missing a form.

The IRS can waive penalties for "reasonable cause" — but the standard is real. "I didn't know" doesn't automatically qualify. You need documentation: that you relied on a competent professional whose advice turned out to be wrong, or that genuine ambiguity existed about how the rules applied to your situation.

How and When to File

Form 3520 is not filed with your regular income tax return — it's mailed separately to an IRS processing center (as of 2026, Ogden, Utah — verify the current address in the Form 3520 instructions, as this occasionally changes).

Key deadlines:

- Calendar year filers: Due April 15, same as your 1040

- Expats with the automatic June 15 extension: Form 3520 follows the same deadline

- With a full extension to October 15: Form 3520 is also extended — but you must file Form 4868 to activate the extension

The form asks for:

- The name, address, and tax identification number of each foreign donor (if known)

- The date and dollar amount of each transfer

- A description of the property received

If you don't have the foreign donor's tax ID — most non-US persons don't have a US TIN — you leave that field blank with an explanation. That's acceptable. The IRS just wants the disclosure on record.

Already Behind? Your Options

If you received foreign gifts or inheritances above the thresholds in prior years and never filed Form 3520, correction paths exist that don't require hoping the IRS never finds out.

Delinquent Information Return Submission Procedures

The IRS has a specific procedure for taxpayers who are otherwise compliant but missed information returns like Form 3520. You file the delinquent forms with an attached statement explaining the late filing. If the IRS determines the failure was due to reasonable cause (not willful neglect), penalties may be waived entirely. This is the first option to explore for a one-time miss.

Streamlined Filing Compliance Procedures

If you're an expat who was non-compliant across multiple years — missing returns or foreign reporting forms like the FBAR — the Streamlined Foreign Offshore Procedures (SFOP) allow you to catch up with zero offshore penalty. You file three years of amended or delinquent returns and six years of FBARs, certify that the non-compliance was non-willful, and pay any back taxes owed. There's no dollar amount penalty for expats who qualify.

Important caveat: the streamlined procedures address the FBAR and your tax returns under specific IRS authority. Form 3520 penalties are assessed under separate authority. A qualified international tax attorney can navigate the overlap and structure a coordinated catch-up strategy.

Making a Reasonable Cause Argument

Even after receiving an IRS penalty notice, you can respond with a reasonable cause argument. Document:

- That you relied on a tax professional who didn't flag Form 3520

- That genuine ambiguity existed about the reporting obligation in your specific circumstances

- That you had no intent to conceal (particularly relevant for inheritances triggered by a death)

The IRS abates Form 3520 penalties under reasonable cause more frequently than practitioners often expect — particularly for first-time failures involving inheritances rather than ongoing structured gift arrangements. Act before the IRS contacts you. Once they send a notice, the negotiating position narrows sharply.

Form 3520-A: The Companion Form You Also Might Miss

Form 3520-A is the annual information return that a foreign trust is supposed to file with the IRS. In most cases, the foreign trust has no idea this obligation exists — foreign banks, pension funds, and family trusts don't have US tax departments monitoring these requirements. The IRS then treats the US beneficiary as responsible for the filing and assesses a 5% of trust assets penalty per year against them.

If you have a UK SIPP, Australian super fund, foreign family trust, or any financial arrangement that might be classified as a trust under US law, get explicit clarity from an international tax professional on whether Form 3520-A applies to your situation. The penalty accumulates annually and can compound over years before it's discovered.

Form 3520 also intersects with estate planning in ways most expats don't anticipate. If you're a beneficiary of a foreign estate that distributes assets over several years rather than in a lump sum, each distribution year has its own reporting requirement — not just the year the person died. This connects directly to broader expat estate planning decisions that compound in complexity as family wealth moves across borders.

Your Form 3520 Checklist: Run This Every Tax Year

- Did I receive any money, property, or assets from a non-US person?

- Did the aggregate value from foreign individuals or estates exceed $100,000?

- Did the aggregate from foreign corporations or partnerships exceed $20,573?

- Do I have any interest in or receive distributions from a foreign trust?

- Did I transfer any assets to a foreign trust?

If you answered yes to any of these and didn't file Form 3520, that's the first item to address — before optimizing the Foreign Earned Income Exclusion, before setting up brokerage structures, before anything else. A 25% penalty on a gift amount erases years of careful tax planning in a single IRS notice.

For expats managing ongoing cross-border financial relationships — receiving regular support from family, inheriting assets in stages, or benefiting from foreign business structures — a reliable US mailing address isn't optional. Form 3520 penalty notices have hard response deadlines. Traveling Mailbox ($15/month) gives you a real US street address in 50+ cities, scans your mail, and forwards IRS correspondence digitally — so a penalty notice sitting in a PO box you haven't checked in six months doesn't become an uncontested default. Read our full guide on why expats need a virtual mailbox.

The Bottom Line

Form 3520 is not a tax. It's a disclosure requirement with a penalty structure that doesn't care whether you owe anything. A $25,000 penalty on a $100,000 gift hits harder than most income tax scenarios you'd work years to optimize around — and it arrives on money that isn't taxable at all.

The form itself isn't complicated. The knowledge gap is. Most expat families handling cross-border transfers have never encountered Form 3520, and US tax preparers without international experience often miss it. If your current accountant didn't raise this form in the same conversation as the FBAR and Form 8938, ask directly: "Does any foreign gift or inheritance I've received trigger Form 3520?" Then get the answer in writing.

For anyone already behind, the correction path is real — delinquent submission procedures and reasonable cause arguments have genuine traction with the IRS for genuine first-time failures. But the window for the best outcomes is before the IRS contacts you. After they send a notice, your options narrow and your leverage disappears.

Disclaimer: This post is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change and individual circumstances vary widely. Consult a qualified international tax professional — ideally a CPA or tax attorney with US expat experience — before making decisions about foreign gift reporting, foreign trust obligations, or IRS compliance. Penalties described reflect IRS guidance current as of publication but may change with inflation adjustments and regulatory updates.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 5, 2026

Expat Tax & FinanceMay 5, 2026

Australian Super & US Taxes: The Trap Nobody Warns You About

The US-Australia treaty gap exposes your super to annual IRS taxation and 0,000/yr penalties. What every US expat in Australia must know.

Expat Tax & FinanceMay 1, 2026

Expat Tax & FinanceMay 1, 2026

IRS Streamlined Filing: Catch Up on Expat Taxes for Free

The IRS offers a penalty-free amnesty program for US expats who missed tax filings. SFOP lets you catch up on 3 years of returns and 6 FBARs with

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

Canadian TFSA and US Taxes: The Reporting Trap

US citizens holding a Canadian TFSA owe tax on all annual growth and must file Form 3520 — PFIC rules apply to Canadian mutual funds inside the