Foreign Mortgages for Expats: How Americans Buy Property Abroad

Most US banks won't finance a foreign property. Here's which countries let Americans get mortgages, current rates, IRS reporting rules, and the 5 mistakes that cost buyers 0k+.

Which countries let Americans get mortgages? Current rates, LTV caps, IRS reporting rules, and the 5 costly mistakes foreign property buyers make.

Rocket Mortgage won't touch it. Bank of America won't either. Neither will Chase, Wells Fargo, or virtually any lender in the Fannie Mae/Freddie Mac universe. If you want a mortgage on a property in Portugal, Panama, or Mexico, your US bank is already out of the picture — and most buyers don't discover this until they're weeks into a purchase process.

Yet Americans are buying homes abroad with local financing every single week. In Panama, they're closing at 6.5–9% interest with 30% down. In Portugal, rates are sitting under 3.5% on 20-year terms. In Mexico, cross-border lenders are funding deals at 70% LTV with an all-in annual cost around 14%. The mechanics are different from a US mortgage, the paperwork is more demanding, and the mistakes are more expensive — but the financing exists.

This guide covers exactly how it works: where you can borrow, what rates look like today, what the IRS expects from you afterward, and the specific mistakes that cost buyers $20,000–$50,000 before they've made a single mortgage payment.

Why No US Lender Will Finance a Foreign Property

The issue isn't regulatory — it's collateral. US mortgage lenders operate within the Fannie Mae/Freddie Mac conforming loan framework, which requires the property to be located in the United States. A villa in Lisbon or a condo in Panama City cannot serve as collateral for a US-originated mortgage because US courts cannot enforce a foreign lien in a foreclosure scenario.

There are two partial exceptions. HSBC Premier/Jade clients can leverage an existing HSBC international banking relationship to access mortgages in select countries (UK, Australia, Hong Kong, UAE) — but Latin America coverage is minimal and requires significant HSBC deposits. And home equity extraction — refinancing a US property to pull out cash, then buying abroad with that cash — is the workaround most Americans actually use. With US cash-out refi rates around 6.5–7.5% in 2025, this often beats local Latin American mortgage rates anyway.

For everything else, you need a local bank in the target country, an international mortgage broker, or developer financing. Here's what that actually looks like.

Country-by-Country Mortgage Breakdown

| Country | Rate (Non-Resident) | LTV Cap | Min. Down | Currency Risk | Max Term |

|---|---|---|---|---|---|

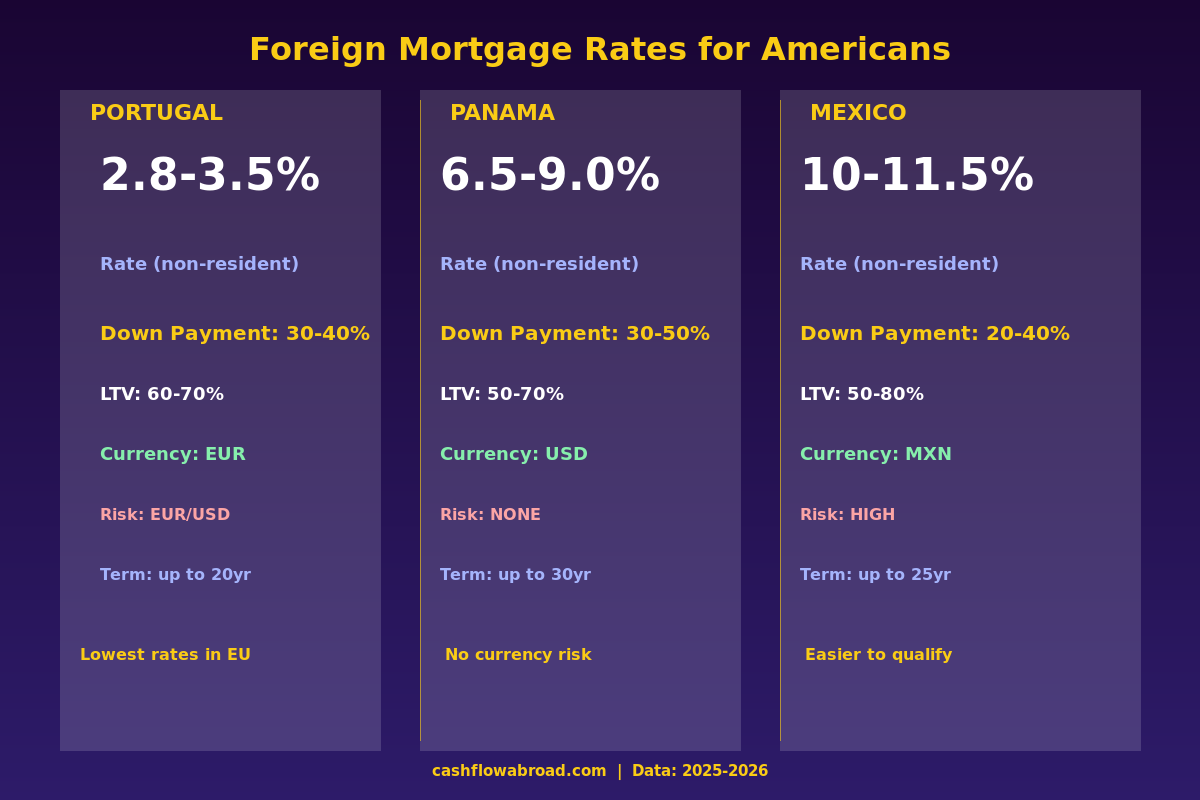

| Portugal | 2.8%–3.5% | 60–70% | 30–40% | EUR/USD (significant) | 30 years |

| Spain | 3.5%–5.0% | 60–70% | 30–40% | EUR/USD (significant) | 20 years |

| Panama | 6.5%–9.0% | 50–70% | 30–50% | None (USD economy) | 30 years |

| Costa Rica | 7.0%–9.5% | 50–60% | 40–50% | CRC/USD (moderate) | 20 years |

| Mexico | 10.0%–11.5% | 50–80% | 20–40% | MXN/USD (high) | 25 years |

| Colombia | 10.4%–17.75% | 50–70% | 30–50% | COP/USD (very high) | 20 years |

Portugal and Spain: Cheapest Rates, Biggest Currency Trap

Portugal's new mortgage rates dropped to 2.83% in early 2026 on the back of ECB rate cuts — historically low. Non-residents pay a spread of 0.4–0.7% above the resident rate, landing in the 2.8–3.5% range. Spain runs 3.5–5.0% fixed for non-residents, with variable Euribor-linked products at Euribor + 1.2–2.0%.

The catch: you're borrowing in euros. If you earn in dollars and the USD weakens 15% against the EUR during your holding period — a scenario that's happened multiple times in the past decade — your effective borrowing cost jumps by that same 15% in dollar terms. Over a 20-year term, currency moves can dwarf the interest rate advantage entirely. Neither country remains a pathway to EU residency through property: Spain ended its Golden Visa program on April 3, 2025, and Portugal removed real estate from its Golden Visa qualifying categories in October 2023.

Panama: The Clear Winner for Dollar Earners

Panama uses the US dollar as its official currency. There's no MXN/USD conversion risk, no COP depreciation spiral, no euro exposure. A Panamanian mortgage stays in dollars from origination to payoff. This eliminates what is usually the biggest hidden cost of buying abroad.

Rates run 6.5–9.0% for non-residents, plus a 1% FECI tax on mortgage interest that pushes the effective rate to 7–9%. LTV caps sit at 50–70%; the Friendly Nations Visa — available to US citizens — can improve your terms with some banks. Panama also permits foreigners to own most property outright without trust structures. For Americans doing geographic arbitrage who want real estate exposure without currency complexity, Panama is the default answer.

Mexico: High Rates, Cross-Border Products Available

Mexico's mortgage market is genuinely accessible to Americans — cross-border lenders advertise rates around 11.42% with an all-in annual cost (CAT) near 14.09%. Expensive relative to US rates, but more accessible on documentation, with some products going to 70–80% LTV at 20–30% down.

Two non-negotiables: First, if the property is within 50km of a coastline or 100km of a border, you cannot hold it directly — you need a fideicomiso (bank trust), costing $1,000–$2,000 to set up and $500–$1,000/year to maintain. Second, closing costs average 4–6% of purchase price on top of your down payment. Mexico is the rental property market where many Americans make their first foreign real estate move — developer financing at 8–12% for new construction is common and requires less paperwork than bank financing.

Colombia: Effectively Cash-Only for Non-Residents

As of 2025, Colombian banks have tightened non-resident lending to the point of functional unavailability through standard channels. Rates for qualified borrowers range from 10.4% to 17.75% — reflecting Colombia's high central bank rate environment and peso volatility premium. Most foreign buyers in Medellín and Bogotá pay cash or negotiate developer financing at closing. Plan for cash unless you have local residency and a Colombian income source.

How to Actually Get a Foreign Mortgage

The process follows a predictable sequence, but timeline surprises kill more deals than anything else. A clean case closes in 8–12 weeks. Add 3–6 weeks if you need apostilled US documents — required in Mexico and some EU countries. The apostille process through your state's Secretary of State takes 3–4 weeks. Start it before you find the property.

Step 1: Find your lender first. Approach local banks directly or engage an international mortgage broker. Global Mortgage Group covers 21 countries. Simon Conn specializes in Europe. Traverse International Finance focuses on Spain, Portugal, France, and Italy. Brokers don't lend — they match you to local banks and navigate paperwork.

Step 2: Gather documents. Standard requirements: passport, 2–3 years of US tax returns (1040), 3–6 months of bank statements, proof of income, source-of-funds letter. Have these ready before you make an offer.

Step 3: Execute a preliminary contract. After pre-approval in principle, you'll sign a purchase agreement (called promesa de compraventa in Latin America). This locks the price and typically requires a 1–10% non-refundable deposit. Do not sign without completing an independent title search first.

Step 4: Underwriting and appraisal. The bank orders its own appraisal ($300–$1,500) and formally underwrites the loan — 14–21 business days once complete documentation is received. Wire down payment funds at least 30 days before planned closing.

Step 5: Close before a notario. In most countries, closing happens before a notario público — a lawyer with judicial authority, not the US administrative variety. The mortgage deed is signed, transfer taxes paid, and the property registered.

US Tax Reporting: What the IRS Requires

Owning foreign real estate directly — in your own name — does not by itself require FBAR or Form 8938 filing. The reporting obligations kick in when you add bank accounts, entities, or rental income.

| Trigger | Form Required | Threshold | Non-Willful Penalty |

|---|---|---|---|

| Foreign bank account (rent/mortgage payments) | FBAR (FinCEN 114) | >$10,000 aggregate at any point | Up to $10,000/year |

| Foreign LLC or trust holds the property | Form 8938 (FATCA) | $200k–$300k for expats; $50k–$75k US-based | $10,000–$50,000 |

| Rental income from the property | Schedule E (Form 1040) | Any amount | Income tax + late penalties |

| Mexican fideicomiso (coastal trust) | Form 3520 potentially | Ownership of trust | Up to 35% of trust value |

Foreign rental property depreciates over 30 years — not the 27.5-year schedule for US domestic rentals. This is the ADS (Alternative Depreciation System) and it's mandatory. The longer schedule means smaller annual deductions, but you do get them. Foreign property taxes and mortgage interest are both deductible against your Schedule E rental income.

The Foreign Tax Credit (Form 1116) is your main shield against double taxation. Tax paid to Portugal, Spain, Panama, or Mexico on rental income can be credited dollar-for-dollar against your US tax liability on that same income. In practice this largely eliminates double taxation — but you must file Form 1116 to claim it.

Currency gains on a foreign-currency mortgage are taxable. If you borrowed €200,000 when EUR/USD was 1.10, and you repay when EUR/USD is 0.95, you've realized a US-taxable currency gain — even if the property itself broke even. This obscure provision blindsides sellers of European properties every year.

For thorough guidance on expat investment reporting, see the expat investing playbook and the US expat banking and taxes guide.

5 Mistakes That Cost Buyers $20,000+

1. Borrowing in a Currency You Don't Earn

A euro mortgage at 3.5% looks cheap until the USD weakens 20% against EUR over a 5-year hold. Your effective cost becomes 7.5%+. Use a forward contract to lock in exchange rates for large transfers, and choose USD-economy markets like Panama when currency certainty matters more than headline rate minimization.

2. Skipping the Independent Title Search

In most foreign markets, title insurance doesn't exist. Unpaid liens, back taxes, unpermitted construction, or a seller without clean title become your problem after closing. Always hire an independent attorney — not the agent's referral — before signing anything.

3. Transferring Funds Without Neutral Escrow

The US escrow system doesn't exist in most Latin American markets. Buyers have handed deposits directly to sellers or developers who then disappeared. Always use a neutral licensed escrow agent or attorney trust account — never transfer funds directly to a seller or developer.

4. Budgeting Only for the Down Payment

Buyer-side closing costs in Spain and Portugal total 10–15% of purchase price (transfer tax, notary, registration). Mexico runs 4–6%. Panama, 3–5%. These are on top of your down payment. A $300,000 purchase in Spain could require $120,000–$135,000 total at closing: $90,000 down plus up to $45,000 in transaction costs.

5. Missing FBAR or Form 8938 Deadlines

The $10,000 FBAR penalty for a non-willful violation is not hypothetical — it gets assessed. Willful violations carry fines up to $100,000 or 50% of the account balance per year, per account. Open a foreign bank account to manage your property and an FBAR obligation likely starts immediately. The IRS's growing international data-sharing network makes foreign accounts less invisible than they once were.

When Local Banks Say No: Your Alternatives

Cash-out refinance on a US property. At 6.5–7.5% in 2025, this beats nearly every Latin American mortgage rate and skips foreign bank underwriting entirely. The leverage stays on your US asset; the foreign property is bought outright. This is the most common path for buyers in Colombia and Costa Rica where local non-resident financing is scarce.

Developer financing. Common in Mexico, Panama, and Costa Rica for new construction. Terms typically run 8–12% over 5–15 years with 30–50% down. Documentation is lighter than bank financing. Stick to established developers with completed projects — if the developer defaults mid-build, recourse is difficult.

Self-Directed IRA. You can legally purchase foreign real estate inside a Self-Directed IRA or Solo 401(k). Rental income flows back tax-deferred (traditional) or tax-free (Roth). The structure requires a true SDIRA custodian and meticulous prohibited-transaction compliance, but the tax efficiency is compelling for a long-hold rental strategy.

For executing large international transfers to fund a foreign down payment, Remitly consistently beats bank wire rates on large USD transfers. If you're maintaining a US address for IRS correspondence, banking, and state domicile while living or investing abroad, Traveling Mailbox ($15/month) provides a real US street address in 50+ cities with mail scanning and check deposits — essential infrastructure for anyone buying foreign property while based overseas.

For maintaining US investment accounts alongside foreign property, Charles Schwab International is the gold standard for American expats — free worldwide ATM withdrawals, no foreign transaction fees, and a brokerage that doesn't close accounts because you live abroad. See the full zero-fee expat banking stack for complete financial infrastructure while holding foreign property.

The Bottom Line

Foreign mortgage financing is viable — in the right countries, with the right preparation. Panama leads for USD earners wanting zero currency risk at 6.5–9%. Portugal and Spain offer the lowest absolute rates (under 3.5%) but carry real EUR exposure and have eliminated their Golden Visa property pathways. Mexico is accessible but expensive, Costa Rica workable at 40–50% down, Colombia effectively cash-only for non-residents.

The mistakes aren't hard to avoid — they're just different from the US playbook. Independent title searches, neutral escrow, apostilled documents, and FBAR/Form 8938 compliance are the checklist items. Miss any of them and geographic arbitrage savings evaporate fast. Get them right and you've built equity in a market that appreciates independently of your US holdings.

For more on protecting foreign assets, see the expat estate planning guide to ensure foreign property passes to your heirs correctly.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute financial, tax, or legal advice. Mortgage rates, LTV ratios, and regulations change frequently — verify current terms directly with lenders and consult a qualified CPA or international tax attorney before making any property purchase or financing decision abroad. The author may receive compensation for affiliate links in this post.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageMay 13, 2026

Geographic ArbitrageMay 13, 2026

Expat Mortgages Abroad: How Americans Actually Get Approved

Portugal lends US expats at under 3%. Spain, Mexico, and France have real mortgage products for non-residents. Rates, LTV limits, and approval tips.

Geographic ArbitrageJuly 19, 2026

Geographic ArbitrageJuly 19, 2026

Sofia Remote Work Budget Under $2,000

Price rent, transit, utilities, insurance, and visa caveats before using Sofia, Bulgaria as a lower-cost EU base for remote work.

Geographic ArbitrageJune 30, 2026

Geographic ArbitrageJune 30, 2026

Moving Abroad with Kids: School Costs and Family Budget

International school fees change the whole geographic arbitrage math for families. Compare real costs in Medellín, Chiang Mai, Mexico, and Lisbon for