Expat Mortgages Abroad: How Americans Actually Get Approved

56% of expat buyers pay all cash—not because they have to. Portugal lends at under 3%, Spain at 60% LTV, Mexico offers 30-year terms. Here's how to get approved.

Portugal lends US expats at under 3%. Spain, Mexico, and France have real mortgage products for non-residents. Rates, LTV limits, and approval tips.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

More than half of Americans who buy property abroad pay entirely in cash. Not because they're richer than their neighbors, but because they assume no bank will touch a cross-border mortgage. That assumption costs buyers their leverage — and in some cases, their shot at ownership altogether.

The reality: Portugal lends to US buyers at rates under 3%. Spain courts non-residents with 60–70% LTV products. Mexico offers 30-year mortgages to foreign nationals with no residency requirement. The market exists. The problem is nobody tells Americans it does.

This guide breaks down who lends to US expats, what rates and LTV limits actually look like in 2026, and exactly what documentation you need to get across the finish line — including the parts that will trip you up specifically because you're American.

Why Your US Bank Won't Touch This

Standard Fannie Mae and Freddie Mac guidelines don't allow conventional US mortgages to be secured against foreign real property. Full stop. The rare US lenders who will consider foreign properties — mostly private banks serving ultra-high-net-worth clients — typically require $1M+ loan minimums, charge rates 2–3% above prime, and take 6+ months to close.

For most buyers, this means one of two paths: foreign bank financing in the country where you're buying, or a US-side home equity strategy (more on that later). Foreign bank lending is more accessible than Americans expect — but it comes with its own set of friction specific to US citizens.

What Foreign Banks Actually Require

Foreign lenders evaluate you on the same core factors as any mortgage — income stability, debt-to-income ratio, assets, credit history — but the documentation requirements multiply when you're earning in dollars while borrowing in euros or pesos.

Standard requirements across most countries:

- Proof of income: 2 years of US tax returns (Form 1040), pay stubs or employment letters, and if self-employed, business bank statements. If any document isn't in the local language, expect to pay for certified translations — typically $50–$150 per document.

- Credit report: Your US credit history doesn't automatically transfer. Most foreign banks will accept a US credit report (Experian or Equifax) but some require a local credit history. Experian has international credit reporting services that can help.

- Local bank account: Most countries require you to hold a local bank account before they'll process a mortgage application. Open one before you start shopping for properties.

- Passport and residency documentation: Some countries require proof of legal residency status; others lend to non-residents freely.

The one thing that complicates all of this specifically for Americans: FATCA.

The FATCA Problem Every US Buyer Faces

The Foreign Account Tax Compliance Act requires all foreign financial institutions to report US citizen account data to the IRS. Banks that fail to comply face a 30% withholding penalty on their US-sourced income. As a result, many foreign banks — especially smaller regional lenders — simply refuse to work with American clients rather than deal with the compliance burden.

In Portugal, for example, not all banks accept US clients. Those that do will require you to complete a FATCA self-certification form (usually a W-8BEN or W-9 equivalent) before the account can be opened. In France, some banks have quietly stopped accepting US nationals altogether since 2023.

The workaround: target banks with international divisions that already have FATCA compliance infrastructure in place. In most popular expat destinations, 2–4 larger banks will have this sorted. Research which ones before you fall in love with a property.

If you want to keep your US banking stable while you build local banking relationships abroad, a Charles Schwab International account gives you fee-free ATM withdrawals worldwide and no foreign transaction fees — useful for covering upfront costs while your local account gets established. For wiring purchase funds internationally, Remitly typically beats bank wire rates on the exchange spread, which matters when you're moving $50K–$200K+ for a down payment.

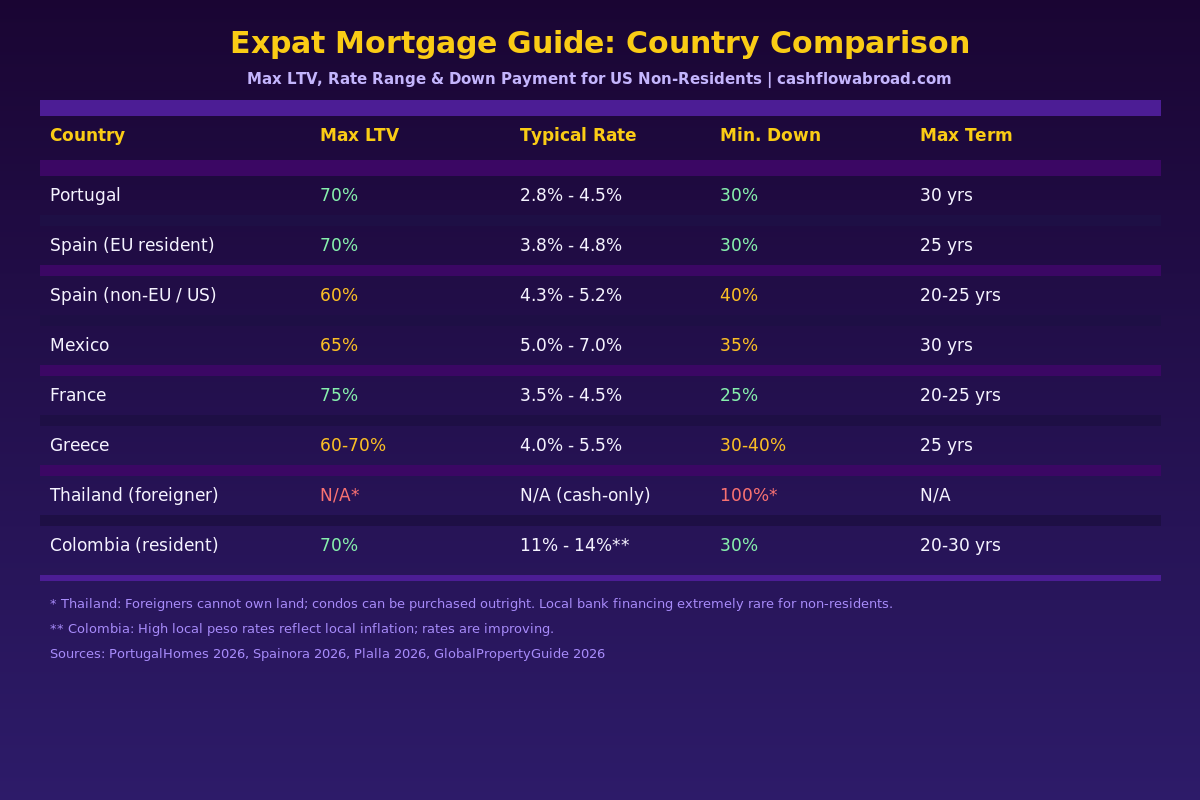

Country-by-Country: What You'll Actually Pay

Rates and LTV limits vary widely. The headline number you'll see advertised is usually for residents with clean local income. As a US expat or non-resident, expect to land at the conservative end of the range.

| Country | Max LTV (Non-Resident) | Typical Rate (2026) | Min. Down | Max Term | FATCA-Friendly? |

|---|---|---|---|---|---|

| Portugal | 70% | 2.8% – 4.5% | 30% | 30 years | Yes (varies by bank) |

| Spain (EU resident) | 70% | 3.8% – 4.8% | 30% | 25 years | Yes (major banks) |

| Spain (non-EU / US citizen) | 60% | 4.3% – 5.2% | 40% | 20–25 years | Yes (major banks) |

| Mexico | 65% | 5.0% – 7.0% | 35% | 30 years | Limited |

| France | 75% | 3.5% – 4.5% | 25% | 20–25 years | Difficult |

| Greece | 60–70% | 4.0% – 5.5% | 30–40% | 25 years | Yes (major banks) |

| Colombia (resident) | 70% | 11% – 14% COP | 30% | 20–30 years | Yes |

| Thailand (foreigner) | N/A | N/A | 100%* | N/A | N/A |

*Thailand: Foreign nationals cannot own land. Condo purchases are possible under the Condominium Act (up to 49% foreign ownership per building), but local bank financing for foreigners is effectively unavailable. Cash-only for most buyers.

Portugal: Best Rates, Easiest Process

Portugal is the most accessible market for US buyers right now. As of March 2026, new mortgage rates averaged 2.83%, with variable rates tied to Euribor (currently ~2.25%) plus a bank spread. Non-residents get a maximum LTV of 70%, down from 80% for residents, but the rates remain competitive relative to what you'd pay in the US on an investment property.

The catch: FATCA paperwork. Bring a completed W-9, be prepared to sign FATCA self-certification forms, and specifically target banks like Millenniumbcp, Santander Portugal, or Novo Banco, which have established US compliance processes. Novo Banco has been particularly expat-friendly in recent years.

Portuguese banks calculate affordability based on a 35% debt-to-income ceiling. If your US student loans, existing mortgage, and car payment already eat 25% of your gross income, you have 10% left to allocate — plan accordingly.

Spain: Bigger Down, but Viable at Scale

Euribor sitting at 2.25% in early 2026 makes Spanish mortgages attractive on paper, but the non-resident premium is real. As a US citizen, expect LTV capped at 60% (meaning you're putting 40% down) and rates in the 4.3–5.2% range on a fixed product.

The often-overlooked kicker: Spanish banks require you to pay roughly 10–12% of the purchase price in taxes and fees on top of the purchase price. On a €400,000 property, that means bringing €160,000 in down payment plus €48,000–€52,000 in fees — roughly €210,000 in total cash before you touch the mortgage. Buyers who run the numbers only on the LTV get blindsided.

Spanish banks also use an internal appraisal (tasación) that legally binds the loan amount. If the bank's appraiser values the property at €380,000 but you agreed to pay €400,000, your mortgage is calculated against €380,000. You absorb the difference in cash.

Mexico: Full Foreign Access, Higher Rates

Any foreigner — resident or not — can apply for a Mexican mortgage from local banks. BBVA México, Banorte, and Santander México all lend to non-residents. Terms of up to 30 years are available, with LTVs up to 65% (35% down). Rates run 5–7% as of 2026, reflecting the higher Banxico benchmark rate environment.

One important note: properties in Mexico's "restricted zone" (within 50km of a coast or 100km of an international border) cannot be directly owned by foreigners. To buy in Cabo, Puerto Vallarta, or the Riviera Maya, you must use a bank trust (fideicomiso) or a Mexican corporation. Both are legal structures with a well-established track record — banks incorporate this into the mortgage process — but they add $1,500–$3,000 in setup costs and $500–$700/year in trust maintenance fees.

Some buyers ask about seller financing instead. Seller financing (crédito vendedor) exists in Mexico and is sometimes offered on higher-priced properties, but terms are typically 3–7 years at higher rates, useful only as a bridge strategy.

How to Maximize Your Approval Odds

Foreign banks approve or decline based on factors you can influence before you apply. A few that matter more than most buyers realize:

Debt-to-income, calculated in their currency. If you earn $8,000/month in dollars, a bank will convert that to euros (or pesos) using that day's rate. A stronger dollar helps; a weaker one shrinks your qualifying income. Apply when your home currency is strong relative to the local one.

Two years of consistent, documented income. Freelancers and self-employed expats face the most friction here. Banks want to see consistent deposits over 24 months. If you switched from employment to freelance 18 months ago, wait another 6 months before applying — your approval rate goes up substantially.

A local bank account with 3–6 months of history. Opening an account before you apply signals commitment and gives the bank a local relationship. In Portugal, Millennium BCP and Caixa Geral de Depósitos both allow non-resident account opening in-person; some branches accept it remotely with notarized documents.

Use an international mortgage broker. Firms like Global Mortgage Group or America Mortgages specialize in cross-border financing for US citizens. They know which local banks accept US clients post-FATCA, understand how to present foreign income, and can get you pre-qualified before you make an offer. Their fee is typically 1–1.5% of the loan amount — worth it if it's the difference between approval and cash-only.

Also worth maintaining: a US virtual mailbox with a real street address. US banks, IRS correspondence, and credit reporting agencies all need a valid US address for their records. Some foreign lenders also want to verify your US address as part of anti-money laundering checks. Traveling Mailbox provides a real street address in 50+ US cities with mail scanning and check deposits for around $15/month — cheaper than an annual trip home to deal with misrouted mail.

The Currency Risk Most Buyers Ignore

Taking a mortgage denominated in euros, pesos, or baht when you earn in dollars creates a risk that doesn't appear on any bank's disclosure form. If the dollar weakens by 15% against the euro after you close, your monthly payment — in dollar terms — just increased by 15%. Your income probably didn't.

The practical implication: if you're earning dollars but servicing a euro mortgage, your effective interest rate floats with the exchange rate, not just with Euribor. In the 2020–2022 period, the dollar strengthened significantly against the euro, which cut effective mortgage costs for dollar earners. The reverse happened in 2023.

Three ways to manage this:

- Earn in local currency. If you have clients in Portugal or Colombia, invoicing in local currency gives you a natural hedge.

- Match mortgage currency to income currency. If you earn EUR through remote work for EU clients, a EUR mortgage is perfectly matched.

- Build a currency buffer. Keep 6–12 months of mortgage payments denominated in the loan currency before you close.

For regular monthly transfers from your US account to service the foreign mortgage, set up a recurring transfer through Remitly to minimize the spread drag over time. On a €1,200/month payment, even a 0.5% better rate versus a bank wire saves you around $72/year — consistent savings compounding over a 20-year mortgage.

US Tax Implications of a Foreign Mortgage

Here's where owning abroad gets complicated for Americans. The IRS taxes you on worldwide income regardless of where you live. What it doesn't always let you do is deduct the interest on a foreign mortgage.

Mortgage interest deductibility: The IRS allows deduction of qualified mortgage interest on a "qualified home," which can include a second home abroad — but only if the mortgage is secured by the property and you actually itemize deductions. With the standard deduction at $30,000 for married filers in 2026, most expats don't itemize, which means the foreign mortgage interest deduction is theoretical for most people, not practical.

Rental income: If the property generates rental income, the math changes. You can deduct mortgage interest and depreciation against rental income, which significantly improves the numbers. Foreign rental properties and their related accounts are subject to FBAR (FinCEN 114) reporting if your total foreign account balances exceed $10,000 at any point during the year. See the rental property abroad IRS tax guide for the full treatment.

PFIC exposure via bundled bank products: If the bank where you hold your mortgage also sells you investment products — common in European banking relationships — be careful. Purchasing shares in foreign investment funds through a foreign bank creates PFIC (Passive Foreign Investment Company) exposure that comes with punitive US tax treatment. Keep the mortgage relationship clean: mortgage only, no bundled funds or insurance products. More on PFIC in the expat investing playbook.

Alternative Financing Strategies

If the foreign mortgage route doesn't work — wrong country, insufficient local income history, FATCA dead ends — there are US-side options worth knowing.

Home Equity Line of Credit (HELOC) on US property. If you own a US home with equity, a HELOC can be drawn and wired abroad as cash. You're borrowing against US property with US terms (currently ~8–9%) to fund a foreign purchase. Rates are higher than European mortgages, but no FATCA complications, no foreign documentation requirements, and no currency-denominated risk on the loan itself. Works well as a bridge until you establish a local mortgage track record.

Seller financing. More common in emerging markets and resort areas where international buyers are frequent. Terms vary — 3–10 years, 6–12% interest — but can bridge to a local refinance once you've built a local banking history. In Mexico, nail down the legal structure (fideicomiso or SA de CV) before signing anything.

Developer financing in new construction. Many developers in Panama, Mexico, and parts of Southeast Asia offer in-house financing for off-plan purchases: 20–30% down, balance on completion, sometimes installment plans during construction. Not a long-term mortgage substitute, but lowers the immediate cash requirement substantially on pre-construction deals.

For a broader view of how property abroad fits into an expat wealth-building strategy — including the cost arbitrage angle on housing across 10 countries — see the geographic arbitrage playbook and the expat estate planning guide.

The Bottom Line

The 56% of expat buyers who pay all cash aren't doing it because that's the optimal financial move — they're doing it because they gave up on financing before they started. Portugal offers 70% LTV at under 3%. Spain at 60% with 30-year terms. Mexico at 65% for non-residents with no local income requirement. These aren't niche products. They're mainstream bank offerings that most US buyers never investigate.

The friction is real: FATCA paperwork, translated documents, local account requirements, currency risk. But for a purchase that might cost you $150,000 instead of $700,000 for an equivalent US property, the friction is worth working through. Get a FATCA-compliant local bank account open early, document your income consistently over 24 months, and target banks with international mortgage divisions. The financing is out there.

For questions about transferring funds internationally as part of this process, see the expat money transfer guide. For ongoing banking setup while living abroad, the US expat banking and taxes guide covers what to keep, what to open, and what to close.

Financial Disclaimer: This post is for informational purposes only and does not constitute financial, tax, or legal advice. Mortgage rates, LTV limits, and lending criteria change frequently and vary by lender and applicant profile. Consult a qualified mortgage professional and a US-licensed CPA or tax attorney familiar with expat tax law before making any property financing decisions. Currency risk is real and can materially affect your total cost of borrowing in a foreign currency.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageMay 2, 2026

Geographic ArbitrageMay 2, 2026

Foreign Mortgages for Expats: How Americans Buy Property Abroad

Which countries let Americans get mortgages? Current rates, LTV caps, IRS reporting rules, and the 5 costly mistakes foreign property buyers make.

Geographic ArbitrageJune 26, 2026

Geographic ArbitrageJune 26, 2026

Colombia Type V Visa: The Remote Worker's Guide

Colombia's Type V digital nomad visa requires ~$1,400/month foreign income, $315 in fees, and 2–6 weeks processing. Step-by-step application guide for

Expat Tax & FinanceJune 23, 2026

Expat Tax & FinanceJune 23, 2026

FBAR vs Form 8938: Expat Reporting Guide

US expats with foreign accounts over $10,000 must file FBAR. Learn how Form 8938 differs, current penalty amounts, and how to catch up.