Buy Rental Property Abroad Without Getting Wrecked by the IRS

Here's a number that should make any US investor uncomfortable: the average gross rental yield in American cities hovers around 6.56% — and after...

Here's a number that should make any US investor uncomfortable: the average gross rental yield in American cities hovers around 6.56% — and after...

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

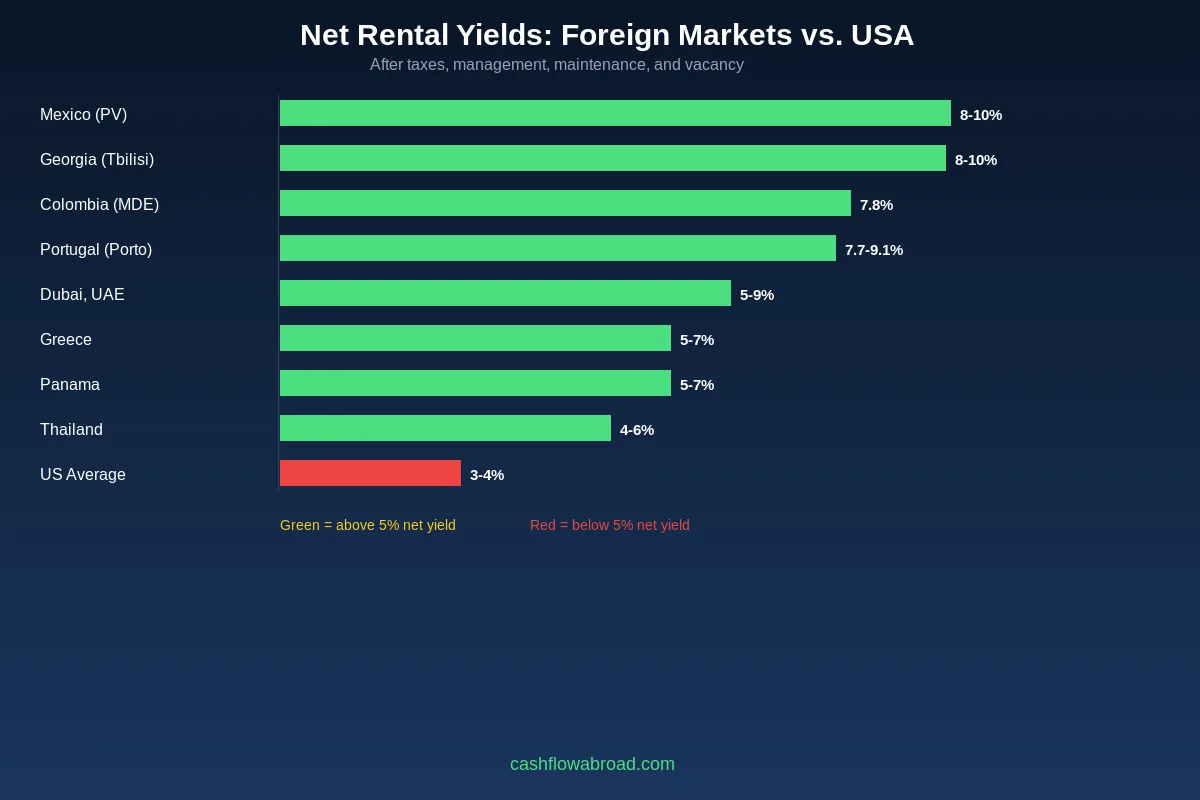

Here's a number that should make any US investor uncomfortable: the average gross rental yield in American cities hovers around 6.56% — and after property taxes, management fees, insurance, vacancy, and maintenance, your net yield collapses to somewhere between 3% and 4%. Meanwhile, a two-bedroom apartment in Medellín, Colombia is currently generating 7.78% average gross yields, with some Airbnb-optimized units clearing 13–16%. A solid one-bedroom in Tbilisi, Georgia (the country, not the state) — priced at around $1,330 per square meter — is yielding 8–10% net after all costs. And Dubai? Zero percent tax on rental income or capital gains, with gross yields of 5–9% in prime neighborhoods.

The counterintuitive truth: the US is one of the worst places to own rental real estate on a pure yield basis, yet most American investors never look beyond their own zip code. As an expat, you're already living the geographic arbitrage lifestyle — why not apply that same thinking to where you park your investment capital?

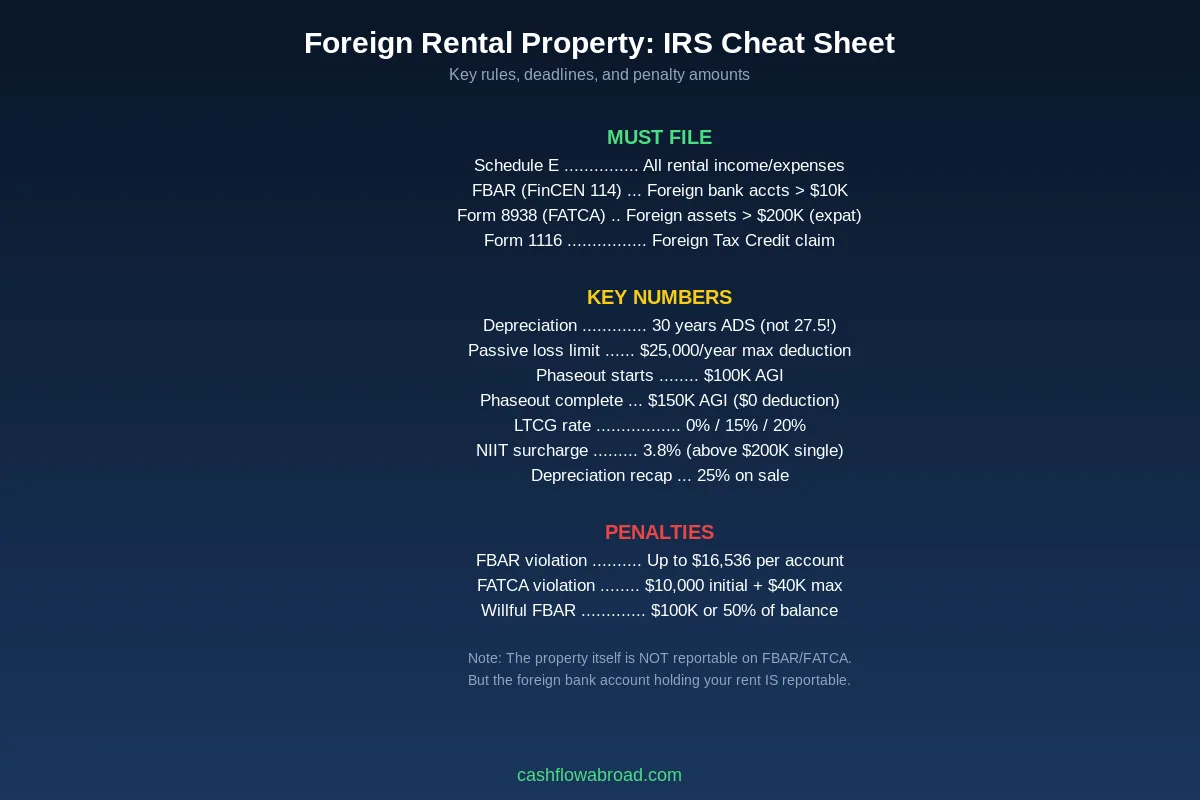

But here's the catch nobody warns you about: the IRS doesn't stop caring about your income just because you bought a bungalow in Batumi. Foreign rental property comes with its own labyrinth of tax rules — Schedule E reporting, 30-year depreciation under ADS, passive activity loss traps, FBAR nuances, and a capital gains structure that can blindside even experienced investors. Get these wrong and you're facing penalties starting at $16,536 per violation.

Related: FEIE zero tax guide

This guide gives you the complete playbook: which countries offer the best risk-adjusted returns, exactly how the IRS taxes your foreign rental income, what you actually have to report (and what you don't), and how to structure everything so you're building real wealth — not a compliance nightmare.

Why Foreign Real Estate Beats US Yields

The math is straightforward once you actually run it. In the United States, high property prices compress gross yields while operating costs remain stubbornly high. A $500,000 rental property in Phoenix might gross $36,000/year (7.2%), but after property management (8–10%), property taxes (~1.5%), insurance (~0.5%), maintenance (~1%), and vacancy (~5%), you're netting $21,000–$23,000 — a 4.2–4.6% net yield. And that's before your mortgage, if you have one.

In emerging expat markets, the equation flips. Lower purchase prices, lower operating cost ratios, and in some cases actively growing tourism infrastructure all drive higher net yields. Add tax-efficient structures and the picture gets even better.

| Country / City | Avg Gross Yield | Avg Entry Price | Local Capital Gains Tax | Foreign Ownership |

|---|---|---|---|---|

| US Average | 6.56% | $350K–$550K | 0–20% + 3.8% NIIT | Unrestricted |

| Medellín, Colombia | 7.78% (13–16% STR) | $120K–$250K | 15% (held 2+ yrs) | Freehold, most areas |

| Tbilisi, Georgia | 7.42% (8.6% avg) | $100K–$180K | 5% capital gains | Freehold (no agri land) |

| Porto, Portugal | 7.72–9.13% | $280K–$450K | 50% of gain taxed at income rates | Freehold |

| Puerto Vallarta, Mexico | 8–10% net | $150K–$350K | 25–30% on gain | Fideicomiso (coast) |

| Dubai, UAE | 5–9% | $200K–$600K+ | 0% | 100% freehold zones |

| Phuket, Thailand | 8–15% (STR) | $100K–$300K | Progressive, ~5–20% | Condos only (49% quota) |

| Athens / Greek Islands | 4–10% (islands higher) | $180K–$500K | 15% | Freehold |

| Panama | ~6% | $150K–$400K | 10% or 3% of sale price | Same rights as citizens |

That table tells a story fast: lower-cost emerging markets consistently deliver superior gross yields, and when you pair them with smart tax planning, the after-tax returns are genuinely impressive. The US average of 6.56% gross compresses to 3–4% net. Several of these foreign markets clear 6–8% net — nearly double.

How the IRS Taxes Foreign Rental Income: Schedule E Explained

Here's what surprises most expat investors: the IRS taxes foreign rental income almost identically to US domestic rental income. You report it on Schedule E (Supplemental Income and Loss, Form 1040), and most of the same deductions apply. There's no special foreign penalty or surcharge just for owning a property abroad.

The key mechanics:

- Currency conversion: All income and expenses must be reported in US dollars. The IRS accepts the annual average exchange rate published by the US Treasury for converting regular monthly transactions. A $1,500 rent payment in Colombian pesos or Georgian lari gets converted at the annual average rate — not the rate on the day you received it. This simplifies bookkeeping considerably.

- Filing deadlines: Standard April 15 deadline, or the automatic June 15 extension for Americans living abroad. Need more time? Form 4868 extends to October 15.

- The FEIE does not apply to rental income: The Foreign Earned Income Exclusion (up to $130,000 in 2025) covers only earned income — wages and self-employment income. Rental income is passive, not earned. It cannot be excluded under FEIE under any circumstances. If you were banking on your foreign rental income being sheltered by FEIE, recalibrate now.

What You Can Deduct on Schedule E

Schedule E allows a wide range of deductions against your foreign rental income:

- Property management fees and leasing commissions

- Repairs and maintenance (not capital improvements — those must be depreciated over time)

- Mortgage interest, if you financed the purchase

- Foreign property taxes — deductible on Schedule E as a rental expense. Important caveat: the Tax Cuts and Jobs Act of 2017 eliminated foreign property tax as an itemized deduction on Schedule A through at least 2025. Your only route is via Schedule E as a rental expense.

- Insurance premiums

- Utilities you pay as landlord

- Legal and accounting fees

- Advertising and tenant-finding costs

- Currency conversion fees

- Depreciation (see the critical details in the next section)

The Foreign Tax Credit: Your Best Friend on Form 1116

If the country where your rental property sits also taxes your rental income, you're potentially paying tax twice on the same money. That's where Form 1116 (Foreign Tax Credit) comes in. The FTC gives you a dollar-for-dollar credit against your US tax bill, up to the US tax owed on that income category (the "passive basket").

In practice: expat landlords in higher-tax countries like Portugal (25–28% rental tax rate) or France often owe little to no additional US tax after applying the FTC. Low-tax jurisdictions like Georgia (20% flat income tax) or Panama may still leave some US tax liability, but the overall combined burden is typically manageable given the yield advantage.

One critical mistake: do not take a Schedule A deduction for foreign taxes if you're also taking a foreign tax credit on Form 1116. You must choose one method for a given year. For most rental property owners, Form 1116 generates more tax savings.

For a complete picture of how these tax mechanisms interact with your overall expat tax strategy, see our complete US expat banking and taxes guide.

The 30-Year Depreciation Trap

This is where foreign real estate diverges from US real estate in a meaningful and expensive way. For US residential rental property, the IRS allows you to depreciate the building over 27.5 years under the General Depreciation System (GDS). For foreign residential rental property, you must use 30 years under the Alternative Depreciation System (ADS), straight-line method.

Foreign commercial property gets even less favorable treatment: 40 years under ADS.

What does this mean in dollars? Take a $300,000 foreign apartment (building value only; land is not depreciable):

- US property equivalent: $300,000 ÷ 27.5 years = $10,909/year depreciation deduction

- Foreign property: $300,000 ÷ 30 years = $10,000/year depreciation deduction

- Annual difference: $909/year in reduced deductions

- Over 30 years: $27,270 in deductions you never access

It's not catastrophic, but it's real money. More importantly: no bonus depreciation, no accelerated depreciation, and no cost segregation studies can change this for foreign property. The ADS 30-year straight-line is mandatory.

Also critical: when you eventually sell, your accumulated depreciation is subject to "depreciation recapture" under IRC Section 1250, taxed at a maximum rate of 25% — regardless of how low your long-term capital gains rate would otherwise be. Factor this into your hold-and-sell math from day one.

The $25,000 Passive Loss Rule That Kills High Earners

This is the most dangerous trap in expat real estate investing, and it catches a huge percentage of higher-income investors. Here's how it works.

Related: expat investing playbook

The IRS classifies rental income as passive activity. If your rental property generates a net loss in a given year — which happens frequently early on, especially with depreciation — you'd normally want to deduct that loss against your ordinary income (salary, consulting fees, business income) to reduce your overall tax bill.

The IRS has a special exception that lets you do exactly this: the $25,000 special allowance. If you own at least 10% of the property and "actively participate" (meaning you approve tenants, set rental rates, and approve repairs — you don't need to be a real estate professional), you can deduct up to $25,000 in rental losses against your ordinary income.

But here's the killer clause: this allowance phases out at higher incomes:

- The $25,000 allowance reduces by $1 for every $2 your Modified Adjusted Gross Income (MAGI) exceeds $100,000

- At $150,000 MAGI: the allowance is completely eliminated

If you're earning $200,000 in freelance income or running a profitable online business — a perfectly normal profile for a geographic arbitrage practitioner — you get zero current-year deduction from your rental losses. The losses don't disappear; they "suspend" and carry forward indefinitely. They release when you generate passive income or when you sell the property. But if you were counting on those deductions to reduce your quarterly estimated tax payments, you'll be unpleasantly surprised.

The workaround for high earners: focus on properties that generate positive cash flow rather than paper losses. That way the passive loss limitation becomes irrelevant — you're making money rather than trying to shelter other income. This is actually easier with foreign real estate, where higher yields mean profitable cash flow from day one in most of the markets on this list.

Our guide to paying zero federal income tax as a US expat covers the intersection of FEIE, passive income, and overall expat tax strategy in full.

FBAR and FATCA: What Foreign Property Owners Actually Report

This is where panic-inducing misinformation is rampant. Let's be precise about what you actually have to file.

Direct Real Estate Ownership: Usually Not Reported on FBAR or FATCA

FBAR (FinCEN Form 114) requires reporting of foreign financial accounts — bank accounts, brokerage accounts, pensions. Direct ownership of foreign real estate does not trigger FBAR. The property itself is not a financial account.

FATCA (Form 8938) requires reporting of "specified foreign financial assets." Real estate held directly — in your own name — is explicitly excluded from Form 8938 by regulation.

In many straightforward cases: you buy an apartment in Tbilisi in your own name, rent it out, and report the income on Schedule E. No FBAR, no Form 8938 for the property itself.

When Real Estate DOES Trigger Reporting

- Foreign bank accounts: If you open a local bank account to receive rent or manage property expenses — which is essentially universal — and that account's balance, combined with any other foreign accounts, exceeds $10,000 at any point during the year, you must file FBAR. This catches virtually every expat property investor who holds rental deposits in a local account.

- Purchase funds: If you wired money through a foreign bank account to complete the purchase, that account may have briefly exceeded $10,000 — triggering FBAR for that year, even if it was just a pass-through transaction.

- Entity ownership: If you hold the property through a foreign corporation, LLC equivalent, partnership, or trust, that entity becomes a reportable "specified foreign financial asset" under FATCA. More on this in the entity trap section below.

FATCA Form 8938 thresholds for Americans living abroad: $200,000 at year-end OR $300,000 at any point during the year (single); $400,000/$600,000 for married filing jointly. These thresholds are higher than for US-based filers.

The Penalty Structure (2025) Is Not Theoretical

- FBAR non-willful violation: Up to $16,536 per violation (inflation-adjusted to January 2025)

- FBAR willful violation: Greater of $165,353 or 50% of the account balance — per year

- FATCA (Form 8938) failure to file: Starting at $10,000; up to $50,000 for continued non-filing after IRS notice

The DOJ has pursued expat real estate investors who failed to report foreign accounts even when the underlying income was otherwise properly declared. The cost of getting FBAR wrong isn't the income tax — it's the disproportionate account balance penalties. Filing FBAR costs you nothing. Missing it can cost six figures.

Capital Gains on Foreign Property Sales

When you sell your foreign rental property, the gain is taxed under US capital gains rules — with a few important wrinkles beyond the standard rates.

Long-Term Capital Gains Rates (2025, Filed 2026)

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | Up to $48,350 | $48,351–$533,400 | Over $533,400 |

| Married Filing Jointly | Up to $96,700 | $96,701–$600,050 | Over $600,050 |

Three additional factors hit expat property sellers hard:

- Net Investment Income Tax (NIIT): An additional 3.8% applies to capital gains when your MAGI exceeds $200,000 (single) or $250,000 (MFJ). So your effective maximum rate isn't 20% — it's 23.8%. And depreciation recapture on top of that at 25%.

- Currency fluctuation gains: If the local currency appreciated against the dollar during your ownership, that gain is also taxable under IRC Section 988. A property that stayed flat in local currency terms can still generate a US capital gain if the exchange rate moved in your favor. Conversely, currency depreciation can generate a tax loss — which is actually a planning opportunity in markets with volatile currencies.

- No cross-border 1031 exchanges: Under Section 1031(h)(1), US real property and foreign real property are explicitly not like-kind. You cannot defer gain by swapping a foreign property for a US one. However, a foreign-to-foreign exchange is permitted — swapping your Tbilisi apartment for a Porto condo, for example, can defer the gain. File Form 8824 for any like-kind exchange.

The Section 121 Exclusion — The Expat's Capital Gains Escape Hatch

Almost nobody uses this: the Section 121 primary residence exclusion applies to foreign property. If you lived in the foreign property as your primary residence for at least 24 of the last 60 months, you can exclude up to $250,000 of gain (single) or $500,000 (married filing jointly) from US capital gains tax when you sell.

The practical strategy: many expats live in their property for two years while testing the local market and enjoying the lifestyle, then convert it to a pure rental, then sell before the 60-month window expires. Execute this correctly and a significant chunk of appreciation escapes US capital gains tax entirely — on top of whatever the local country's exemptions allow. Run this scenario with your CPA before deciding whether to rent from day one or live there first.

The full landscape of expat investment vehicles and their tax treatment is covered in our expat investing playbook.

Related: money transfer guide

8 Countries Ranked: Net Yield, Tax Rates, and Ownership Rules

1. Medellín, Colombia — Best All-Around for US Expats

Medellín has become the sleeper hit of expat real estate investing. Entry prices in El Poblado and Laureles run $1,500–$2,500/sqm USD, meaning a solid two-bedroom can be acquired for $120,000–$200,000. That's not a typo — and for context, a comparable apartment in Miami would run $600,000+.

Gross long-term rental yields average 7.78%. Short-term Airbnb-optimized units in premium buildings are generating $3,000–$4,000/month revenue, hitting 13–16% yields on purchase price — numbers that are genuinely difficult to replicate anywhere in the United States. Price appreciation ran at 10.3% in 2025 city-wide, with 5-year projections holding at 4–6% annually.

Tax structure: Colombia imposes a 15% flat capital gains tax on properties held 2+ years. Hold under 2 years and it's taxed as ordinary income at up to 39% — so hold longer. For US investors, apply the FTC to offset the US tax. Transaction costs run 3–5% of purchase price. Annual property tax: 0.3–1% of assessed value. Foreign buyers must register their investment with Colombia's Central Bank (Banco de la República) — a process that takes a few weeks but is routine.

One key risk: the Colombian peso has historically been volatile. Many investors in expat neighborhoods price rentals in USD to sidestep currency conversion issues. Worth considering when you model net returns.

If you're combining property ownership with residency, the ColombiaMove guide to moving to Colombia as an American covers the visa landscape in full. And the Medellín cost of living breakdown gives you the full budget picture for life there as an owner-occupier or investor.

2. Tbilisi, Georgia — Lowest Entry Price, Surprising Yields

Georgia (the country, at the crossroads of Europe and Asia) has become a genuine darling of the expat investor world. Average new apartment prices in Tbilisi sit at $1,330/sqm, with resale apartments at $1,099–$1,150/sqm. A solid one-bedroom in a central Tbilisi neighborhood: $60,000–$100,000.

Average gross rental yields hit 7.42%. In Batumi on the Black Sea coast, short-term rentals in beachfront buildings generate 10–18% net annually, with dedicated short-stay developments reportedly hitting 15–20%. Foreigners made up 20%+ of all 2024 real estate transactions in the country — a strong signal of international investor confidence.

Local tax advantages are significant: Georgia taxes rental income at a flat 20%, but capital gains are taxed at only 5%. Combined with the FTC, the total US+Georgian tax burden for most investors is remarkably manageable. Foreigners can own Georgian real estate on a freehold basis with virtually no restrictions (agricultural land is the main exception).

The Georgian economy has been growing at 6–8% annually, underpinning property appreciation. Currency risk (the Georgian lari) is lower than Colombia's peso historically but still a factor for USD-reporting investors.

3. Porto, Portugal — EU Stability with Strong Yields

Porto has become the preferred entry point for European expat property investors, offering yields that Lisbon can no longer match. Porto city center yields average 7.72%; metro areas hit 9.13%. Prices run €2,581–€4,055/sqm depending on location — substantially cheaper than Lisbon (€3,987–€5,538/sqm).

The major 2025 caveat: Portugal's original NHR tax regime ended in March 2025, replaced by NHR 2.0 (officially IFICI). The new regime is restricted to qualifying researchers and innovation sector professionals — passive investors and retirees no longer qualify for the flat 10% preferential tax rate. Rental income is now taxed at 25% (residential) or 28% (commercial) for most foreign investors. Portugal's Golden Visa program also no longer allows residential real estate in major urban centers as qualifying investment.

Despite the NHR closure, Porto remains attractive: strong long-term rental demand from students and digital nomads, EU legal and property rights security, and projected annual price growth of 7.8%. Just price your after-tax returns using the 25% rental tax rate, not the old NHR structure.

4. Puerto Vallarta / Riviera Nayarit, Mexico — Tourism-Driven Cash Flow

Mexico's Pacific corridor generates some of the most consistent short-term rental income in the expat investor universe. Puerto Vallarta and Riviera Nayarit are producing net yields of 8–10% on well-positioned properties. Gross yields in peak season hit 15% in tourist-optimized condos.

The ownership complication: foreigners cannot directly own land within 50km of a coastline or 100km of a national border. Property in these zones must be held through a fideicomiso — a bank trust in which a Mexican bank holds legal title on your behalf. Setup cost: $2,000–$3,000. Annual maintenance: $550–$1,000. It's bureaucratic but legally secure — hundreds of thousands of Americans own Mexican property this way.

One firm warning: avoid Tulum condos for investment purposes. The market is severely oversupplied as of 2025, and regular condos barely break even after management fees and platform costs. Puerto Vallarta, Cabo, and Riviera Nayarit are far more reliable.

Capital gains in Mexico: sellers can choose between 25–30% on actual gain or a flat 3.5% on total sale price — whichever is more favorable. Get local tax advice before closing a sale.

5. Dubai, UAE — Tax-Free Yields with Global Liquidity

Dubai's unique value proposition is simple: 0% tax on rental income, 0% capital gains tax, 0% income tax. The UAE has no personal income tax and no capital gains tax at the emirate or federal level. Gross yields in prime areas (Downtown, Palm Jumeirah, Dubai Marina) run 5–9%. Short-term vacation rentals: 8–10%.

Related: cheapest countries guide

Property values have risen approximately 15% since 2021, with projections of another 10% growth by end of 2026. Foreign ownership is unrestricted in designated freehold zones, which cover most developments marketed to international buyers. Dubai's 10-year Golden Visa is available for properties purchased at AED 750,000 (~$205,000).

The catch for US investors: even with UAE's 0% tax, you still owe US tax on your rental income and capital gains. Without a foreign tax credit (since you paid nothing to the UAE), the US tax is calculated directly on your Schedule E income. However, with full depreciation deductions, management expenses, and the fact that you're starting from higher gross yields, most US investors still net more after-tax than on a comparable US property.

6. Athens / Greek Islands — Yield Plus Scarcity Premium

Athens central neighborhoods offer yields of 4–6% — lower than others on this list, but backed by EU legal security and strong appreciation. The real investment play is in the islands: Crete and Rhodes are generating 10% yields annually driven by peak tourism demand. Annual price appreciation in Crete and Rhodes runs around 10%; Halkidiki and Skiathos: 6–8%.

Property transfer tax was recently reduced to 3%. Greece's Golden Visa requires €250,000 (renovation projects) or €400,000 (new construction in major metros) — over 11,000 foreign investors secured Greek residency in 2024, contributing €2.5 billion to the market. Capital gains: 15% tax rate, with potential reductions for long-hold properties.

The island play is fundamentally a tourism arbitrage: buy in a location with 3–4 months of extremely high occupancy and price-insensitive demand, then manage through a local operator year-round. The best Aegean island properties are becoming increasingly scarce as foreign demand grows.

7. Phuket / Koh Samui, Thailand — Highest Gross Yields, Most Restrictions

Thailand's gross rental yields are genuinely impressive: short-term rentals in Phuket routinely hit 8–15%. But ownership is structurally constrained. Foreigners cannot own land in Thailand — period. Your options are:

- Condominium freehold — permitted, but foreigners can only hold up to 49% of units in any building. You must verify the foreign quota hasn't been filled before purchasing.

- 30-year leasehold with a 30-year renewable option — legally structured but not equivalent to freehold.

In 2025, Thailand restructured its property tax system: there's now an annual property tax of 0.3–1% of cadastral value, plus an additional 2–5% tax on properties above 10 million baht (~$250,000). These changes compress net yields modestly relative to pre-2025 projections.

Thailand's Digital Nomad Visa (DTV) launched in 2024. If you're considering Thailand as a base, combining a condo purchase with the DTV is worth modeling. Just verify the 49% foreign quota status in any building before you commit capital.

8. Panama — USD Economy, Stable Framework, Conservative Yields

Panama operates entirely in US dollars — eliminating currency risk entirely — and grants foreigners identical property ownership rights to Panamanian citizens. Gross yields average around 6% annually. Lower than the other markets here, but paired with the stability of a USD economy, transparent legal framework, and proximity to the US, it's the right choice for conservative investors.

Capital gains: choose between 10% of profit or 3% of total sale value — whichever produces the lower tax. Annual property tax: graduated, with the first $120,000 of assessed value exempt. Non-resident mortgages run 5–7% with 50–70% down required.

Panama's position as a logistics and financial hub means stable long-term rental demand from business travelers and professionals — less seasonal volatility than tourism-focused markets like Thailand or Greece's islands.

The Entity Ownership Trap

Many expat investors are advised — often by local lawyers who don't understand US tax implications — to hold foreign real estate through a foreign entity: a local corporation, LLC equivalent, or trust. This might make sense for local liability or estate planning reasons, but it introduces significant US tax compliance complexity:

- Foreign corporation: Requires Form 5471 — one of the most complex international information returns the IRS produces. A qualified CPA will charge $1,500–$3,000+ just to file this correctly. Every year.

- Foreign partnership: Requires Form 8865. Similar complexity and annual cost.

- Foreign trust: Requires Forms 3520 and 3520-A. If you accidentally create a foreign trust through a local ownership structure (which some inadvertently do), you're in expensive compliance territory. Automatic penalty for missing Form 3520: 35% of the trust's gross value.

- FATCA exposure: A foreign entity holding real estate becomes a "specified foreign financial asset" for Form 8938 purposes — even though direct real estate isn't reportable. The entity is what's reportable.

For most expat investors purchasing a single property for rental income, direct ownership in your own name is simpler, cheaper to maintain, and fully legal. If liability is a concern, a US LLC holding foreign property may be cleaner from a compliance perspective — though you'll need local counsel to confirm the entity is recognized in the target country.

The compliance cost of an entity done wrong far exceeds any benefit from asset protection. Our expat estate planning guide covers international ownership structures in depth.

How to Get Started: The Expat Property Investor's Checklist

If you've read this far, you're serious. Here's the practical sequence for getting into foreign real estate without blowing up your finances or your tax situation:

- Choose your market first, not your property. Decide which country aligns with your yield targets, risk tolerance, and life plans. Do you want to visit regularly? Do you need EU residency? Are you prioritizing maximum yield or currency stability? These criteria narrow the field faster than browsing real estate portals.

- Get a US-qualified expat tax professional on board before you buy. Not after. Not at tax time. Before you wire any money. The entity question, the FBAR question, the passive loss calculation — you need to understand the US tax picture before you commit capital. Greenback Tax Services, Taxes for Expats, and 1040 Abroad all specialize in this area.

- Set up your US banking infrastructure. Mercury is the go-to US banking layer for expat business and investment income — excellent international wire capabilities, no surprise account closures for having a foreign address, and strong customer service. You want a clean US account that receives rental income conversions and handles reporting cleanly. Pair Mercury with Traveling Mailbox (from $15/month) so tax documents and property-related mail reach you anywhere via scanned delivery.

- Hire local legal counsel in the target country. Every market has its quirks: Colombia's Banco de la República registration requirement, Mexico's fideicomiso, Thailand's 49% condo quota. Budget $1,500–$5,000 for legal setup depending on the country and complexity.

- Understand the remittance and transfer mechanics. Getting money from a Colombian or Georgian bank account to your US account efficiently is a real operational question. Remitly handles smaller monthly rental distributions well; for larger property-scale wire transfers, use a dedicated international transfer service with competitive mid-market exchange rates.

- Build a realistic net-yield financial model. Gross yield is vanity; net yield is sanity. Model: gross rent minus property management (8–15%), minus property tax, minus insurance, minus maintenance reserve (budget 1% of property value annually), minus vacancy (budget 5–10%), minus the incremental CPA cost to handle Schedule E. Then calculate your after-tax net. Compare against alternatives.

- Plan your FBAR compliance from day one. Assume you'll open a foreign bank account. Assume it will exceed $10,000. Set a recurring calendar reminder every January to file FBAR before April 15. The penalty for forgetting is genuinely disproportionate to the oversight.

- Model the Section 121 strategy before you decide on day-one rental. If you're planning to live in the country anyway, spending two years in the property before converting to rental can shelter significant appreciation from US capital gains. Run the numbers with your CPA before assuming you should rent immediately.

For the full picture on managing passive income streams as an expat — including the interaction between rental income, FEIE, and your overall tax optimization — our guide to passive income streams that work from any country covers the complete framework.

Bottom Line

Foreign real estate investing is one of the most powerful tools in the expat wealth-building toolkit — not because the IRS treats it specially, but because the underlying economics are genuinely superior in many markets. When you can buy a $150,000 apartment in Medellín that generates $14,000/year in net rent (a 9.3% net yield), while a comparable-yield US property would cost $350,000+, the math speaks for itself.

The complexity is real but manageable. Schedule E reporting is familiar to any US CPA who handles expat returns. The 30-year ADS depreciation limit costs you less than $1,000/year in deductions relative to a US property. The passive loss phaseout is a non-issue if you're investing in cash-flow-positive properties — which most of these markets deliver. And FBAR, once you understand what it actually covers, is mostly a matter of remembering to file it every April.

The investors who get hurt aren't the ones who bought foreign property. They're the ones who bought it without understanding the rules, held it through an unnecessarily complex entity structure, or forgot to file FBAR on the local account where they deposited their rent.

Get the compliance right, choose your market based on net yield and lifestyle fit, and foreign real estate can be exactly the kind of compounding wealth engine that looks obvious in hindsight: a $200,000 apartment generating 8% yields, appreciating at 6% annually, in a market where your dollar buys three times the lifestyle it would at home. That's geographic arbitrage applied to your net worth — not just your monthly budget.

Financial Disclaimer: This article is for informational and educational purposes only and does not constitute tax, legal, or financial advice. International tax law is complex and changes frequently. The information presented reflects rules as understood at time of writing and may not reflect current law. US expats with foreign rental property should consult a qualified US international tax professional (CPA or tax attorney with international experience) before making any investment or tax filing decisions. Rental yields and property prices cited are historical averages from third-party industry sources; past performance does not guarantee future results. Currency exchange rates, local regulations, and market conditions can materially affect actual investment returns.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

Canadian TFSA and US Taxes: The Reporting Trap

US citizens holding a Canadian TFSA owe tax on all annual growth and must file Form 3520 — PFIC rules apply to Canadian mutual funds inside the

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

State Income Tax for Expats: Which States Follow You

California, New York, and Virginia keep taxing Americans abroad. Learn which states follow you, what triggers audits, and how to exit cleanly.

Expat Tax & FinanceJuly 3, 2026

Expat Tax & FinanceJuly 3, 2026

FBAR: The $10,000 Expat Rule Most People Get Wrong

FBAR: when any foreign account aggregate hits $10,000 during the year, all accounts must be reported. Penalties, Bittner ruling, and catch-up