The US government quietly sent out $17 billion in checks to 3.1 million Americans in early 2025 — and most expats who qualified had no idea the money was coming. If you ever worked abroad, paid into a foreign pension system, or married someone who did, there's a real chance the Social Security Administration owes you thousands in back payments right now.

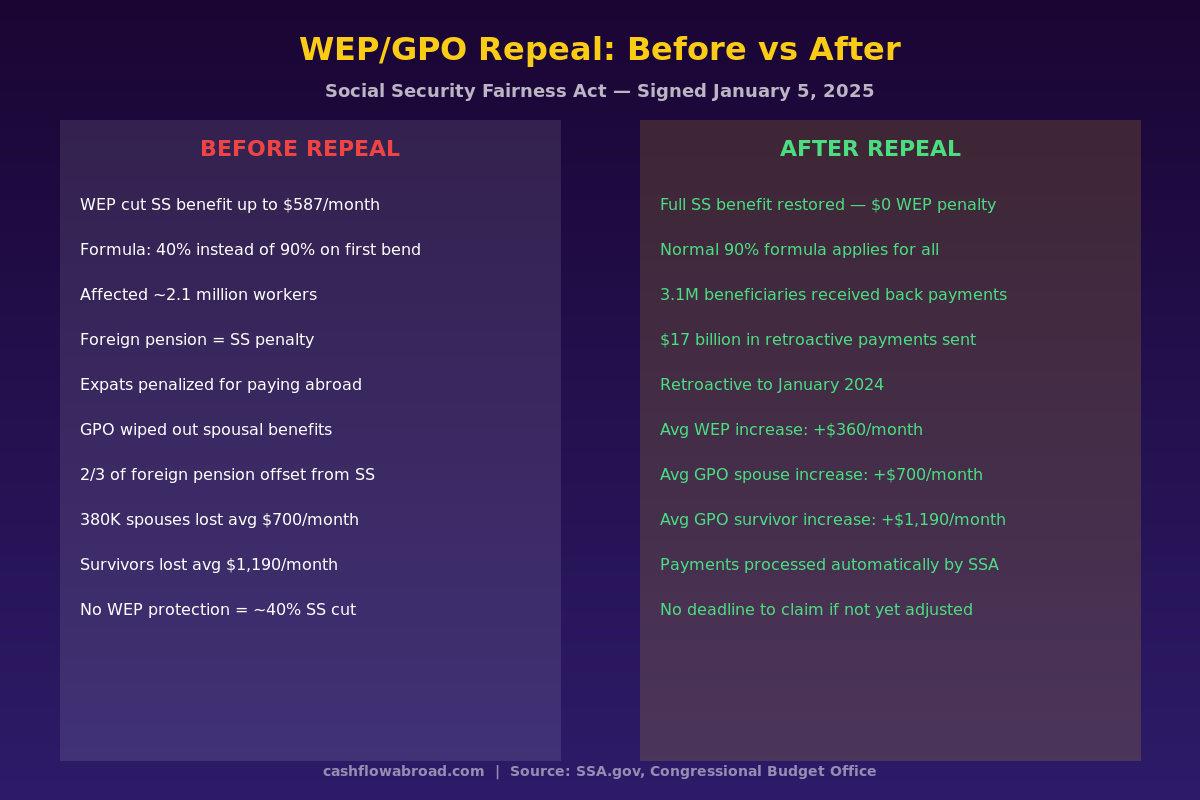

For 40 years, two provisions buried inside the Social Security rulebook systematically slashed benefits for workers who split their careers between US-covered employment and non-covered work — including foreign pension systems. On January 5, 2025, both provisions were permanently eliminated. Here's what that means for your retirement math and what you need to do before you leave any of that money unclaimed.

What WEP Was — And Why Expats Got Hammered

The Windfall Elimination Provision (WEP) was introduced in 1983 to fix what Congress saw as an unintended perk: workers who split careers between SS-covered and non-SS-covered employment (like a foreign company's payroll) were being classified by the Social Security formula as "low earners," triggering a generous replacement rate designed for people who spent entire careers in low-wage domestic jobs.

The fix turned into a punishment. The standard Social Security benefit formula applies a 90% replacement rate to the first "bend point" of your average monthly earnings (the 2024 bend point was $1,174/month). Under WEP, that 90% could be slashed to as low as 40% — a difference worth up to $587/month in 2024. Over a 20-year retirement, that's over $140,000 in lost benefits.

The severity depended on your "years of coverage" — how many years you had substantial earnings under US Social Security:

| Years of US SS Coverage | First Bend Point Rate (Before Repeal) | Monthly Reduction (Approx.) |

|---|---|---|

| 30+ years | 90% (no WEP) | $0 |

| 25–29 years | 65%–85% | $59–$293/month |

| 21–24 years | 45%–60% | $352–$528/month |

| 20 or fewer years | 40% (maximum WEP) | Up to $587/month |

A US expat who spent 15 years working in Germany, Australia, or the UK — then returned to work 20 years in the US — would land in the maximum WEP bracket. Their Social Security benefit wouldn't reflect 35 years of work history; it would look like they were a short-term domestic worker, penalized accordingly.

Roughly 2.1 million workers were hit by WEP before the repeal. Many expats planning for retirement discovered their expected Social Security check was hundreds of dollars lighter — sometimes when it was too late to recalibrate their savings strategy.

Which Foreign Pensions Triggered WEP

Not every foreign pension triggered WEP — but the exceptions were narrower than most advisors understood. The default assumption should always have been: your foreign pension is reducing your Social Security benefit.

The US has totalization agreements with 30+ countries including the UK, Canada, Australia, Germany, France, Japan, and most of Western Europe. These agreements eliminate dual Social Security taxation and let workers combine credits across both systems. Many people assumed a totalization agreement meant WEP exemption. It often didn't.

Under SSA rules, a totalization-based foreign pension could be WEP-exempt only if the foreign country used your US Social Security earnings to qualify you for their pension. If you qualified for the foreign pension purely through your own work in that country — regardless of whether a totalization agreement existed — that pension still triggered WEP.

For countries without totalization agreements — India, China, the UAE, Saudi Arabia, Singapore, Thailand, Indonesia, the Philippines, Hong Kong, most of Latin America (excluding Chile and Brazil), and most of Africa — WEP applied without question. US expats working for local employers in these countries and contributing to local pension schemes got zero protection.

All of that is moot now. WEP is gone. Every worker, regardless of foreign pension source or totalization agreement status, is now calculated on the full 90% first bend point formula.

GPO: The Spousal Benefit Killer

The Government Pension Offset (GPO) was a separate, harsher provision targeting spouses and surviving spouses who received pensions from government work not covered by Social Security. The formula: Social Security reduced spousal or survivor benefits by two-thirds of the non-covered government pension.

Example: A widow receives a $3,000/month government pension. GPO reduction: 2/3 × $3,000 = $2,000. If her SS survivor benefit was $2,000, her benefit dropped to $0. Completely eliminated.

GPO affected roughly 770,000 people total: about 380,000 spouses (average benefit increase of +$700/month after repeal) and 390,000 surviving spouses (average increase of +$1,190/month).

Critical nuance for expats: GPO applied only to US governmental pensions — federal, state, or local. A foreign pension generally did not trigger GPO for spousal benefits. This distinction mattered enormously for expats married to US government employees or public-sector workers under CSRS (Civil Service Retirement System). If your spouse or late spouse worked for the federal government and you're receiving a survivor benefit — or not receiving one because GPO eliminated it — the repeal is your biggest financial news in decades.

The Social Security Fairness Act: What Changed

The Social Security Fairness Act (H.R. 82, Public Law 118-273) had been introduced in every Congress for over a decade. It finally passed with bipartisan support and was signed into law on January 5, 2025. Both WEP and GPO were permanently and fully repealed, effective retroactively to January 2024 — December 2023 was the last month either provision applied.

SSA's implementation was remarkably fast. By July 7, 2025 — five months ahead of schedule — the agency had processed 3.1 million payments totaling $17 billion in retroactive benefit increases. By March 4, 2025 alone, 1.1 million people had received over $7.5 billion.

For the average affected retiree, the impact is:

- +$360/month permanently added to monthly Social Security checks (WEP-affected workers)

- A retroactive lump sum covering January 2024 through the processing date

- Recalculated spousal and survivor benefits for GPO-affected families

For expat retirees in Southeast Asia, Latin America, or Eastern Europe — where $360/month represents a significant share of monthly living costs — this is a material change in financial security. The purchasing power of Social Security stretches considerably further abroad, and now there's simply more of it to work with.

How to Claim Your Retroactive Payment

For most affected beneficiaries, SSA processed retroactive payments automatically — no action required. The agency deposited funds directly to the bank account on file. But not everyone was reached.

Already receiving SS benefits but no adjustment received

Call SSA directly at 1-800-772-1213 (Monday–Friday, 8am–7pm local time) or visit your local Social Security office. Ask specifically about your WEP/GPO adjustment under the Social Security Fairness Act. International callers can reach SSA through the Federal Benefits Unit at the nearest US Embassy or consulate — every major expat destination has one.

Not yet claiming Social Security

If you delayed filing because WEP would have made your benefit too small, run the numbers again. Your projected benefit is now higher. Use SSA's online estimator at SSA.gov or call for your current estimated benefit amount. For expats who strategically deferred based on WEP-penalized projections, the break-even calculation has shifted meaningfully.

Previously withdrew an application or never applied due to WEP

This is the highest-stakes group. If you filed for Social Security and voluntarily withdrew the application because WEP made the benefit untenable — or never filed at all — you need to contact SSA proactively. You may need to file or re-file an application. SSA has not announced a cutoff date, but acting promptly preserves the most retroactive coverage.

Maintaining a current US address on file with SSA matters here. Expats who've been abroad for years sometimes have outdated contact information, which delays or misdirects deposits and tax forms. A virtual US mailbox with a real street address — the service we use and recommend for expats managing IRS and SSA correspondence — ensures deposit notifications and your Form SSA-1099 actually reach you. See our full guide on virtual mailboxes for expats for the setup.

Tax Implications of the Lump-Sum Payment

The retroactive payment is taxable Social Security income. Depending on its size, it could meaningfully affect your 2025 federal tax bill. SSA will issue a Form SSA-1099 for the full amount received in 2025, even though the payments represent benefits owed from 2024.

| Scenario | Approximate Retroactive Lump Sum (13 months) | Ongoing Monthly Increase |

|---|---|---|

| Average WEP-affected worker | ~$4,680 | +$360/month |

| Maximum WEP reduction (2024) | Up to $7,631 | Up to +$587/month |

| Average GPO-affected spouse | ~$9,100 | +$700/month |

| Average GPO-affected survivor | ~$15,470 | +$1,190/month |

There's a tax-reduction option worth knowing: the lump-sum election under IRS rules lets you allocate portions of a retroactive Social Security payment to the prior tax years they were meant to cover, if doing so results in lower total tax. This doesn't require amended returns — it's computed on your current-year Form 1040 using a specific IRS worksheet. Your tax preparer should run this comparison before filing.

For expats using the Foreign Earned Income Exclusion, the analysis gets more nuanced. FEIE excludes foreign earned income, but Social Security benefits remain federally taxable regardless. If the lump sum pushes you into a higher bracket, the lump-sum election calculation becomes especially valuable. For expats on the Foreign Tax Credit path, additional foreign taxes may be available to offset the SS income — but this depends heavily on your country of residence and applicable treaty provisions.

Your Updated Social Security Strategy

WEP repeal doesn't just affect what you receive — it changes when you should claim. The standard claiming trade-offs now apply cleanly again:

- Claiming at 62 permanently reduces your benefit by roughly 25–30% vs. full retirement age (FRA)

- Delaying past FRA earns 8% per year in delayed retirement credits through age 70

- The break-even point for delay is typically around age 80 in longevity math

For expat retirees in lower-cost countries, a smaller benefit claimed earlier often makes more sense than maximizing the eventual amount — especially if you're already covered by local or international healthcare and your baseline expenses are low. At $360–$587/month in additional permanent income, the math for living abroad changes dramatically.

If you're reinvesting SS proceeds rather than spending them immediately, make sure your US brokerage account is expat-proof. Charles Schwab International remains the gold standard — no account closure threats for expats, commission-free trading, and unlimited ATM fee reimbursement worldwide when you need to access funds locally. For a full breakdown of where to hold your US investments as an expat, see the expat investing playbook and the guide to brokerage accounts that won't close on you.

The Bottom Line

The Social Security Fairness Act is the most consequential positive change to expat retirement income in a generation. For 40 years, workers who spent time abroad — paying into foreign pension systems, building split-career histories — were quietly penalized every month. That penalty is gone. The money that was being withheld is now being returned, retroactively and permanently.

Most people received their adjustment automatically. But a meaningful number haven't — people who never filed because WEP made benefits negligible, who withdrew applications, who have outdated SSA contact information, or who simply didn't know any of this happened. Check your SSA.gov account, verify your bank information is current, and if you believe you qualify and haven't seen an adjustment, call 1-800-772-1213. The government has already calculated what you're owed. You just have to make sure you collect it.

This article is for informational purposes only and does not constitute financial, tax, or legal advice. Social Security rules and benefit calculations are complex and vary by individual circumstances. Consult a qualified expat tax advisor or financial planner before making retirement decisions based on WEP/GPO repeal. Benefit amounts cited are based on 2024 SSA data and Congressional Budget Office projections.