The 1% US Remittance Tax: Who Owes It and Who Doesn't

The new 1% US remittance excise tax panicked expats — but bank-funded wire transfers are fully exempt. Here's exactly who owes it and how to owe nothing.

The 1% US remittance excise tax (IRC 4475) hits cash transfers, not bank wires. Learn which transfers are exempt and how expats pay /bin/bash.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

When the One Big Beautiful Bill Act landed on the President's desk, the remittance industry panicked. Headlines declared that the US was now taxing money sent abroad — and expat forums lit up with people asking whether every international wire transfer was suddenly 1% more expensive. The answer surprises most people: if you're sending money the way virtually every financially literate expat already does, your tax bill is exactly $0.

That's the buried truth inside IRC Section 4475, which took effect January 1, 2026. The tax is real. The exemptions are huge. And understanding both could save you real money — or at least spare you a lot of unnecessary panic.

What Is the New US Remittance Transfer Tax?

The One Big Beautiful Bill Act (Public Law 119-21) added a brand-new section to the Internal Revenue Code: Section 4475, imposing a 1% federal excise tax on certain outbound remittance transfers from the United States. It applies to transfers made after December 31, 2025.

Specifically, a "remittance transfer" under this law means an electronic transfer of funds initiated by a sender located in the US to a recipient located in a foreign country, processed through a remittance transfer provider. That sounds broad — and it is. But here's where the carve-outs matter.

The excise tax is collected by the provider at the time of the transfer. The sender bears legal liability, but Western Union, MoneyGram, and similar services must collect it on your behalf and remit it quarterly to the IRS using Form 720. During 2026's first three quarters, the IRS issued penalty relief for providers while the system gets up to speed — but the tax obligation itself is immediate and not going away.

The Exemption That Most Expats Miss Completely

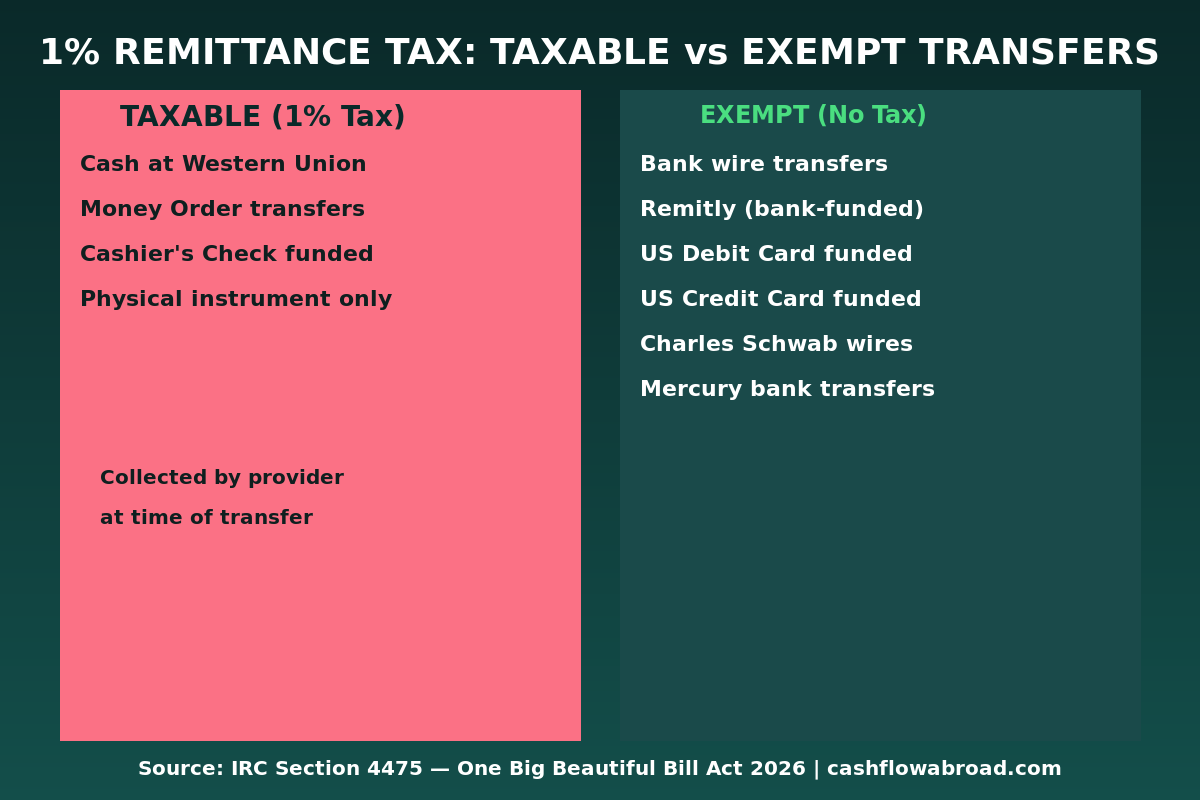

Section 4475 contains a critical limitation that drastically narrows who actually owes the tax. The 1% tax applies only when the sender funds the transfer with cash, a money order, a cashier's check, or another similar physical instrument.

If you fund the transfer from a US bank account, a US-issued debit card, or a US-issued credit card — the tax does not apply. Full stop.

This single carve-out exempts the majority of US expat transfers. Why? Because financially banked expats almost universally send money via wire transfers from checking accounts, or use bank-connected apps like Remitly that pull directly from a US bank account. These are categorically exempt under the law.

The 1% remittance tax was designed to target unbanked cash remittances — primarily sent by undocumented workers who walk into Western Union with dollar bills and send them to Mexico, Central America, or the Philippines. It was not designed for expats with Charles Schwab accounts.

Taxable vs. Exempt: The Complete Breakdown

| Transfer Method | Funding Source | 1% Tax Applies? | Notes |

|---|---|---|---|

| Western Union (cash at counter) | Cash | YES | Tax collected at point of service |

| MoneyGram (cash or money order) | Cash / money order | YES | Same as above |

| Cashier's check funded transfers | Physical instrument | YES | Physical instrument = taxable |

| Bank wire transfer | US checking/savings | NO | Exempt — not a physical instrument |

| Remitly (bank-funded via ACH) | US bank account | NO | Exempt if funded via bank link |

| Charles Schwab international wire | US bank account | NO | Free international wires, exempt |

| Mercury business wire | US business account | NO | Exempt; commercial transfers also excluded |

| US Debit Card funded transfer | Debit card (US-issued) | NO | Explicitly exempt by statute |

| US Credit Card funded transfer | Credit card (US-issued) | NO | Explicitly exempt by statute |

| Business payroll abroad | Any source | NO | Commercial transfers excluded by law |

What 1% Actually Costs — And Who Really Pays It

For the transfers that do get hit, the math is simple but the amounts compound fast for high-volume cash senders:

| Monthly Cash Transfer | Annual Excise Tax | On Top of Existing Fees |

|---|---|---|

| $300/month | $36/year | Plus ~$12–18 in provider fees |

| $500/month | $60/year | Plus ~$20–30 in provider fees |

| $1,000/month | $120/year | Plus ~$35–60 in provider fees |

| $3,000/month | $360/year | Plus ~$80–120 in provider fees |

For a worker sending $500 per month in cash remittances, that's $60 per year in new taxes on top of whatever fees the provider already charges. Across the estimated 50 million outbound cash remittance transactions processed annually in the US, the revenue impact is significant. For any individual, the fix is simple: open a US bank account, fund your transfers from it, and owe $0 in excise tax permanently.

The Best Exempt Transfer Services for US Expats

Since all bank-funded transfers are exempt, the choice comes down to exchange rates, fees, and speed. Here are the tools that matter in the expat financial stack:

Remitly — The Go-To for Regular Transfers

Remitly connects directly to your US bank account via ACH and delivers to 170+ countries. Because the transfer is bank-funded, it's fully exempt from the 1% excise tax. Rates are competitive, speeds range from instant to 3–5 business days depending on the corridor and speed tier, and the mobile app makes recurring transfers frictionless. This is the practical default for most expats moving money regularly. For full fee analysis, see the expat money transfer guide.

Charles Schwab International — Free Wires, Free ATMs

Charles Schwab's international checking account lets you send outbound international wire transfers — bank-funded, fully exempt — at competitive exchange rates. Schwab also reimburses all ATM fees worldwide with no cap, which makes it the most powerful single financial account for expats who need cash access abroad without accumulating fees. Wire transfers from Schwab are free for the first two per month and nominal beyond that.

Mercury — For US Business Operations Abroad

If you operate a US LLC or S-corp from abroad, Mercury gives you full domestic and international wire capability from a US business account. Commercial transfers get a double exemption under IRC 4475 — bank-funded AND outside the definition of taxable remittances. For context on structuring this correctly, see how to run a US business while living abroad.

Don't Lose Your Bank Access: Keep a US Address

None of the above matters if your bank freezes your US account because you updated your address to a foreign country. The IRS requires a US address, and most US banks will restrict accounts associated with an overseas address — or flag your login from a foreign IP. Traveling Mailbox provides a real US street address (not a PO Box) in 50+ cities starting at $15/month — specifically designed to work with US banking and financial accounts. It's the infrastructure that keeps everything else functional while you live abroad.

The Broader 2026 Expat Tax Picture

The remittance tax dominated the headlines, but it's just one piece of several 2026 changes US expats need to actually track:

FEIE Increased to $132,900

The Foreign Earned Income Exclusion jumped to $132,900 for tax year 2026 (up from $130,000 in 2025). A married couple where both spouses qualify can exclude up to $265,800 combined. Add the housing exclusion ($39,870 limit for 2026) and the standard deduction, and a single expat can potentially eliminate federal income tax on roughly $149,000 in foreign earned income. The OBBBA preserved FEIE entirely — despite earlier proposals to eliminate it. Full breakdown at zero federal income tax for expats using the FEIE, and a comparison of strategies at FEIE vs. Foreign Tax Credit.

Foreign Gift Reporting Threshold Cut to $50,000

This one catches people off guard. The OBBBA reduced the reporting threshold for foreign gifts and inheritances received by US persons from $100,000 to $50,000. If you receive more than $50,000 from a foreign person in a single tax year, you must report it on Form 3520. The penalty for missing it: 5% of the gift amount per month, up to 25% — assessed automatically, regardless of whether any tax was owed. If your family abroad has been discussing inheritance or large transfers, this change deserves immediate attention.

FBAR: Unchanged, Still Dangerous

Despite lobbying to consolidate or reform foreign account reporting, the OBBBA left FBAR and Form 8938 completely intact. You must still file FinCEN Form 114 if your aggregate foreign account balances exceeded $10,000 at any point during the year — and aggregate is the critical word. Two accounts holding $6,000 and $5,000 trigger the filing requirement even though neither account individually crosses $10,000.

Non-willful violations carry civil penalties up to $16,536 per violation (inflation-adjusted for 2026). The 2023 Supreme Court ruling in Bittner v. United States clarified that non-willful penalties are assessed per annual report — not per account — which was a significant win for expats with multiple accounts. But the threshold for "willful" remains dangerously subjective, and IRS enforcement is only increasing. Full context in the US expat banking and taxes guide.

The automated international data-sharing under CARF and CRS means undisclosed foreign accounts are far less safe than they were five years ago. Read about the end of expat financial invisibility for what that actually means operationally.

Your 2026 Action Checklist

Concrete steps based on where you actually stand:

If you're already sending transfers via US bank account: Nothing changes. Your transfers are exempt from IRC 4475. Confirm your provider pulls from your bank account (not cash) and move on.

If you've been using cash-funded services: Open a US bank account (Charles Schwab or Mercury are the best fits for expats). Link it to Remitly or your preferred service. Your transfers immediately become exempt and will likely be cheaper overall due to better exchange rates than cash services offer.

If you don't have a US address: Get one before your bank freezes your account. Traveling Mailbox at $15/month is cheaper than losing access to your exempt transfer infrastructure — or losing access to your brokerage during a volatile market.

If you received a large foreign gift or inheritance in 2026: Check whether it exceeds $50,000. If so, Form 3520 is required with your 2026 return. The penalty is automatic and the IRS does not commonly grant first-time abatement for this one.

If you're not filing FBAR: The Streamlined Filing Compliance Procedures are still available for non-willful cases — but only if you come forward before the IRS initiates contact. Once they reach out, the program closes for you. The cost of compliance is far lower than the cost of being found non-compliant.

The Bottom Line

The 1% US remittance excise tax is real law with real consequences — for the roughly 50 million cash-funded outbound transfers processed annually in the US. For the overwhelming majority of US expats who wire money from bank accounts or use bank-linked transfer apps, the tax is a complete non-event. Zero exposure. $0 owed.

The irony is that the expats most likely to panic about this law are precisely the expats least likely to be affected by it. Meanwhile, the foreign gift threshold reduction to $50,000 and unchanged FBAR penalties are far more likely to catch financially literate expats off guard — because those traps hit people who actually have assets and receive money, not people sending $300 in cash to a relative abroad.

Know what you owe. Transfer from a bank account. Keep your US address active. And don't let tax hysteria push you into restructuring something that was never broken.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. IRC Section 4475 and related regulations are new and subject to IRS guidance updates throughout 2026. Tax rules vary based on individual circumstances, residency status, and transfer methods. Consult a qualified international tax professional before making decisions based on this content. The author may receive compensation from affiliate partners linked in this article.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 23, 2026

Expat Tax & FinanceMay 23, 2026

The Big Beautiful Bill: What US Expats Won and Lost

FEIE rose to $132,900 but citizenship-based taxation survived the OBBB unchanged. Full expat scorecard + why the RBT compliance clock is ticking.

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

FBAR vs FATCA: What Every Expat Must Know

FBAR and FATCA are two separate foreign account reporting requirements with different penalties and thresholds. Learn what every US expat must file.

Expat Tax & FinanceMay 30, 2026

Expat Tax & FinanceMay 30, 2026

The 3 Bank Accounts Every US Expat Actually Needs

Stop paying $2,400/year in bank fees abroad. This 3-account expat banking setup—Schwab, Mercury, Traveling Mailbox—costs just $180/year.