Your US Life Insurance May Be Void If You Live Abroad

Not lapsed. Not reduced. Void . A death in Bangkok or Medellín triggers a clause most policyholders never read, and the insurer walks away paying nothing.

Not lapsed. Not reduced. Void . A death in Bangkok or Medellín triggers a clause most policyholders never read, and the insurer walks away paying nothing.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

An estimated 9.3 million Americans live outside the United States — and most of them have no idea that the life insurance policy sitting in their filing cabinet back home may already be worthless. Not lapsed. Not reduced. Void. A death in Bangkok or Medellín triggers a clause most policyholders never read, and the insurer walks away paying nothing.

This isn't a fringe risk. It's the standard behavior of US domestic life insurance contracts, and the expat community largely ignores it until a widow in Lisbon spends six months fighting a claims denial. Here's what the fine print actually says — and what to do about it before it matters.

The Residency Clause Nobody Reads

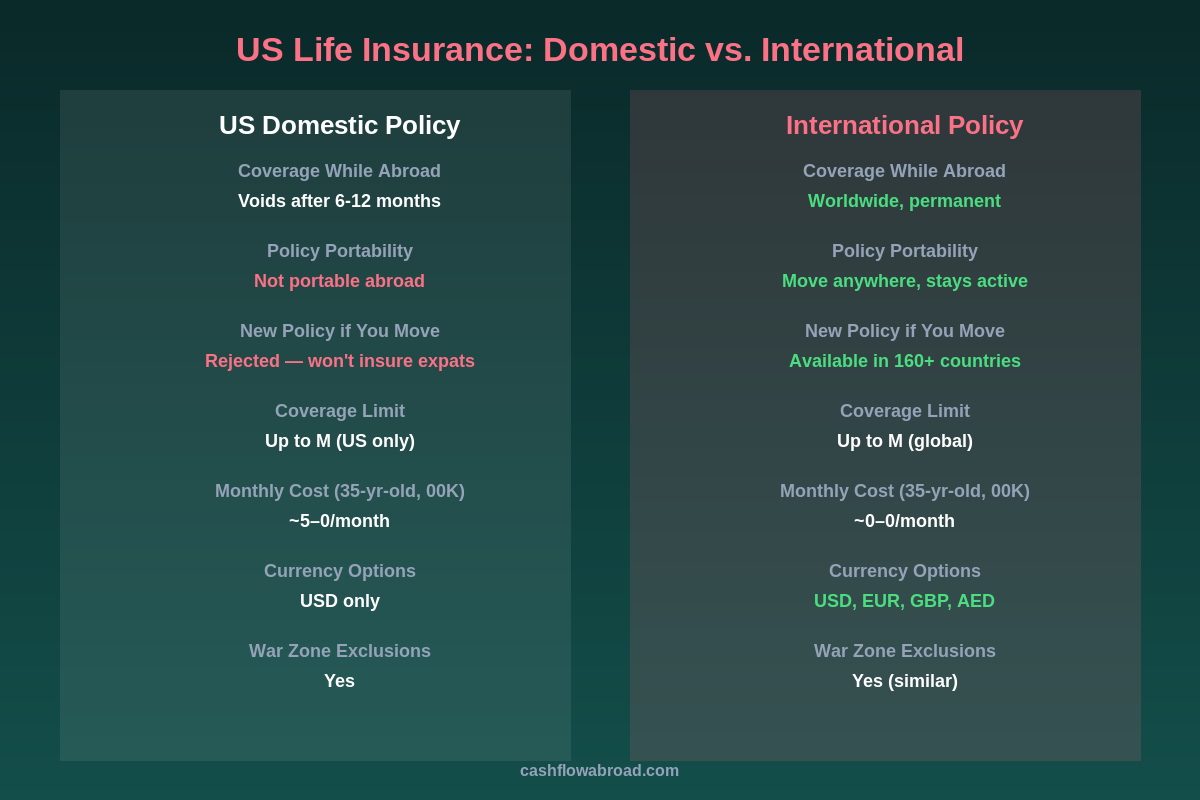

Standard US term and whole life policies are underwritten based on a specific risk profile: where you live, your access to healthcare, local mortality rates, and the legal system governing any claims. When you signed the application, you listed a US address. That address was the foundation of the risk calculation.

Most policies include what's called a residency or travel exclusion clause. The language varies by insurer, but the core mechanism is the same: if you relocate to a country outside an approved list — or if the insurer classifies your destination as "high-risk" — coverage can be restricted, suspended, or terminated. Failing to notify your insurer of an international move, even if unintentional, gives them clean grounds to deny a death claim after the fact.

The legal argument insurers make is straightforward: by moving abroad, you fundamentally changed the risk they agreed to cover. Courts have generally sided with insurers on this point. The policy premium you've dutifully paid every month is not, by itself, proof of continued coverage.

What Actually Voids Your Coverage

There's no single universal rule — it depends on your insurer and your specific contract. But these are the most common triggers:

- Living outside the US for more than 6 months in a calendar year. Many policies define "residency" using the same 183-day threshold as US tax law. Cross it, and you're technically no longer a US resident under the policy's terms — regardless of your citizenship.

- Moving to a restricted country. Active conflict zones (Ukraine, Sudan, Yemen), countries under US sanctions (North Korea, Iran, Cuba), and nations flagged for elevated mortality risk are explicitly excluded in most policies. Some insurers extend restrictions to countries with high violent crime statistics.

- Not disclosing your move. Almost every life insurance application asks about intended travel or relocation plans. Failing to update the insurer after moving can be treated as material misrepresentation — voiding the policy retroactively from the date of the unreported change.

- Death from excluded circumstances. Even if the insurer honors your residency abroad, many policies exclude deaths resulting from "war or acts of terrorism" — a clause that becomes immediately relevant if you're living in certain regions of the world.

The 6-Month Trigger Most Expats Hit Without Realizing It

Here's where most expats get caught. They leave the US thinking of their move as "temporary" — a one-year contract job in Singapore, a digital nomad stretch in Lisbon, a retirement trial run in Oaxaca. They keep paying premiums. They never call their insurer. Six months pass.

At month seven, if something happens, the insurer can argue that residency effectively shifted. The policyholder changed the underlying risk. The ongoing premium payments don't create liability for the insurer — they create opportunity for a denial, because the insurer's ignorance of the move was the policyholder's failure to disclose, not the insurer's obligation to verify.

The problem compounds when someone tries to buy a new domestic policy from abroad. If you live more than six months per year outside the US, the majority of American insurers won't issue a new policy at all. You're not just losing coverage — you're locked out of the domestic market entirely, often precisely when you've realized you need to act.

Your Three Realistic Options

Once you understand the gap, there are three practical paths forward — not four, not nine, three. Each has a specific use case.

Option 1: Formally Notify Your Insurer and Keep the Policy

Some carriers — particularly Prudential, AIG, and Transamerica — will continue coverage if you formally notify them of an international move and your destination country isn't on their restricted list. Coverage continues, but you're accepting annual uncertainty about claim eligibility, and if the policy lapses for any reason, you cannot replace it from abroad.

A handful of US insurers offer an expatriate rider — an optional endorsement that explicitly extends coverage to international residents. This costs extra but provides documented, enforceable protection. Ask your broker specifically about this before assuming your policy transfers intact.

Option 2: Get a Dedicated International Life Insurance Policy

This is the cleanest solution. International life insurance is designed specifically for globally mobile individuals. Coverage follows you regardless of country, is portable across relocations, and is underwritten with international mortality data rather than US-specific actuarial tables.

Key differences from domestic policies:

- Renewable annually up to age 70 (William Russell), or available as 10- and 20-year term equivalents from other carriers

- Multi-currency payout options: USD, EUR, GBP, or AED — protects beneficiaries from exchange rate risk at the worst possible moment

- Coverage valid in 160+ countries with no ongoing residency requirements

- Lump-sum death benefit with optional terminal illness acceleration benefit

- Repatriation benefits sometimes bundled (returning remains from abroad runs $5,000–$15,000 depending on distance)

Option 3: Layer Both for Higher Coverage

If your US policy is stable and your insurer has confirmed continued coverage in writing, keeping it while adding an international policy for supplemental protection makes sense — particularly for higher earners whose dependents need US-level death benefits plus liquidity that doesn't require navigating a foreign insurance claim.

Top International Life Insurance Providers for US Expats

| Provider | Max Coverage | Countries Covered | Currency Options | Best For |

|---|---|---|---|---|

| William Russell | $2,000,000 | 160+ | USD, GBP, EUR, AED | Globally mobile; renewable to age 70 |

| AIG International | $5,000,000 | 80+ | USD, EUR | High-net-worth expats needing large coverage |

| Cigna Global | $2,000,000 | 200+ | USD, EUR, GBP | Bundling health and life in one carrier |

| Guardian Life | $3,000,000 | Selected markets | USD | US citizens in lower-risk expat destinations |

| Prudential (expat) | $2,000,000 | Limited list | USD | Existing US policyholders formally disclosing a move |

| Expat Financial | $1,500,000 | 150+ | USD, GBP, EUR | Budget-conscious expats, straightforward coverage |

What Does It Actually Cost?

International term life costs more than domestic — the premium difference is real. But it's not as dramatic as most expats assume, especially for younger applicants. Here's a rough comparison across age and coverage levels:

| Age / Coverage | US Domestic (term) | International Policy | Monthly Difference |

|---|---|---|---|

| 35 / $500,000 | ~$25–$40/month | ~$45–$70/month | ~$20–$30 more |

| 40 / $500,000 | ~$40–$60/month | ~$65–$100/month | ~$25–$40 more |

| 50 / $500,000 | ~$100–$150/month | ~$140–$220/month | ~$40–$70 more |

| 35 / $1,000,000 | ~$40–$65/month | ~$75–$130/month | ~$35–$65 more |

For most expats under 45, the international premium is an extra $30–$50 per month. In countries where geographic arbitrage cuts your cost of living by $1,000–$2,000/month, that's an obvious trade-off. The question isn't whether you can afford international coverage — it's whether you can afford to skip it.

Can You Keep Your Existing US Policy?

Possibly — but only with deliberate action. Here's the checklist that actually matters:

- Read the policy's territorial and residency exclusions now. Usually found in the "General Exclusions" or "Territorial Limits" section. Look for language about "residing outside the United States" or specific country restrictions.

- Call your insurer before moving. Ask directly: "If I relocate to [country], will my policy remain in force?" Get the answer in writing, with a reference number. This documentation protects you against a future claim denial based on changed residency.

- Ask about an expatriate rider. If your carrier offers one, add it before departure. Adding it from abroad is usually impossible — insurers require this to be completed while you're still a US resident.

- Set up automatic premium payments from a US account. A lapsed policy is one you cannot reinstate from abroad. Charles Schwab's international checking account maintains a US banking presence while you're overseas, charges no foreign transaction fees, and refunds ATM fees worldwide — exactly what you need to keep US financial obligations on autopilot.

- Maintain a US mailing address. Insurers require a US address for correspondence. A virtual mailbox like Traveling Mailbox gives you a real US street address in 50+ cities, scans incoming mail digitally, and keeps your account paperwork from bouncing. At $15/month it's the cheapest way to preserve the administrative footprint US institutions require.

How Much Coverage Do You Need as an Expat?

The standard US rule of thumb — 10–12× annual income — needs recalibration for the expat context. If your dependents live in a low-cost country, the capital required to replace your income is lower in absolute terms. A family living on $2,500/month in Medellín needs meaningfully less capital than one living on $2,500/month in Boston.

A $500,000 policy invested conservatively at 4% generates $20,000/year — more than sufficient in much of Southeast Asia or Latin America. If your dependents plan to return to the US after your death, the math shifts back toward US cost-of-living numbers. Model both scenarios before settling on a coverage amount.

Also factor in:

- Outstanding US debt: mortgage, student loans, business obligations — anything that doesn't disappear with you

- Repatriation costs: returning remains from abroad typically runs $5,000–$15,000 depending on country and distance

- Currency risk for beneficiaries: if your beneficiaries live in a country with a weak local currency, a USD-denominated death benefit provides stability a local-currency policy wouldn't

Getting Coverage Before You Leave: The Smart Window

If you're still in the US and planning a move, this window matters more than most expats realize. US insurers require the medical exam and policy signing to take place on US soil for most products. Once you're abroad, your options narrow sharply — and the policies you can access internationally cost more.

- If you don't already have a policy, apply before departure to lock in domestic pricing

- Simultaneously request an international provider quote for comparison — William Russell and Cigna Global both offer online estimates

- If your destination is on your insurer's restricted list, don't wait — your existing coverage may void on day one of your move

- Confirm beneficiary designations include international wire transfer instructions or a US account the beneficiary can actually access from abroad

For more on structuring your financial life abroad — banking, tax, and insurance together — the complete US expat banking and tax guide walks through the full stack. On the health side, SafetyWing's Nomad Insurance starts at $56/month for adults under 40 and pairs naturally with an international term life policy — the health plan handles medical costs while the life policy handles the catastrophic financial gap if the worst happens. Our expat health insurance guide compares SafetyWing, Cigna Global, and Allianz side by side if you're still deciding on that piece.

The Bottom Line

The expat life insurance gap isn't hypothetical — it shows up in real claim denials every year, in countries with large American communities, involving policyholders who paid every premium on time. The fix is not complicated: either confirm in writing that your existing policy covers you in your new country, add an expatriate rider before departure, or transition to a dedicated international policy while you still can.

The premium difference for international coverage runs $30–$70/month above comparable domestic policies. Against the geographic arbitrage savings most expats are realizing — often $1,000–$3,000/month in reduced cost of living — that's a rounding error. The financial gap it closes for your family is not.

Don't let a clause nobody reads undo the protection you spent years building.

Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or insurance advice. Life insurance policies vary significantly by issuer, jurisdiction, and individual circumstances. Premium estimates are approximate and based on publicly available data — actual quotes will vary based on age, health, coverage amount, and carrier. Consult a licensed insurance broker with international experience before making coverage decisions. Pricing and availability referenced here are subject to change.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Health & InsuranceJuly 14, 2026

Expat Health & InsuranceJuly 14, 2026

Expat Health Insurance With Pre-Existing Conditions

How international health insurers handle pre-existing conditions, which providers cover what, and how to avoid a coverage gap when moving abroad.

Expat Health & InsuranceJuly 11, 2026

Expat Health & InsuranceJuly 11, 2026

Medical Evacuation Insurance for US Expats Abroad

Most expat health plans don't cover air ambulance transport home. Learn how medevac memberships from Medjet and Global Rescue fill the gap for under

Expat Health & InsuranceJune 27, 2026

Expat Health & InsuranceJune 27, 2026

Dental Care Abroad: Costs, Coverage, and Where to Go

Root canals for $350, implants for $1,100. Compare dental costs in Mexico, Thailand, Hungary and Colombia — plus what your expat insurance covers.