Uruguay Tax Residency: The Hidden Catch Expats Miss

Uruguay is not a territorial tax system — it's a worldwide system with a timed exemption. Here's what the glossy guides miss before you commit.

Uruguay is a worldwide tax system with an 11-year exemption — not permanently territorial. Here's the full breakdown vs Panama and Paraguay.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Here's the pitch you'll hear in expat circles: "Uruguay gives you zero tax on foreign income — it's like Paraguay but with better steak." That framing gets one thing right and one thing dangerously wrong. Paraguay is a permanently territorial system. Uruguay is a worldwide tax system with a timed exemption that expires. After year eleven, the government starts collecting. Most expats who move for the tax deal don't stay long enough to find out.

That distinction — timed versus permanent — changes every calculation. It affects which passport you prioritize, how you structure investment accounts, and whether the $15,000+ deposit requirement is worth it compared to Panama's $4,000 entry fee. None of the glossy relocation guides explain this cleanly, so here's the full picture.

What Actually Makes Uruguay Different

Uruguay sits in a tier of its own among Latin American residency destinations. It consistently ranks as the least corrupt country in Latin America (Transparency International's 2024 index), has a functioning public healthcare system, a stable currency, and a legal tradition that's genuinely independent from the executive branch. These aren't small things. Residency in Paraguay costs less and takes less time, but Paraguay has a weaker institutional track record and a history of rapid policy swings.

The trade-off is cost and commitment. Uruguay requires more of both — and in exchange, you get a country that actually behaves like a developed nation. For high-net-worth individuals who want a second passport pathway with real stability, that premium is often worth paying.

The Tax Holiday: What It Is and What It Isn't

Uruguay's tax regime for new residents is governed by Law N° 20.446, updated effective January 1, 2026. Under the current rules, new tax residents can elect one of two structures for foreign-source capital income:

- Option A — Zero for 11 years: Pay 0% on all foreign-sourced dividends, interest, and capital gains for the year residency is established plus 10 additional years. After that, the standard 12% flat rate applies.

- Option B — Permanent 7% flat: Opt into a permanent 7% rate on foreign income with no expiration date.

Option A sounds better. For most US expats, Option B is actually more rational. Here's why: US citizens owe US taxes on worldwide income regardless of where they live. The Foreign Tax Credit lets you offset US liability with taxes paid abroad — but only if you actually pay foreign taxes. If Uruguay charges you 0%, you get $0 in foreign tax credits, and you owe full US rates on top. At 7%, you're generating some offsetting credit and creating a paper trail of foreign tax compliance. The practical difference in take-home is minimal, but the documentation value is real.

More importantly: Option A has a cliff. If you're still a Uruguayan tax resident in year twelve, you owe 12% on all foreign income. Nomads who plan to move before the holiday expires may not care. Anyone building permanent roots needs to account for that cliff.

The Three Ways to Get Residency

Uruguay offers multiple paths. The right one depends on how much time you plan to spend there and what assets you're working with.

Path 1: Physical Presence (183 Days/Year)

Spend more than 183 days per year in Uruguay and you automatically become a tax resident. This is the standard path for retirees, remote workers, and anyone actually living there. The deposit requirement is roughly $15,000 (placed in a Uruguayan bank account — you keep the money, it's not a fee). Temporary residency can be issued in as little as 10 days; permanent residency takes 4–8 months. During the waiting period, each exit from Uruguay requires a re-entry permit at approximately $40 per trip.

The 183-day rule is the same threshold used by Spain, Portugal, and most European countries. It's meaningful — this is half your year. Nomads who want maximum flexibility should look elsewhere.

Path 2: Passive Income / Retirement Visa

If you have recurring passive income of at least $1,500/month from abroad — pension, investment income, rental income, Social Security — you qualify for residency without meeting the 183-day requirement immediately. The income must be verifiable and lawful. Retirees with Social Security checks, dividend portfolios, or rental income abroad fit this profile cleanly. Check out the broader breakdown of how Social Security goes further abroad if you're running those numbers.

Path 3: Real Estate or High Investment

Under the updated 2026 rules, you can qualify for tax residency by owning Uruguayan real estate valued above $2,000,000 USD — or through qualifying venture capital investments. An older real estate threshold (approximately $378,000 with 60 days/year presence) still applies for standard temporary residency but no longer triggers the updated Tax Holiday 2.0 benefits on its own. If you're buying property expecting a decade of zero tax, verify which law applies to your entry date with a local attorney.

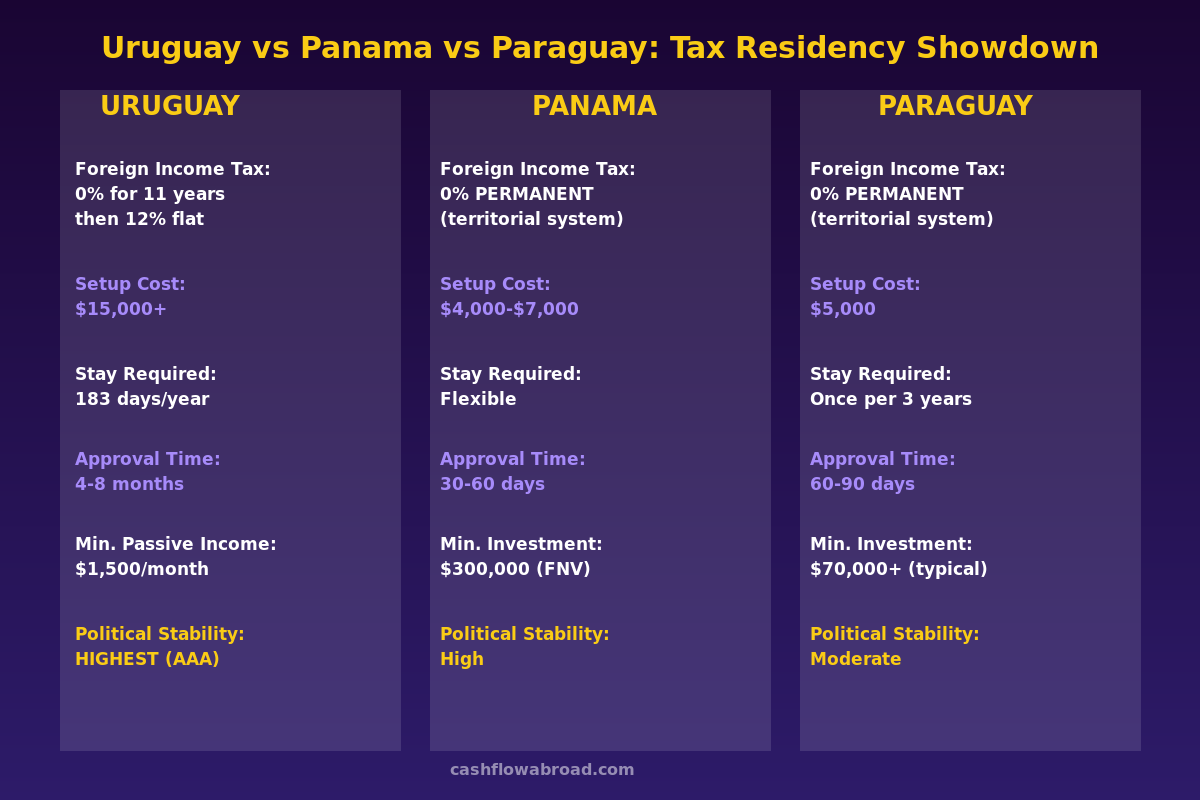

Uruguay vs. Panama vs. Paraguay: The Numbers

| Factor | Uruguay | Panama | Paraguay |

|---|---|---|---|

| Foreign income tax | 0% for 11 years, then 12% | 0% permanently | 0% permanently |

| Tax system type | Worldwide (with timed exemption) | Territorial | Territorial |

| Setup cost | $15,000+ deposit | $4,000–$7,000 | $5,000 |

| Approval timeline | 4–8 months | 30–60 days | 60–90 days |

| Physical presence requirement | 183 days/year | Flexible | Once every 3 years |

| Minimum passive income | $1,500/month | $1,000/month (Pensionado) | None |

| US tax treaty | No | No | No |

| Dollarized economy | No (Uruguayan peso) | Yes (USD) | No (Guaraní) |

| TI Corruption Index 2024 | #21 globally, #1 in LATAM | #83 globally | #105 globally |

The table makes one thing obvious: if pure tax efficiency and maximum travel flexibility are your goals, Paraguay wins on every metric. You get permanent 0% on foreign income, the lowest setup cost, approval in 60–90 days, and you only have to show up once every three years. For a nomad with no intention of actually living in South America, Paraguay is the clean answer.

Uruguay wins when you actually want to live there. It has a lower crime rate than Panama, better infrastructure than Paraguay, a strong social safety net, and one of the few Latin American countries where rule of law functions predictably. If you're putting down roots — buying property, starting a business, raising a family — Uruguay's institutional quality is a genuine differentiator. More on the full geographic arbitrage playbook if you're comparing across more countries.

The US Expat Tax Situation

Uruguay has no tax treaty with the United States. That means no reduced withholding rates, no tiebreaker residency rules, and no treaty shopping. What you do have:

- Totalization Agreement: Uruguay and the US have a Social Security totalization agreement, which prevents double taxation of Social Security contributions if you're self-employed or employed by a US company while living in Uruguay.

- FEIE still applies: The Foreign Earned Income Exclusion ($126,500 for 2024) can offset earned income. Since you're in Uruguay 183+ days to maintain tax residency, passing the physical presence test is straightforward.

- Foreign Tax Credits: Available, but limited. If you elected Option A (0% Uruguayan tax), you have no Uruguayan taxes to credit against your US bill. Option B's 7% generates some credits — helpful for investment income that doesn't qualify for FEIE.

- FBAR and FATCA: If you hold a Uruguayan bank account with the $15,000 deposit requirement, you almost certainly need to file an FBAR annually. Accounts over $10,000 at any point in the year are reportable. For a deeper dive, see the US expat banking and taxes guide.

Bottom line for US expats: Uruguay doesn't eliminate your US tax burden. It gives you a stable second base, a legal tax residence, and — if structured correctly — a lower effective blended rate on investment income through the 7% election. Anyone telling you Uruguay means "pay zero total taxes as a US citizen" is either confused or selling something.

The Real Cost of Living in Uruguay

Uruguay is the most expensive country in South America. Montevideo — where most expats land — runs comparable to a mid-tier European city.

| Expense | Monthly Cost (USD, Montevideo) |

|---|---|

| 1BR apartment (city center) | $700–$1,100 |

| 1BR apartment (outside center) | $500–$750 |

| Utilities (electricity, water, internet) | $120–$200 |

| Groceries (single person) | $300–$450 |

| Dining out (mid-range, estimated monthly) | $250–$400 |

| Public health insurance (FONASA) | $100–$200 (income-based) |

| Private health insurance | $150–$350 |

| Total comfortable single lifestyle | $1,800–$2,800 |

For context: comparable comfort in Asunción, Paraguay runs $800–$1,400/month. In Medellín, Colombia, $1,000–$1,800. Uruguay's premium is real. The passive income visa requirement of $1,500/month is the floor, not the target. A comfortable single expat life costs closer to $2,200–$2,500/month.

On the upside: Uruguay's peso has held up better than its neighbors', property rights are rock solid, and the country doesn't carry the safety concerns or expat-targeting scams that make some cheaper destinations exhausting to navigate daily.

Banking and Financial Setup

Opening a Uruguayan bank account is a requirement for the $15,000 deposit and a practical necessity. The major banks — BROU (state-owned), Santander, BBVA, and Scotiabank — all operate there. Expect documentation requirements: passport, residency application, proof of income or funds. Opening can take 2–4 weeks after your initial residency paperwork is filed.

Keep your US banking stack active. Charles Schwab International remains the gold standard for expats — free ATM withdrawals worldwide, no foreign transaction fees, and full brokerage access. Uruguay ATMs often charge local fees of $2–$5 per withdrawal, which Schwab reimburses monthly.

For international transfers from the US to your Uruguayan account, Remitly regularly offers competitive USD-to-UYU rates with first-transfer promotions. The exchange rates typically beat bank wire rates by 1.5–3%.

If you're concerned about maintaining a US address for banking, IRS correspondence, and state domicile purposes while abroad, a Traveling Mailbox virtual US address ($15/month) keeps your US financial infrastructure intact. The IRS requires a valid US address on file; losing that can complicate FBAR filings and bank account retention. See the full virtual mailbox guide for expats for the setup details.

Health Insurance

Uruguay has a public health system (FONASA/ASSE) that new residents can access after paying into it. Monthly contributions are income-based, typically $100–$200/month for most expats. Quality is adequate for routine care; wait times for specialists can be long.

Most expats supplement with a private mutualista (cooperative medical provider) or international health coverage. SafetyWing offers international nomad plans starting around $45–$100/month that pair well with Uruguay's public system as a backstop. More details in the expat health insurance guide.

Who Should Actually Choose Uruguay

Uruguay makes sense for a specific profile. It does not make sense for everyone chasing low taxes:

Good fit: Retirees or semi-retired expats with $2,500+/month passive income who want a stable, developed country in South America. Couples or families who want quality schools, walkable cities, and low violent crime. High-net-worth individuals ($2M+) who want a legally clean second residency with institutional credibility for banking and estate planning.

Poor fit: Nomads who don't plan to spend 183 days/year in one place. Anyone optimizing purely on cost — Paraguay, Colombia, and Thailand all cost significantly less. US expats expecting to zero out their total global tax bill — the lack of a US treaty makes that math not work. Anyone on a tight setup budget — the $15,000 deposit plus legal fees ($1,000–$2,500) plus relocation costs add up fast.

If you want permanent zero tax on foreign income with the lowest entry cost and maximum flexibility, the Paraguay residency guide is the better starting point. For a broader comparison across the full spectrum of low-tax residency options, the territorial tax countries guide covers more ground.

Getting Started: Practical Steps

- Hire a Uruguayan attorney. Legal fees run $1,000–$2,500 for a qualified immigration attorney in Montevideo. Budget for it from day one.

- Open a Uruguayan bank account. You need this before depositing residency funds. Start the process as soon as you arrive in country.

- Determine your path: 183-day physical presence, passive income visa, or investment route. Your income level and lifestyle determine which applies.

- File US informational returns from day one. FBAR, Form 8938 (FATCA), and potentially Form 8833 if you rely on the Totalization Agreement. Consult a US expat tax advisor — this is not optional.

- Decide on Option A vs. Option B before your first tax year as a Uruguayan resident. You cannot switch retroactively, so get qualified advice before the deadline.

The Bottom Line

Uruguay is not the easy offshore tax hack it's sometimes marketed as. The tax holiday is real, the stability is real, and the quality of life is genuinely high — but so are the costs, the time commitment, and the complexity of navigating a worldwide tax system with no US treaty protection. For US expats, the honest math is this: Uruguay won't eliminate your US tax bill, and it costs more to live there than almost anywhere else in Latin America.

What Uruguay does offer is something harder to quantify: a place you'd actually want to live, built on institutions that work, in a region where that's rarer than the tax guides suggest. If that fits your goals and budget, the residency is worth pursuing seriously. If it doesn't, Paraguay and Panama offer cleaner, cheaper paths to the same headline benefit.

Financial disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently, and individual circumstances vary widely. Consult a licensed US expat tax advisor and a qualified Uruguayan attorney before making any residency or tax decisions. Nothing in this article constitutes a recommendation to relocate or restructure your finances for tax purposes.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJune 6, 2026

Geographic ArbitrageJune 6, 2026

Vienna Expat Guide: RWR Card, Taxes, and Living Costs

Vienna ranks #1 in livability. Complete guide to Austria's Red-White-Red Card, the 30% expat tax deduction, income brackets, and real monthly living

Expat Tax & FinanceMay 26, 2026

Expat Tax & FinanceMay 26, 2026

Portugal IFICI: Is the NHR Replacement Worth It?

NHR ended in 2025. Portugal's IFICI replacement gives tech workers and researchers a 20% flat tax for 10 years — but retirees and passive investors.

Geographic ArbitrageMay 3, 2026

Geographic ArbitrageMay 3, 2026

Andorra Tax Residency: Europe's Hidden 10% Tax Haven

Andorra offers 10% max income tax, zero inheritance tax, and 4.5% VAT. Full 2026 guide to residency options, costs, and the US expat catch.