UK for US Expats: Taxes, the New FIG Regime & Real Costs

The UK abolished its non-dom regime in 2025. Here is what the new FIG regime means for American expats, plus real costs, visa options, and why most Americans owe $0 to the IRS from London.

The UK abolished its non-dom regime in 2025. Learn the new FIG 4-year exemption, UK tax rates, visa options, and why most Americans owe $0 to the IRS.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

The average American moving to the UK expects a tax nightmare. Two governments, two filing deadlines, complex treaty rules — and a country famous for some of the highest marginal rates in the developed world. What most don't realize: the math almost always works out to $0 owed to the IRS. And in April 2025, the UK quietly introduced one of the most expat-friendly foreign income regimes it has had in 225 years. Here's what changed, what it costs to actually live there, and the one salary trap that catches even well-advised expats completely off guard.

The FIG Regime: UK's New 4-Year Foreign Income Exemption

On April 6, 2025, the UK abolished its centuries-old non-domicile regime — a system that had allowed wealthy foreign nationals to live in Britain while shielding offshore income from UK tax indefinitely. In its place: the Foreign Income and Gains (FIG) regime, a cleaner, time-limited structure that's actually better news for the typical American expat arriving fresh.

Under FIG, anyone who has been non-UK resident for at least the previous 10 consecutive tax years gets a 4-year window of full exemption on foreign income and gains — even if that income is remitted to the UK. Citizenship and domicile are irrelevant. A US citizen who last lived in the UK before 2015 and returns today qualifies automatically. So does a tech worker moving to London for the first time.

The practical effect for a new American arrival: your US rental income, US dividends, US capital gains, and any foreign consulting revenue are completely invisible to HMRC for four full tax years. Only UK-sourced income — your British salary, UK freelance income — gets taxed locally. That's a meaningful window to build wealth before full worldwide taxation kicks in.

After year four, the exemption expires and you're taxed on worldwide income as a standard UK resident. For most Americans, the Foreign Tax Credit still eliminates any US liability on top of that. But the FIG regime changes the calculus for people considering a medium-term UK stint: four years of low-tax income deferral, inside one of the world's most liveable cities, is a genuinely attractive deal.

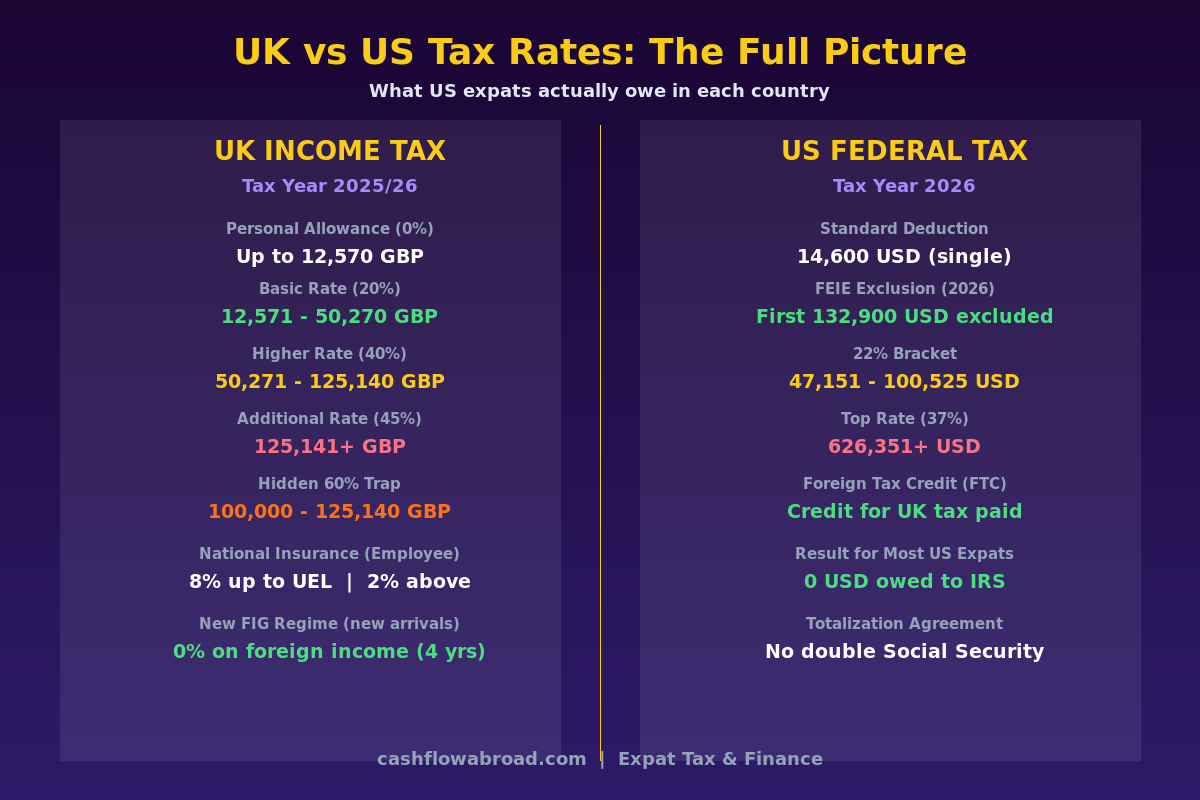

UK Income Tax Rates: What You're Actually Paying

UK income tax operates on a multi-band system for 2025/26 and 2026/27. The personal allowance — the amount you earn entirely tax-free — is frozen at £12,570 through 2030/31. Here's the structure:

| Band | Taxable Income | Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 – £50,270 | 20% |

| Higher Rate | £50,271 – £125,140 | 40% |

| Additional Rate | £125,141+ | 45% |

On top of income tax, employees pay National Insurance contributions: 8% on earnings between £242 and £967 per week, dropping to 2% above that upper earnings limit. Employer NI jumped to 15% in April 2025 (up from 13.8%), which has made British companies increasingly cautious about base salaries — factor that into any compensation negotiation.

The Hidden 60% Marginal Rate Trap

Here's the number that no one mentions until after the job offer: between £100,000 and £125,140, your effective marginal rate is 60%. As your income climbs through that band, the UK gradually claws back your entire personal allowance (£1 lost for every £2 earned over £100,000). You're paying 40% income tax on the extra income and losing 20% of what was previously tax-free. The mechanics are confusing enough that some very well-paid expats don't realize until their first self-assessment return.

If your UK salary is anywhere near £100,000, negotiate pension contributions, salary sacrifice arrangements, or other pre-tax benefits to pull your taxable income below that threshold. Above £125,140, the personal allowance is fully gone and you're at a clean 45%.

Your US Tax Obligations From London

The US taxes its citizens on worldwide income regardless of where they live. That rule doesn't change when you move to Shoreditch. What changes is how you offset the bill — and in the UK specifically, the math almost always works in your favor.

Two tools eliminate most or all US liability for UK-based Americans:

- Foreign Tax Credit (FTC): Dollar-for-dollar credit for UK taxes paid. Since UK income tax rates (20%–45%) are higher than equivalent US rates for most income levels, the credit typically wipes out US liability entirely. For most UK-based earners, there's simply no US tax left after the credit is applied.

- Foreign Earned Income Exclusion (FEIE): Exclude up to $132,900 (2026) of foreign earned income from US taxation. However, the FEIE and FTC cannot both be applied to the same income — you choose one. For most UK-based earners, the FTC wins because it credits both income and investment taxes; FEIE only covers earned income and blocks Roth IRA contributions.

For a deeper breakdown of how to choose between these two tools, see our guide to FEIE vs. Foreign Tax Credit. The short version for UK expats: if your UK salary exceeds $132,900, or you have investment income, the FTC is almost certainly the better choice.

The Tax Treaty Limitation Most People Miss

The US-UK tax treaty's saving clause largely renders treaty protections void for US citizens living in the UK. The treaty mostly helps UK citizens in the US, not Americans in the UK. Don't structure your finances expecting treaty relief to protect your income — rely on the Foreign Tax Credit instead. See our full guide on the saving clause for what the treaty actually does and doesn't do for Americans abroad.

The Totalization Agreement between the US and UK prevents double Social Security and National Insurance payments. If your UK employer is withholding NI, you don't simultaneously pay into US Social Security — and vice versa for Americans sent to the UK on short-term assignments (under 5 years) by US employers.

Maintaining a US address while you're in the UK is non-negotiable for keeping your US bank accounts, brokerage accounts, and IRS correspondence functional. Traveling Mailbox gives you a real US street address in 50+ cities for $15/month, with mail scanning and check deposit services. Without it, your US broker may flag your account when it detects a UK IP address — Vanguard, Fidelity, and Schwab have all restricted expat accounts after address mismatches since 2024. See our virtual mailbox guide for a full comparison of options.

For US-side banking that actually works abroad, Charles Schwab International remains the standard recommendation — no foreign transaction fees, free ATM withdrawals worldwide, and no known issues with expat account maintenance. For a comprehensive walkthrough of the full expat banking stack, see our US Expat Banking & Taxes Guide.

Visa Routes for Americans Moving to the UK

The UK has no passive income visa or official digital nomad visa. Your route depends entirely on how you plan to earn while there.

| Visa Type | Who It's For | Key Requirement | Duration |

|---|---|---|---|

| Skilled Worker | Employed by UK company | Job offer from approved sponsor, £41,700 minimum salary (or going rate for role) | Up to 5 years, renewable |

| UK Ancestry | Those with UK-born grandparent | One UK-born grandparent, ability to work, usually Commonwealth citizenship | 5 years, path to ILR |

| Global Talent | Leaders in tech, science, arts | Endorsement from recognized body (UKRI, Royal Society, etc.) | Up to 5 years |

| Innovator Founder | Entrepreneurs starting UK business | Endorsement from approved body, genuine innovative business plan | 3 years, renewable |

| Family Visa | Spouse/partner of UK settled person | Sponsor meets income threshold (£29,000+ as of 2024) | 2.5 years initially |

| Student Visa | Full-time study | Licensed sponsor, English proficiency, financial maintenance | Duration of course + 4 months |

Most Americans arrive via Skilled Worker — either relocating for a job or being transferred by a US employer with a UK entity. If you have a UK-born grandparent, the Ancestry visa is one of the most underused routes available: no employer sponsorship required, immediate right to work, and a direct path to Indefinite Leave to Remain (ILR) after 5 years.

Remote workers employed by non-UK companies have no clean legal path. You cannot work remotely for a foreign employer on a Standard Visitor visa. If you're operating this way, you're in a grey area — consult an immigration solicitor before you arrive.

Cost of Living: London vs the Rest

London has a premium that surprises even well-paid American expats. But most of the UK is dramatically cheaper — and the cities have gotten more attractive as remote and hybrid work normalized high salaries outside the capital.

| City | 1-Bed (Central) | 1-Bed (Outer Areas) | Monthly Budget (Single) |

|---|---|---|---|

| London | £1,800 – £2,500 | £1,200 – £1,800 | £3,500 – £5,500 |

| Manchester | £900 – £1,300 | £650 – £900 | £2,000 – £3,200 |

| Edinburgh | £1,000 – £1,500 | £700 – £1,000 | £2,200 – £3,500 |

| Birmingham | £800 – £1,200 | £600 – £850 | £2,000 – £3,000 |

| Bristol | £950 – £1,400 | £700 – £1,000 | £2,200 – £3,400 |

Council tax — the UK's equivalent of local property tax, charged to both renters and owners — runs £1,000–£2,500 per year depending on property band and location. It's one of those costs Americans don't see coming because nothing equivalent exists in most US states. Budget £100–£200/month and factor it in from day one.

Utilities (electricity, gas, broadband) run £150–£300/month in most UK homes. UK energy costs spiked significantly in 2022–2023 and have partially recovered, but remain roughly 2–3x higher per unit than the US average. Older British housing stock is notoriously poorly insulated — check the property's Energy Performance Certificate (EPC) rating before signing a lease.

Grocery prices are roughly 20–30% lower than comparable US prices for most staple categories. Eating out in London averages £60–£90 for dinner for two with drinks. Outside London, £35–£55 is more typical.

Banking in the UK as an American

Opening a UK bank account as a new arrival is harder than it should be. Traditional banks like Barclays, Lloyds, and NatWest typically require proof of UK address before you've had time to secure one — a classic chicken-and-egg problem for your first month.

The practical path forward:

- Monzo or Starling: Open instantly with a UK address, including temporary accommodation. These digital banks are free, app-based, widely accepted for direct deposit, and require no minimum balance. Start here on day one.

- HSBC Expat: HSBC's offshore banking arm accepts Americans with international financial relationships. Accounts hold USD, EUR, and GBP. No monthly fee if you meet their eligibility criteria — good for larger balances and international wires.

- Barclays International: Requires £100,000 minimum across all accounts. Only relevant if you're moving significant assets.

All UK banks are FATCA-compliant and will report your account details to the IRS. That's expected and doesn't create additional US liability — the data just flows. Make sure you're filing your FBAR (FinCEN Form 114) if your UK accounts exceed $10,000 in aggregate at any point during the calendar year.

For moving money between the UK and US, Remitly offers competitive GBP/USD rates with predictable delivery and substantially lower fees than traditional wire transfers. For occasional large transfers, compare rates on the day — exchange spreads vary considerably.

Healthcare: NHS, the IHS, and Private Insurance

Healthcare is where the UK genuinely delivers value for American expats — if you understand the mechanics.

Most visa holders arriving on visas of 6+ months must pay the Immigration Health Surcharge (IHS): £1,035 per year as of 2025, paid upfront with your visa application. In exchange, you get full NHS access — primary care, hospital care, mental health services — with no co-pays and no deductibles. The median US employer-sponsored health insurance premium for a single employee was $8,435 in 2024. At £1,035/year (~$1,300), the NHS represents roughly a 6x cost advantage for comparable catastrophic coverage.

The known limitation is waiting times. As of late 2025, over 7.5 million people were on NHS waiting lists for routine consultant-led treatment in England. Elective procedures — hip replacements, cataracts, non-urgent specialist referrals — can involve waits of several months. NHS prescription charges are frozen at £9.90 per item through April 2027.

For immediate or elective access, private health insurance starts at £60–£150/month for individual coverage. Many UK professional roles include private medical insurance (PMI) as a standard benefit — negotiate for it if it's not in your initial offer. Bupa, AXA Health, and Aviva are the main providers.

During your transition period — or if you're testing the UK before committing — SafetyWing's Nomad Insurance offers flexible month-to-month international coverage starting around $56/month, covering you across 180+ countries with no long-term commitment. For a full comparison of international health insurance options, see our Expat Health Insurance Guide.

The Verdict: Who the UK Actually Works For

The UK doesn't fit the standard expat tax optimization playbook — there's no territorial regime, no lump-sum flat tax, no residency-light structure. What it offers instead is a set of advantages most competitors can't match: world-class infrastructure, English language, a legitimate path to permanent residency, and tax mechanics that almost universally produce $0 owed to the IRS.

The FIG regime's 4-year window makes the UK genuinely interesting for Americans who qualify (10+ years outside the UK) and who have substantial foreign income to shield during that window. US dividends and rental income that would add 40–45% UK tax liability after year four can compound tax-free for four full years under FIG.

The UK works best for:

- Earning a UK salary in the £50,000–£95,000 range — high enough to live well in any UK city outside central London, low enough to avoid the 60% trap

- New arrivals qualifying for FIG (haven't been UK-resident for 10+ years) who have significant foreign investment income to shield

- Families willing to leave London — Manchester, Edinburgh, and Bristol offer comparable quality of life at 40–50% lower housing costs

- Anyone with an existing US investment portfolio — FTC eliminates US tax on that income; FIG eliminates UK tax during the exemption window

The UK is the wrong base for: high earners approaching £100,000 who can't optimize pension contributions, remote workers with no viable visa path, and anyone expecting a low-tax jurisdiction in absolute terms. It isn't low-tax. But the treaty plumbing means it's rarely the double-taxation disaster people assume before they do the math.

For a broader view of how high-tax-country residency fits into an expat tax strategy, our zero federal income tax guide covers which structures work for US citizens in countries like the UK, and our expat investing playbook addresses how to manage a US brokerage account from abroad without triggering PFIC issues.

Summary: Key Numbers for UK-Bound Americans

- FIG regime: 4-year foreign income exemption for new UK residents with 10+ consecutive years outside the UK (from April 6, 2025)

- UK income tax: 20% basic / 40% higher / 45% additional; effective 60% marginal rate between £100,000–£125,140

- Employee National Insurance: 8% up to £967/week; 2% above

- FEIE exclusion (2026): $132,900 on foreign earned income

- IHS surcharge: £1,035/year for full NHS access on qualifying visas

- Skilled Worker visa minimum salary: £41,700 (or role's going rate)

- London 1-bed apartment (central): £1,800–£2,500/month

- Manchester / Birmingham / Bristol 1-bed: £700–£1,300/month

- US federal tax result for most UK expats: $0 via Foreign Tax Credit

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws in both the US and UK are complex and change frequently. Individual circumstances vary significantly — always consult a qualified tax professional with experience in US expat taxation and UK tax law before making decisions about your residency, tax filing strategy, or financial planning. The author and cashflowabroad.com are not liable for any actions taken based on this content.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJune 17, 2026

Expat Tax & FinanceJune 17, 2026

Form 1116: How to Recover Foreign Taxes as a US Expat

Learn how Form 1116 works: income baskets, the credit limitation formula, dividend withholding recovery, FEIE interaction, and the 10-year

Expat Tax & FinanceJune 10, 2026

Expat Tax & FinanceJune 10, 2026

Norway Wealth Tax and Income Tax: A US Expat's Guide

Norway levies a 1.0% annual wealth tax on assets above $174,000 plus income tax reaching 47.5%. US expats learn what they owe, FTC strategy, and visa

Expat Tax & FinanceJune 5, 2026

Expat Tax & FinanceJune 5, 2026

Foreign Pensions and US Tax: UK, Canada, Germany

UK state pension is taxable in US. Canadian RRSP defers automatically. German pension triggers US tax. Country-by-country expat pension tax guide.