UAE Free Zone: 0% Tax, $2,500 Setup, One Big Catch for Americans

That company pays 0% corporate tax on foreign-sourced income. No personal income tax. No capital gains tax. No withholding tax on dividends.

That company pays 0% corporate tax on foreign-sourced income. No personal income tax. No capital gains tax. No withholding tax on dividends.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Here's a number that should stop you mid-scroll: the United Arab Emirates has 45 free zones, and the cheapest legitimate company setup costs around $1,565. That company pays 0% corporate tax on foreign-sourced income. No personal income tax. No capital gains tax. No withholding tax on dividends.

For most nationalities, this is a clean arbitrage play. For US citizens, there's a layer of complexity that can turn a smart tax structure into a compliance disaster — or if you handle it right, still make the whole thing worth it.

This guide cuts through the marketing noise from UAE business setup agencies and explains the structure honestly: what the 0% tax actually covers, what it costs to maintain, and what US reporting obligations you're taking on the moment you incorporate abroad.

What UAE Free Zones Actually Are

Free zones are special economic areas within the UAE that operate under their own regulatory frameworks. They were created to attract foreign investment — letting foreigners own 100% of their company (versus the 51% local partner requirement on mainland UAE), repatriate profits freely, and import/export goods without customs duties.

There are now more than 45 of them: DMCC (Dubai Multi Commodity Centre), RAKEZ (Ras Al Khaimah Economic Zone), SHAMS (Sharjah Media City), IFZA (International Free Zone Authority), DIFC (Dubai International Financial Centre), JAFZA (Jebel Ali Free Zone), and dozens more. Each has a niche. DMCC focuses on commodities and finance. SHAMS caters to media, marketing, and creative freelancers. RAKEZ is general-purpose and budget-friendly. DIFC is the serious financial services hub with its own common law court system.

When the UAE introduced a 9% corporate tax in June 2023 — its first-ever — free zone companies were carved out with a specific exemption called Qualifying Free Zone Person (QFZP) status. Meet the criteria, and you still pay 0%.

The 0% Tax Structure — How QFZP Status Works

To maintain the 0% rate, a free zone company must qualify as a QFZP. That requires meeting all of these conditions simultaneously:

- Incorporated or registered in a recognized free zone

- Derives "qualifying income" (see below)

- Maintains "adequate substance" inside the free zone

- Has non-qualifying revenue below the de minimis threshold

- Prepares audited IFRS financial statements

- Complies with UAE transfer pricing documentation requirements

What Counts as Qualifying Income

Qualifying income covers two broad buckets: income from transactions with other free zone persons (B2B free zone to free zone), and income from "qualifying activities" — manufacturing, logistics, distribution, financial services under certain conditions, and intellectual property assets. Services to mainland UAE companies or individuals generally do not qualify. If you're a consultant billing primarily to UAE mainland clients, that revenue hits the 9% rate. Services to clients outside the UAE are typically fine.

The De Minimis Rule

There's a useful escape hatch: if non-qualifying income stays below the de minimis threshold — the lower of AED 5 million (~$1.36 million) or 5% of total revenue — the company can still maintain QFZP status. This lets companies with occasional mainland UAE clients keep the 0% rate on everything else.

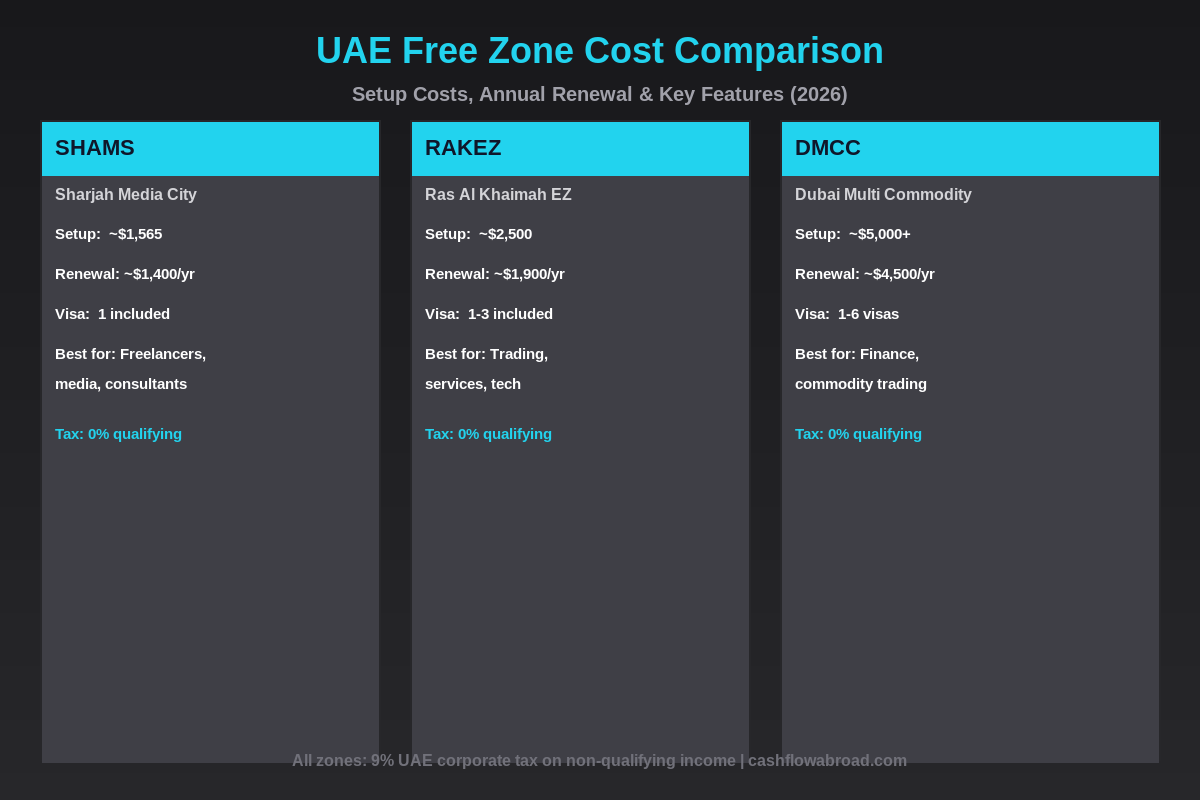

Free Zone Cost Breakdown: SHAMS, RAKEZ, IFZA, and DMCC

Setup costs vary significantly across zones. Here's an honest all-in breakdown for 2026 — not the teaser prices agencies advertise:

| Free Zone | Location | Setup Cost | Annual Renewal | Visas Included | Best For |

|---|---|---|---|---|---|

| Ajman Free Zone | Ajman | ~$1,330 | ~$1,100/yr | 0 (add-on) | Ultra-budget, solo operators |

| SHAMS | Sharjah | ~$1,565 | ~$1,400/yr | 1 included | Freelancers, media, creatives |

| RAKEZ | Ras Al Khaimah | ~$2,500–$4,100 | ~$1,900/yr | 1–3 included | Trading, services, tech |

| IFZA | Dubai | ~$2,970–$3,515 | ~$2,800/yr | 1–3 included | General business, consulting |

| DMCC | Dubai | ~$5,000–$13,600 | ~$4,500/yr | 1–6 visas | Finance, commodities, prestige |

| DIFC | Dubai | ~$15,000+ | ~$12,000+/yr | Varies | Financial services, funds |

Two costs get buried in agency quotes: the residency visa (roughly $950–$1,900 per visa once you factor in medical tests, Emirates ID, and processing fees) and accounting/audit fees (mandatory audited financials run $1,500–$4,000/year for small operations). Add those before making comparisons.

The annual commitment matters more than the setup cost. If you're choosing between SHAMS at $1,565 and IFZA at $2,970, the real question is $1,400/year vs $2,800/year — a $1,400 annual gap that compounds significantly over a 3–5 year horizon.

The US Expat Problem: What Nobody Tells You at the Setup Desk

Most free zone business setup agencies in Dubai have no idea how US tax law interacts with their product. They'll quote you 0% tax and hand you a brochure. What they won't mention:

Form 5471: The Annual $10,000 Penalty You've Never Heard Of

The moment a US citizen owns 10% or more of a foreign corporation — which a free zone company is — they're required to file Form 5471 (Information Return of US Persons with Respect to Certain Foreign Corporations) with their annual tax return.

Miss it? The IRS automatically assesses a $10,000 penalty per form, per year. Ignore an IRS notice for more than 90 days, and additional $10,000 penalties stack every 30 days, up to $50,000 per form. The IRS has been enforcing this aggressively since FATCA created cross-border financial data sharing between governments.

Form 5471 also triggers Subpart F income analysis. If your UAE company is a Controlled Foreign Corporation — meaning US persons own more than 50% of it — certain passive income (interest, royalties, dividends) may be "deemed distributed" to you and taxed in the US even if you never moved money. This intersects with GILTI (Global Intangible Low-Taxed Income), which hit foreign business owners hard after the 2017 Tax Cuts and Jobs Act. See our PFIC and CFC tax guide for the full breakdown.

FBAR and FATCA Reporting

Your UAE company bank account — at Emirates NBD, Mashreq, or whichever local bank you use — must be reported on FinCEN 114 (FBAR) if the aggregate balance exceeds $10,000 at any point during the year. FBAR is separate from your tax return, due April 15 with an automatic extension to October 15.

If your foreign financial assets exceed $200,000 (filing single while abroad), you also file Form 8938 under FATCA. Both the account balance and your ownership interest in the company can trigger this threshold independently.

Keeping a clean US banking relationship while managing UAE accounts is doable. Mercury handles USD operations with no monthly fees, and Charles Schwab International gives you fee-free ATM withdrawals worldwide plus a solid brokerage account — arguably the single best combination for US expats managing money across borders. Both require a US mailing address to maintain; Traveling Mailbox provides a real US street address with mail scanning from $15/month, which most UAE-based Americans use to keep their US accounts active and satisfy the IRS address requirement.

No US-UAE Tax Treaty Means No Easy Escape

The United States does not have an income tax treaty with the UAE. That means no treaty tie-breaker provisions to shed US tax residency, and no treaty mechanism to prevent double taxation on business income.

Your tools are the Foreign Earned Income Exclusion (FEIE) — which excludes up to ~$130,000 (2026) of foreign-earned income if you pass the bona fide residence or physical presence test — and the Foreign Tax Credit (FTC). Since the UAE collects 0% personal income tax, the FTC provides zero relief. You're relying on FEIE, which only covers earned income. Dividends and passive income flowing through the company are not protected. Read our complete FEIE guide before building your tax plan around it.

Who This Structure Actually Works For

Despite the compliance overhead, UAE free zones make genuine sense for a specific profile:

The genuine UAE relocator. If you're physically moving to Dubai, spending 183+ days there, establishing UAE tax residency, and running a business primarily serving international (non-US, non-UAE mainland) clients — the structure works. Your salary from the company is foreign-earned income covered by FEIE. The company pays 0% UAE tax. US liability gets managed through a combination of FEIE and careful corporate structuring.

The high-revenue service business. At $300,000+ in annual revenue, the compliance costs ($7,000–$10,000/year fully loaded) produce a net saving versus operating through a US S-corp or LLC while living in a high-tax state. Below $150,000 in profit, the math gets tight.

The non-US client business. SaaS products selling to European or Asian users, content agencies billing international brands, trading companies dealing with non-UAE parties — these are natural fits for clean QFZP status.

Who it doesn't work for: US expats primarily billing US clients (no UAE tax savings on that income), anyone planning to stay in the US or in a tax treaty country, and businesses below ~$120,000 in annual profit where compliance costs approach or exceed the benefit.

The UAE Tax Residency Piece

To actually sever tax residency in most countries (not the US — Americans are always US taxpayers), you need to become a UAE tax resident. That requires either:

- 183 days of physical presence in the UAE in any 12-month period, or

- 90 days in the UAE if it's your center of vital interests — primary home, family, business

Your free zone setup automatically qualifies you for a 2-year renewable residency visa as the company's owner or employee. That visa is your legal permission to live in the UAE — it's not the same as tax residency, but it enables it. The UAE's Golden Visa (5- or 10-year residency) is available to investors putting AED 2 million (~$545,000) into UAE property or qualifying public funds.

For US citizens specifically: UAE tax residency reduces your exposure to other countries (if you had prior residency in a high-tax jurisdiction), but it does nothing to reduce US obligations. The UAE arrangement simply means neither the UAE nor your prior country is taxing you — giving FEIE maximum room to cover your salary.

The Real Cost Math

Concrete scenario: a US freelance software consultant earning $200,000/year, moving to Dubai, billing European clients through a SHAMS free zone company.

| Annual Cost Item | Amount |

|---|---|

| SHAMS free zone renewal | $1,400 |

| UAE residency visa (2-yr, prorated) | $475 |

| Audited IFRS financial statements | $2,000 |

| US international tax CPA (expat specialist) | $4,500 |

| Traveling Mailbox US address | $180 |

| Total annual compliance cost | ~$8,555 |

Against that: the consultant saves UAE corporate tax (0% vs 9% on $200,000 profit = $18,000 theoretical saving), pays zero UAE personal income tax, and eliminates US taxable income on the first ~$130,000 of salary via FEIE. Depending on their previous state of residency, annual net savings versus operating a US LLC from a high-tax state run $25,000–$55,000. The structure pays for its compliance cost inside the first year for most six-figure earners.

How to Set One Up: The Actual Process

If the numbers work, setup is genuinely fast — free zones have made the mechanics deliberately simple to attract capital:

- Choose your free zone by business activity: media/creative → SHAMS; general services → RAKEZ or IFZA; commodities/finance → DMCC

- Select your license type: most service businesses use Professional Services or Freelancer — general trading requires a different structure

- Submit documents: passport copy, recent photo, application form, basic business plan for some zones

- Pay setup fee and receive trade license (typically 5–15 business days)

- Apply for UAE residency visa: entry permit → medical test → Emirates ID → visa stamping (~3–4 weeks total)

- Open UAE bank account: Emirates NBD, Mashreq, or First Abu Dhabi Bank — budget 4–8 weeks, UAE banks are slow and document-heavy

- Engage UAE accountant to set up IFRS-compliant books and handle mandatory annual audit

- Hire US international tax CPA before your first year-end — not after

Step 8 is where Americans get burned. Free zone agents will help with steps 1–6. None of them will mention Form 5471 or Subpart F income. You need a CPA who specializes in US expat international business taxation — not the agency that sold you the license, and not your domestic accountant back home. Our US expat banking and tax guide covers the full reporting framework you'll need to understand going in.

On banking: some free zone owners maintain dual setups — UAE account for local operations and AED transactions, US accounts for dollar-denominated income and investments. That works well. Keep your US banking alive with a virtual mailbox address, and use Schwab for fee-free ATM access across the 180+ countries the UAE sends you to for business.

Bottom Line

The UAE free zone play is legitimate — but it's not the turnkey 0% tax solution the setup agencies sell. For US expats specifically, it comes packaged with mandatory Form 5471 filings, FBAR reporting, zero treaty protection, and GILTI exposure on passive income. The compliance infrastructure runs $7,000–$10,000/year to maintain correctly.

Done right — with the right revenue level, the right client base, and genuine UAE presence — it generates net tax savings that dwarf the compliance cost. Done sloppily (LLC registered in a free zone you've never physically visited, run from a US IP address) it creates penalties that make the tax savings irrelevant and then some.

Start with a US expat tax attorney before you sign anything with a free zone agent. The $500 consultation costs less than one month of Form 5471 penalties. And read our guide to building an online business from anywhere for the full framework on structuring income that stays clean across jurisdictions.

Financial disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. UAE tax law, IRS regulations, and free zone rules change. Consult a qualified international tax professional before making decisions about foreign company formation or tax structuring.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Business & Remote WorkJuly 22, 2026

Expat Business & Remote WorkJuly 22, 2026

US Company EU VAT Number: When You Need One

Know when US companies need EU VAT registration, OSS, IOSS, reverse charge, or marketplace handling before selling to Europe.

Expat Business & Remote WorkJuly 10, 2026

Expat Business & Remote WorkJuly 10, 2026

EU VAT for US Digital Sellers: A Practical Guide

US expats selling digital products to EU consumers owe VAT once sales top €10,000/year. How OSS registration, B2B reverse charge, and platform

Expat Business & Remote WorkJune 30, 2026

Expat Business & Remote WorkJune 30, 2026

Brixaz Opens a Free US Marketplace

Use Brixaz to post or find US gigs, services, jobs, housing, vehicles, and classifieds with free posting and direct contact.