Switzerland for US Expats: Taxes, Visas & the $5K/Month Life

Switzerland is the fourth most expensive country on earth. The federal income tax rate caps at just 11.5% . The catch? The right one keeps it under 22%.

Switzerland is the fourth most expensive country on earth. The federal income tax rate caps at just 11.5% . The catch? The right one keeps it under 22%.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Switzerland is the fourth most expensive country on earth. A single bedroom in Zurich runs CHF 2,500–3,800 a month, a café lunch costs CHF 25, and a restaurant bottle of wine will cheerfully relieve you of CHF 50. Yet by the standards of most US expat destinations, Switzerland is also a surprisingly low-tax jurisdiction — if you play it right.

The federal income tax rate caps at just 11.5%. Capital gains on private stock portfolios are zero in every canton. And a program called lump-sum taxation lets wealthy retirees pay a fixed annual bill instead of disclosing actual income. The catch? Swiss tax is three-dimensional: federal, cantonal, and municipal layers stack on each other, and the wrong canton can push your effective rate past 43%. The right one keeps it under 22%.

This guide covers everything a US citizen needs to know before making the move: canton arbitrage, the FEIE vs. Foreign Tax Credit decision, residency paths, banking as an American, and what CHF 5,000 a month actually buys.

Switzerland's Three-Layer Tax System

Every Swiss resident pays income tax at three levels simultaneously: federal, cantonal, and municipal. Federal rates are uniform across the country and top out at 11.5% on income above CHF 895,800. The cantonal and municipal layers are where the real variation lives.

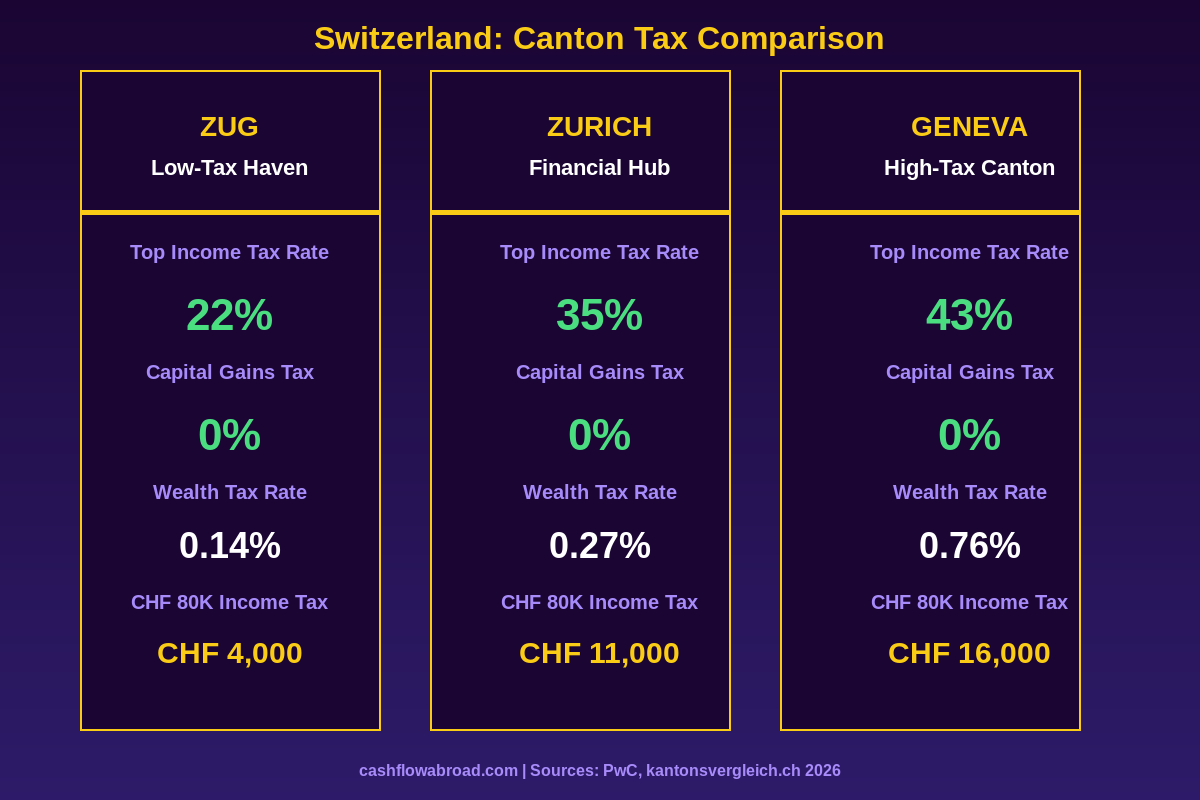

Cantons set their own base rates, then municipalities apply a multiplier. Move from Geneva to Zug — a one-hour drive — and your combined effective rate drops from 43% to 22% on the same income. That's not a rounding error. On a CHF 500,000 income, choosing Zug over Geneva saves more than CHF 100,000 per year in income tax alone.

The other thing Switzerland taxes that most US expats don't expect: wealth tax. Unlike income tax, this is an annual levy on your net assets — bank accounts, investment portfolios, real estate equity. Rates range from roughly 0.14% in Zug to 0.76% in Vaud. On a $2 million net worth, that's $2,800 to $15,200 per year, every year, just for existing. Canton selection matters here too.

Canton Shopping: The 21-Point Arbitrage

The difference in Swiss tax burdens between cantons is one of the largest legal tax arbitrage plays available to any expat anywhere in the developed world. Here's how the major cantons compare:

| Canton | Top Effective Rate | Wealth Tax Rate | Tax on CHF 80K Income | Character |

|---|---|---|---|---|

| Zug | 22% | 0.14% | ~CHF 4,000 | Lowest in Switzerland, global finance hub |

| Schwyz | 22–24% | 0.17% | ~CHF 4,500 | Lake access, 45 min from Zurich by train |

| Obwalden | 24% | 0.15% | ~CHF 5,200 | Flat cantonal rate, rural Alpine setting |

| Zurich | 35–38% | 0.27% | ~CHF 11,000 | Major global city, top salaries, higher cost |

| Vaud | 40% | 0.76% | ~CHF 14,000 | Lausanne, Lake Geneva, wine country |

| Geneva | 43% | 0.56% | ~CHF 16,000 | UN/international orgs, luxury expat scene |

For context: CHF 12,000 in annual tax savings — the Zug-vs-Geneva delta on CHF 80K income — is enough to pay several months of rent in Zug. At higher income levels the math becomes overwhelming. The caveat: Zug and Schwyz lack the cosmopolitan amenity set of Zurich or Geneva, though Zug has developed a thriving expat community, and Zurich is a 25-minute train ride away.

You must actually live in the low-tax canton. Swiss authorities pay close attention to genuine domicile. The 183-day standard applies, but Swiss tax inspectors also look at center-of-life factors: where your family lives, where you sleep on weekends, where your car is registered. Paper-only canton shopping gets challenged.

Your US Tax Obligations Don't Move with You

Switzerland does not make you a non-filer with the IRS. The US taxes citizens on worldwide income regardless of residence, so you'll still file a federal return every year. What changes is how you reduce or eliminate that liability. For the full framework, see our US Expat Banking & Taxes guide.

Two tools dominate for Switzerland-based Americans:

- Foreign Earned Income Exclusion (FEIE): Excludes up to $132,900 of foreign-earned income from US tax in 2026 (indexed annually). Requires either the Physical Presence Test (330+ days abroad in any 12-month period) or the Bona Fide Residence Test. Applies only to earned income — wages, freelance, self-employment. Not dividends or capital gains.

- Foreign Tax Credit (FTC): Credits Swiss taxes paid against your US liability dollar-for-dollar. Particularly powerful on investment and passive income, and in high-tax cantons where Swiss rates exceed what the US would charge.

The choice between FEIE and FTC is not arbitrary. It depends almost entirely on which canton you live in — and how your income is structured.

FEIE vs. Foreign Tax Credit: The Canton-Driven Decision

In a high-tax canton like Geneva (effective rate 43%), the Foreign Tax Credit almost always wins for earned income. Your Swiss tax bill exceeds the US tax on the same income, creating excess credits that roll forward to offset future US liability. Using FEIE instead would leave that Swiss tax overpayment unclaimed.

In a low-tax canton like Zug (effective rate 22%), the equation can flip. Switzerland collects less tax than the US would on the same income, so the FTC may not fully zero out your US bill. The FEIE might exclude more liability — especially if your earned income stays under $132,900. But FEIE zeroes out your earned income for contribution purposes, killing your ability to fund a Roth IRA. If wealth accumulation through tax-advantaged accounts matters, that's a real cost. Our deeper analysis is in the FEIE guide and the expat investing playbook.

The practical answer: run both scenarios before you file. The difference can easily run $10,000–$30,000 per year depending on income and canton.

Zero Capital Gains: Switzerland's Most Underrated Benefit

Switzerland does not tax capital gains on securities for private investors. Sell $500,000 worth of stocks, ETFs, or bonds — zero Swiss capital gains tax. This is one of the most underappreciated benefits of Swiss residency, and a primary reason wealthy individuals in finance and tech specifically choose Zug.

The exemption applies to private investors, not professional traders. Swiss authorities use a multi-factor test to determine if you've crossed into "professional" status — red flags include holding periods under six months, high transaction frequency, use of leverage, and capital gains exceeding total earned income. Passive, long-term investors should be well clear of those thresholds.

Crucially: the IRS still taxes your US-side gains under normal rules. This only eliminates the Swiss-side liability. But for a US expat who owes Swiss tax on nothing and US capital gains tax at the standard long-term rate (0–20%), Switzerland's zero treatment is worth real money. For brokerage infrastructure that works for expats, Charles Schwab International is one of the few major US brokerages that actively supports expat accounts, provides fee-free global ATM withdrawals, and won't close your account because you moved abroad.

The Forfait Fiscal: Switzerland's Secret for Wealthy Retirees

Switzerland offers one of the world's most unusual tax structures for wealthy foreigners: expenditure-based taxation, known locally as the forfait fiscal or Pauschalsteuer. Instead of paying tax on actual income, you pay tax on a flat estimate of your annual living expenses. No income disclosure. No asset reporting to Swiss authorities.

The federal minimum taxable base is CHF 435,000. In practice the actual minimum annual tax burden runs CHF 200,000–500,000 depending on the canton, since cantons apply their own higher floors. That's not a tool for mid-level earners — this structure exists for people with large investment portfolios or business exits where the alternative is paying Swiss income tax on CHF 2M+ per year.

| Feature | Details |

|---|---|

| Eligibility | Foreign nationals new to Switzerland (or absent for 10+ years); no gainful employment in Switzerland |

| Federal minimum taxable base | CHF 435,000 |

| Estimated annual minimum tax | CHF 200,000–500,000 (cantonal variation) |

| Cantons offering the program | Most cantons — Zurich, Basel-Stadt, Basel-Landschaft, Schaffhausen have abolished it |

| Popular choices | Valais, Graubünden, Ticino, Nidwalden |

| US tax interaction | IRS still taxes actual worldwide income; forfait fiscal only covers Swiss side |

The math works for someone generating, say, CHF 3M+ in annual investment returns. Swiss tax on that income under normal rules might run CHF 700,000–1,200,000. Under the forfait fiscal, the bill might be CHF 250,000–400,000. The Swiss government gets a stable, predictable revenue stream; you get privacy and a significantly lower bill.

Residency and Visa Paths for Americans

Switzerland is not in the EU, has no open-door policy for third-country nationals, and offers no dedicated digital nomad visa. Long-term residency for Americans requires one of a limited number of routes:

| Permit Type | Who It's For | Key Requirement | Duration |

|---|---|---|---|

| B Permit (Employment) | Hired by Swiss employer | Job offer; employer must demonstrate no suitable local candidate | 1–2 years, renewable |

| B Permit (Self-Employment) | Entrepreneurs, freelancers | Prove economic benefit to Switzerland; very high bar for non-EU nationals | 5 years if approved |

| Lump-Sum Residency | Wealthy retirees/investors | Agree to forfait fiscal; cannot work in Switzerland | B Permit, renewable |

| Family Reunification | Married to Swiss citizen or resident | Valid marriage, co-habitation | B Permit → C Permit after 5 years |

| Schengen Tourist | Short-stay exploration | No visa needed for US citizens | 90 days in any 180-day period |

For US remote workers — earning income from US clients while living in Switzerland — the path is harder than in countries with explicit digital nomad visas. Self-employment as a non-EU national requires demonstrating that your activity economically benefits Switzerland, which is a genuinely high bar. The workaround most attorneys recommend: establish a Swiss GmbH (LLC equivalent, minimum capital CHF 20,000) or work with a Swiss co-founder who can help justify the permit. After five continuous years on a B Permit you can apply for the C Permit (permanent residency), and after 10 total years of legal residence, Swiss citizenship — which allows dual nationality.

What CHF 5,000 a Month Actually Buys

Switzerland is genuinely expensive, and the people who moved here expecting Paris prices got an education fast. CHF 5,000/month (~$5,500 USD) is a lean but livable single-person budget in a smaller city like Zug or Winterthur; it's tight in Zurich or Geneva. Here's the honest breakdown:

| Expense | Monthly Cost (CHF) | Notes |

|---|---|---|

| 1BR apartment (Zug / smaller city) | 1,800–2,500 | Zurich / Geneva add CHF 600–1,200 |

| Groceries (single person) | 400–600 | 50–100% more expensive than neighboring Germany |

| Health insurance (mandatory LaMal plan) | 300–450 | Must enroll within 3 months of arrival; covers most care |

| Public transport | 70–200 | SBB GA travelcard ~CHF 3,860/year covers all trains and buses |

| Utilities (electricity, water, internet) | 150–300 | Often partially included in rent |

| Dining out (occasional) | 300–600 | CHF 20–35 lunch, CHF 50–90 dinner for one |

| Lean total | ~CHF 3,000–4,650 | Leaves CHF 350–2,000 discretionary on CHF 5K budget |

The tricks most expats learn quickly: shop at Aldi and Lidl (yes, they operate in Switzerland and run 30–40% cheaper than Migros or Coop), buy an annual transit pass instead of a car, and cook at home most nights. With those habits, a single person can live reasonably well on CHF 4,500–5,000 per month in Zug or Winterthur. Budget CHF 6,000–7,500 for Zurich city proper, more for Geneva.

One upside that surprises most Americans: Swiss healthcare quality is exceptional. Even the basic mandatory LaMal plan gives you access to world-class facilities, with annual deductibles running CHF 300–2,500. The monthly premium (CHF 300–450 for a healthy adult) can feel steep, but the per-visit costs and hospital care costs are a fraction of what Americans pay out-of-pocket at home. See our broader expat health insurance comparison for context.

Banking as an American in Switzerland

FATCA has complicated US-expat banking everywhere, but Switzerland especially. After FATCA implementation in 2014, many private Swiss banks quietly stopped accepting US clients rather than build IRS reporting infrastructure. UBS — which absorbed Credit Suisse after its 2023 collapse — still serves US persons but with minimum deposits often running CHF 250,000–1,000,000 for investment accounts.

For most Americans, the practical everyday banking solution is PostFinance, Switzerland's postal bank. PostFinance accepts US persons with Swiss residency, charges no additional FATCA fees, and handles current accounts straightforwardly. It won't do investment management, but it works for day-to-day life.

Keep your US banking infrastructure intact regardless. Mercury works well for business accounts. Charles Schwab International covers US investing and global ATM withdrawals with zero foreign transaction fees — critical in a country where ATM usage is still common. For USD-to-CHF transfers, Remitly provides transparent fee structures and market-competitive exchange rates.

Also maintain a valid US mailing address. Banks and the IRS send correspondence to a US address, and letting that lapse leads to account closures and missed notices. A virtual mailbox like Traveling Mailbox ($15/month, real street address in 50+ US cities, digital mail scanning, check deposits) solves this completely. It's one of the most important — and most overlooked — pieces of the expat banking stack. Full breakdown in our virtual mailbox guide.

The US-Switzerland Tax Treaty: Useful but Incomplete

The US-Switzerland Income Tax Treaty has been in force since 1998 (updated by a 2009 Protocol). It provides reduced withholding rates on dividends (15% standard, 5% for significant shareholders), interest, royalties, and pension income, plus tie-breaker rules for dual residents.

The limitation most expats run into: the savings clause. The US reserves the right to tax its citizens as if the treaty didn't exist, which largely blocks US citizens from using treaty provisions to reduce US tax on their own worldwide income. The treaty's main practical benefit for US citizens is preventing Switzerland from taxing US-source income, reducing Swiss withholding on cross-border payments, and providing a mutual agreement procedure when both countries try to tax the same income. It's useful — it's not a silver bullet.

The Bottom Line: Who Switzerland Actually Makes Sense For

Switzerland is not a budget expat play. The lifestyle is extraordinary and the stability is unmatched, but you need income that can support CHF 5,000–7,500/month in living costs while still building wealth. With that caveat, three profiles genuinely benefit:

- High-income tech and finance professionals hired by Swiss multinationals — Zurich and Zug salaries for senior engineers and finance roles often run CHF 150,000–250,000+. Combined with zero Swiss capital gains tax and a moderate income rate in Zug, net wealth accumulation beats most OECD peers.

- Wealthy retirees with large investment portfolios — the zero capital gains treatment and the forfait fiscal together make Switzerland genuinely competitive with Monaco and Andorra for the right net worth level, at a far higher quality of life than either.

- Remote workers earning USD who can qualify for a self-employment permit — living in Zug on a strong remote salary with zero Swiss capital gains and a 22% effective income tax rate is a legitimate, powerful structure.

Switzerland is not for the digital nomad on a tight budget, the person who wants an easy visa process, or anyone hoping the expensive reputation is exaggerated. It rewards people who can absorb the cost of living and who have the income structure to benefit from zero capital gains, low cantonal tax rates, and world-class financial infrastructure. For those people, the canton-shopping arbitrage alone can save more than the entire annual cost of living somewhere cheaper.

Conclusion

The cliché that Switzerland is both expensive and high-tax is half-right at best. It is genuinely expensive — own that upfront. But the tax picture is far more nuanced: federal rates top out at 11.5%, capital gains on private portfolios are untaxed in every canton, and a 21-percentage-point spread in effective rates between cantons creates real arbitrage for anyone willing to live in Zug instead of Geneva. Add a comprehensive US tax treaty, a credible FEIE/FTC strategy, and the most stable banking and political environment on the continent, and Switzerland earns serious consideration from expats who can clear the cost-of-living hurdle.

The homework is non-trivial. B Permits require real legal groundwork, the FEIE vs. FTC decision changes by canton and income structure, and PostFinance is not the same experience as Credit Suisse's private banking. But for the expat who gets those pieces right, Switzerland is one of the rare places where premium lifestyle and below-expectation taxes coexist — not despite the price tag, but in part because of the quality it funds.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. US expat tax rules are complex and fact-specific. Swiss income tax rates, cantonal variations, and permit requirements change regularly. Consult a qualified cross-border CPA or tax attorney with Swiss expertise before making residency or tax strategy decisions. Verify current permit requirements with Swiss cantonal immigration authorities.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJuly 19, 2026

Geographic ArbitrageJuly 19, 2026

Sofia Remote Work Budget Under $2,000

Price rent, transit, utilities, insurance, and visa caveats before using Sofia, Bulgaria as a lower-cost EU base for remote work.

Geographic ArbitrageJune 30, 2026

Geographic ArbitrageJune 30, 2026

Moving Abroad with Kids: School Costs and Family Budget

International school fees change the whole geographic arbitrage math for families. Compare real costs in Medellín, Chiang Mai, Mexico, and Lisbon for

Geographic ArbitrageJune 29, 2026

Geographic ArbitrageJune 29, 2026

Bali for US Expats: Monthly Costs and Permit Guide

How much Bali costs, which Indonesian stay permit suits long-term stays, and what US citizens owe the IRS while living there in 2025.