South Korea for US Expats: Taxes, Visas & the $1,800/Month Life

It also charges qualifying foreign workers a flat 19% income tax — for up to 20 years. That's cheaper than Austin. This guide runs them for you.

It also charges qualifying foreign workers a flat 19% income tax — for up to 20 years. That's cheaper than Austin. This guide runs them for you.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

South Korea is the 12th largest economy on earth, has some of the world's fastest internet (median 200+ Mbps), and runs a public healthcare system consistently ranked among the top five globally. It also charges qualifying foreign workers a flat 19% income tax — for up to 20 years. And a single American can live comfortably in Seoul on $1,800 a month.

That's cheaper than Austin. For a developed OECD nation with a subway system that makes the NYC MTA look like a museum exhibit.

Yet South Korea rarely shows up in the expat finance conversation the way Thailand or Portugal do. The language barrier, the cultural intensity, the "Korea is expensive" reputation from Seoul's glitzy districts — all of it keeps Americans from running the numbers. This guide runs them for you.

Why South Korea Is Quietly Winning the Expat Race

Korea's per capita GDP sits around $35,000 — solidly developed world. Unemployment under 3%. Seoul's Incheon Airport has ranked as the world's best airport for 12 consecutive years. You get all the infrastructure of a first-world country at prices that have been suppressed by a Korean Won that's traded at a structural discount to the dollar for years.

The expat community is diverse: around 400,000 foreign residents live in Korea, with a significant US military and civilian presence, tech professionals working at Samsung, LG, and Hyundai affiliates, and a fast-growing contingent of remote workers drawn in by the F-1-D Workation Visa. English is widely spoken in Seoul's expat-friendly neighborhoods like Itaewon, Hongdae, and Mapo-gu.

The K-pop and Korean drama cultural wave has also driven enormous demand from younger Americans who already speak basic Korean, understand the culture, and are genuinely excited to be there — an underrated factor in long-term quality of life abroad.

The F-1-D Workation Visa: What Americans Need to Know

Korea launched its F-1-D "Workation" visa in January 2024 and made it a permanent program. For remote workers with US or international clients, this is the cleanest path to legally living in Korea.

Requirements:

- Annual income of at least ₩88.1 million (~$66,000 USD) — roughly double Korea's GNI per capita

- Income must come from clients or employers outside South Korea

- Private health insurance covering at least ₩100 million (~$75,000) including medical treatment and repatriation

- Valid passport, bank statements, employer or client documentation

What you get:

- 1-year multi-entry visa, renewable once (2 years total maximum)

- Spouse and minor children can accompany you as dependents

- No requirement to register a Korean business or find a Korean employer

For health insurance, SafetyWing's Nomad Insurance covers remote workers in 180+ countries and satisfies many digital nomad visa insurance requirements — verify it meets the ₩100 million threshold before submitting your application.

If you want to stay longer than two years or pursue permanent residency, the E-7 (skilled worker), D-8 (corporate investment), and F-2 (long-term residence) visas are worth exploring. F-5 permanent residency typically requires five continuous years of legal residence.

South Korean Income Tax: The 19% Flat Rate Most Americans Miss

Korea uses a progressive income tax system with eight brackets — and it gets steep fast:

| Taxable Income (KRW) | Approx. USD | National Rate | With 10% Local Surtax |

|---|---|---|---|

| Up to ₩14M | ~$10,500 | 6% | 6.6% |

| ₩14M–₩50M | ~$37,500 | 15% | 16.5% |

| ₩50M–₩88M | ~$66,000 | 24% | 26.4% |

| ₩88M–₩150M | ~$112,500 | 35% | 38.5% |

| ₩150M–₩300M | ~$225,000 | 38% | 41.8% |

| Over ₩300M | $225,000+ | 40–45% | 44–49.5% |

Here's the part most expats miss: foreign workers who begin employment in Korea by December 31, 2026 can elect a flat 19% national tax rate (20.9% with local surtax) instead of the progressive brackets — and maintain that flat rate for up to 20 years.

The catch: you forfeit all deductions and credits under this election. The math depends on your income level. If you're earning ₩130–150 million ($97,000–$112,000) or more annually in Korea, the flat rate typically wins. Below that threshold, the progressive system with deductions often produces a lower effective rate.

There's also the 5-year rule: if you've spent fewer than 5 years in Korea out of any 10-year period, you're only taxed on Korean-source income — not your worldwide income. This is a significant protection for expats in the early years of residence. Cross the 5-year mark and Korea taxes everything globally, just like the US.

Additionally, employees pay into Korea's social insurance system: National Pension (4.75% of gross salary) and National Health Insurance (4.07%), with employers matching. These are substantial contributions to factor into any compensation package.

How US-Korea Double Taxation Actually Works

The US-Korea Income Tax Treaty dates to 1976 and remains in force. It allocates taxing rights, reduces withholding rates on passive income, and provides a framework for resolving disputes — but it doesn't eliminate the need to file with both countries. Americans abroad always owe the IRS a return on worldwide income.

Your two main tools for avoiding double taxation:

Foreign Earned Income Exclusion (FEIE): Excludes up to $132,900 of foreign-earned income from US tax in 2026. You qualify by passing either the bona fide residence test or the physical presence test (330 days outside the US). For a full walkthrough, see our FEIE guide.

Foreign Tax Credit (FTC): Provides a dollar-for-dollar credit for taxes paid to Korea. Since Korea's effective rates frequently exceed US rates — especially once you're above the ₩88M bracket — the FTC typically eliminates more US liability than the FEIE would. Most US expats in Korea earning above $80,000 use the FTC.

The treaty also reduces withholding rates on dividends (15% max), interest (12% max), and royalties (15% max) paid between the two countries. If you hold US dividend-paying stocks while residing in Korea, this matters. Keep in mind the PFIC rules for any Korean-domiciled investment funds — that's a separate minefield covered in the expat investing playbook.

One practical note for F-1-D holders: the visa requires you to work for non-Korean clients or employers, which means your income is US or foreign-sourced. This doesn't exempt you from Korean residency tax after 183 days, but it gives you more flexibility in structuring your tax position during the early years under the 5-year rule.

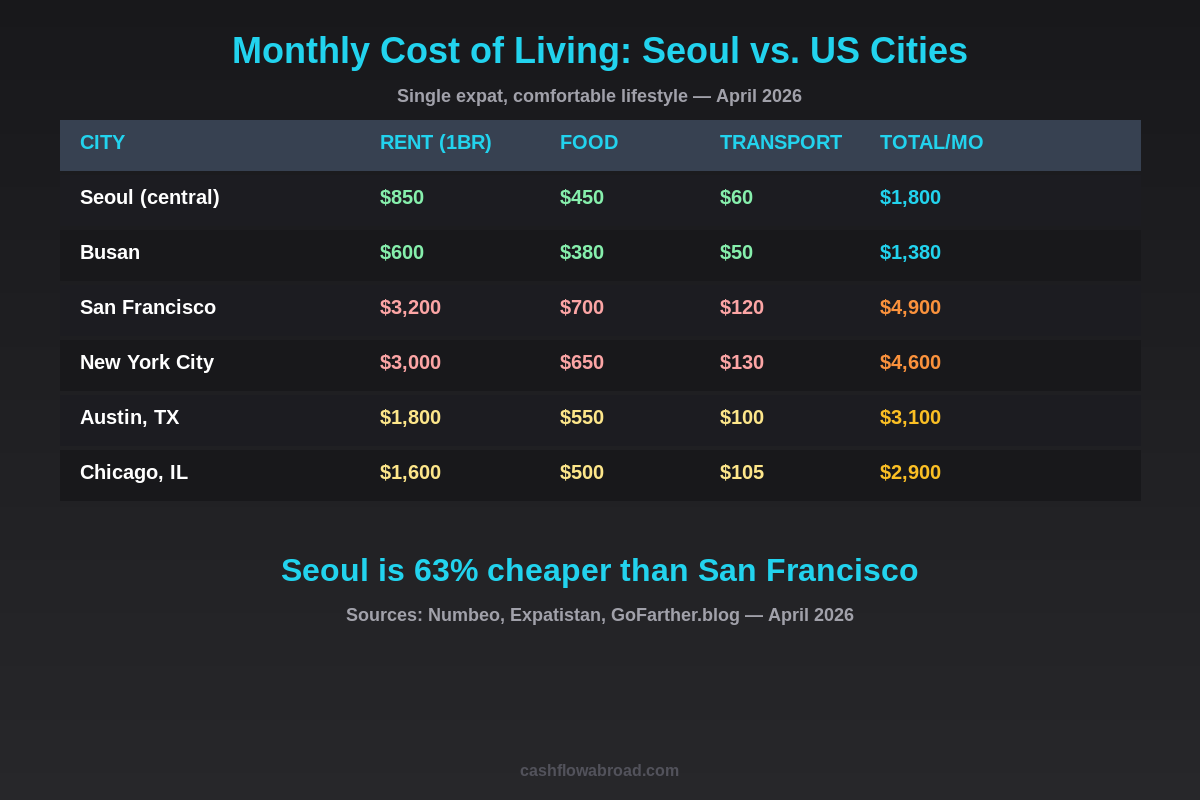

The Real Cost of Living in Seoul (And Why Busan Is Smarter)

Seoul's Gangnam and Apgujeong neighborhoods skew the perception. Yes, you can spend $4,000 a month in Seoul. You can also spend $1,500. The difference is neighborhood choice, not sacrifice.

| Expense | Seoul (central) | Seoul (outer) | Busan |

|---|---|---|---|

| 1BR apartment (monthly rent) | $800–$1,200 | $500–$800 | $400–$650 |

| Local restaurant meal | $6–$9 | $6–$8 | $5–$7 |

| Monthly groceries | $250–$350 | $220–$300 | $200–$280 |

| Subway/transit (monthly) | $50–$75 | $50–$70 | $40–$60 |

| Internet + mobile | $65–$90 | $65–$90 | $60–$85 |

| Coworking space | $100–$200 | $80–$150 | $70–$130 |

| All-in monthly total | ~$1,800 | ~$1,400 | ~$1,200 |

Korea's Jeonse rental system is worth knowing about: instead of monthly rent, you pay a large lump-sum deposit (typically 60–70% of the property value) and live rent-free for the lease term, with the full deposit returned at the end. It's unusual but can work in your favor if you have capital — you're essentially giving the landlord an interest-free loan. Most short-term expats stick to monthly rentals (wolse).

Busan is the city most Korea expats don't consider seriously enough. Korea's second city has ocean views, a thriving food scene, a growing tech community, and costs 20–30% less than central Seoul across every category. The KTX bullet train gets you to Seoul in under three hours for about $25. If you're not tethered to Seoul's specific industry connections, Busan is a compelling base — and its Haeundae and Gwangan Beach neighborhoods have attracted a growing expat cluster.

Banking, Healthcare, and Staying Connected

Banking: Korean banks (Kakao Bank, Kookmin, Shinhan) require a foreigner registration card (ARC), which is issued after 90 days of legal residency. Until you have your ARC, you'll rely on US accounts. The Charles Schwab International Account is the standard recommendation — it refunds all ATM fees worldwide and charges zero foreign transaction fees. Open it before you leave the US.

For moving larger sums between your US accounts and Korean banks, Remitly consistently offers better exchange rates than bank wires with transparent fees on USD-to-KRW transfers.

Maintaining a real US street address matters more than most expats expect — for IRS correspondence, 1099s, brokerage statements, and preserving state domicile. Traveling Mailbox provides a real US street address in 50+ cities, scans your mail on demand, and deposits checks at $15/month. It's covered in depth in the virtual mailbox guide.

Healthcare: Korea's National Health Insurance (NHI) becomes mandatory for foreign residents after six months of legal residence. Premiums are income-based — typically around 7–8% of assessed income, split between employer and employee. Quality of care is genuinely exceptional: Seoul has internationally accredited hospitals with English-speaking staff, short wait times, and costs that are a fraction of US prices. An MRI that costs $3,000 in the US typically runs under $300 in Korea. Before you establish NHI eligibility, SafetyWing covers the gap.

Connectivity: Korea's internet infrastructure is among the world's best — median download speeds of 200+ Mbps are standard in cities. Monthly home internet plans run ₩28,000–₩40,000 ($21–$30). Mobile plans with unlimited data run ₩50,000–₩90,000 ($38–$68). If you're arriving on a short trip or need a backup SIM, Saily eSIM covers South Korea with competitive data pricing and instant activation.

Who Actually Moves to South Korea

The US expat population in Korea falls into fairly distinct groups:

English teachers: The E-2 visa has been placing American graduates in Korean public schools and private academies (hagwons) for decades. Salaries typically run ₩2.0–₩2.8 million per month ($1,500–$2,100), with free housing, round-trip airfare, and pension contributions included. The low cost of living means an English teacher can save $800–$1,200 per month with discipline.

Corporate and military: US military presence at bases like Camp Humphreys, combined with Korean chaebols (Samsung, LG, SK Hynix, Hyundai) regularly recruiting foreign talent for international divisions and semiconductor R&D roles. Compensation packages at this level typically run ₩120–200M+ annually ($90,000–$150,000+), often with housing allowances.

Remote workers and digital nomads: The primary audience for the F-1-D visa. Korea's infrastructure — fast internet, safe streets, excellent food, robust transit — makes it a high-quality base for remote professionals. The $66K income floor filters out early-career freelancers but aligns well with established remote professionals in tech, finance, marketing, or consulting.

Entrepreneurs: Korea's D-8 corporate investment visa requires a ₩100 million ($75,000) investment in a registered Korean company and offers a path to longer-term residence. The Seoul tech startup ecosystem — particularly in Gangnam and the Seongsu "Seoul of Seoul" district — has attracted international founders, supported by government programs like K-Startup Grand Challenge.

US Tax Filing Checklist for Korea-Based Americans

- Form 1040: File annually — worldwide income, no exceptions

- Form 2555 (FEIE): If using the earned income exclusion ($132,900 for 2026)

- Form 1116 (FTC): If claiming credit for Korean taxes paid — typically more valuable than FEIE at incomes above $80K in Korea

- FinCEN 114 (FBAR): If aggregate foreign account balances exceed $10,000 at any point during the year

- Form 8938 (FATCA): If foreign financial assets exceed $200,000 (married filing jointly while abroad)

- Form 8833: Required if claiming treaty-based positions to reduce US tax liability

The Korean tax year is January 1–December 31 (matching the US), and Korean residents must file by May 31 of the following year. Managing both returns simultaneously — plus potentially FBAR — makes February the time to start, not April. The full FBAR and FATCA threshold breakdown is in our US expat banking and taxes guide.

Is South Korea the Right Move?

Korea rewards people who lean into it. The food is extraordinary and cheap. The public transit is faster and cleaner than anything in the US. Crime rates are among the lowest in the world. Healthcare quality is world-class at a fraction of US prices. And the combination of the flat 19% tax election plus the 5-year rule shielding foreign-source income from Korean taxation makes the tax position surprisingly attractive for remote workers earning in dollars.

The friction points are real: Korean is a genuinely difficult language and most government services run in Korean. The cultural expectations around work ethic and social hierarchy can be jarring. The visa is capped at two years, which means Korea works best as a 1–2 year rotation in a broader strategy rather than a permanent base. And the $66K income floor for the F-1-D rules out many early-stage freelancers.

But if you're a US remote professional earning $80K+ who wants to cut your cost of living roughly in half, live in one of the world's most functional cities, eat extraordinarily well, and do it all with solid tax protection and fast infrastructure — South Korea is dramatically underrated.

Financial disclaimer: This post is for informational purposes only and does not constitute tax or legal advice. South Korean and US tax laws change frequently, and individual circumstances vary significantly. Consult a qualified cross-border tax professional before making decisions based on this information. Exchange rates are approximate and subject to change.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJuly 19, 2026

Geographic ArbitrageJuly 19, 2026

Sofia Remote Work Budget Under $2,000

Price rent, transit, utilities, insurance, and visa caveats before using Sofia, Bulgaria as a lower-cost EU base for remote work.

Geographic ArbitrageJune 30, 2026

Geographic ArbitrageJune 30, 2026

Moving Abroad with Kids: School Costs and Family Budget

International school fees change the whole geographic arbitrage math for families. Compare real costs in Medellín, Chiang Mai, Mexico, and Lisbon for

Geographic ArbitrageJune 29, 2026

Geographic ArbitrageJune 29, 2026

Bali for US Expats: Monthly Costs and Permit Guide

How much Bali costs, which Indonesian stay permit suits long-term stays, and what US citizens owe the IRS while living there in 2025.