Singapore for US Expats: Taxes, Visas & the $3K/Month Life

Singapore has no tax treaty with the United States. For most US expats, that sentence triggers immediate alarm. The other pull is practical.

Singapore has no tax treaty with the United States. For most US expats, that sentence triggers immediate alarm. The other pull is practical.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Singapore has no tax treaty with the United States. For most US expats, that sentence triggers immediate alarm. No treaty means no protection, no tie-breakers, no pension carve-outs — just two countries that both think they own your income. And yet, thousands of American professionals are moving to Singapore and paying less total tax than they did in California. Some are paying nothing at all on foreign-earned income. Here's how that works, and whether the math actually makes sense for you.

Why Singapore Keeps Winning the Expat Finance Argument

Singapore's pitch isn't "no tax." It's "rational tax." The city-state has no capital gains tax, no dividend tax for individuals, no inheritance tax, and a top personal income rate of 24% that kicks in only above S$1 million in chargeable income. For comparison, California's top marginal rate alone is 13.3%, before federal taxes touch a dollar.

The numbers that draw high earners: Singapore's effective tax rate on a S$150,000 salary (roughly $112,000 USD) is around 11.5%. In New York, that same income pays a combined federal, state, and city rate above 40%. Singapore isn't a tax haven in the offshore sense — it's a high-functioning, transparent financial center that simply taxes less. That distinction matters enormously if you're a US citizen who still files with the IRS no matter where you live.

The other pull is practical. English is an official language. The legal system is British common law. Banking infrastructure is world-class. A single MRT card handles your entire commute for under $95/month. And Singapore Changi Airport, consistently rated the world's best, puts you within a 7-hour flight of nearly every major Asian business hub.

How Singapore Taxes US Expats (And How the IRS Still Gets Involved)

Singapore taxes residents on Singapore-sourced income only — not worldwide income. If you work remotely for a US client from a Singapore apartment, that income is generally treated as Singapore-sourced and taxed here. If you earn dividends from overseas investments, Singapore doesn't touch them.

The rates for tax residents in 2026:

| Chargeable Income (SGD) | Approximate USD | Tax Rate |

|---|---|---|

| First S$20,000 | ~$15,000 | 0% |

| S$20,001–S$30,000 | ~$22,500 | 2% |

| S$30,001–S$40,000 | ~$30,000 | 3.5% |

| S$40,001–S$80,000 | ~$60,000 | 7–11.5% |

| S$80,001–S$120,000 | ~$90,000 | 15% |

| S$120,001–S$160,000 | ~$120,000 | 18% |

| Above S$320,000 | ~$240,000+ | 22–24% |

You become a Singapore tax resident if you work here for at least 183 days in a calendar year, or if you're on an Employment Pass for the full year. Non-residents pay a flat 15% on employment income (or resident rates, whichever is higher), and 24% on other income types including directors' fees.

The IRS Still Wants Its Cut — Here's the Workaround

US citizens owe a federal return every year, regardless of where they live. Since there's no tax treaty between the US and Singapore, you can't rely on a treaty provision to eliminate double taxation. What you can use:

Foreign Earned Income Exclusion (FEIE): The 2026 exclusion amount is $126,500. If you meet the bona fide residence or physical presence test, your first $126,500 of Singapore-sourced earned income is excluded from US taxable income. For most EP holders earning S$100,000–S$200,000 annually, this eliminates most or all federal tax liability on wages.

Foreign Tax Credit (FTC): Any Singapore income tax you actually pay can be credited dollar-for-dollar against US tax owed on the same income. The FTC is particularly useful for income above the FEIE threshold or for passive income — dividends, rental income, capital gains — that the FEIE doesn't cover. Crucially, because Singapore taxes capital gains at 0%, the FTC doesn't help you there; but neither does it hurt you, since there's no US capital gains tax issue until you actually sell US assets.

One critical wrinkle: if you claim the FEIE, any contributions to a Roth IRA must come from non-excluded income. If your entire salary is excluded, you have no earned income for IRA purposes. The backdoor Roth strategy is worth understanding before you leave.

Singapore Work Visas: Three Paths for US Expats

Employment Pass (EP)

The standard route for professionals with a job offer. Requirements as of 2026:

- Minimum monthly salary: S$5,600 (~$4,200 USD) for most sectors

- Financial services sector: S$6,200 (~$4,650 USD)

- Age adjustments apply — applicants in their late 30s and 40s may need S$10,000–S$12,000/month under the COMPASS points framework

- Employer must demonstrate the role can't be filled locally

- Thresholds increase to S$6,000 / S$6,600 in January 2027

The EP is employer-tied — if you lose your job, you have 60 days to find a new sponsor or leave. It's renewable in 2–3 year increments and is the most common path for multinational employees.

ONE Pass (Overseas Networks & Expertise)

Singapore's premium visa for senior talent, founders, and high-earning specialists. The threshold: a fixed monthly salary of at least S$30,000 (~$22,500 USD) for the 12 months preceding your application, or a comparable offer from an established Singapore company. That's roughly $270,000 USD annually.

The ONE Pass is individual-attached rather than employer-tied — you can switch companies, run a side business, and consult without reapplying. Validity is 5 years. Spouses of ONE Pass holders receive automatic work authorization, a significant advantage for dual-career couples. For senior tech executives and finance professionals, this is the cleanest structure available.

EntrePass (Entrepreneurs)

For founders building a Singapore-registered startup. You'll need funding from an accredited investor or incubator, or demonstrated significant business activity. The bar has risen sharply — this isn't a casual option, but it works well for venture-backed founders who want a Southeast Asian base of operations.

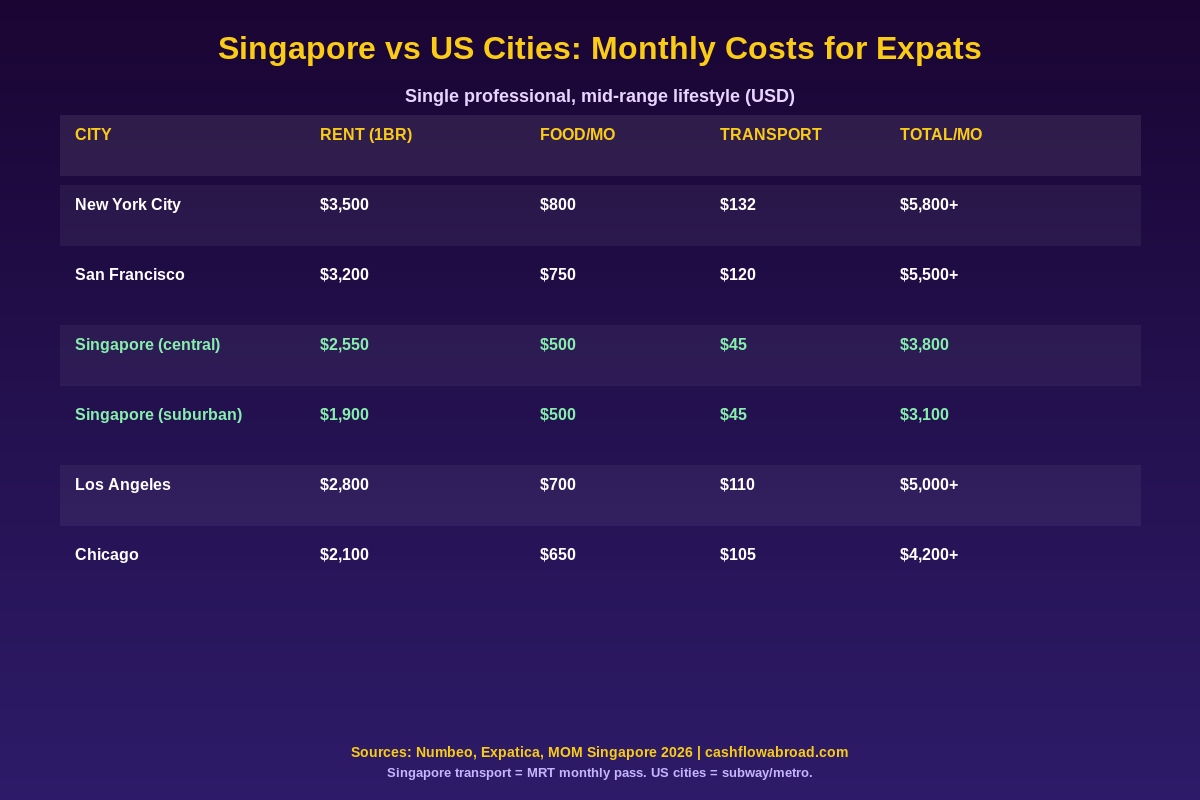

Cost of Living: The Real Numbers

Singapore is expensive. Let's be direct. It's roughly 27% more costly than the US average, and significantly pricier than most Southeast Asian alternatives. But compared to the US cities where most Singapore-bound expats are coming from — New York, San Francisco, Seattle, Chicago — the math looks very different.

The single biggest unlock: transport. Singapore's MRT system is fast, reliable, and covers the entire island. A monthly transit pass costs around S$128 (~$95). Nobody needs a car. In the US, car payments, insurance, and fuel add $800–$1,200/month — a line item that simply disappears in Singapore.

Food is the other counterintuitive win. Hawker centres — government-subsidized open-air food courts found in every neighborhood — serve full meals for S$4–$8 ($3–$6 USD). Chicken rice, laksa, char kway teow — all under $5. Expats who embrace hawker culture rather than exclusively eating at Western restaurants can feed themselves for S$300–$400/month. That figure shocks people coming from Manhattan delivery app bills.

Where Singapore bites: housing and alcohol. A one-bedroom in the central districts (Orchard, River Valley, Tanjong Pagar) runs S$3,000–$4,500/month. Suburban neighborhoods like Jurong, Tampines, or Woodlands bring that to S$1,800–$2,500. Alcohol is heavily taxed — a beer at a bar costs S$12–$18, and a restaurant wine bottle runs double the US price.

What $3,500/Month Gets a Single Expat in Singapore

| Category | SGD/Month | USD/Month |

|---|---|---|

| Rent (1BR suburban) | S$2,200 | ~$1,650 |

| Groceries + hawker food | S$600 | ~$450 |

| Transport (MRT + occasional Grab) | S$200 | ~$150 |

| Utilities + internet | S$150 | ~$115 |

| Entertainment + dining out | S$500 | ~$375 |

| Gym + personal care | S$150 | ~$115 |

| Total | S$3,800 | ~$2,850 |

Comfortable central-district living adds $600–$1,000 in rent. Families with kids at international schools face a different budget tier entirely — most employer-sponsored relocations cover tuition, which runs S$30,000–$60,000 annually per child.

The Lifestyle Reality

Singapore punches above its weight on quality of life. Healthcare is excellent — government polyclinics charge S$15–$50 per visit, while private GPs run S$60–$120. Emergency care is fast and functional. Unlike most Southeast Asian expat destinations, you're not rolling the dice on substandard care when something goes wrong.

Safety is almost a non-issue. Singapore's crime rate is extraordinarily low by any global comparison. Walking anywhere at midnight without concern is a quality-of-life factor that doesn't appear in budget spreadsheets but shapes daily life more than most expenses do.

The tradeoffs are real. The heat and humidity are relentless — 85–90°F year-round, no seasons, guaranteed sweating. The city can feel controlled and small after a year; free speech is restricted, political dissent is essentially absent, and online content faces regulatory oversight. Some expats find the order and efficiency a relief after American chaos. Others find it sterile. Singapore doesn't provide its own energy — you have to bring it.

Banking as a US Expat in Singapore

Opening a local account is straightforward with an EP — DBS, POSB, OCBC, and UOB all accept EP holders with standard documentation. The complication is the US side: most US brokerages and online banks will close accounts or restrict trading when they discover you're abroad.

The solution: Charles Schwab International is built for Americans abroad — no account closures based on foreign address, worldwide ATM fee reimbursement, and transparent currency conversion. For business banking, Mercury works well for expat entrepreneurs maintaining a US entity.

FBAR requirements don't disappear in Singapore. If your Singapore accounts exceed $10,000 combined at any point in the year, you file. FATCA reporting thresholds apply the same as anywhere. Singapore's financial institutions are FATCA-compliant — they're already reporting your accounts to the IRS, so the best move is to file correctly rather than hope for obscurity. The full FBAR/FATCA guide walks through deadlines and thresholds.

A virtual US mailbox is essential. Your brokerage, the IRS, and Social Security need a physical US address, and hotels don't count. Traveling Mailbox ($15/month) gives you a real US street address with mail scanning — it's what keeps your accounts from getting locked the moment your address updates to Singapore.

Healthcare: What US Expats Need to Know

Singapore's public healthcare is excellent, but Employment Pass holders pay "foreigner rates" at restructured hospitals rather than heavily subsidized local rates. A specialist consultation runs S$150–$300, and a 3-day hospital stay might cost S$3,000–$8,000 without coverage.

Most multinational employers include health insurance in EP packages. If yours doesn't, or you're self-employed, SafetyWing's Nomad Health plan covers expats living abroad with solid international coverage — typically $150–$250/month depending on age and tier. For a country with Singapore's care quality, you're getting genuine value for that premium.

Singapore vs. Other Asian Expat Hubs

| City | Income Tax (top rate) | Capital Gains | Monthly Budget | US Treaty? |

|---|---|---|---|---|

| Singapore | 24% | 0% | $3,000–$5,000 | No |

| Hong Kong | 17% | 0% | $3,500–$6,000 | No |

| Dubai, UAE | 0% | 0% | $3,000–$6,000 | No |

| Bali, Indonesia | 30% (residents) | Variable | $1,200–$2,500 | No |

| Bangkok, Thailand | 35% (residents) | Taxable remitted | $1,500–$3,000 | Yes |

Dubai is the only hub that fully beats Singapore on tax — 0% income tax — at comparable cost. Hong Kong has lower top rates but political uncertainty has reshaped expat flows substantially since 2020. Bangkok is significantly cheaper but Thailand's 2024 change to tax remitted foreign income has complicated the math for remote workers and investors. Singapore's rule of law and financial infrastructure make it the safe institutional choice in Asia for anyone managing serious assets or building an international career.

For US expats specifically: the lack of a tax treaty matters less than most people fear once you run the FEIE and FTC numbers. If you want to explore lower-cost alternatives across different risk profiles, the geographic arbitrage playbook maps out 10 countries at different price points.

Bottom Line

Singapore makes sense for a specific type of US expat: a high-earning professional, typically with an employer-sponsored package, who values stability, safety, and access to Asian business networks over maximum tax savings or low cost of living. It's not the cheapest move in Asia — not close. It's not a tax haven. But it offers something rarer: a financial environment that actually works for Americans, with 0% capital gains, low effective income tax rates, and infrastructure you can trust.

The no-treaty situation is real but manageable. FEIE covers the first $126,500 of earned income; FTC handles the rest. The bigger risk for most expats isn't double taxation — it's forgetting to cut state tax ties before leaving, or losing access to US banking because they didn't set up a virtual mailbox first. Get those right, and Singapore becomes one of the most financially coherent expat destinations in the world.

Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. US expat tax obligations are complex and individual circumstances vary significantly — consult a qualified international tax professional before making decisions. All figures are approximate, based on publicly available 2026 data, and subject to change as Singapore updates its tax and immigration policies.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJuly 19, 2026

Geographic ArbitrageJuly 19, 2026

Sofia Remote Work Budget Under $2,000

Price rent, transit, utilities, insurance, and visa caveats before using Sofia, Bulgaria as a lower-cost EU base for remote work.

Geographic ArbitrageJune 30, 2026

Geographic ArbitrageJune 30, 2026

Moving Abroad with Kids: School Costs and Family Budget

International school fees change the whole geographic arbitrage math for families. Compare real costs in Medellín, Chiang Mai, Mexico, and Lisbon for

Geographic ArbitrageJune 29, 2026

Geographic ArbitrageJune 29, 2026

Bali for US Expats: Monthly Costs and Permit Guide

How much Bali costs, which Indonesian stay permit suits long-term stays, and what US citizens owe the IRS while living there in 2025.