Renting Your US Home While Abroad: The Capital Gains Trap

Renting your US home before selling while living abroad can cost married couples $30,000–$100,000 in taxes that would have been completely free. Here's the Section 121 math.

Renting your US home before selling while living abroad can cost $30,000–$100,000 in taxes. Learn the Section 121 trap and how to avoid it.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Here's a number that should stop any expat homeowner cold: a married couple who rents their US home for just three years before selling could lose $112,500 in gains that would have been completely tax-free — plus owe $8,727 in depreciation recapture they never anticipated. Throw in the 3.8% Net Investment Income Tax for high earners, and the bill easily clears $30,000. Every dollar of it avoidable with different timing.

This is the Section 121 capital gains trap — and it silently catches thousands of expats who assumed renting their home before eventually selling was the obvious, rational move.

The Section 121 Exclusion: Your Biggest Tax Break Runs on a Timer

Under IRC Section 121, US homeowners can exclude up to $250,000 (single filers) or $500,000 (married filing jointly) of capital gain when they sell their primary residence. For anyone who bought in a major metro area in the last decade, this is almost certainly the single most valuable tax break they will ever receive in their lifetime.

The qualifying test reads simply: you must have owned and used the home as your principal residence for at least 2 of the last 5 years before the sale date. But for expats who plan to rent the home before eventually selling, that "5 years" creates a clock that most people don't realize is already ticking.

A few Section 121 rules that matter specifically for expats:

- The 2-year residency requirement does not need to be consecutive — gaps are allowed

- Active military and certain foreign service personnel get a 10-year lookback window — civilian expats do not

- The exclusion can be used once every 24 months

- Depreciation claimed during any rental period is never covered by the exclusion — that tax is always due

How the Five-Year Clock Works When You Move Abroad

The day you move out of your US home, the five-year window starts running. Your two years of primary residence start to age out of that window. Here's how the math plays out:

- Move out, sell within 3 years: Your 2 years of prior primary use are still inside the 5-year window. You qualify for the exclusion — subject to the non-qualified use calculation (see below).

- Move out, sell between 3 and 5 years out: You may still technically qualify (if you lived there 2 full years before leaving), but the non-qualified use rules reduce your exclusion proportionally for every year the home was rented.

- Move out, sell after 5+ years: Your 2 years of primary use have aged out of the lookback window entirely. The exclusion is zero. 100% of the gain is taxable at long-term capital gains rates.

That hard cutoff — 5 years after you moved out — is the point of no return. Expats who bought into the idea of "I'll sell eventually when it makes sense" and let years slip by discover too late that they lost the exclusion entirely.

The Non-Qualified Use Rule: How Renting Shrinks Your Exclusion

Even if you sell within the 5-year window, Congress added a second trap in 2009: the non-qualified use rule under IRC Section 121(b)(5).

Any period during which your home was used as a rental after January 1, 2009, and after you moved out is defined as "non-qualified use." The IRS then calculates what portion of your total gain is excludable on a straight pro-rata basis:

Excluded Gain = Total Gain × (Qualified Use Period ÷ Total Ownership Period)

The non-qualified fraction of the gain cannot be excluded and is fully taxable as long-term capital gains.

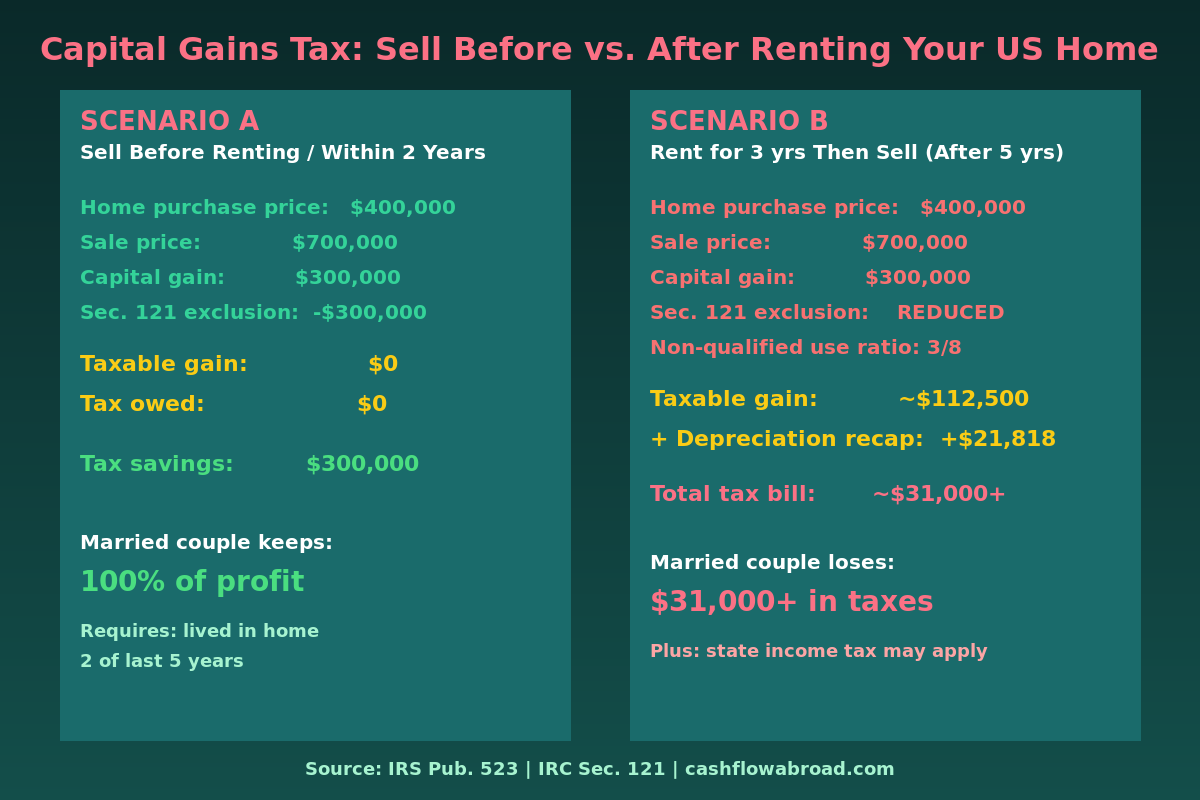

Worked example: You owned the home for 8 years total. You lived in it as your primary residence for 5 years, then moved abroad and rented it for 3 years, then sold.

- Total ownership: 8 years

- Rental period (non-qualified use): 3 years = 37.5% of ownership

- If total gain = $300,000 → non-qualified gain = $112,500 (fully taxable)

- Excludable gain = $187,500 (covered by Section 121)

On $112,500 of taxable gain at the 15% federal LTCG rate, a married couple owes $16,875 federal. In California (13.3%), add $14,962 state. Total: over $31,000 in taxes on a gain that would have been completely shielded if they'd sold before leaving.

The Depreciation Recapture: Another Tax Nobody Warned You About

Even after applying whatever Section 121 exclusion you have left, there's a second tax embedded in every year you rented: depreciation recapture under Section 1250.

When your home becomes a rental, you're required to depreciate it over 27.5 years using straight-line method. The depreciable basis is typically the lesser of your original cost basis or fair market value at conversion — usually 80% of purchase price to account for land, which isn't depreciated.

The IRS recaptures all depreciation you claimed (or that you were required to claim but didn't) at a flat 25% maximum rate when you sell. Section 121 explicitly does not shield depreciation recapture from taxation — that provision is carved out in the statute.

| Rental Duration | Annual Depreciation | Total Depreciation | Recapture Tax (25%) |

|---|---|---|---|

| 1 year | $11,636 | $11,636 | $2,909 |

| 2 years | $11,636 | $23,272 | $5,818 |

| 3 years | $11,636 | $34,909 | $8,727 |

| 4 years | $11,636 | $46,545 | $11,636 |

Basis: $400,000 purchase × 80% building value = $320,000 depreciable basis ÷ 27.5 years = $11,636/year.

One critical trap: if you decide to skip claiming depreciation to avoid the recapture later, it doesn't work. The IRS applies recapture to depreciation "allowed or allowable" — meaning they compute it as if you took the deduction whether you did or not. Skip the deduction, owe the same recapture anyway. Always take the depreciation.

What Rental Income Costs You While You're Abroad

Beyond the eventual sale, each year you rent the property creates annual filing requirements and potential tax exposure while you're living abroad. Three points that consistently surprise expats:

Rental Income Is Immune to the FEIE

The Foreign Earned Income Exclusion is powerful — up to $132,900 in 2026 of earned income excluded from US taxation. But rental income from a US property is passive income, not earned income from services you performed. It sits entirely outside the FEIE's reach. You'll report it on Schedule E, net out deductions (mortgage interest, property taxes, insurance, repairs, management fees, depreciation), and any remaining profit is taxable at ordinary income rates.

The $25,000 Passive Activity Loss Phase-Out

If your rental generates a tax loss after depreciation (common in the early years), you may deduct up to $25,000 against ordinary income — but only with active participation in management and a Modified Adjusted Gross Income under $100,000. The deduction phases out completely at $150,000 MAGI.

Many expats — remote tech workers, consultants, business owners — sit above the $150,000 threshold. Their rental losses become suspended passive activity losses (PALs) that carry forward. The silver lining: suspended PALs release fully in the year of sale, potentially creating a significant deduction to offset capital gains at that time.

The 3.8% NIIT for High Earners

If your MAGI exceeds $200,000 (single) or $250,000 (married), net rental income is subject to the 3.8% Net Investment Income Tax on top of regular income tax. On $30,000 of net rental profit, that's an additional $1,140 per year that many expats don't budget for. We cover this tax in depth in our guide to NIIT and expat investors.

The Full Cost Comparison: Sell Before vs. Rent Then Sell

| Scenario (married couple) | Total Gain | Taxable Portion | Est. Federal Tax | Depreciation Recapture |

|---|---|---|---|---|

| Sell before leaving | $300,000 | $0 | $0 | $0 |

| Rent 1 yr, sell within 5 yrs | $300,000 | ~$37,500 | ~$5,625 | $2,909 |

| Rent 3 yrs, sell within 5 yrs | $300,000 | ~$112,500 | ~$16,875 | $8,727 |

| Rent 3 yrs, sell after 5 yrs (no exclusion) | $300,000 | $300,000 | ~$45,000 | $8,727 |

Estimates assume 15% federal LTCG rate. State taxes, NIIT (3.8%), and individual circumstances vary. Consult a tax professional for your situation.

The practical implication is stark: for a married couple with $300,000+ in appreciation, selling before leaving costs nothing in federal capital gains tax. Renting for three years then selling within the window costs roughly $25,000 all-in. Waiting past the five-year window transforms a tax-free event into a $50,000+ obligation.

Strategies for Expats Already Renting Their US Home

If you're already living abroad with your US home rented out, the window hasn't necessarily closed — but you need to manage it actively.

Track the 5-year deadline precisely. Know the exact date your window closes. Put it in your calendar 18 months, 12 months, and 6 months out as decision checkpoints. Most expats miss the deadline by drifting, not by deciding.

Consider temporarily re-establishing residency. If you have substantial appreciation and the 5-year window is approaching, returning to your US home and genuinely living there for 24 months resets the qualifying use clock. You'd then qualify for a fresh Section 121 exclusion. The IRS looks at actual habitation — you need utility bills, mail delivery, and evidence of primary residence, not just a forwarding address.

Model the 1031 exchange option. If you've formally converted the home to investment property (fully rented, no personal use), a 1031 like-kind exchange can defer all capital gains and depreciation recapture into a new investment property. Your gain carries forward rather than disappearing, but you also keep compounding without the tax drag. This is particularly useful for expats with large gains who intend to keep owning real estate.

Harvest suspended PALs at sale. Every year of losses you couldn't deduct due to the income phase-out becomes available at sale. If you've accumulated $50,000 in suspended PALs, those offset your capital gain in the year you sell — reducing your net taxable gain by that amount. Model this into your sale-year tax projection.

Don't skip depreciation. As noted above, the IRS recaptures depreciation "allowed or allowable" regardless of whether you claimed it. Always take the depreciation deduction and let it reduce your rental income. The recapture tax at sale is the same either way.

Annual Reporting Requirements You Can't Ignore

Renting your US home while abroad creates filing obligations beyond the standard Form 1040 that many expats miss:

- Schedule E: Annual rental income and expenses

- Form 4562: Depreciation claimed on the property each year

- Form 8960: Net Investment Income Tax calculation (if MAGI thresholds are met)

- Form 4797: If fully converted to investment property, gains on sale may route through this form before Schedule D

- State tax returns: Many states tax rental income from state-located property regardless of where you live — your state of property location likely has a filing requirement

If you're using a property management company, they'll issue a 1099 for gross rents received. That income shows up on Schedule E whether or not you've filed a change of address with anyone.

Managing the Administrative Reality of a US Rental from Abroad

Beyond tax calculations, being a long-distance landlord requires functional US-based infrastructure that many expats don't set up properly before they leave.

You'll need a real US mailing address for IRS notices, insurance documents, mortgage servicer correspondence, and property management reports. A virtual mailbox service like Traveling Mailbox provides a real US street address in 50+ cities with mail scanning and check deposit — the difference between catching a time-sensitive IRS notice and missing it entirely. At $15/month, it's the cheapest line item in your expat admin stack. We cover the full setup in our virtual mailbox guide for expats.

You'll also need a US bank account to receive rental deposits and pay property expenses. Charles Schwab International is the benchmark account for US citizens abroad — no monthly fees, free global ATM withdrawals, and it won't close your account because you changed your address to Spain or Colombia. Many other US banks will. For the complete breakdown of expat-friendly banking options, see our US expat banking guide.

The Core Decision: Sell Before You Leave or Rent First?

The right answer depends on three variables: your total appreciation, how long you plan to be abroad, and your certainty about eventually returning.

If your gain is modest (under $50,000), the tax exposure from renting a few years is relatively small and the rental income may genuinely outweigh it. If you're sitting on $200,000–$500,000 in appreciation and you qualify for the married exclusion, selling before you leave is often the superior financial move — especially if you're uncertain about your timeline abroad.

The mental math most expats do: "The home is worth $X, and if I sell I'll get $Y after the mortgage. But I can rent it for $Z per month while I'm gone." What the math doesn't include: the tax clock, the shrinking exclusion, the recapture liability building annually, and the administrative cost of managing a property from 6,000 miles away.

Run the full numbers — including the Section 121 phase-down at sale — before assuming the rental income wins.

The Bottom Line

The Section 121 exclusion is the most valuable tax break most Americans ever qualify for. For a married couple who bought in 2015 in any major US metro, that exclusion could represent $200,000–$500,000 in tax-free gain — a figure large enough to change retirement math entirely.

Renting the property before selling doesn't eliminate that exclusion, but it erodes it every year through the non-qualified use calculation. Add depreciation recapture, passive activity loss phase-outs, and NIIT, and the true cost of "just renting until we decide" can easily reach $40,000–$100,000 for high-appreciation properties.

If you're planning to move abroad and own a home, get a qualified CPA who specializes in US expat taxation to model the sell-now vs. rent-then-sell scenarios with your actual numbers before you book the flight. The tax decision is irreversible once you've been abroad for years with a rented home. Make it intentionally.

Financial Disclaimer: This article is for educational and informational purposes only and does not constitute tax, legal, or financial advice. Tax laws are subject to change and individual circumstances vary significantly. The examples provided are illustrative estimates. Consult a qualified CPA or enrolled agent with expertise in US expat taxation before making any decisions about your property. Relevant IRS authority: IRC Section 121, IRS Publication 523, Revenue Ruling 2002-83.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJune 13, 2026

Expat Tax & FinanceJune 13, 2026

Section 121 Exclusion: Selling Your US Home as an Expat

Move abroad and a 3-year clock starts on your $250K–$500K Section 121 exclusion. Learn the deadline, depreciation recapture, and how not to lose it.

Expat Tax & FinanceJune 2, 2026

Expat Tax & FinanceJune 2, 2026

Foreign Rental Income: US Tax Guide for Expat Landlords

Own rental property abroad? US expats owe Schedule E reporting, 30-year ADS depreciation, Form 1116 foreign tax credit, and 3.8% NIIT. Complete guide.

Investing & Wealth BuildingJune 26, 2026

Investing & Wealth BuildingJune 26, 2026

Options Trading for US Expats: Tax Rules and Traps

Section 1256 contracts cap US expat options traders at a 26.8% blended rate. Understand wash sales, NIIT traps, mark-to-market, and Form 6781 rules.