The W-2 Abroad Tax Trap Most Remote Workers Never See Coming

FEIE zeros your federal income tax — but not FICA. A $120K W-2 employee abroad still owes $9,180/yr in payroll taxes FEIE cannot touch. Here's the full breakdown.

FEIE eliminates federal income tax but not FICA. A $120K W-2 employee abroad still pays $9,180/yr in payroll taxes. Here are the real fixes.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

You did everything right. You claimed the Foreign Earned Income Exclusion, moved abroad, and reduced your federal income tax bill to near zero on your first $126,500 of salary. Then you looked at your W-2 in January and found the IRS had still taken $9,180 from you — money that FEIE absolutely cannot touch. Welcome to the W-2 abroad tax trap, and you are far from alone.

Millions of US workers relocated internationally after 2020. Most focused on eliminating federal income tax and stopped there. But a W-2 employee who lives abroad still owes FICA payroll taxes, can get haunted by state income tax withholding on their old address, and may be accidentally creating a corporate tax problem for their employer in whatever country they live in. None of this appears in the standard "how to pay zero taxes as an expat" explainers.

What FEIE Actually Covers — And What It Doesn't

The Foreign Earned Income Exclusion lets qualifying US citizens and permanent residents exclude up to $126,500 (2024) in foreign-earned income from their federal taxable income. If you pass the bona fide residence test or physical presence test (330 days outside the US in a 12-month period), you can knock out your federal income tax liability almost entirely on that first $126,500.

What FEIE does NOT cover:

- FICA (Social Security and Medicare payroll taxes) — zero exemption, regardless of where you live

- State income taxes — FEIE is a federal mechanism; states set their own rules

- Net Investment Income Tax (NIIT) — the 3.8% surcharge on passive income has a separate trap entirely

- Self-employment tax — covered under a different mechanism

The gap that catches W-2 employees off guard is always FICA. It's not income tax — it's a payroll tax — and FEIE doesn't touch it.

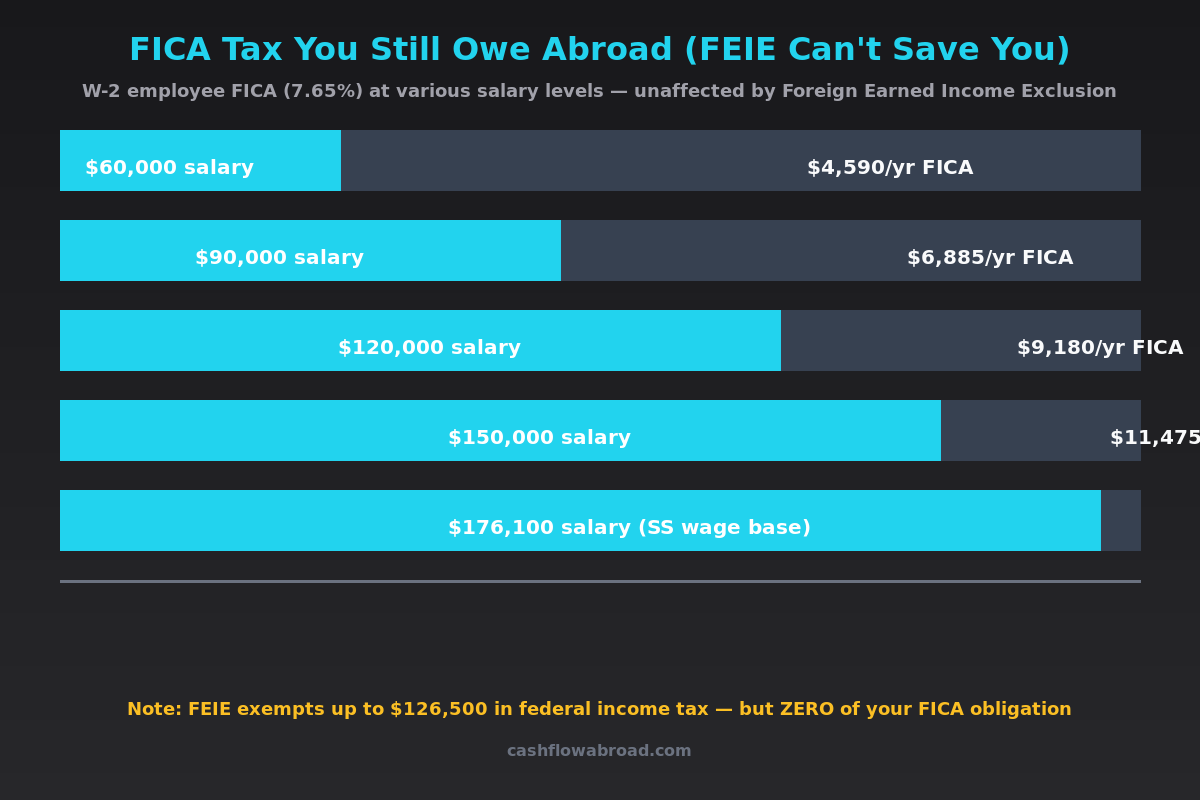

The FICA Problem: $9,000/Year That FEIE Can't Touch

FICA stands for Federal Insurance Contributions Act. It funds Social Security (6.2%) and Medicare (1.45%), totaling 7.65% on your side. Your employer matches another 7.65%. Both sides pay regardless of whether you live in Dallas or Da Nang.

The Social Security component applies to earnings up to $176,100 in 2025 (the SS wage base). Medicare has no cap. On salaries above $200,000 (individual), an additional 0.9% Additional Medicare Tax kicks in.

| Annual Salary | Employee FICA (7.65%) | Employer FICA Match | Total FICA Cost | Federal Income Tax After FEIE (est.) |

|---|---|---|---|---|

| $60,000 | $4,590 | $4,590 | $9,180 | ~$0 |

| $90,000 | $6,885 | $6,885 | $13,770 | ~$0 |

| $120,000 | $9,180 | $9,180 | $18,360 | ~$0 |

| $150,000 | $11,475 | $11,475 | $22,950 | ~$1,800 on income above $126,500 |

| $176,100 (SS wage base) | $13,472 | $13,472 | $26,944 | ~$5,200 on income above $126,500 |

The person earning $120,000 who celebrates a near-zero federal income tax bill is still paying $9,180 out of pocket in FICA. Their employer is paying another $9,180 on their behalf — a cost that factors into compensation negotiations and remote work policy decisions. That $18,360 combined cost is real money leaving the table every year.

The only real escape from FICA as a US worker is to stop being a US W-2 employee. More on that below.

The State Tax Ghost: Withholding That Follows You Abroad

Your employer's payroll system withholds state income tax based on the address on your W-4. If that address is California when you move to Chiang Mai, your employer keeps withholding California state income tax at rates up to 13.3% — even if you haven't set foot in California in two years.

You'll get it back — but only if you file a California nonresident return and claim a refund. Most people don't know to do this. Some just let it ride, effectively overpaying by thousands every year. Others stop filing state returns entirely, which can trigger an audit.

California and New York are the two most aggressive states for pursuing tax residency claims on departed residents. California's Franchise Tax Board uses a 19-factor domicile test, and physical absence alone is not enough to terminate residency. State taxes follow US expats in ways most people don't expect — and the W-4 issue is the most immediate version.

The fix on the withholding side: update your W-4 to remove the state withholding entry, or update your address to reflect a state with no income tax (Alaska, Florida, Nevada, South Dakota, Texas, Washington, Wyoming). For California and New York specifically, get a tax attorney involved — those states will audit the domicile change aggressively.

Form 673: The Fix That Doesn't Fix the Big Problem

IRS Form 673 is titled "Statement for Claiming Exemption from Withholding on Foreign Earned Income Eligible for the Exclusion Provided by Section 911." You file it directly with your employer (not with the IRS), and it instructs them to stop withholding federal income tax on wages you expect to exclude via FEIE.

This is genuinely useful. Without Form 673, your employer withholds federal income tax all year and you have to wait until tax season to get the refund. With Form 673, your cash flow improves immediately — you're not lending the IRS an interest-free loan for 12 months.

What Form 673 does not do:

- Stop FICA withholding — Social Security and Medicare continue regardless

- Stop state income tax withholding — that requires a W-4 update

- Automatically qualify you for FEIE — you still need to pass the bona fide residence or physical presence test when you file

- Protect you if you return to the US mid-year — if you don't qualify for FEIE after all, you'll owe the taxes that weren't withheld, plus potential underpayment penalties

Many US employers — especially mid-size companies without international HR experience — don't know what Form 673 is. HR departments regularly reject it or escalate it to legal counsel who sit on it for months. If your employer won't accept it, your only option is the standard route: withhold through the year, file a 1040 with the FEIE claim, get the refund in spring.

One practical caution: if you expect to spend more than 35 days in the US in a calendar year, don't use Form 673 for that year. Failing the physical presence test while having stopped withholding creates a painful reconciliation at tax time.

Your Employer's Hidden Problem: Permanent Establishment Risk

Here's the dimension of this issue that affects you even if your personal tax situation is perfectly arranged. When you work as a W-2 employee for a US company while physically in another country, you may be creating a taxable presence — a "permanent establishment" or PE — for your employer in that country.

Permanent establishment doctrine allows host countries to tax foreign companies on income attributable to business activities conducted there. An employee routinely doing substantive work from a country where the company has no legal entity can trigger PE status. The company then owes corporate income tax in that country on the PE's income — potentially years' worth retroactively, with penalties.

This is not theoretical. Germany, France, the Netherlands, Australia, and Canada have active PE enforcement programs. The risk is highest when:

- The employee is in a senior or client-facing role

- The employee interacts with local customers or vendors

- The arrangement is indefinite rather than a temporary assignment

- The host country has no tax treaty PE exception with the US

This is why many US companies have blanket policies against unauthorized remote work abroad even for fully remote roles. They're not trying to stop you from living abroad — they're protecting themselves from inadvertent corporate tax liability in a foreign jurisdiction. If your employer is unaware of this risk, it's worth a conversation with HR. Get their approval in writing before you move.

Totalization Agreements: A Partial Escape Hatch

The US has bilateral totalization agreements with 30 countries including Germany, the UK, France, Italy, Japan, South Korea, Australia, and Canada. These agreements prevent dual Social Security taxation — in theory, you pay into one country's system, not both.

For W-2 employees of US employers, totalization agreements generally do not provide an escape from FICA unless one of these applies:

- Your US employer sends you abroad on a documented temporary assignment (typically under 5 years) and obtains a Certificate of Coverage from the SSA — you continue paying US Social Security, exempt from the host country's system

- You transition to employment by a foreign entity — you may pay into the host country's social insurance system instead of FICA

Most expat employees working abroad indefinitely for a US employer with no foreign entity structure don't get relief from totalization. Countries with aggressive social contribution enforcement: France (CSG/CRDS at ~9.7% on earned income), Germany (up to 20% employee-side social insurance), Netherlands (approximately 27.65% combined). Without a formal foreign employment structure, you can end up paying both US FICA and host-country contributions — the exact dual taxation scenario totalization is supposed to prevent.

Three Real Fixes — Ranked by Simplicity

Fix 1: Employer of Record / PEO Structure

A Professional Employer Organization (PEO) or Employer of Record (EOR) like Deel, Remote.com, or Papaya Global acts as your legal employer in the country where you live. Your US company pays the PEO; the PEO handles local payroll, benefits, and compliance. You become an employee of a foreign entity.

This eliminates US FICA (you pay the host country's social contributions instead — often lower), eliminates the PE risk for your US employer, and handles local employment law automatically. Cost: $400–$600 per month typically charged to your employer.

The trade-off: you lose access to US employer-sponsored benefits that require W-2 status — 401k plans, certain stock option structures, some US health insurance. You'll need separate solutions. For investing, Charles Schwab International stays open to US citizens abroad and offers free worldwide ATM access. For health coverage, SafetyWing offers nomad plans starting around $56/month that function regardless of employment structure.

Fix 2: Convert to 1099 Contractor Status

If your US employer converts your arrangement to an independent contractor (1099) relationship, you step off the FICA treadmill — but onto a different one. Self-employed individuals pay self-employment tax at 15.3% on net income (the combined employee + employer FICA rate). The offset: you can deduct the employer-equivalent half of SE tax, contribute up to $69,000 annually to a Solo 401k, and deduct legitimate business expenses before SE tax applies.

For banking, Mercury works well for US-based contractors operating abroad — no fees, clean API integrations, and built for companies and freelancers who transact internationally.

Fix 3: Employer Establishes a Foreign Subsidiary

The cleanest long-term solution: the US company establishes a local entity in the country where you live. You become a local employee paid in local payroll, fully subject to local employment law. The US parent is completely insulated from PE exposure. Cost: $2,000–$25,000+ to establish depending on jurisdiction, plus ongoing compliance. Makes sense for multiple employees in the same country or long-term strategic expansion, not for a single employee working abroad for a year.

Practical Checklist for W-2 Employees Moving Abroad

| Action | Timing | Impact |

|---|---|---|

| Update W-4 to remove state withholding for departed state | Before first paycheck abroad | Stops over-withholding of state tax immediately |

| File Form 673 with employer | Once you qualify for FEIE (after 330 days) | Stops federal income tax withholding; improves cash flow |

| Get employer HR approval; document the arrangement in writing | Before moving | PE risk protection; employment law compliance |

| Set up a US virtual mailbox | Before departure | Maintains US address for banking, IRS, state domicile purposes |

| Discuss PEO/EOR options if staying abroad more than 1 year | 6+ months into arrangement | Eliminates FICA; permanently resolves PE risk |

| Work with an expat CPA for year-one filing | Year 1 — mandatory | Correct FEIE election, state refund claims, FICA reconciliation |

On the virtual mailbox point: US banks, brokerages like Charles Schwab, and the IRS all need a valid US address on file. Traveling Mailbox gives you a real US street address in 50+ cities, scans and forwards mail digitally, and handles check deposits for around $15/month. It's the cleanest way to maintain a US presence your finances require without complications. See our full virtual mailbox guide for expats.

For the tax filing itself — FEIE election, state returns, foreign-earned income sourcing — our expat banking and taxes guide covers the structural pieces. If you're weighing FEIE against the Foreign Tax Credit as a strategy, our FEIE vs. Foreign Tax Credit breakdown walks through when each makes more sense.

The Bottom Line

The dream of working remotely abroad while paying near-zero taxes is real — but the full picture is more complicated than the FEIE headline. A US W-2 employee earning $120,000 abroad who has perfectly executed FEIE is still paying $9,180 per year in FICA, potentially thousands more in state tax if the W-4 isn't updated, and may be creating an undisclosed corporate tax exposure for their employer. None of this is catastrophic. All of it is solvable. But solving it requires knowing the problems exist — which is exactly where most expat tax content fails people.

Update your W-4 this week. File Form 673 once you qualify. Schedule a consultation with an expat CPA before your first full tax year abroad. The $300–$500 that conversation costs will return itself many times over.

Financial disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and vary by individual circumstance. Consult a qualified expat tax professional — ideally one specializing in US citizens abroad — before making any decisions about FEIE elections, FICA planning, state tax domicile, or international employment structures.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 29, 2026

Expat Tax & FinanceJuly 29, 2026

Form 4868 vs 2350 for Expats

Compare Form 4868 and Form 2350 for expats, choose the right extension, and protect cash flow before claiming Form 2555.

Expat Tax & FinanceJuly 28, 2026

Expat Tax & FinanceJuly 28, 2026

US Mortgage as an Expat: Document Checklist

Prepare the income, asset, credit, translation, and closing documents lenders ask for when expats apply for a U.S. mortgage.

Expat Tax & FinanceJuly 27, 2026

Expat Tax & FinanceJuly 27, 2026

EU VAT for US Ecommerce Sellers

Learn when U.S. ecommerce sellers need EU VAT, OSS, or IOSS, and fix checkout rules before taxes erase profit margins overseas.