Puerto Rico Act 60: Legal 0% Capital Gains Tax

Puerto Rico Act 60 lets US citizens pay 0% on capital gains, dividends, and interest — legally, without renouncing citizenship. Here's the full breakdown.

Act 60 lets US citizens legally pay 0% on capital gains & dividends in Puerto Rico. Full requirements, costs, IRS risks & 2026 deadline explained.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

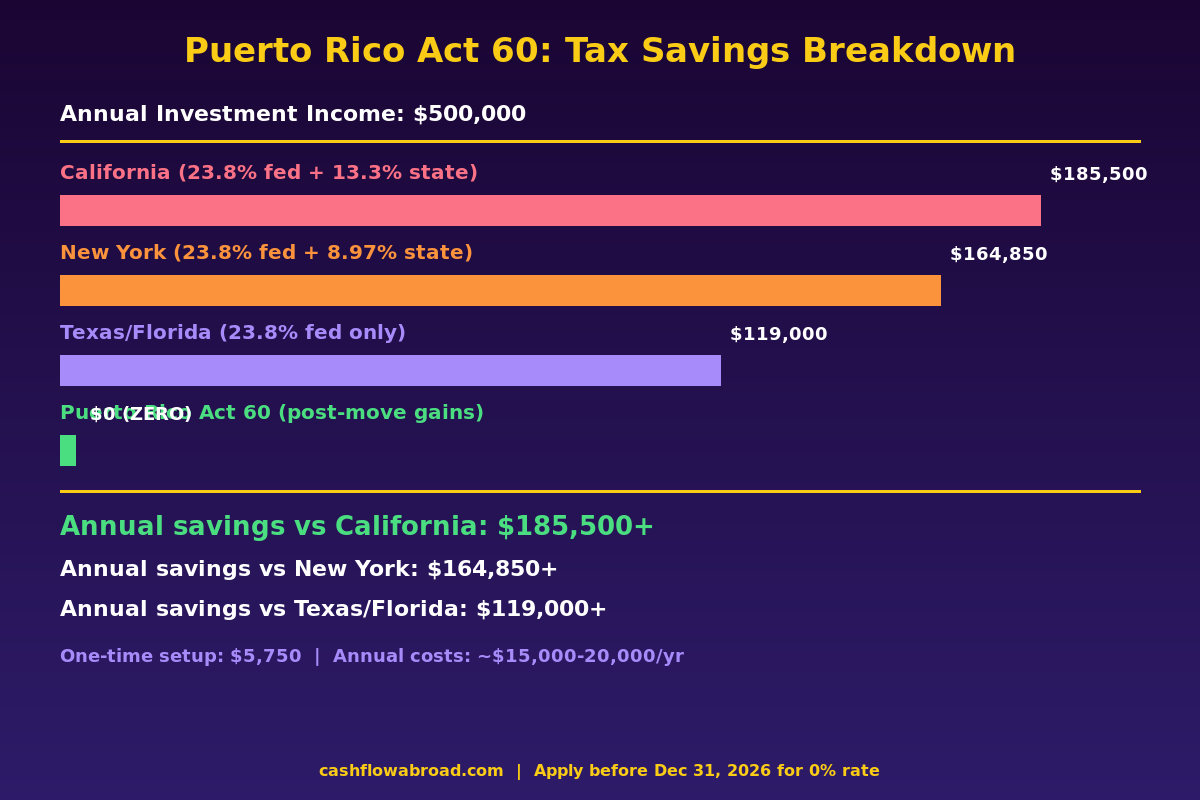

A California-based investor with $500,000 in annual capital gains writes a check to the IRS for $185,500 every April. An identical investor who moved to San Juan two years ago writes a check for $0. Same citizenship, same assets, same gains — different zip code. That's not a loophole. It's a congressional statutory arrangement baked into U.S. tax law since 1954, turbo-charged by Puerto Rico's Act 60 in 2019.

This guide covers exactly who qualifies, what the real costs are, where the IRS is hunting, and why the window to lock in the 0% rate closes on December 31, 2026.

What Is Puerto Rico Act 60?

Act 60-2019 is Puerto Rico's omnibus tax incentives code, signed into law by Governor Rosselló on July 1, 2019. It consolidated dozens of prior incentive programs — most importantly Act 20 (Export Services) and Act 22 (Individual Investors) — into a single statute that took effect January 1, 2020.

The two chapters most relevant to U.S. expats and investors are:

- Chapter 2 — Individual Resident Investor: For high-net-worth individuals who physically relocate. Benefits: 0% tax on capital gains, dividends, and interest that accrue after you establish residency.

- Chapter 3 — Export Services: For businesses that perform services in Puerto Rico for clients outside the territory. Benefit: 4% corporate tax rate on eligible export income, vs. up to 37% federally.

The legal foundation is IRC §933, which excludes Puerto Rico-source income from U.S. federal taxation for bona fide Puerto Rico residents. This isn't a gray-area strategy — it's the same statute that has governed Puerto Rico's tax relationship with Washington since Eisenhower was president. Act 60 simply layers territorial exemptions on top of it.

In March 2026, Puerto Rico enacted Act 38-2026, extending the entire program through 2055 — but with a critical split: applicants who file before December 31, 2026 lock in the 0% rate through at least 2035. Applicants who wait until January 1, 2027 or later will face a new 4% preferential rate instead of 0%.

The Tax Math — What You Actually Save

For someone with significant investment income, the savings are not incremental. They're categorical.

| State of Residence | Federal Rate | State Rate | Tax on $500K Gains |

|---|---|---|---|

| California | 23.8% (20% + 3.8% NIIT) | 13.3% | $185,500 |

| New York City | 23.8% | 8.97% state + ~3.88% city | $183,250 |

| Texas / Florida | 23.8% | 0% | $119,000 |

| Puerto Rico — Act 60 (post-move gains) | 0% | 0% | $0 |

Even compared to zero-income-tax states like Texas and Florida, Act 60 saves $119,000 per year on $500,000 of gains. Against California, that jumps to $185,500 annually. Crypto traders with a single large liquidation event can save seven figures on one transaction.

Net the compliance overhead (~$15,000–$20,000/year in fees, annual report, and charitable donation), and the math still overwhelmingly favors anyone with $300,000+ in annual investment income.

The Critical Caveat: Pre-Move Gains Are Not Exempt

This is the single most misunderstood aspect of Act 60, and the detail that has triggered the most IRS enforcement actions.

The 0% rate applies only to appreciation that accrues after you become a bona fide Puerto Rico resident. Pre-move appreciation — the gain built up before you established residency — remains fully subject to U.S. federal capital gains tax when you eventually sell.

Concrete example: You bought stock for $1M. It's worth $5M when you move to Puerto Rico — $4M in unrealized pre-move gains. After two years in San Juan, it grows to $8M. When you sell:

- The $4M pre-move gain: taxable at U.S. federal rates — up to 23.8%, meaning roughly $952,000 owed

- The $3M post-move gain: $0 tax under Act 60

The lesson: Act 60 is most powerful for investors who move with assets that have not yet substantially appreciated, or for investors actively generating new capital gains going forward (traders, business sellers, real estate developers). For someone sitting on a $10M long-term stock position, the move mostly shelters future appreciation, not existing gains.

Cryptocurrency gets particular scrutiny here. The IRS has targeted crypto holders who tried to claim 0% on coins that were worth pennies when acquired but $millions by the time they sold post-move. Revenue agents look at blockchain transaction history, not just brokerage statements.

Who Qualifies: The Bona Fide Residency Test

Qualification hinges entirely on becoming a bona fide resident of Puerto Rico under IRC §937. Three tests must all be met:

1. The Presence Test

You must meet at least one of these:

- Spend at least 183 days in Puerto Rico during the tax year

- Spend 549 days in Puerto Rico over 3 consecutive years (minimum 60 days/year)

- Spend no more than 90 days in the U.S. during the year

- Earn no more than $3,000 from U.S. sources AND spend more days in Puerto Rico than in the U.S.

In practice, most Act 60 participants use the 183-day rule. That means no more than 182 days in the U.S. — including quick trips home for holidays, business, or family.

2. The Tax Home Test

Your principal place of business must be in Puerto Rico. If you're a remote worker whose "office" is technically in San Francisco, you have a problem. If you run a consulting business whose clients are all on the mainland but you perform the work in Puerto Rico, you're fine — as long as you can document where the work actually occurs.

3. The Closer Connection Test

This is the messy one. The IRS asks: where is your life actually centered? They examine driver's license, car registration, where your doctor and dentist are, where your children go to school, club memberships, bank accounts, social media check-ins, passport stamps, and credit card transaction locations.

Keeping your family in Greenwich while you spend 190 nights in a condo in Dorado fails this test. The IRS has said so explicitly in multiple audit determinations.

Act 60-Specific Requirements

Beyond the bona fide residency tests, Act 60 Chapter 2 adds:

- Purchase a primary residence in Puerto Rico within two years of receiving the decree (rental does not count)

- Annual charitable donation of $10,000 to qualifying Puerto Rico nonprofits — at least $5,000 must go to organizations focused on child poverty

- No prior Puerto Rico residency in the six years before applying (a 2025 rule change to prevent gaming)

- Applicants must be at least 18 years old

For context on the state domicile strategy that many mainland expats use before going abroad, the same "closer connection" analysis applies — Puerto Rico is an intensified version of that playbook.

The Real Cost of Getting a Decree

| Cost Item | Amount | Frequency |

|---|---|---|

| Application fee | $750 | One-time |

| Acceptance fee | $5,000 | One-time |

| Annual report filing fee | $5,000 | Annual |

| Charitable donation requirement | $10,000 | Annual |

| Attorney/consultant (application) | $3,000–$10,000 | One-time |

| CPA dual-filing compliance | $3,000–$10,000 | Annual |

Total first-year cost: roughly $26,000–$40,000. Ongoing annual cost: $18,000–$25,000. At $500,000 in annual capital gains, those costs represent about a 4–5% overhead against the $185,500 you'd otherwise send to California. Still a 75%+ effective savings rate.

The breakeven point — where Act 60 compliance costs equal your tax savings — is roughly $75,000–$100,000 in annual investment income compared to a zero-income-tax state, or $50,000–$65,000 compared to a high-tax state like California or New York.

Chapter 3: The 4% Business Tax

Formerly Act 20, the Export Services chapter is the business owner's version of this deal. If you run a consulting firm, software company, financial advisory, marketing agency, or legal practice — and you perform that work in Puerto Rico for clients outside the territory — your net income from those services is taxed at 4% in Puerto Rico and 0% federally (for bona fide residents).

A U.S. consultant earning $500,000 net profit pays up to 37% federal income tax — $185,000. Under Chapter 3, the same income generates $20,000 in Puerto Rico tax. The remaining $165,000 stays in the business or flows to the owner as a tax-exempt distribution.

Key operational requirements:

- A bona fide Puerto Rico office (not just a registered agent address)

- The services must actually be performed in Puerto Rico — work done while traveling stateside is U.S.-sourced and federally taxable

- Businesses with more than $3M in annual revenue must employ at least one full-time Puerto Rico resident (the owner can fill this role)

- Books, records, and accounting systems maintained on the island

Decree term: 15 years, renewable for another 15. That's up to 30 years of 4% corporate tax, locked in by a contract with the government of Puerto Rico.

The IRS Is Watching — Closely

Act 60 compliance is an IRS audit campaign priority, formally designated since 2021 and intensifying annually. A GAO report flagged the program for inadequate IRS oversight, which triggered congressional pressure and, eventually, a structured enforcement campaign.

What an Act 60 audit looks like: the IRS opens with an Information Document Request containing approximately 36 questions, more than 20 of which focus entirely or partially on bona fide residency. Agents request:

- Passport and travel records (every entry and exit stamp)

- Credit card transaction history showing where purchases were made

- Cell phone location data (carriers keep this; the IRS can subpoena it)

- Utility bills, lease agreements, and property records

- Social media posts, check-ins, and tagged photos

- Medical and dental records showing where you receive care

- School enrollment records for children

High-profile enforcement case: An investor attempted to shelter nearly $30 million in pre-move gains under Act 60 by fraudulently backdating corporate documents. He pleaded guilty in June 2025 and faces up to 3 years in prison plus $15.3 million in restitution to the IRS.

California and New York have also begun piggybacking on IRS audits. If you left either state claiming Puerto Rico as your new domicile, expect a state-level inquiry as well. The closer connection test matters for state tax purposes just as much as federal.

The lesson from enforcement patterns: people who genuinely live in Puerto Rico are fine. The IRS is targeting the "I own a condo there and visit 185 days a year but my family, business, and life are really in California" crowd.

For a broader look at how the IRS is expanding international enforcement using AI and data-sharing, see this breakdown of the CARF global data-sharing regime.

The December 31, 2026 Deadline

This is not a marketing deadline invented by Puerto Rico relocation consultants. Act 38-2026 draws a hard statutory line: applications filed on or before December 31, 2026 receive the 0% rate on qualifying income through at least 2035. Applications filed from January 1, 2027 onward receive a 4% preferential rate instead.

4% is still dramatically better than U.S. federal rates — on $500,000 in gains, it's $20,000 vs. $119,000 in a zero-tax state. But for investors and traders who can actually make the move, the 0% window represents roughly $99,000 per year in additional savings over the 4% structure, at that income level.

Timeline if you want to apply before the deadline:

- Establish physical residency in Puerto Rico (ideally before mid-2026, to document 183+ days in 2026)

- Hire a Puerto Rico tax attorney to prepare the application (budget 4–8 weeks for preparation)

- File application and pay $750 fee — application must be received before December 31, 2026

- Receive decree, pay $5,000 acceptance fee

- Purchase primary residence within two years of decree issuance

- Make annual $10,000 charitable donation starting in year one

Who Should Actually Consider This?

Act 60 Chapter 2 is not for everyone. It's a fit if:

- You have $300,000+ in annual investment income (capital gains, dividends, or interest) — below this, the compliance overhead may eat the savings

- You're a trader, crypto investor, or business seller anticipating a large liquidity event — Act 60 can save seven figures on a single transaction

- You can genuinely make Puerto Rico your home — you like the weather, the culture, the lifestyle, and you're not just farming a tax benefit

- Your assets have not yet substantially appreciated — the more unrealized pre-move gains you're sitting on, the less Act 60 helps on those specific positions

- You're already exploring geographic arbitrage and want to stay on U.S. soil

Chapter 3 is a fit if:

- You run a service business (consulting, tech, finance, creative) with $200,000+ in net income

- Your clients are primarily outside Puerto Rico (this is required by statute)

- You can genuinely operate the business from the island

For banking while living in Puerto Rico, U.S. mainland banking structures remain available — Puerto Rico is U.S. territory so your Mercury business account and Charles Schwab international brokerage work the same as from the mainland. FBAR and FATCA reporting obligations also remain — Act 60 doesn't exempt you from those.

If you need a reliable U.S. mailing address during the transition (especially for IRS correspondence, financial accounts, and state domicile documentation), a Traveling Mailbox virtual mailbox gives you a real U.S. street address in your chosen state for $15/month — essential while you're establishing your Puerto Rico residency record.

The Controversy You Should Know About

Act 60 is not politically neutral. A Harvard ReVista analysis characterized it as "more than an economic issue — a human rights issue," citing documented gentrification in San Juan, Condado, and Dorado. Long-time Puerto Rican residents have been priced out of their neighborhoods by an influx of high-income Act 60 participants. The $10,000 charitable donation requirement was introduced partly in response to this criticism.

Locally, the policy remains contentious. Many Puerto Ricans resent a program that reduces their tax base (by attracting wealthy individuals who pay 0% where they'd otherwise pay 33%+) while doing little to generate local employment or community investment. The required donation to child poverty nonprofits is a statutory acknowledgment of this tension.

This doesn't make Act 60 illegal or inadvisable for eligible investors. But if you're moving to San Juan under this program, engage genuinely with the local community. The $10,000 donation floor is a minimum, not a ceiling.

Conclusion

Puerto Rico Act 60 is the most powerful legal tax reduction tool available to U.S. citizens who don't want to renounce their citizenship or leave U.S. territory. For investors generating $300,000+ in annual capital gains, dividends, or interest — or for service business owners with $200,000+ in net income — the savings can reach six to seven figures annually.

The key constraints are real: you must actually live in Puerto Rico, your life's center of gravity must genuinely shift to the island, and the 0% rate applies only to post-move appreciation. The IRS is auditing aggressively and has both the tools and the mandate to pursue participants who fake it.

For those who can genuinely commit, the December 31, 2026 deadline to lock in 0% rates through 2035 creates an unusual urgency. Act 60 has been extended to 2055, so the opportunity isn't disappearing — but the best terms have an expiration date.

Related reading: FEIE: How expats abroad pay zero federal income tax | The expat investing playbook (PFIC traps and what to use instead) | The five flag strategy for tax minimization

Financial disclaimer: This article is for informational and educational purposes only and does not constitute tax, legal, or financial advice. Tax laws are complex and change frequently. Consult a qualified tax attorney or CPA licensed to practice in Puerto Rico and familiar with IRC §937 before making any residency or investment decisions. Individual circumstances vary significantly and the analysis in this post may not apply to your situation.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 26, 2026

Expat Tax & FinanceMay 26, 2026

Portugal IFICI: Is the NHR Replacement Worth It?

NHR ended in 2025. Portugal's IFICI replacement gives tech workers and researchers a 20% flat tax for 10 years — but retirees and passive investors.

Expat Tax & FinanceMay 25, 2026

Expat Tax & FinanceMay 25, 2026

State Domicile for Expats: Avoid the States That Chase You Abroad

California can tax your foreign income at 13.3% even after you leave. Learn how to change state domicile and save 5,000+ per year as a US expat.

Expat Tax & FinanceMay 6, 2026

Expat Tax & FinanceMay 6, 2026

The Foreign Housing Exclusion Most Expats Forget to Claim

Calculate the 2026 foreign housing exclusion on Form 2555: the $21,264 base, general limit, high-cost cities, and interaction with the FEIE.