The US government accidentally built a legal tax haven inside its own borders. Puerto Rico residents who qualify under Act 60 can pay 0% capital gains (if your decree is grandfathered pre-2027) or a flat 4% on investment income — while keeping a US passport, banking freely at American institutions, and never filing a Foreign Bank Account Report. No PFIC nightmare. No FBAR. No renouncing citizenship. Just a 90-minute flight from Miami.

Most people chasing geographic arbitrage ship everything to Medellín or Tbilisi. The ones who've run the math quietly moved to San Juan.

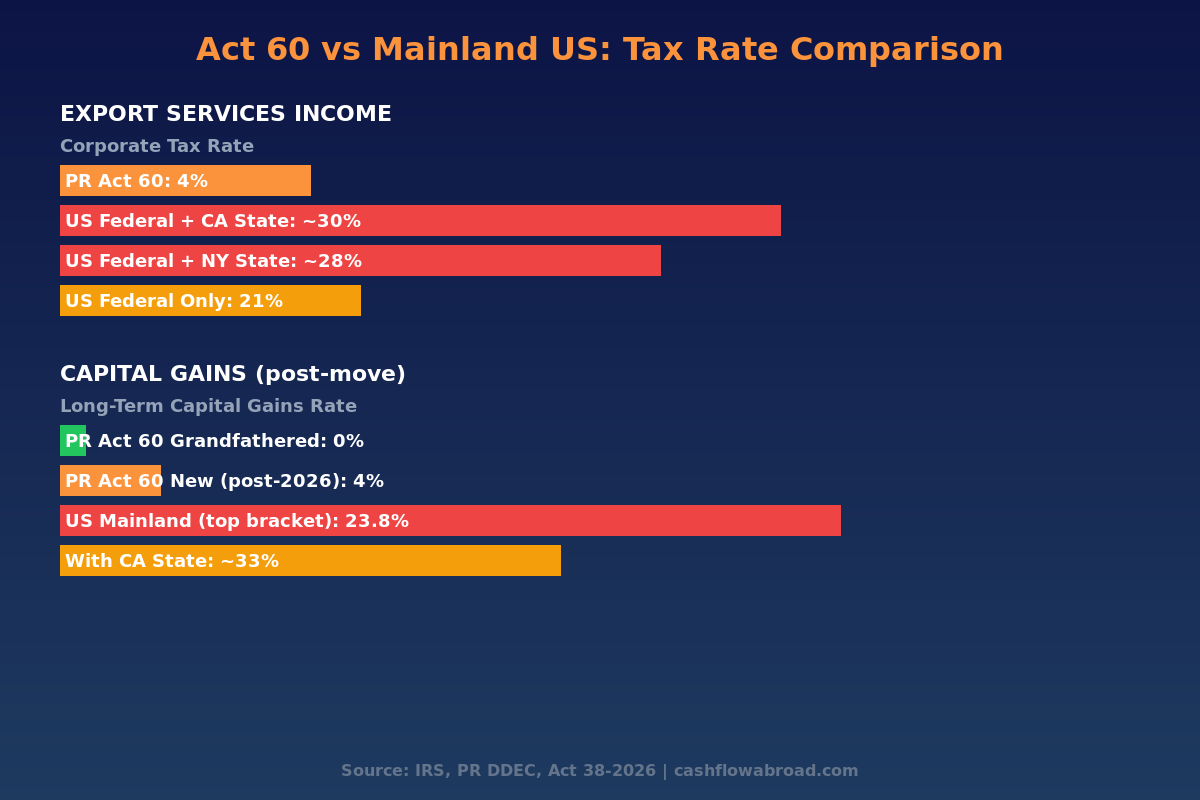

What Act 60 Actually Gives You

Act 60 consolidated Puerto Rico's former Acts 20 and 22 into a single incentive code in 2019. It has two chapters that matter for high-income earners: Chapter 2 for individual investors, and Chapter 3 for businesses exporting services.

The legal foundation is IRC Section 933, which has existed since 1954. US citizens who are bona fide Puerto Rico residents during the entire tax year exclude Puerto Rico-sourced income from their US federal return. Congress wrote this carve-out specifically because Puerto Rico residents pay into the PR treasury, not Washington. Act 60 supercharges that carve-out by setting Puerto Rico's local tax rate on qualifying income to near-zero.

The result: a US citizen living in San Juan, selling appreciated stock bought after establishing residency, legally owes $0 in federal income tax and $0 (grandfathered) or 4% (new applicants) in local tax on those gains. A California resident in the same situation owes 23.8% federal plus 13.3% state — a combined 37.1%. The spread on a $1 million capital gain: $371,000.

Two Chapters, Two Strategies

Chapter 2: Individual Resident Investor

Chapter 2 targets investors — people whose primary income comes from capital appreciation, dividends, interest, and crypto gains. Qualifying individuals receive:

- 0% tax on capital gains accrued after becoming a bona fide resident (grandfathered decree holders pre-2027)

- 4% on capital gains, dividends, and interest for new applicants filing after December 31, 2026 (under Act 38-2026)

- 100% exemption on interest and dividends from Puerto Rico sources

Important nuance: gains that accrued while you lived on the mainland are still US-taxable when realized. The clock starts when you establish residency — so the strategy is to move, then sell.

Chapter 3: Export Services

Chapter 3 applies to businesses providing services to clients outside Puerto Rico — consulting, software, financial services, marketing, remote work. Qualifying businesses pay:

- 4% fixed income tax (vs the US federal rate of 21% plus state taxes averaging 5–8%)

- 100% exemption on profit distributions from the qualifying business

- 75% exemption on municipal taxes

- 60% exemption on property taxes

A consultant billing $300,000/year from San Juan pays roughly $12,000 in income tax. That same income run through a Delaware LLC while living in New York hits approximately $84,000 in combined taxes. The Chapter 3 route saves roughly $72,000 annually — enough to buy a decent condo in the Puerto Rican highlands.

Bona Fide Residency: What It Really Takes

This is where people get burned. "I spend summers there" doesn't cut it. The IRS uses three tests simultaneously — you must pass all three:

The Three IRS Tests

| Test | Requirement | Common Failure Point |

|---|---|---|

| Presence Test | 183+ days/year in Puerto Rico | Spending summers on the mainland "visiting" |

| Tax Home Test | No tax home outside Puerto Rico | Keeping a US business address or primary office |

| Closer Connection Test | Stronger ties to PR than any other jurisdiction | Family, doctor, car, gym membership still in the US |

Beyond the IRS tests, Act 60 Chapter 2 imposes two additional requirements that mainland expat programs don't:

- Property purchase: You must buy residential property in Puerto Rico and use it as your principal residence within two years of receiving your decree. Not rent — own. The PR housing market has responded accordingly: prices in desirable areas jumped 71% year-over-year through 2025. Budget $350,000–$600,000 for a quality condo in San Juan, Dorado, or Río Grande.

- Annual charitable donation: $10,000/year to qualifying Puerto Rico-based nonprofits. This is baked into every decree.

One eligibility requirement most guides bury: you must not have been a Puerto Rico resident at any point in the 10 years prior to filing your application. Grew up in PR? You're likely ineligible.

The 2026 Deadline: What Act 38-2026 Changed

In March 2026, Puerto Rico's governor signed Act 38-2026, extending the program through 2055 — but with a critical catch. Anyone who files their Act 60 decree application on or after January 1, 2027 will pay a 4% rate on qualifying investment income instead of 0%. Decree holders who secured approval before that date are grandfathered at 0% for the life of their decree.

The window is closing. Applications typically take 60–120 days to process through DDEC's Single Business Portal. To lock in the 0% rate, applications need to be submitted well before year-end 2026.

| Scenario | Capital Gains Rate | Deadline |

|---|---|---|

| Decree approved before Jan 1, 2027 | 0% (grandfathered) | Apply now — 60–120 day processing |

| Decree filed after Jan 1, 2027 | 4% on gains, dividends, interest | Still dramatically better than mainland |

| US Mainland top bracket | 23.8% federal + up to 13.3% state | No deadline needed — it never improves |

Real Costs: Housing, Living, and Compliance

Puerto Rico is not a cheap-cost destination in the way Panama or Colombia are. The island's unique position as a US territory means mainland-level goods prices with Caribbean infrastructure frustrations. Here's the honest breakdown:

| Expense | Monthly Cost (San Juan) | Notes |

|---|---|---|

| 1BR apartment (rent) | $900–$1,400 | $1,200–$2,000 for 2BR in Condado/Santurce |

| Groceries | $400–$600 | Imported goods ~20% more expensive than mainland |

| Utilities (electricity) | $150–$350 | PREPA rates are volatile; outages are real |

| Transportation | $200–$400 | Car near-mandatory outside metro areas |

| Health insurance | $80–$200 | US plans work here; PR hospital quality varies |

| Act 60 compliance (annualized) | ~$200 | CPA + attorney fees, annual DDEC report |

| Single-person total | ~$2,700/month | Above global arbitrage destinations but no FBAR/PFIC |

The $10,000/year charity requirement adds another ~$833/month effectively — though donors often find organizations they genuinely support. Puerto Rico's median household income is roughly $26,000/year, so that donation is real money in the local economy.

For banking: US banks work seamlessly from Puerto Rico — no foreign account headaches. Charles Schwab International remains the top brokerage pick for Act 60 residents: free ATM withdrawals worldwide, no foreign transaction fees, and no PFIC complications since your accounts stay domestic. For new US business banking during the transition from mainland to island, Mercury is a strong option for export services LLCs that need a clean, modern platform that doesn't blink at non-traditional operating locations.

The IRS Is Watching: Campaign 685 and the GAO Report

Act 60 has attracted exactly the kind of aggressive tax-minimization attention that invites enforcement. In 2021, the IRS launched Campaign 685, a dedicated initiative targeting Act 60 participants who claim exemptions without genuinely meeting residency and income-sourcing requirements.

Then on December 12, 2025, the US Government Accountability Office released a detailed audit report recommending that the IRS establish formal procedures to systematically monitor all taxpayers claiming Puerto Rico's resident investor incentive and review referrals from Puerto Rico's own government agencies. The IRS agreed with every recommendation.

Cryptocurrency is the sharpest enforcement edge. Through Chief Counsel Memorandum 202538025, the IRS has made clear it will challenge whether crypto gains are genuinely Puerto Rico-sourced. Appreciation that accrued before you established residency is US-sourced, period. Selling Bitcoin bought in 2019 one week after getting your decree does not make those gains Puerto Rican. The IRS has the on-chain data, the exchange records, and now a formal program to match them against Act 60 filers.

Compliance basics the IRS looks for:

- Day-count documentation (entry/exit stamps, credit card records, phone pings)

- Genuine local ties: Puerto Rico driver's license, voter registration, local doctors and dentist

- No maintaining a full-time US office while "working remotely from San Juan"

- Selling assets only after — not before — residency is established and documented

The people who get caught are invariably the ones who tried to claim the benefits while keeping their actual life on the mainland. If you genuinely move to Puerto Rico, genuinely spend 183+ days there, and genuinely run your business from the island — the program works exactly as advertised. For crypto tax documentation as an Act 60 holder, CoinTracking generates the detailed records needed to distinguish pre-residency from post-residency appreciation — essential for any Act 60 holder with significant crypto positions.

Who Act 60 Makes Sense For (and Who It Doesn't)

Act 60 has a specific user profile. It's not a universal solution.

Strong fit:

- Investors with significant unrealized capital gains in taxable accounts — stock options, appreciated securities, or crypto acquired post-move

- Service business owners billing international clients (consulting, software, financial advisory, marketing, legal services)

- People who can genuinely spend 183+ days/year on the island and find Caribbean island life appealing

- Those who dislike the complexity of FBAR, PFIC rules, and foreign tax credits that full expatriate life requires

Poor fit:

- W-2 employees — salary from a mainland employer is US-sourced income regardless of where you sleep

- People whose family remains on the mainland — the closer connection test is nearly impossible to pass while your spouse and kids are in Connecticut

- Anyone unwilling to purchase property or make the minimum charitable donation

- Those expecting the exemption to apply to gains that built up before the move

For those open to full expatriation, the geographic arbitrage playbook compares Act 60 against jurisdictions like Serbia's 15% flat tax, Andorra's 10% max, and Georgia's 1% freelancer rate. The FEIE approach — which can zero out up to $126,500 of earned income for Americans living fully abroad — is covered in the FEIE guide. Act 60 doesn't require you to leave the US legal system; the FEIE requires you to actually leave. Both are valid; which is right depends entirely on your income mix and risk tolerance for foreign infrastructure.

How to Apply: The Step-by-Step Process

- Spend time on the island first. Rent month-to-month in Condado, Isla Verde, Palmas del Mar, or Dorado. Understand what you're committing to before filing. The 183-day clock starts when you establish genuine residency, not when your decree arrives.

- Hire a Puerto Rico-licensed attorney. The application requires sworn statements, detailed financial disclosures, and compliance agreements. Budget $3,000–$6,000 in legal fees. Application fees to DDEC are paid separately.

- File through DDEC's Single Business Portal. Processing runs 60–120 days. To lock in the pre-2027 grandfathered 0% rate, submit by September 2026 at the latest.

- Purchase residential property within 2 years of decree. This is a hard contractual requirement. Start looking early — Act 60 hotspot areas like Dorado Beach move fast and have already absorbed significant demand-driven price appreciation.

- File annual compliance reports. Every year, submit documentation proving residency days, the charitable donation, and that the property remains your principal residence. Missing a year risks decree revocation.

If you're unwinding a mainland address while setting up on the island, a virtual US mailbox becomes essential — particularly for IRS correspondence, state domicile management, and any accounts that require a physical US address. Traveling Mailbox provides a real US street address in 50+ cities with mail scanning, forwarding, and check deposit starting at $15/month. The virtual mailbox guide covers how to use one properly during a domestic relocation like this. For health coverage during extended travel off-island, SafetyWing Nomad Insurance provides supplemental travel medical coverage at $56–$92/month.

Conclusion

Puerto Rico Act 60 is the most underused legal tax optimization available to US citizens — largely because people assume the only path to lower taxes is leaving the country entirely. A US territory with 83°F winters, direct flights from every East Coast city, and no FBAR requirement doesn't fit most people's mental model of "offshore tax planning." But the math is hard to ignore: $371,000 saved on a $1 million gain, $72,000 saved annually on service business income, zero foreign bank account compliance overhead.

The window for locking in the 0% grandfathered rate closes December 31, 2026 — and with 60–120 day processing times, that means acting now, not in November. The IRS scrutiny is real, and it's increasing. The housing market has already priced in demand. None of those factors eliminate the opportunity; they just reward the people who move deliberately and actually comply.

If you have unrealized gains, a location-flexible income, and an appetite for year-round sunshine, the arithmetic here doesn't ask permission.

Financial disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Puerto Rico Act 60 benefits are subject to eligibility requirements, individual circumstances, and compliance with IRS and DDEC regulations. Tax laws change. The Act 38-2026 provisions, rate changes, and application deadlines referenced reflect information available as of May 2026. Consult a licensed Puerto Rico tax attorney and CPA before making any relocation or financial decisions.