Portugal for US Expats: Taxes, Visas, Cost of Living

NHR is gone, but 21,000 Americans moved to Portugal anyway. Here is what the visa options, IFICI tax regime, and real monthly costs look like in 2025.

NHR ended in 2024. Here is what Americans actually pay in Portugal now, D7 vs D8 visa requirements, cost of living in Lisbon vs Porto, and IFICI explained.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Portugal's famous NHR tax deal — 10 years of 0% tax on foreign income — ended December 31, 2023. The internet declared Portugal dead for expats. Meanwhile, the number of Americans living there jumped 50% in a single year, reaching roughly 21,000 registered US citizens by 2024. The math still works. It just looks different than it did three years ago.

This guide covers everything American expats need to know: the visa options that remain, the IFICI regime that replaced NHR, what you'll actually pay in taxes, and how much life costs in Lisbon versus Porto.

Why Portugal Still Makes Sense

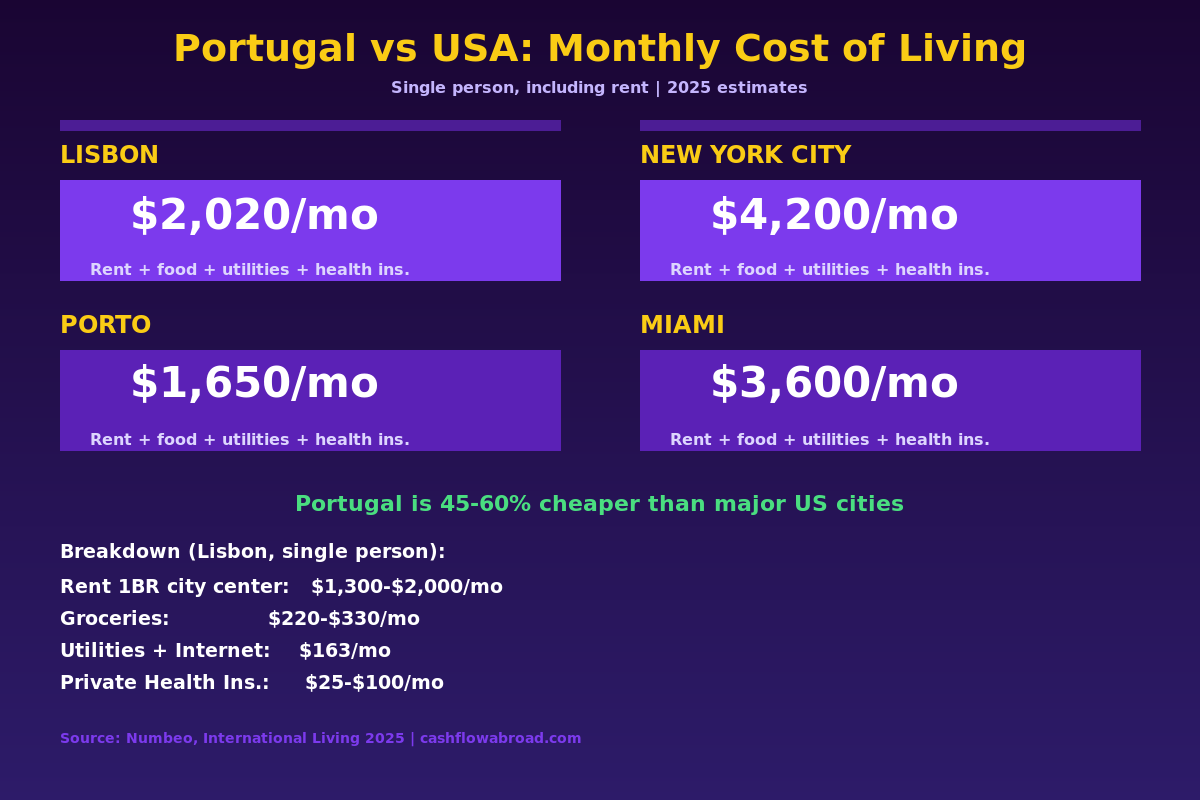

Portugal offers a rare combination that most expat destinations can't match: EU residency with a path to citizenship, English widely spoken (especially in cities), a functioning national healthcare system, sub-$2,000/month living costs in a Western European capital, and a stable political environment. Compare that to the US, where a single person in New York pays $4,200+/month just to break even, and Portugal's value proposition is obvious even without a preferential tax regime.

The country also has legitimate infrastructure: gigabit fiber internet in Lisbon and Porto, reliable public transit, direct flights to the US, and a legal system rooted in EU law. For Americans who want Europe without the chaos of Germany's bureaucracy or France's administrative hostility toward foreign income, Portugal tends to win.

Visa Options for Americans

D7: Passive Income Visa

The D7 is Portugal's entry point for retirees, dividend investors, and anyone living off passive income. You don't need a job or a business — just provable, recurring income originating outside Portugal.

- Minimum income: €920/month (~$1,010) for a single applicant

- For couples: €1,380/month (~$1,520)

- Add per dependent child: +30%

- Qualifying sources: Social Security, pension, dividends, rental income, royalties

- Visa fee: ~€110 (~$121) plus ~€40 VFS service fee and ~€170 for the AIMA residence permit

- Processing time: ~60 days from submission

One important shift: as of 2024, AIMA (Portugal's immigration agency) has started rejecting D7 applications from active freelancers and remote employees. If you're working for clients or an employer, the D7 is not your path. Remote workers need the D8.

D8: Digital Nomad Visa

Launched in 2022, the D8 targets remote workers who earn income from foreign employers or international clients. The income threshold is substantially higher than the D7 — this isn't a budget nomad visa.

- Minimum income: €3,680/month (~$4,050) — 4× the Portuguese minimum wage

- Savings requirement: €11,040 (~$12,150) in a bank account

- Duration: 2-year initial visa, renewable for 3 more years (5 years total)

- Path to permanent residency and citizenship: 5 years of continuous legal residency

The $4,050/month income floor filters out a significant share of applicants. If you clear it working remotely, the D8 is one of the cleanest paths into the EU available to Americans. For context on how Portugal compares to other nomad visa options, see our ranked guide to digital nomad visas.

Golden Visa: What's Left

The real estate investment route — which fueled Portugal's Golden Visa boom for a decade — was permanently closed in October 2023. What remains are higher-capital routes:

| Route | Minimum Investment |

|---|---|

| Qualifying venture capital / investment fund | €500,000 (~$550,000) |

| Arts or national heritage donation | €250,000 (~$275,000) |

| Scientific or technological research | €500,000 (~$550,000) |

| Create 10+ jobs | €500,000 (~$550,000) |

One development to watch: Portugal's parliament voted in late 2025 to extend the residency requirement for citizenship from 5 to 10 years — significantly reducing a core appeal of the Golden Visa. If EU citizenship is your goal, verify the current timeline with a Portuguese immigration attorney before committing capital.

The NHR Is Dead. Meet IFICI.

The NHR regime (Non-Habitual Resident) closed to new applicants on December 31, 2023. Anyone who got in before that date keeps their 10-year benefit — including the 10% flat tax on foreign pension income — for their remaining term. If you entered NHR in 2020, you're protected until 2030.

New applicants get IFICI (Incentivo Fiscal à Investigação Científica e Inovação), which the press sometimes calls "NHR 2.0." The name oversells it. Here's the reality:

- 20% flat rate on Portuguese-sourced employment or self-employment income in qualifying activities

- Foreign-sourced income: Exempt — with one major exception: pensions are taxed at progressive rates up to 48%

- Duration: 10 consecutive tax years

- Qualifying sectors: R&D, technology startups, scientific research, healthcare in specific roles, and other approved activities

- Education requirement: Must hold at minimum a Level 6 EQF degree (bachelor's + 3 years relevant experience) or a doctorate

- Prior residency rule: Cannot have been a Portuguese tax resident in the 5 preceding years

IFICI is a meaningful benefit for tech workers and researchers actively employed in Portugal. For retirees and remote workers whose income is entirely foreign-sourced, IFICI doesn't apply — their foreign income is already exempt under standard rules, and they don't earn qualifying Portuguese income to benefit from the 20% rate.

What Americans Actually Pay in Taxes

Most Portugal expat guides focus entirely on Portuguese tax while glossing over the US side. Americans owe taxes in two systems simultaneously — and how you structure the interaction determines whether you owe anything at all.

Portugal Side

Portugal taxes residents on worldwide income at progressive rates from 13.25% to 48%. If you're a D7 resident living off US dividends, Social Security, or a pension, Portugal will assess you on those amounts at standard rates unless a treaty provision reduces it. Portugal and the US have a tax treaty (signed 1994), but it doesn't exempt Americans from US tax the way it might for citizens of other countries — the US taxes its citizens on worldwide income regardless of where they live.

The Foreign Tax Credit Strategy

For most Americans in Portugal, the Foreign Tax Credit (FTC) is the better tool — not the FEIE. Portugal's top marginal rate (48%) exceeds the US top rate (~37%). When you claim the FTC, you credit your US tax liability with taxes already paid to Portugal. In most scenarios, the FTC wipes out the entire US tax bill and often generates carry-forward credits.

The FEIE (which excludes up to $132,900 in 2026) works technically, but it reduces adjusted gross income in ways that can eliminate IRA contribution eligibility and certain tax credits. Most US expat CPAs recommend FTC for Portugal-based Americans. For a full comparison, see our FEIE guide.

Bottom line: most Americans in Portugal owe zero US income tax — but they still must file a US return every year, report Portuguese bank accounts on FBAR if balances exceed $10,000 at any point, and potentially file FATCA Form 8938. Our FBAR and FATCA guide covers the mechanics.

Cost of Living: Lisbon vs Porto

Lisbon has gotten expensive by Portuguese standards. A city-center one-bedroom now runs $1,300–$2,000/month — real money, though still less than half of comparable New York rents. Porto is where the value concentrates: the same apartment goes for $870–$1,100/month, and the city has the same fiber internet, good food, and European infrastructure as Lisbon at a 30–40% discount.

| Expense | Lisbon | Porto |

|---|---|---|

| 1BR apartment (city center) | $1,300–$2,000/mo | $870–$1,100/mo |

| 3BR apartment (city center) | $1,900–$2,900/mo | $1,500–$2,100/mo |

| Monthly groceries (one person) | $220–$330 | $190–$280 |

| Inexpensive restaurant meal | $13–$17 | $11–$15 |

| Dinner for two (mid-range) | $38–$60 | $30–$50 |

| Electricity, water, heating | ~$127/mo | ~$110/mo |

| Fiber internet (60+ Mbps) | ~$36/mo | ~$33/mo |

| Monthly total (single, comfortable) | ~$2,020–$2,750 | ~$1,650–$2,200 |

| Monthly total (couple, comfortable) | ~$3,500–$4,500 | ~$2,750–$3,500 |

Portugal's internet infrastructure is genuinely strong. By late 2025, 93.8% of fixed broadband connections offer at least 100 Mbps, with fiber now the standard in both cities. NOS, MEO, and Vodafone offer gigabit plans in the $25–$40/month range. Remote workers don't give anything up on connectivity.

Healthcare for US Expats

Legal residents can register with Portugal's SNS (Serviço Nacional de Saúde). Once registered, primary care is largely free or costs €5–€20 per visit. Specialist care is subsidized. The SNS's drawbacks are wait times and limited English-speaking staff outside of Lisbon and Porto.

Most American expats run a hybrid: SNS registration as a safety net, private insurance for routine and elective care. Private health insurance costs €20–€50/month for a healthy person under 40 on a basic plan, and €100–€300/month for comprehensive coverage. For Americans still traveling or splitting time between Portugal and the US, SafetyWing offers nomad health coverage that bridges the gap while you establish residency. See our expat health insurance guide for a full breakdown of options.

Banking: The FATCA Problem

Portugal signed a FATCA Intergovernmental Agreement with the US in 2015, requiring Portuguese banks to report US-citizen accounts to the IRS. The administrative burden causes some smaller institutions to simply decline American applicants.

Banks that routinely accept US citizens without problems:

- Millennium BCP — Portugal's largest private bank, most experienced with FATCA

- Caixa Geral de Depósitos — state-owned, generally US-friendly

- Santander Portugal — international bank, familiar with cross-border clients

Before approaching any bank, get your NIF number (Número de Identificação Fiscal — Portugal's tax ID). A fiscal representative can obtain one for you before you even arrive. Without it, no Portuguese bank will open your account.

Keep your US accounts open. Charles Schwab International is the standard for expat banking: no foreign transaction fees, global ATM reimbursements, and a US address on file — which matters for brokerage, FBAR, and tax filing. Our full Schwab guide covers the account setup. If you're running a US business from Portugal, Mercury handles US business banking cleanly for non-resident founders.

You'll also want a US mailing address to maintain banking relationships and IRS correspondence. Traveling Mailbox provides a real US street address in 50+ cities with mail scanning and check deposit for ~$15/month — the site owner uses this personally. See the full guide at virtual mailbox for expats.

For moving money between your US and Portuguese accounts, Remitly consistently beats bank wire rates on USD-to-EUR transfers.

Buying Property in Portugal

Foreigners pay the same property taxes as Portuguese nationals — no surcharge. The two main costs at purchase and over time:

IMT (one-time purchase transfer tax):

| Property Value | IMT Rate |

|---|---|

| Up to €97,064 | 0% |

| €97,064–€132,774 | 2% |

| €132,774–€181,034 | 5% |

| €181,034–€301,688 | 7% |

| €301,688–€578,598 | 8% |

| Above €578,598 | 6% (flat) |

IMI (annual municipal property tax): 0.3%–0.5% of the assessed taxable value for urban properties. Lisbon charges 0.3% — on a €300,000 property, that's €900/year (~$990). An additional AIMI surcharge applies on values above €600,000.

One tax trap worth flagging: when Americans eventually sell a Portuguese property, the IRS taxes the full USD gain — including any appreciation driven by EUR/USD exchange rate movement, not just actual property value growth. Model this exposure before buying. Our phantom gains guide covers the mechanics.

Is Portugal Right for You?

Portugal makes the most sense for Americans who want EU residency with a genuine path to citizenship, can meet either the D7 passive income threshold (€920/month) or the D8 remote work threshold (€3,680/month), and want Western European living standards at 45–60% below comparable US city costs.

It's a harder case for new retirees who expected the NHR's 10% flat tax on pension income — that window closed at the end of 2023. Under the current regime, US pension income gets taxed at Portugal's progressive rates, and you're relying on the FTC to neutralize the US side. The cost-of-living arbitrage still justifies the move for many retirees, but the pure tax play is gone. For a deeper look at how Social Security and pension income works abroad, see our retirement abroad guide.

Conclusion

Portugal's NHR was one of the best expat tax deals in the world. Its replacement, IFICI, is narrower and more restrictive — but the underlying reasons Americans choose Portugal haven't changed. Living costs are 45–60% below major US cities, EU residency is achievable, the infrastructure works, and ~21,000 Americans are already there making it work. The tax math in 2025 requires more deliberate planning than it did in 2020, but it still pencils out for the right profile.

Start with the visa question — D7 or D8 — then map out the FTC strategy with a US expat CPA before you move. Getting the tax election right from year one avoids costly corrections later.

Financial disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws change frequently and individual circumstances vary significantly. Consult a qualified US expat tax professional and a licensed Portuguese immigration attorney before making any residency or financial decisions. FEIE, FTC, and FBAR/FATCA filing requirements have specific eligibility rules that require professional evaluation for your specific situation.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Geographic ArbitrageJune 6, 2026

Geographic ArbitrageJune 6, 2026

Vienna Expat Guide: RWR Card, Taxes, and Living Costs

Vienna ranks #1 in livability. Complete guide to Austria's Red-White-Red Card, the 30% expat tax deduction, income brackets, and real monthly living

Geographic ArbitrageMay 12, 2026

Geographic ArbitrageMay 12, 2026

Saudi Arabia for US Expats: Zero Tax, High Pay, Real Traps

Saudi Arabia has 0% local income tax but US citizens still owe the IRS. FEIE strategy, Iqama visa, expat salaries, and FBAR rules explained.

Geographic ArbitrageMay 5, 2026

Geographic ArbitrageMay 5, 2026

Uruguay Tax Residency: The Hidden Catch Expats Miss

Uruguay is a worldwide tax system with an 11-year exemption — not permanently territorial. Here's the full breakdown vs Panama and Paraguay.