Portugal's NHR Is Gone — What IFICI Means for Expats

Portugal killed its famous NHR tax regime in 2024. Here's what the IFICI replacement actually means for tech workers, retirees, and digital nomads — with real numbers.

NHR closed in 2024. Portugal's IFICI replacement has a 20% flat rate — but no pension exemption. See who qualifies, who doesn't, and the real tax math.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Portugal's NHR tax regime attracted more than 74,000 registered beneficiaries by 2023. A retiree with €50,000 in foreign pension income paid a flat 10% — €5,000 — instead of the standard progressive rate that could hit €13,000 or more. Physicians relocated from Paris. Tech executives left London. Entire coworking spaces in Lisbon filled up with people who'd specifically moved for the tax deal.

Then the Portuguese government closed it on December 31, 2023. And the replacement — IFICI, officially the Incentivo Fiscal à Investigação Científica e Inovação — arrived quietly, with a ministerial order that wasn't even published until December 24, 2024. Nearly a year of ambiguity followed, and a lot of misinformation about who the new regime actually serves.

Here's the honest assessment: IFICI is worse than NHR for retirees. It's comparable for qualifying tech employees. And for most freelance digital nomads, it offers essentially nothing. Which matters because tens of thousands of people are still choosing Portugal every year and making financial decisions based on the old reputation.

What Made NHR So Powerful

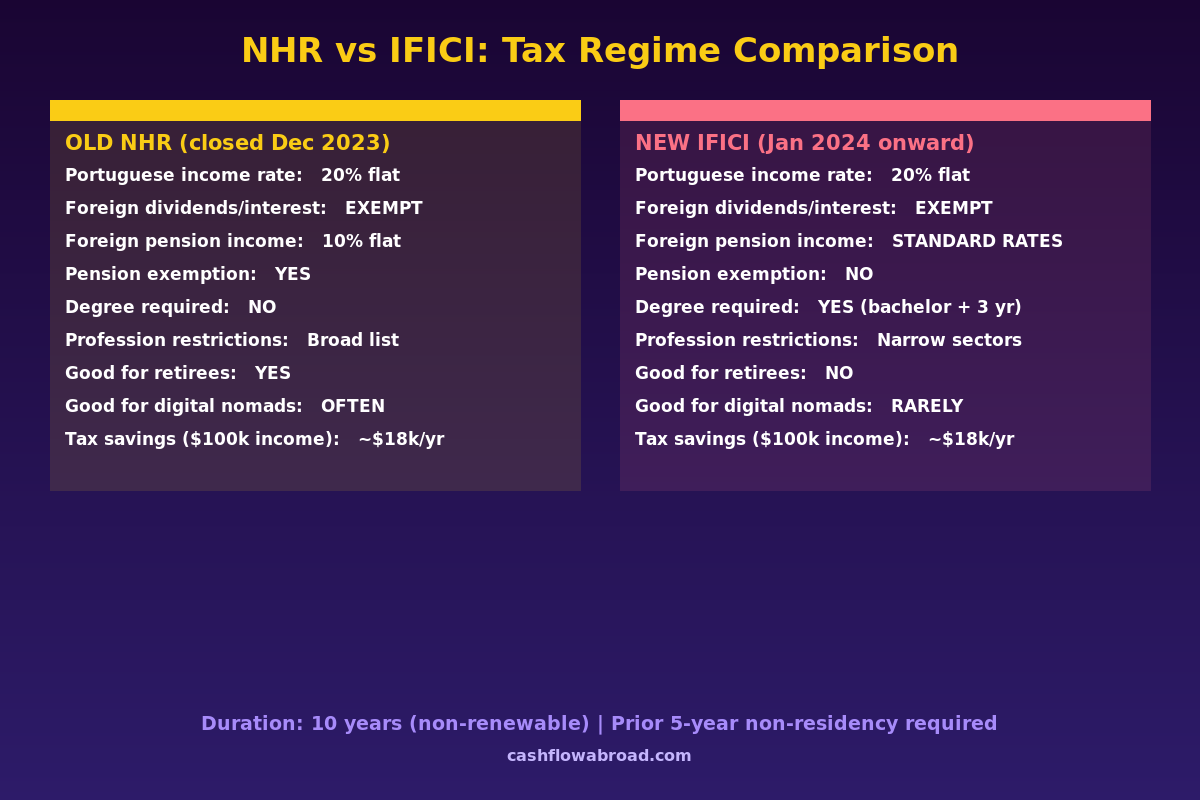

The Non-Habitual Resident regime ran from 2009 to 2023. The core mechanics were simple: move to Portugal, prove you haven't been a Portuguese tax resident in the previous five years, get your profession certified as a "high-value activity," and lock in a flat 20% rate on Portuguese-sourced income for ten years.

But the real money was in the foreign income exemption. Dividends, interest, capital gains, rental income, employment income — if it came from a country with which Portugal had a tax treaty, it was either exempt at 0% or taxed at low flat rates. Foreign pensions took a hit in April 2020 when Portugal added a 10% flat rate (after Denmark and other countries complained about pensioners draining their systems), but even at 10%, NHR was dramatically cheaper than the alternative.

Portugal's standard progressive tax brackets run from 13% on the lowest incomes to 48% on anything above €83,696 — plus a 2.5% solidarity surcharge above €80,000 and 5% above €250,000. At the top, effective rates reach 53%. NHR wasn't just good. For high earners and retirees, it was transformative.

Why Portugal Killed It

The short version: housing prices. Lisbon's residential property market more than doubled between 2015 and 2023. Locals watched wealthier foreigners — many of them NHR beneficiaries — outbid them for apartments in neighborhoods they'd grown up in. The political pressure became impossible to ignore.

Critics also pointed to the fiscal cost. KPMG and other tax advisory firms estimated Portugal was forgoing billions in tax revenue annually from NHR holders who paid minimal Portuguese income tax on massive foreign portfolios. The argument that these residents contributed to the economy through spending, job creation, and investment eventually lost the political battle.

The new IFICI was designed explicitly to attract working professionals who contribute to Portugal's innovation economy — not retirees living off foreign pensions, and not passive investors whose main tie to Portugal is a nice apartment and a favorable tax rate.

How IFICI Works

The headline number is identical to old NHR: a 20% flat rate on qualifying Portuguese-sourced income. The foreign income exemption also survives — dividends, interest, capital gains, and foreign employment income are still taxed at 0%, provided the source country isn't on Portugal's tax haven blacklist.

What changed is everything else.

Pensions are out. Foreign pension income is no longer covered by the flat rate. It falls into the standard progressive brackets — up to 48% at the top end. A retiree with €60,000 in annual pension income who previously paid €6,000 (10%) now pays approximately €20,000–€22,000 under standard Portuguese rates. That's a €14,000–€16,000 annual swing.

Qualifications are now required. Old NHR had no education requirement. IFICI requires either a bachelor's degree (minimum EQF Level 6) plus three years of relevant professional experience, or a PhD with no experience threshold. This immediately disqualifies some NHR beneficiaries who wouldn't have met this bar.

The profession list is narrower. The qualifying occupations (defined in Annex I of Portaria 352/2024, published December 24, 2024) include senior managers of qualifying companies, engineers, ICT specialists, R&D professionals, industrial designers, and university professors. The old NHR list was broader — it covered architects, healthcare professionals, artists, and a range of creative industries that no longer qualify.

The employer matters now. For most IFICI pathways — particularly for those applying through AICEP (Portugal's investment agency) — you need to be employed by or providing services to a certified company. This means a Portuguese startup officially recognized under law, or a company that exports more than 50% of its revenue. A freelancer working from a Lisbon café for clients in New York doesn't automatically qualify, even if their job title is on the approved list.

The Real Numbers: What IFICI Saves (and Doesn't)

The value of IFICI depends almost entirely on what type of income you have and whether you qualify at all.

Scenario 1: Senior software engineer, €100,000 Portuguese salary

Under standard Portuguese rates, this person pays roughly €36,000–€38,000 in income tax plus €11,000 in employee social security contributions. Total burden: approximately €47,000–€49,000. Net take-home: ~€52,000.

Under IFICI at the 20% flat rate: €20,000 in income tax plus €11,000 in social security. Total burden: €31,000. Net take-home: ~€69,000.

Annual IFICI benefit: ~€17,000–€18,000. Over ten years, assuming income stays roughly flat, that's approximately €170,000 in cumulative tax savings — before accounting for the foreign income exemption on dividends or investment returns.

Scenario 2: Tech executive, €200,000 qualifying income

| Tax Regime | Income Tax | Net Income (est.) | Annual Savings vs. Standard |

|---|---|---|---|

| Standard Portuguese rates | ~€87,000 | ~€102,000 | — |

| IFICI (20% flat) | €40,000 | ~€149,000 | ~€47,000/year |

| Old NHR (20% flat) | €40,000 | ~€149,000 | Identical to IFICI |

Over a full ten-year IFICI period, a €200,000 earner saves approximately €470,000 versus paying standard Portuguese rates. That's meaningful — enough to buy a significant property in Porto outright or fund several years of retirement in a lower-cost location afterward.

Scenario 3: American retiree, €50,000 foreign pension

| Regime | Annual Tax on €50k Pension | Effective Rate |

|---|---|---|

| Old NHR (grandfathered holders only) | €5,000 | 10% |

| IFICI (new applicant) | €12,500–€14,000 | ~25–28% |

| Standard Portuguese resident (no regime) | €12,500–€14,000 | ~25–28% |

For a retiree, IFICI delivers zero benefit on pension income. The tax hit is identical to what a non-qualifying resident pays. Anyone who moved to Portugal specifically for the NHR pension benefit — and hasn't yet registered — is looking at the wrong country for the wrong reasons.

If retirement tax efficiency is the primary goal, geographic arbitrage in lower-cost countries or establishing residency in a territorial tax country typically delivers better outcomes — and neither route requires a qualifying employer or a degree verification process.

Who Actually Qualifies for IFICI

The practical test has three parts: education, profession, and employer.

Education: A bachelor's degree (EQF Level 6 or higher) in a field relevant to your qualifying profession, plus three years of demonstrable professional experience. A PhD bypasses the experience requirement. Self-taught professionals and those without formal credentials don't qualify regardless of income level or skills.

Profession: Your job title must appear in Annex I of Portaria 352/2024. The main categories: senior managers and directors of qualifying firms (with specific economic criteria), engineers, ICT specialists, R&D and scientific research personnel, industrial and product designers at certified companies, and academic/university faculty. Architects, lawyers, financial advisors, doctors, and most creative professionals who qualified under old NHR are not on the IFICI list.

Employer pathway: Depending on how you apply, your employer may need to be certified. Three main channels exist:

- AICEP route: Employees of Portuguese companies that export 50%+ of revenue — registered through Portugal's trade and investment agency

- Startup route: Employees of officially certified Portuguese startups under the national startup law

- Direct Finanças route: Qualifying high-value professions listed in Annex I can apply directly through the tax authority — no employer pre-certification required, but profession verification is still mandatory

The direct route is the most accessible for self-employed professionals, but they must operate in a qualifying profession and demonstrate that their work aligns with the approved activity codes.

How to Apply: Step-by-Step

Five steps, one hard deadline.

Step 1: Get your NIF. Your Portuguese tax identification number is the foundation. Obtain it at a Finanças office in person, or through a fiscal representative if applying from outside Portugal. Without a NIF, nothing else proceeds.

Step 2: Establish tax residency. Spend 183+ days in Portugal during the calendar year, or maintain a habitual home there before December 31. The year you establish residency is the anchor year for your application.

Step 3: Get pre-certified (if applicable). AICEP and startup pathways require employer certification from the relevant agency. This can take several weeks. Start this process early — ideally before the end of your residency year.

Step 4: Apply through Portal das Finanças. Navigate to Serviços Tributários → Inscrição IFICI. Upload your degree certificates, employment contract (or self-employment registration documents), proof of professional experience, and any certification letters. Processing typically takes days to a few weeks.

Step 5: Meet the January 15 deadline. Applications must be submitted by January 15 of the year following your first year of Portuguese tax residency. Became resident in 2025? Apply by January 15, 2026. There is no extension mechanism — miss it and you lose IFICI for that entire year.

For the US expat banking side of a Portugal relocation: a Charles Schwab International account handles ATM withdrawals worldwide with full fee reimbursement and no foreign transaction fees — essential when you're splitting time between Lisbon and the US. Maintaining a US mailing address through Traveling Mailbox (~$15/month) keeps your IRS correspondence address and any remaining US state domicile clean while you're physically in Portugal. Our guide to virtual mailboxes for expats covers why this matters for banking and tax compliance.

Existing NHR Holders: You're Protected

If you registered under NHR before January 1, 2024, your status is untouched. You keep your original NHR for the remainder of your ten-year period, including the 10% flat rate on foreign pensions, the 20% rate on qualifying Portuguese income, and all original foreign income exemptions. IFICI does not affect existing NHR holders in any way.

The last "normal" NHR registrants — those who became residents in 2023 and registered by March 31, 2024 — hold NHR through December 31, 2033. After their ten years expire, they fall into standard Portuguese rates or leave.

There was also a transitional window that's now closed: individuals who became Portuguese tax residents during 2024 and met at least one specific qualifying criterion (a work contract signed before December 31, 2023, a residency visa application filed before that date, a Portuguese property agreement before October 10, 2023, school enrollment for a dependent child, or a statement of interest filed with Portuguese immigration) could apply for legacy NHR status by March 15, 2025. That window is gone.

Is Portugal Still Worth It?

For qualifying tech and R&D professionals: yes, clearly. The tax math on €150,000–€200,000 in Portuguese-sourced income still generates €35,000–€47,000 in annual savings versus standard rates, combined with relatively affordable living costs compared to comparable Western European cities, excellent infrastructure, easy access to the US and UK, and a growing startup ecosystem concentrated in Lisbon.

For US citizens, the IFICI structure also interacts well with the Foreign Earned Income Exclusion. If your FEIE exclusion covers the first ~$130,000 in foreign earned income, the IFICI 20% flat rate applies only to the excess — and any US-sourced dividends or capital gains remain subject to US tax treatment separately, while Portugal exempts foreign investment income entirely. The combined result can be remarkably efficient for the right profile.

For retirees, passive investors, and most independent digital nomads, Portugal's tax case has effectively collapsed. The honest advice is to look at other jurisdictions — countries with territorial tax systems, low-cost geographic arbitrage destinations with better tax treaties, or the Five Flag Strategy for those willing to more fully optimize. The full nomad visa rankings also cover Portugal's D8 Digital Nomad Visa, which addresses the residency question separately from the tax question.

Health coverage is essential regardless of tax status. Portugal's public healthcare system is functional but has extended wait times for specialists. Most expats add international coverage — SafetyWing Nomad Insurance starts at $56.28/month for remote workers under 39, while their Remote Health plan covers those wanting comprehensive expat coverage. Our expat health insurance guide breaks down the full range of options.

For moving money between the US and Portugal — setting up recurring transfers to a Millennium BCP or Caixa Geral account, or repatriating earnings — Remitly offers competitive EUR/USD exchange rates without the markups embedded in bank wire spreads.

Conclusion

Portugal's NHR was Europe's most broadly accessible expat tax deal for fourteen years. Its replacement, IFICI, is a narrower, better-targeted tool that serves one specific group well — and leaves everyone else with essentially the same tax burden as any other Portuguese resident.

The shift isn't Portugal becoming a bad destination. It's Portugal changing what kind of expat it's trying to attract. High-earning professionals in the innovation economy, R&D workers, and tech company employees still get a compelling package. Retirees and lifestyle nomads no longer get a tax advantage for being there. Making the move now requires clarity about which group you're in — and the honest answer is that most people currently planning a Portugal relocation "for the tax benefits" are working from outdated information.

IFICI lasts ten years, is non-renewable, and requires annual upkeep of your qualifying status. Treat it as a temporary structure, not a permanent solution, and plan accordingly for what happens in year eleven.

Disclaimer: This article is for informational and educational purposes only and does not constitute tax, legal, or financial advice. Portuguese tax regulations are complex and subject to change. US citizens living abroad have separate US tax filing obligations regardless of their Portuguese residency status. Always consult a qualified Portuguese tax advisor and a US expat tax professional before making any residency or financial decisions.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceMay 26, 2026

Expat Tax & FinanceMay 26, 2026

Portugal IFICI: Is the NHR Replacement Worth It?

NHR ended in 2025. Portugal's IFICI replacement gives tech workers and researchers a 20% flat tax for 10 years — but retirees and passive investors.

Expat Tax & FinanceJuly 14, 2026

Expat Tax & FinanceJuly 14, 2026

Expat State Taxes: Which US States Won't Let You Go

Move abroad and California may still tax you 13.3%. Learn which five states chase expats, how domicile works, and how to sever state ties legally.

Expat Tax & FinanceJuly 4, 2026

Expat Tax & FinanceJuly 4, 2026

State Income Tax for Expats: Which States Follow You

California, New York, and Virginia keep taxing Americans abroad. Learn which states follow you, what triggers audits, and how to exit cleanly.