Over 20,000 Americans now live in Portugal. A huge chunk of them made the move specifically because of one thing: the Non-Habitual Residency (NHR) regime — a tax deal that let foreign retirees pay a flat 10% on pension income and many workers pay 0% on foreign earnings. It was one of the best expat tax structures in the developed world.

It ended on January 1, 2025.

What replaced it — IFICI (Incentivo Fiscal à Captação de Investimento) — is so different that calling it "NHR 2.0" is borderline misleading. Retirees are out. Remote workers who don't have a Portuguese employer are largely out. And those foreign pensions that used to get a 10% flat rate? They're now taxed at progressive rates that can hit 48%.

Here's everything US expats and prospective Portugal movers need to know before making a decision based on outdated tax information.

The NHR's 14-Year Run — and Why Portugal Pulled the Plug

Portugal launched the NHR in 2009 as an economic recovery tool post-financial crisis. The pitch was simple: spend 183+ days a year in Portugal, and for 10 years, your foreign-source income faces 0% Portuguese tax. Pensions from abroad got a flat 10% (raised from 0% after international pressure in 2020). Portuguese-source qualifying income was taxed at a flat 20%.

It worked spectacularly well. The number of Americans living in Portugal jumped 239% between 2017 and 2023. Lisbon and Porto became fixtures on every "best places for expat retirees" list. The Algarve coast became the unofficial US retirement community of Europe.

The backlash was predictable. Local housing prices in Lisbon surged over 60% between 2015 and 2023. Portuguese residents and politicians grew frustrated watching foreign retirees pay 10% on pensions while locals paid up to 48% on their income. In October 2023, the government announced the NHR would end for new applicants as of January 1, 2024, with a transition period through March 2025.

The new regime, IFICI, was designed with a completely different goal: not attracting wealthy retirees, but bringing skilled professionals and innovators who create economic value inside Portugal.

What IFICI Actually Is (Not What Most Articles Tell You)

IFICI stands for Incentivo Fiscal à Captação de Investimento — Tax Incentive for Investment Attraction. It is not a broad income-shelter program. It's a targeted incentive for qualified professionals working in specific sectors with Portuguese-registered employers.

The headline benefit is real: 20% flat tax on qualifying Portuguese-source income for 10 years, plus 0% on qualifying foreign-source income. On the surface that sounds similar to NHR. The devil lives in the eligibility requirements.

To qualify, you need all of the following:

- Not have been a tax resident in Portugal in the 5 years before applying

- Hold at least an EQF Level 6 qualification (a bachelor's degree plus 3 years of relevant professional experience, or a master's degree)

- Work in a qualifying sector — specifically: information technology, scientific R&D, manufacturing, healthcare, higher education, or green energy

- Be employed by or provide services to a Portuguese-registered entity that meets economic activity criteria

That last requirement is doing a lot of work. A fully remote worker employed by a US company and living in Lisbon almost certainly does not qualify. The regime requires genuine economic activity rooted in Portugal — not just physical presence.

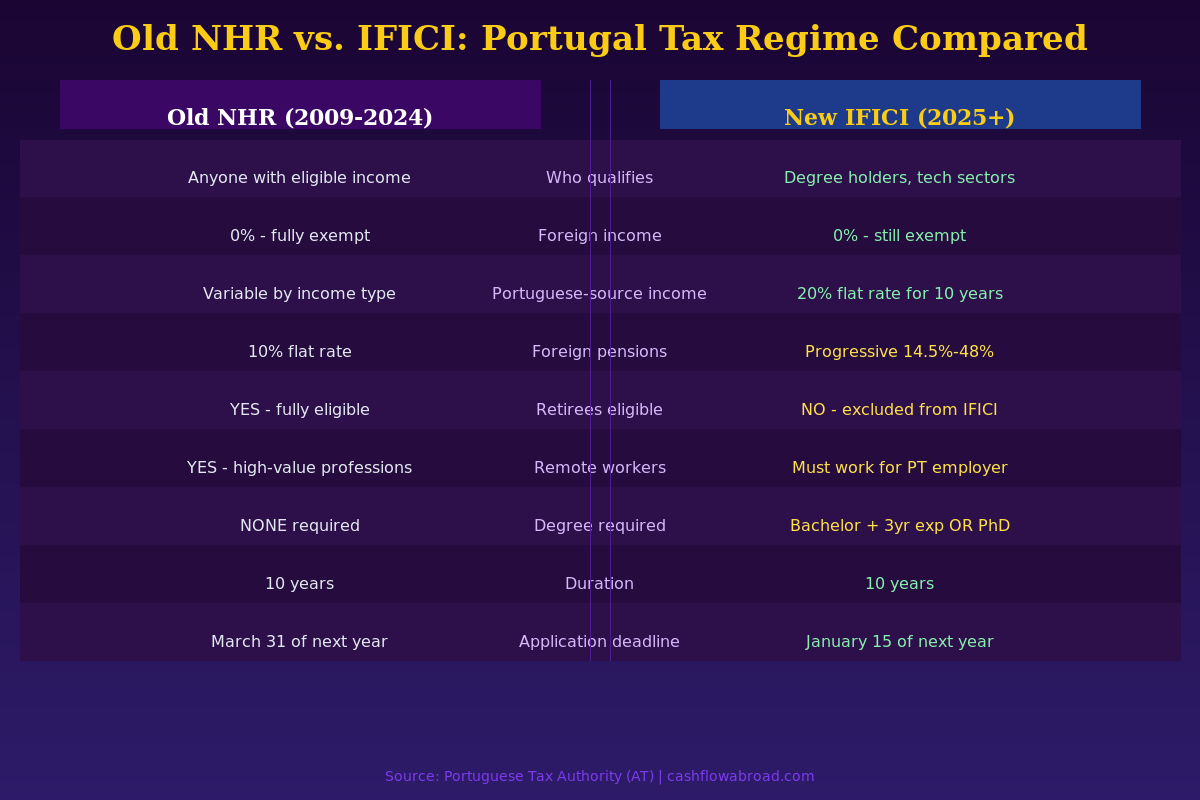

The Hard Numbers: IFICI vs. Old NHR

The numbers tell the story more bluntly than any summary:

| Category | Old NHR (2009–2024) | New IFICI (2025+) |

|---|---|---|

| Foreign income (non-blacklisted) | 0% — exempt | 0% — still exempt |

| Portuguese-source qualifying income | 20% flat rate | 20% flat rate |

| Foreign pension income | 10% flat rate | Progressive 14.5%–48% |

| Foreign dividends & capital gains | 0% (if treaty-eligible) | 0% (if non-blacklisted country) |

| Retirees eligible | Yes | No |

| Remote workers (US employer) | Often yes | Generally no |

| Degree requirement | None | EQF Level 6+ required |

| Duration | 10 years | 10 years |

| Application deadline | March 31 of following year | January 15 of following year |

The pension treatment is the biggest shock. Under NHR, a US retiree receiving $60,000/year in Social Security and pension income paid a flat 10% to Portugal — roughly €5,500. Under IFICI, that same income gets taxed at progressive Portuguese rates. The first €7,703 is taxed at 14.5%. Income between €7,703 and €11,623 hits 21%. Higher brackets climb to 35%, 43%, and 48%. For a $60,000 pension, the effective Portuguese tax rate could reach 25–35% — multiplying the tax bill by 2.5x to 3.5x compared to the old NHR flat rate.

Who Actually Qualifies for IFICI

Portugal's tax authority uses specific CAE (Classificação das Atividades Económicas) codes to define eligible employers. Not every tech job qualifies — the employer must be formally classified under information and communication (CAE 58–63), scientific R&D (CAE 72), manufacturing in high-tech sub-sectors, healthcare services, or higher education.

The clearest use cases:

- Software engineers hired by Portuguese tech companies — Portugal's tech sector has grown substantially, with companies like Farfetch, Sword Health, and numerous EU-funded R&D operations hiring internationally.

- Researchers at Portuguese universities or hospitals — Academic and clinical roles at institutions with formal R&D designations qualify.

- Founders relocating a startup to Portugal — If you can incorporate a qualifying Portuguese startup and draw salary through it, IFICI may apply. Several immigration lawyers specialize in structuring this compliantly.

- Healthcare professionals — Physicians, dentists, and specialists hired by Portuguese hospitals or clinics are specifically included.

Remote workers employed by US or UK companies with no Portuguese business presence are the group that lost the most. Under NHR, a US tech worker living in Lisbon and working remotely for a San Francisco employer could qualify as a "high-value added professional." IFICI closes that door almost completely.

The Pension Trap No One's Talking About

Portugal built its expat reputation significantly on the retiree market. The Algarve has neighborhoods where English is the dominant language at the local café. Many of those residents moved specifically under NHR's pension incentive. Those who applied for NHR before December 31, 2023 are grandfathered — their 10-year clock keeps running under the old rules. If your NHR started in 2020, you're protected through 2030.

The trap springs for anyone who:

- Was planning to move to Portugal in 2024 or later for retirement

- Has primarily pension or Social Security income (not employment income from a qualifying Portuguese employer)

- Was counting on the 10% pension rate as part of their retirement math

For a retiree with $80,000/year in US pension and Social Security income, the difference between 10% NHR tax and a 30% effective IFICI rate equals $16,000 per year in additional Portuguese tax — before any US tax obligations. Over a 10-year stay, that's $160,000 in extra taxes. Portugal is still affordable, but that gap changes the calculus completely.

For comparison, other geographic arbitrage destinations like Paraguay, Panama, and Georgia still offer straightforward 0% treatment on foreign-source income with no sector or degree requirements.

How IFICI Interacts with US Tax Obligations

American citizens never escape US tax obligations regardless of where they live. Portugal's IFICI creates specific planning complexity for US expats.

Foreign Earned Income Exclusion (FEIE): If you qualify for IFICI and earn employment income from a Portuguese employer, you can potentially claim the FEIE — which shelters up to $130,000 (2026 indexed amount) of earned income from US tax. But IFICI's 20% Portuguese flat rate is lower than most US marginal rates, meaning the Foreign Tax Credit won't fully offset US liability on income above the FEIE cap. You may end up paying both 20% to Portugal and the difference to the IRS on the excess. Our full breakdown of FEIE strategy for expats walks through the mechanics.

Social Security: The US-Portugal tax treaty does not shelter US Social Security from Portuguese tax under IFICI. Pensions including Social Security are taxed at progressive Portuguese rates. The treaty does prevent double taxation — Portuguese tax paid creates a Foreign Tax Credit on your US return.

FBAR and FATCA: Portuguese bank accounts trigger FBAR filing (FinCEN 114) any year you exceed $10,000 aggregate in foreign accounts. FATCA Form 8938 kicks in at $200,000 total foreign financial assets for single filers. Our complete expat banking and tax guide covers the full reporting stack.

Maintaining your US financial infrastructure matters more than ever when abroad. Charles Schwab International remains the gold standard for US expats — free ATM withdrawals worldwide, no foreign transaction fees, and a US brokerage account that stays open when you live abroad. Most US banks close accounts for non-residents; Schwab explicitly accommodates them.

You'll also need a valid US mailing address for the IRS and to maintain any US banking relationships. A Traveling Mailbox gives you a real US street address with mail scanning and check deposit for around $15/month — essential for keeping your US financial life intact while your physical address is in Lisbon. See our full virtual mailbox guide for expats for the setup process.

The Cost Arbitrage Still Works

IFICI's restrictions don't erase the fundamental math of living in Portugal versus the US. Overall costs are 34% lower than the US average.

| Expense | Lisbon Average (2026) | US Average (comparable city) |

|---|---|---|

| 1BR apartment (city center) | €1,200–€1,500/month | $2,500–$3,500/month |

| Monthly groceries (1 person) | €250–€350 | $450–$600 |

| Restaurant meal (mid-range) | €12–€18 | $25–$40 |

| Monthly transportation pass | €40 | $120–$180 |

| Private health insurance (healthy adult) | €100–€200/month | $400–$700/month |

| Total comfortable single lifestyle | €2,300–€2,500/month | $5,000–$7,000/month |

Restaurants are 38% cheaper than the US. Groceries are 39% cheaper. Even without a favorable tax regime, the purchasing power advantage of earning in US dollars while living in Portugal is significant. For people with substantial passive income who don't qualify for IFICI, the cost savings can offset a meaningful portion of the higher tax burden.

For health coverage while establishing access to the Portuguese national health system (the SNS), SafetyWing's Nomad Insurance provides international coverage starting at $56.28/month for adults under 40. For a comprehensive look at expat health coverage options, see our expat health insurance guide.

The Application Process and Timeline

If you qualify for IFICI, the application window is strict. You must file with the Portuguese Tax and Customs Authority (AT) by January 15th of the year following your first year of tax residency. Miss that date and you lose IFICI eligibility for that tax year — there are no extensions.

The steps:

- Get your NIF number — The Número de Identificação Fiscal is your Portuguese tax ID. Obtainable at any Finanças office or through a fiscal representative. You need this before everything else.

- Establish tax residency — Register your Portuguese address with AT and confirm 183+ days of physical presence (or your primary home) in Portugal during the qualifying year.

- Gather documentation — Degree certificate, proof of professional experience, employment contract with a qualifying Portuguese employer, and confirmation of the employer's qualifying CAE code.

- Submit IFICI application via Portal das Finanças — The online AT portal accepts applications from October through January 15. You'll enter your NIF, residency start date, qualifying activity type, and employer details.

- Receive confirmation — AT processes applications within 60–90 days. Approval is required before filing your first Portuguese IRS return under the IFICI rate.

The 5-year prior residency restriction catches people off guard. Any year you spent more than 183 days in Portugal, or declared Portuguese tax residency, in the 5 years before your application year disqualifies you. An extended Airbnb stay that inadvertently crossed the 183-day threshold can kill an otherwise clean IFICI application.

Portugal Without IFICI: Your Realistic Options

If you don't qualify for IFICI — you're a retiree, remote worker, or primarily passive income earner — Portugal is still open to you, just without the tax advantage.

D7 Passive Income Visa: Portugal's D7 visa targets people with passive income of at least €760/month (the minimum wage). You get a residency permit and path to permanent residency, but no special tax regime. You're taxed as a standard Portuguese resident at progressive rates.

Digital Nomad Visa (D8): Portugal launched a digital nomad visa in 2022 for remote workers earning at least four times the Portuguese minimum wage (approximately €3,040/month as of 2025). You get legal residency but standard tax treatment — IFICI does not apply to most D8 holders.

NHR grandfathered status: If you established NHR before December 31, 2023, your 10-year clock continues under original rules. These are currently the most advantaged expats in Portugal — particularly retirees in early NHR years with 6–8 years of 10% pension tax remaining.

For expats open to alternatives, territorial tax countries with no sector requirements offer straightforward 0% on foreign-source income with no degree constraints. Paraguay, Panama, and Georgia consistently top that list for simplicity and accessibility.

Should You Still Move to Portugal?

For the right profile, yes. The "right profile" is now much narrower.

IFICI works for you if: You have a bachelor's degree or higher, work in tech, science, healthcare, or R&D, and can either get hired by a qualifying Portuguese company or structure a Portuguese entity to employ you compliantly. The 20% flat rate offers real certainty for 10 years, and Portugal's infrastructure, EU residency access, and quality of life are genuine advantages.

IFICI doesn't work for you if: You're retired or semi-retired with pension and investment income as your primary source. You work remotely for a foreign employer with no Portuguese presence. Your income is primarily passive — dividends, capital gains, rental income. You were counting on the old NHR math to justify the move.

The most expensive mistake anyone can make right now is relocating to Portugal based on 2021–2022 "NHR tax haven" content. Run your actual scenario with a cross-border tax advisor who handles both US and Portuguese compliance. The difference between assuming NHR rates and facing real IFICI outcomes can be €15,000–€25,000/year for a retiree. Over a decade, that's a beach house in the Algarve.

Bottom Line

Portugal's NHR was exceptional while it lasted. IFICI is a legitimate, competitive benefit for a narrower audience — skilled professionals creating economic value inside Portugal, not passive income earners or location-independent remote workers. The 10% pension flat rate is gone. Retirees are out. Most remote workers employed by foreign companies are out.

If you're genuinely evaluating Portugal in the current environment, run your numbers under IFICI's actual rules, check whether a D7 or D8 visa with standard taxation still makes financial sense given Portugal's cost advantage, and factor in the full US compliance picture — FBAR, FATCA, FEIE interaction, and Social Security treaty treatment. Our expat investing playbook covers how your US brokerage and retirement accounts interact with foreign residency.

Portugal's charm, food, climate, and infrastructure haven't changed. The tax calculus has changed — a lot. Know which version of Portugal's tax story you're actually moving to before you sign a lease in Alfama.

Financial Disclaimer: This article is for informational purposes only and does not constitute tax, legal, or financial advice. US tax law and Portuguese tax regulations are complex and subject to change. The interaction between US citizenship-based taxation and Portuguese residency rules requires individualized professional analysis. Nothing in this article should be relied upon as a substitute for advice from a qualified cross-border tax professional with US and Portuguese expertise. Consult a licensed tax advisor before making any residency or tax planning decisions.