The 3.8% Tax Trap Catching US Expat Investors Off Guard

Most US expats obsess over two tax tools: the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC). The IRS casts a wide net here.

Most US expats obsess over two tax tools: the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC). The IRS casts a wide net here.

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

Most US expats obsess over two tax tools: the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC). They spend hours calculating which one saves more, file their 1040 correctly, and pat themselves on the back. What many don't realize is that a separate 3.8% tax — one that doesn't care about your FEIE election, doesn't respond to your foreign tax credits, and doesn't shrink just because you live in Portugal or Dubai — is quietly eating into their investment income.

The Net Investment Income Tax (NIIT) hit 7.3 million Americans in 2021, up from just 3.1 million in 2013. It generated $59.8 billion in tax revenue that year alone. The income thresholds that trigger it — $200,000 for single filers, $250,000 for married filing jointly — have not been adjusted for inflation since the tax was created over a decade ago. And for expats using the FEIE, there's a twist that makes this worse: your excluded foreign income gets added back into your MAGI for NIIT purposes.

What Is the Net Investment Income Tax?

The NIIT is an additional 3.8% tax on "net investment income" for US taxpayers whose Modified Adjusted Gross Income (MAGI) exceeds the statutory thresholds. It was created under the Affordable Care Act in 2013 and is calculated on IRS Form 8960.

The MAGI thresholds are:

| Filing Status | MAGI Threshold |

|---|---|

| Single / Head of Household | $200,000 |

| Married Filing Jointly | $250,000 |

| Married Filing Separately | $125,000 |

If your MAGI exceeds the threshold, you pay 3.8% on the lesser of: (a) your total net investment income, or (b) the amount your MAGI exceeds the threshold. Single filer, MAGI of $230,000, NII of $40,000 — you pay 3.8% on $30,000 = $1,140.

What Counts as Net Investment Income?

The IRS casts a wide net here. Net investment income includes dividends (qualified and non-qualified), interest income, capital gains (short and long term), rental income after allowable deductions, royalties, income from passive business activities, and gains from selling a passive interest in a partnership or S-corp.

What's not included: wages, self-employment income, Social Security, pensions, and distributions from IRAs or 401(k)s — though those distributions do raise MAGI, which can push other investment income over the threshold. For expats, the critical point is that foreign-sourced investment income counts identically to domestic income. Dividends from a Swiss brokerage, rental income from a Medellín apartment, capital gains from selling Australian shares — all of it feeds into the NII calculation.

The FEIE MAGI Trap: How Exclusions Work Against You

Here's where expats using the FEIE run into an obscure but expensive quirk in the tax code.

For regular income tax purposes, the FEIE allows you to exclude up to $126,500 (2024) of foreign earned income from taxable income. For NIIT purposes, however, MAGI is calculated differently. Under IRC Section 1411(c)(4), the excluded amount under Section 911 — the FEIE — is added back to your MAGI when determining whether you exceed the NIIT threshold. This single rule turns a tax benefit into a liability accelerator for expat investors.

Walk through a concrete example. You're a single US expat living in Germany. You earn $126,500 in salary — fully excluded under FEIE. You also have $60,000 in dividend and interest income. Your regular taxable income looks like zero. But for NIIT:

- Regular AGI: $60,000

- Add back FEIE exclusion: +$126,500

- NIIT MAGI: $186,500 — still under $200K, so no NIIT here

Now assume your salary is €140,000 (~$153,000) and your investment income is $80,000. The math changes:

- Regular AGI: ~$26,500 (salary over FEIE cap) + $80,000 NII = $106,500

- Add back FEIE exclusion: +$126,500

- NIIT MAGI: $233,000

- NIIT: min($80,000, $33,000) × 3.8% = $1,254 in extra tax

And it scales fast. An expat with $200,000 in capital gains from a property sale and a full FEIE exclusion could face a NIIT MAGI north of $350,000 — even if their regular income tax is near zero.

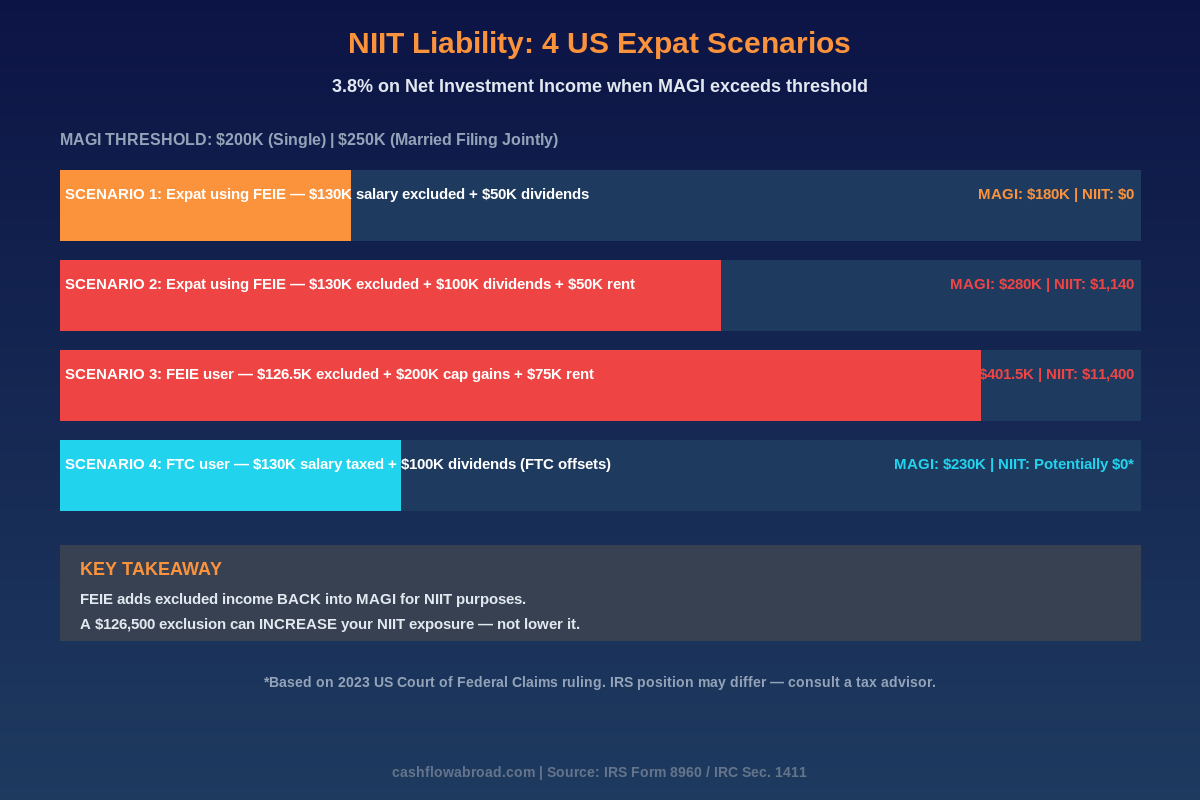

Four Expat Scenarios: Who Pays, Who Doesn't

| Scenario | Salary | Investment Income | FEIE Used? | NIIT MAGI | NIIT Owed |

|---|---|---|---|---|---|

| Low earner abroad | $80,000 | $40,000 dividends | Yes | $120,000 | $0 |

| Mid earner + moderate portfolio | $126,500 | $90,000 dividends | Yes | $216,500 | $635 |

| High earner + active rental portfolio | $126,500 | $150,000 (gains + rent) | Yes | $276,500 | $2,907 |

| FTC user in high-tax country | $150,000 | $80,000 dividends | No (FTC) | $230,000 | Potentially $0* |

*Based on the 2023 US Court of Federal Claims ruling. IRS position differs — consult a tax advisor before claiming this.

The 2023 Court Ruling That Changes the Math

In October 2023, the US Court of Federal Claims issued a significant ruling: foreign tax credits can be used to offset NIIT liability. This directly contradicts the IRS's longstanding position that NIIT is a separate chapter of the tax code (Chapter 2A) and therefore cannot be offset by FTCs, which only apply against Chapter 1 taxes.

If you're living in Germany, France, or Japan — where income tax rates run 40–50% — you likely have excess FTCs generating no benefit under normal Chapter 1 calculations. The 2023 ruling theoretically allows you to apply those excess credits against NIIT, potentially eliminating the 3.8% tax entirely.

The catch: the IRS has not formally accepted this ruling and has appealed. Claiming FTCs against NIIT is an aggressive position that invites scrutiny. If you want to pursue it, work with a qualified expat tax attorney who can properly document the position on your return. This is not a DIY move.

FEIE vs. FTC: Which Lowers Your NIIT Exposure?

The single biggest lever most expats can pull on NIIT is reconsidering whether FEIE is the right election at all. For expats with substantial investment income, FTC often wins — not just on regular income tax but on NIIT as well.

The FTC does not trigger the FEIE add-back rule. If you live in Germany and use FTC rather than FEIE, your foreign salary stays on your return as taxable income — but it's zeroed out by foreign tax credits. Your MAGI for NIIT purposes doesn't get artificially inflated by the Section 911 add-back.

The trade-off: if you live in a low-tax country (UAE, Paraguay, Panama), your foreign taxes may be minimal and FEIE is the better play. But in a high-tax country with unused excess FTCs, switching to FTC can eliminate thousands per year in NIIT. For a detailed breakdown of when each election wins, see the full analysis at FEIE vs. Foreign Tax Credit.

One important caveat: revoking the FEIE triggers a mandatory 5-year restriction period. Once you elect out, you cannot re-elect without IRS approval via Private Letter Ruling for five years. This makes switching a long-term decision. Run multi-year projections before acting.

6 Strategies to Cut Your NIIT Bill

1. Maximize tax-deferred accounts

Contributions to a traditional 401(k) or SEP-IRA reduce your MAGI dollar-for-dollar. A self-employed expat contributing $23,500 to a Solo 401(k) in 2025 drops MAGI by the same amount — potentially falling below the NIIT threshold entirely. SEP-IRA contributions can reach 25% of net self-employment income (up to $69,000 in 2024), which is a massive MAGI reduction for high earners.

2. Harvest capital losses before year-end

Capital losses directly offset capital gains in the NII calculation. If you're approaching year-end with gains that could push you over the NIIT threshold, selling losing positions reduces NII. Up to $3,000 in net losses can also offset ordinary income annually, with unlimited loss carryforward. This is standard portfolio tax management that many expats skip because their US financial advisor isn't coordinating with their overseas tax situation.

3. Time large capital events across years

Selling a rental property, exiting a business, or liquidating a large position creates one-year MAGI spikes. If you can spread a transaction across two tax years via installment sale, you may stay under the NIIT threshold both years. A $400,000 gain in one year at 3.8% NIIT costs $15,200. Split evenly across two years at $200,000 each, it costs nothing if MAGI stays below $200K in both years. The math alone can justify structuring deals as installment sales.

4. Consider real estate professional status

Rental income is passive by default, feeding directly into NII. However, a taxpayer who qualifies as a "real estate professional" under IRS rules — spending over 750 hours per year on real estate activities, and more time on real estate than any other profession — converts rental income to active. Active rental income exits the NII calculation entirely. This is a legitimate but high-scrutiny classification requiring meticulous hour logs and documentation. For expats with large rental portfolios, it's worth modeling.

5. Switch from FEIE to FTC in high-tax jurisdictions

Covered in detail above — the most impactful strategy for high earners in countries with tax rates above 30%. If you're paying 45% in Germany and have unused FTCs, switching to FTC keeps your MAGI lower for NIIT purposes and (per the 2023 ruling) may allow FTCs to offset NIIT directly. Run the numbers for your specific situation before acting.

6. Use a US-based expat-friendly brokerage

For expats holding investments in foreign accounts or foreign funds, NIIT still applies — but foreign mutual funds also trigger PFIC rules, creating a separate tax nightmare on top of the 3.8% charge. Keeping investments in a US-based account like Charles Schwab International — which actively accepts expat accounts and offers free worldwide ATM withdrawals — sidesteps PFIC issues and keeps your NII calculation clean. For a deep dive on PFIC traps, see The Expat Investor's Playbook.

What You Need to File

If you owe NIIT, you must attach Form 8960 to your Form 1040. The form walks through three sections: Part I lists all NII items, Part II calculates MAGI (Line 7 is the FEIE add-back — this is where most expats miss the adjustment), and Part III computes the actual tax owed.

Most DIY tax software doesn't handle the expat FEIE add-back correctly on Form 8960. If you have investment income over $50,000 and use the FEIE, have an expat tax preparer verify the NIIT calculation. Also watch quarterly estimated payments — the IRS requires payment as you earn, not just at filing. Failing to make adequate quarterly estimates triggers an underpayment penalty currently running at 8% annualized.

The Bottom Line

The NIIT is one of the most consistently underestimated taxes in the expat toolbox. It's small enough to miss on a single dividend check, but significant enough to cost a high-earning expat investor $5,000–$15,000 per year once capital gains and rental income accumulate. The FEIE — the same tool most expats use to zero out regular income tax — actively works against you by inflating MAGI for NIIT purposes. The 3.8% rate sounds manageable until you're writing a $12,000 check to the IRS for income you earned in another country.

Know your MAGI. Model the FEIE vs. FTC switch if you're in a high-tax country. Keep investments in US-regulated accounts to avoid stacking PFIC complications on top of NIIT. Use tax-deferred contributions aggressively to hold MAGI below thresholds. And if you have significant investment income, get a qualified expat tax advisor to review Form 8960 before you file.

For the full picture on how FEIE, FTC, and passive income interact, the US Expat Banking & Taxes guide and the FEIE zero-tax guide cover the foundations in detail.

Financial Disclaimer: This article is for educational purposes only and does not constitute tax or legal advice. US expat tax law is complex and highly fact-specific. The NIIT FTC ruling discussed is under IRS appeal — claiming FTCs against NIIT without professional guidance may result in penalties. Consult a qualified expat tax advisor before making any changes to your tax elections or investment strategy.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 29, 2026

Expat Tax & FinanceJuly 29, 2026

Form 4868 vs 2350 for Expats

Compare Form 4868 and Form 2350 for expats, choose the right extension, and protect cash flow before claiming Form 2555.

Expat Tax & FinanceJuly 28, 2026

Expat Tax & FinanceJuly 28, 2026

US Mortgage as an Expat: Document Checklist

Prepare the income, asset, credit, translation, and closing documents lenders ask for when expats apply for a U.S. mortgage.

Expat Tax & FinanceJuly 27, 2026

Expat Tax & FinanceJuly 27, 2026

EU VAT for US Ecommerce Sellers

Learn when U.S. ecommerce sellers need EU VAT, OSS, or IOSS, and fix checkout rules before taxes erase profit margins overseas.