Netherlands 30% Ruling: The Expat Tax Break Worth €14K/Year

The Netherlands charges up to 49.5% income tax on earnings above €76,817. What Exactly Is the Netherlands 30% Ruling? Who Qualifies for the 30% Ruling?

The Netherlands charges up to 49.5% income tax on earnings above €76,817. What Exactly Is the Netherlands 30% Ruling? Who Qualifies for the 30% Ruling?

Disclosure: this article contains affiliate links. If you open an account through one of them, Cashflow Abroad may earn a referral commission at no extra cost to you.

The Netherlands charges up to 49.5% income tax on earnings above €76,817. Yet tens of thousands of foreign workers there are legally paying an effective rate closer to 34% on the exact same salary. The mechanism is the 30% ruling — a Dutch tax break so powerful that multinationals explicitly use it as a recruitment tool to pull global talent to Amsterdam, Rotterdam, and The Hague. If you're considering a move to the Netherlands for work, this ruling isn't a footnote in your offer letter negotiation. On a €100,000 package, it's worth up to €14,850 per year in cash-equivalent tax savings.

The problem: most expats either don't know it exists, apply too late, or assume their employer is handling it when they're not. This guide covers what the ruling actually is, who qualifies, how to calculate your savings, and what's changing in 2027.

What Exactly Is the Netherlands 30% Ruling?

The 30% ruling (officially the 30%-facility or expat scheme) lets Dutch employers pay qualifying foreign employees up to 30% of their gross salary completely tax-free. The allowance compensates for "extraterritorial costs" — the real financial burden of relocating internationally: shipping belongings, finding housing, international school fees for children, airfare home, and the general premium of being a newcomer in an expensive country.

In practice, it means 30% of your total compensation package never hits your taxable income. Instead of paying 49.5% on your full earnings, you pay it on only 70% of what you earn. The benefit runs for a maximum of 5 years from your Dutch start date.

Who Qualifies for the 30% Ruling?

Eligibility is specific but achievable for anyone being genuinely hired from abroad into a Dutch employer relationship.

Core Requirements

- Employed by a Dutch company or Dutch branch of a foreign company — the ruling requires an actual employer-employee relationship, not freelance or self-employed work

- Recruited from outside the Netherlands: you must have lived at least 150km from the Dutch border for at least 16 of the 24 months immediately before your first working day in the Netherlands

- Specific expertise: you must have skills considered scarce on the Dutch labor market — in practice, this bar is loose and rarely a blocker for professional and technical roles

- Meet the minimum salary threshold for 2026

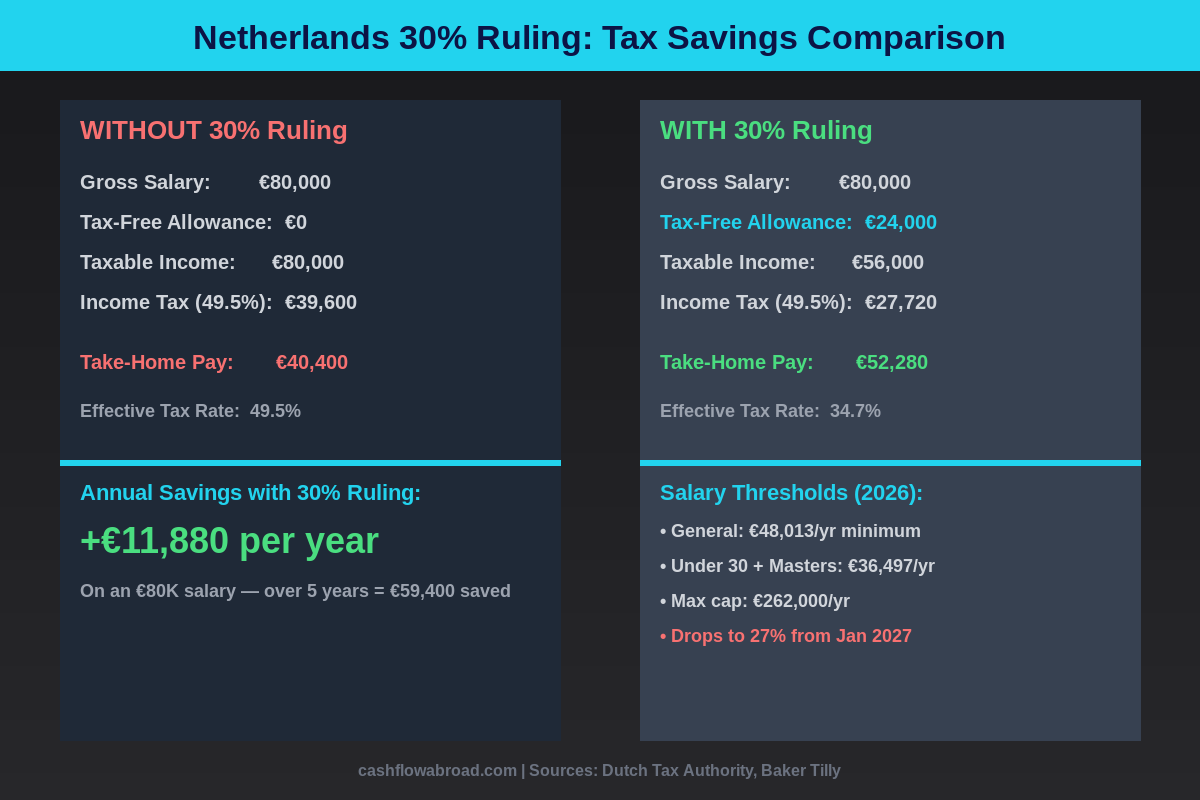

2026 Salary Thresholds

| Category | Minimum Gross Salary (Excl. Allowance) |

|---|---|

| General (all employees) | €48,013/year |

| Under 30 with qualifying Master's degree | €36,497/year |

| Maximum salary cap (benefit ceiling) | €262,000/year |

The cap means the 30% benefit is calculated on a maximum of €262,000 in 2026 — so the absolute maximum tax-free allowance you can receive this year is €78,600. At a 49.5% marginal rate, that's a theoretical saving of up to €38,907 in a single tax year for very high earners.

For context on managing your US financial life while working in the Netherlands, see our US expat banking and taxes guide.

How Much Can You Actually Save?

The math across four realistic salary levels, using the 49.5% marginal rate applied to the tax-free allowance (your actual saving may vary based on your full income profile and deductions):

| Total Package | 30% Tax-Free Allowance | Taxable Portion | Est. Annual Tax Saving | 5-Year Total Savings |

|---|---|---|---|---|

| €60,000 | €18,000 | €42,000 | ~€8,910 | ~€44,550 |

| €80,000 | €24,000 | €56,000 | ~€11,880 | ~€59,400 |

| €100,000 | €30,000 | €70,000 | ~€14,850 | ~€74,250 |

| €150,000 | €45,000 | €105,000 | ~€22,275 | ~€111,375 |

Over a 5-year Dutch assignment, a senior professional earning €100,000/year saves over €74,000 compared to a colleague without the ruling. That's not theoretical — it hits your paycheck every month. Dutch companies competing for international talent increasingly structure offers to include the ruling as standard, not optional.

A concrete example from the Dutch Tax Authority: an employee with a base salary of €54,000 receives a tax-free allowance of €23,142 (calculated as 30/70 × €54,000), reducing their taxable income accordingly. The effective rate drops from 49.5% toward the mid-30% range.

How to Apply — and When

The application is filed by your employer, not by you personally. Your Dutch company submits a joint request to the Belastingdienst (Dutch Tax Authority). You provide the supporting documentation; your HR or payroll department handles the filing itself.

The 4-Month Window

If approved, the ruling applies from your first day of work in the Netherlands — but only if your employer submits within 4 months of your start date. Miss that window, and the ruling starts from the month after the late application is submitted. Every month of delay is real money lost, not recoverable retroactively.

Late applications are common at smaller companies unfamiliar with the process, or at larger ones where HR moves slowly on new hires. Don't assume it's happening — confirm with your employer's payroll team in your first week.

What You'll Need to Provide

- Proof of foreign residence outside the Netherlands covering the 24 months before your start date: foreign utility bills, rental contracts, bank statements, or tax returns

- Evidence that your previous address was 150km+ from the Dutch border — the Belastingdienst cross-references addresses against geographic databases

- Your employment contract showing salary meets the 2026 threshold

- Degree certificate, if applying under the under-30 / Master's reduced threshold

Typical processing time: 4–8 weeks. Complex cases or incomplete documentation can add months. Apply immediately — don't wait for your first paycheck to raise the topic.

2026 Status and the 2027 Reduction

The 30% ruling has been politically turbulent. Critics — particularly in the Dutch Labour Party — call it a subsidy for already high-earning foreigners in a country with housing shortages and pressure on public services. Supporters, led by multinational employers and the tech sector, counter that international talent recruitment depends on it.

The Dutch parliament in 2024 originally passed a plan to phase the ruling down to a 30/20/10 tiered structure over three years — which would have effectively decimated the benefit. After intense lobbying from companies in Amsterdam's Zuidas financial district, the chip manufacturers in Eindhoven (notably ASML), and the broader international business community, the government reversed course.

2026: Full 30% Intact

- The full 30% tax-free allowance remains for 2026 — no tiered phasedown

- The income cap of €262,000 applies to all employees; the transitional regime ended December 31, 2025

- Partial foreign tax liability (partiële buitenlandse belastingplicht) is no longer available for ruling holders since January 1, 2025 — meaning foreign savings, investments, and real estate are now included in Dutch Box 3 (wealth tax) calculations during your Dutch residency

2027: Drops to 27%

From January 1, 2027, the maximum tax-free allowance drops from 30% to 27% for employees hired from 2024 onward who still have time remaining on their 5-year window. Employees who had the ruling before January 1, 2024, retain their original 30% terms through their 5-year period.

On a €100,000 package, the shift from 30% to 27% costs roughly €1,485/year in additional tax — a real hit, but far smaller than the original 30/20/10 plan. There is ongoing parliamentary discussion about potentially reversing even this 27% reduction, but nothing has been legislated as of early 2026. Plan for 27% from 2027 and treat any reversal as upside.

What the 30% Ruling Does NOT Cover

Self-employed workers are excluded. The ruling requires a genuine employer-employee relationship. ZZP (sole proprietor) contractors and workers operating through their own BV without a real employment contract don't qualify.

Social security contributions are not reduced. Dutch social security premiums (covering state pension, unemployment insurance, and disability) are calculated on full taxable income. The 30% exclusion doesn't touch these.

The 150km rule is strictly enforced. Brussels is 185km from Amsterdam — just barely qualifying. London is 350km. Paris is 430km. But Antwerp (95km), Liège (150km on the nose, so borderline), and Cologne (195km) are checked carefully. People who briefly relocated to a qualifying location right before taking a Dutch job have been denied.

Employment gaps affect eligibility. If you previously worked in the Netherlands and left, returning to work for a new Dutch employer generally does not restart the clock — unless the gap between your previous Dutch employment and your new start date was more than 8 years.

US Expats in the Netherlands: The Double-Filing Layer

American citizens working in the Netherlands face an obligation that non-US workers don't: the US taxes worldwide income regardless of where you live. The 30% ruling reduces your Dutch tax burden but does nothing about your IRS filing obligations.

The practical options for US citizens in the Netherlands:

Foreign Tax Credit (FTC) — usually the better choice. File Form 1116 to claim a dollar-for-dollar credit against US taxes for Dutch tax paid on the same income. Since Dutch rates (even with the 30% ruling at play) are often still higher than US rates at comparable income levels, the FTC can generate credits large enough to offset your entire US liability — sometimes with carryforward excess credits.

Foreign Earned Income Exclusion (FEIE). The FEIE lets you exclude up to $132,900 (2026) of foreign earned income from US taxes. But for Netherlands-based Americans, the FTC usually outperforms the FEIE because Dutch taxes paid are high enough to cover most or all of your US liability without sacrificing the tax base that the FTC would otherwise shield.

The US-Netherlands income tax treaty is generally workable — it includes tie-breaker rules for dual residency, pension provisions, and dividend withholding reductions. It's not as generous as the US-France or US-Germany treaties, but it's functional.

Maintaining Your US Financial Footprint

American expats in the Netherlands need to maintain a real US mailing address for IRS correspondence, state tax filings, US bank statements, and account verification. Traveling Mailbox provides a real US street address in 50+ cities — incoming mail is scanned and accessible online, checks can be deposited remotely — starting at $15/month. It's an essential piece of infrastructure for keeping US financial accounts active and your IRS address current. See the full virtual mailbox setup guide.

For US banking that doesn't penalize you for an overseas IP address or foreign address, Charles Schwab International is the standard recommendation: no foreign transaction fees, unlimited ATM rebates worldwide, and no tendency to close accounts when you move abroad.

Banking Setup in the Netherlands

Opening a Dutch bank account requires your BSN number (citizen service number), which you get after registering at your local municipality (gemeente). The timeline: arrive → register at gemeente → receive BSN → open bank account. For most expats, this process takes 2–4 weeks from arrival.

The most expat-friendly Dutch banks:

| Bank | Monthly Fee | English App | Can Open Pre-Arrival |

|---|---|---|---|

| Bunq | €3–10/month | Yes | Yes (limited) |

| ING | €3.95/month | Partial | No |

| ABN AMRO | €4.75/month | Partial | No |

| N26 (German fintech) | €0–9.90/month | Yes | Yes |

Bunq is the first choice for expats who want full English and pre-arrival access. N26 works as a bridge until you have a BSN. For sending money internationally, Remitly offers competitive USD/EUR rates with transparent fees.

Health Insurance: Mandatory Within 4 Months

Once you register as a Dutch resident, you're legally required to purchase Dutch zorgverzekering (basic health insurance) within 4 months of registration. The basic premium runs €120–170/month in 2026, with a mandatory deductible (eigen risico) of €385/year. Supplemental coverage (dental, physio, optician) adds €20–60/month depending on the plan.

Dutch healthcare ranks consistently in Europe's top 5 — GP access is solid, hospital care is high-quality, and the system is genuinely functional. The insurance is purchased from private insurers (Zilveren Kruis, VGZ, CZ are the major ones) but heavily regulated by the government.

For international coverage during the gap between arrival and sorting your Dutch plan — or for travel outside the Netherlands — SafetyWing provides solid bridge coverage. The expat health insurance guide covers international options in detail.

Cost of Living: What the Netherlands Actually Costs

The 30% ruling exists partly because the Netherlands — especially Amsterdam — is genuinely expensive by global standards. Here's realistic monthly budgeting across major cities:

| Expense | Amsterdam | Rotterdam / The Hague | Eindhoven / Other |

|---|---|---|---|

| 1-bedroom apartment rent | €1,800–€2,600 | €1,300–€1,900 | €900–€1,400 |

| Monthly transit pass | €100–€140 | €90–€120 | €70–€100 |

| Groceries (1 person) | €300–€450 | €280–€400 | €250–€380 |

| Dutch health insurance | €130–€170 | €130–€170 | €120–€160 |

| Dining out per meal | €15–€30 | €12–€25 | €10–€20 |

| Realistic monthly total | €2,800–€4,200 | €2,200–€3,400 | €1,700–€2,800 |

Amsterdam's housing market is historically tight — vacancy rates near zero and fierce competition for any decent rental. Many expats choose Rotterdam (30 minutes by train) or The Hague for meaningfully lower rent while maintaining easy access to Amsterdam-based employment. Eindhoven has become a serious tech hub in its own right; ASML, the dominant global maker of chip-making equipment, is headquartered there and actively uses the 30% ruling to recruit globally.

Other Dutch Expat Tax Benefits the Ruling Unlocks

The 30% ruling is the headline, but it traditionally unlocked secondary benefits — some of which have recently been curtailed:

International school reimbursement. Dutch international schools cost €15,000–30,000/year per child. Under certain structures, employers can pay these fees as part of the extraterritorial cost package, potentially tax-free alongside or in addition to the 30% allowance. Ask your employer's HR directly — this varies by company policy.

Home leave flights. Employer reimbursement of return flights to your home country may be structured as extraterritorial cost compensation — tax-free in certain arrangements.

Partial foreign tax status — removed. Until 2024, ruling holders could elect partial foreign tax liability, exempting foreign savings and investments from Dutch Box 3 (wealth) tax. This was removed from January 1, 2025. Foreign accounts, investment portfolios, and real estate now fall into Box 3 calculations during Dutch residency. For Americans with large brokerage accounts, this is a meaningful change that affects tax planning.

Is the Netherlands Worth It Compared to Lower-Tax Destinations?

With the 30% ruling, a Netherlands-based professional on €100,000 pays income tax on €70,000. Dutch income tax on €70,000 runs roughly €25,000–27,000 (the Netherlands has a two-bracket system: 36.97% up to €76,817, 49.5% above). Effective rate on total package: roughly 25–27%. That's surprisingly competitive with "low-tax" expat destinations once you factor in that Dutch salaries are significantly higher than comparable roles in Southeast Asia or Eastern Europe.

If you're weighing a Dutch employment offer against remote work under another country's tax regime, the comparison isn't just tax rates — it's total compensation package, career trajectory, and lifestyle. Our geographic arbitrage playbook breaks down how the math compares across 10 countries with real salary benchmarks.

The Netherlands also sits in the center of Europe — a practical benefit for anyone who wants to travel extensively while maintaining stable employment and a functioning social safety net. The infrastructure, English fluency (the Netherlands is #1 globally in English proficiency among non-native speakers), and quality of life make it a compelling package for professionals willing to engage seriously with the tax optimization.

Bottom Line

The Netherlands 30% ruling is one of the most generous legitimate tax breaks available to skilled workers in any developed country. On a €100,000 package, it's worth €14,850 annually — over five years, that's over €74,000 in cumulative tax savings. The 2027 reduction from 30% to 27% shaves some of that benefit, but the ruling remains powerful relative to paying full Dutch rates.

Apply within your employer's first four months. Keep clean records of your pre-Netherlands address. If you're American, layer in the Foreign Tax Credit — and don't forget a virtual US mailbox to maintain your financial infrastructure stateside. Combine those pieces correctly and the Netherlands' punishing headline tax rate becomes something you're paying at a steep discount.

This post is for informational purposes only and does not constitute tax, legal, or financial advice. Dutch tax law and 30% ruling eligibility rules can change. Consult a qualified tax advisor with expertise in Dutch and international tax law before making decisions based on this information. US citizens should additionally consult an advisor familiar with US expat tax obligations, FBAR, and FATCA requirements.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Related guides

Expat Tax & FinanceJuly 29, 2026

Expat Tax & FinanceJuly 29, 2026

Form 4868 vs 2350 for Expats

Compare Form 4868 and Form 2350 for expats, choose the right extension, and protect cash flow before claiming Form 2555.

Expat Tax & FinanceJuly 28, 2026

Expat Tax & FinanceJuly 28, 2026

US Mortgage as an Expat: Document Checklist

Prepare the income, asset, credit, translation, and closing documents lenders ask for when expats apply for a U.S. mortgage.

Expat Tax & FinanceJuly 27, 2026

Expat Tax & FinanceJuly 27, 2026

EU VAT for US Ecommerce Sellers

Learn when U.S. ecommerce sellers need EU VAT, OSS, or IOSS, and fix checkout rules before taxes erase profit margins overseas.