More than 700,000 Americans collect Social Security checks from outside the United States. Almost none of them can use Medicare to pay for a single doctor's visit. These are two entirely separate programs with two entirely different rules — and the gap between them has cost returning expats thousands of dollars in permanent premium surcharges they never saw coming.

Medicare Part B costs $202.90 per month in 2026. That's $2,434.80 per year for coverage that is, in almost every scenario, worthless the moment you board a plane to Lisbon or Medellín. The question of whether to keep paying, drop it, or pause it is one of the most consequential financial decisions a US expat over 65 can make — and the penalties for getting it wrong are permanent.

What Medicare Actually Covers Outside the US

The short answer: almost nothing. Medicare is a domestic program. Original Medicare (Parts A and B) does not cover medical services rendered outside the 50 states, Washington D.C., Puerto Rico, the US Virgin Islands, Guam, American Samoa, or the Northern Mariana Islands.

The narrow exceptions are almost never applicable to actual expat life:

- Canadian border emergencies: If you're a US citizen traveling through Canada to or from Alaska, Medicare may cover emergency care at a Canadian hospital if the US hospital is unreasonably far away.

- Mexican border emergencies: Similar rule applies if you're closer to a Mexican hospital than a US one.

- Cruise ships: Coverage applies when the ship is within 6 hours of a US port.

None of these apply if you're retired in Costa Rica, working remotely from Spain, or wintering in Thailand. If you're hospitalized in any of those places, Medicare pays zero — and you're paying out of pocket or through a separate international policy.

Medicare Advantage (Part C) plans occasionally market limited international benefits, but read the fine print: most emergency-only benefits cap at $50,000–$100,000 lifetime, exclude pre-existing conditions for foreign care, and require reimbursement rather than direct billing. For anyone living abroad full-time, it's not a substitute for real international coverage.

Three Parts, Three Different Decisions

Medicare is not one program — it's three, each with different rules for expats.

Part A: The Trap You Can't Escape

Part A covers inpatient hospital care, skilled nursing facilities, and hospice. For most Americans — anyone with 40 quarters (10 years) of Social Security-taxed wages — Part A is free. And therein lies the problem.

If you have premium-free Part A, you cannot voluntarily disenroll without simultaneously forfeiting all Social Security retirement or disability benefits and repaying every dollar Medicare has ever paid on your behalf. The Social Security Administration enforces this under 42 U.S.C. §1395q. The SSA's position: Medicare entitlement is tied to Social Security eligibility, and you can't separate them.

In practice, this means virtually every expat keeps Part A regardless of where they live. It costs nothing to hold, and surrendering it would mean giving up Social Security income — which is portable abroad — to escape a zero-cost insurance policy that doesn't work outside the US anyway. Not a trade worth making.

Part B: The $202.90 Decision

Part B covers outpatient care, doctor visits, and preventive services. Unlike Part A, it has a monthly premium — $202.90 in 2026, up from $174.70 just two years ago. It also carries a $257 annual deductible and 20% coinsurance for covered services.

This is where expats face a real financial decision: keep paying $2,434.80 annually for coverage that won't be used, or drop it and risk a permanent penalty if you return to the US. Getting this wrong either direction costs serious money.

Part D: Drug Coverage and Its Own Penalty

Part D covers prescription drugs. The national base premium is $38.99/month in 2026. Many expats abroad access the same medications at a fraction of US costs — a month's supply of a common blood pressure medication that runs $200 in the US costs under $15 in Mexico or Colombia. But the penalty for skipping coverage has teeth.

Going 63+ consecutive days without creditable drug coverage triggers a permanent Part D late enrollment penalty: 1% of the national base premium per month without coverage, for life. At $38.99/month, that's roughly $0.39 of extra premium per uncovered month — small individually, but permanent and compounding.

The Penalty That Follows You Home Forever

Here's where most expats get blindsided. The Medicare Part B late enrollment penalty is not a one-time fee. It is a permanent, lifetime surcharge added to your monthly premium — and it compounds with every 12-month period you spent without coverage.

The formula: 10% of the standard Part B premium per 12-month period without Part B, applied for as long as you have Medicare. There is no cap. There is no phase-out.

Run the math on a 5-year expat stint:

- You drop Part B at 65, live abroad for 5 years, return at 70.

- Penalty: 50% permanent surcharge.

- 2026 standard premium: $202.90. Your premium: $304.35/month for life.

- Extra cost over 20 years of retirement: roughly $24,348 extra versus someone who kept it.

| Years Without Part B | Penalty | Monthly Premium (2026 rates) | Extra Cost Over 20 Years |

|---|---|---|---|

| 1 year | +10% | $223.19/mo | +$4,869 |

| 3 years | +30% | $263.77/mo | +$14,602 |

| 5 years | +50% | $304.35/mo | +$24,336 |

| 10 years | +100% | $405.80/mo | +$48,672 |

| 15 years | +150% | $507.25/mo | +$73,008 |

Ten years abroad with no Part B means you're paying $405.80/month — double the standard rate — for the rest of your life. The math only gets worse from there.

The Exception That Changes Everything

Here's the critical good news that often gets buried in the Medicare-abroad coverage: documented foreign residency qualifies you for a Special Enrollment Period (SEP).

If you can prove you lived outside the US while not enrolled in Part B, you can re-enroll when you return — without paying the late penalty. The key word is prove. Acceptable documentation includes:

- Foreign income tax returns

- Signed foreign lease agreements or property ownership records

- Foreign utility bills in your name

- Employer letters confirming a foreign work location

- Foreign bank statements with a foreign address

The expat SEP gives you 2 months after returning to the US to enroll, with no late penalty. This fundamentally changes the calculus. If you keep meticulous records of your foreign residency — which you should be doing for your IRS filings and FBAR requirements anyway — dropping Part B is a legitimate strategy.

The catch: "I just didn't need it" is not a qualifying reason. Documented foreign residency is the only basis. Someone who stayed in the US but skipped Part B gets no mercy. Keep your lease, utility bills, foreign bank statements, and tax receipts organized in a dedicated folder, updated every year you're abroad.

A virtual US mailbox helps here in a specific way: it gives you a real US street address for SSA correspondence and financial institutions, while your documented foreign address stays clean for residency purposes. The SSA needs somewhere to send enrollment notices and Medicare cards — a professional mail service handles that without muddying your residency proof. At $15/month, it's cheap insurance for a five-figure decision.

IRMAA: The Surcharge That Hits High-Earning Expats Hardest

The $202.90 standard premium assumes your modified adjusted gross income (MAGI) was under $106,000 single or $212,000 married in 2024 — because Medicare uses a 2-year income lookback. Earn above those thresholds and you owe an Income-Related Monthly Adjustment Amount (IRMAA) surcharge on top of the standard premium.

| 2024 MAGI (Single Filer) | 2026 Part B Monthly Premium | Annual Cost |

|---|---|---|

| ≤$106,000 | $202.90 | $2,435 |

| $106,001 – $133,000 | $284.10 | $3,409 |

| $133,001 – $167,000 | $365.30 | $4,384 |

| $167,001 – $200,000 | $446.50 | $5,358 |

| $200,001 – $500,000 | $527.70 | $6,332 |

| Above $500,000 | $608.90 | $7,307 |

The trap for expats: foreign earned income excluded via the FEIE is still counted in your MAGI for IRMAA purposes. If you used the FEIE to exclude $130,000 from your regular income tax, that $130,000 gets added back in when Medicare calculates your surcharge bracket. High-earning digital nomads sometimes discover they're paying $400–$600/month for Part B they cannot use — in a country they don't live in.

If your income drops significantly when you move abroad (say, from $200K to $80K), you can file Form SSA-44 to request an IRMAA reduction based on a qualifying life-changing event. Retirement or a significant reduction in work hours qualifies. Moving abroad alone does not, but the associated income reduction often does.

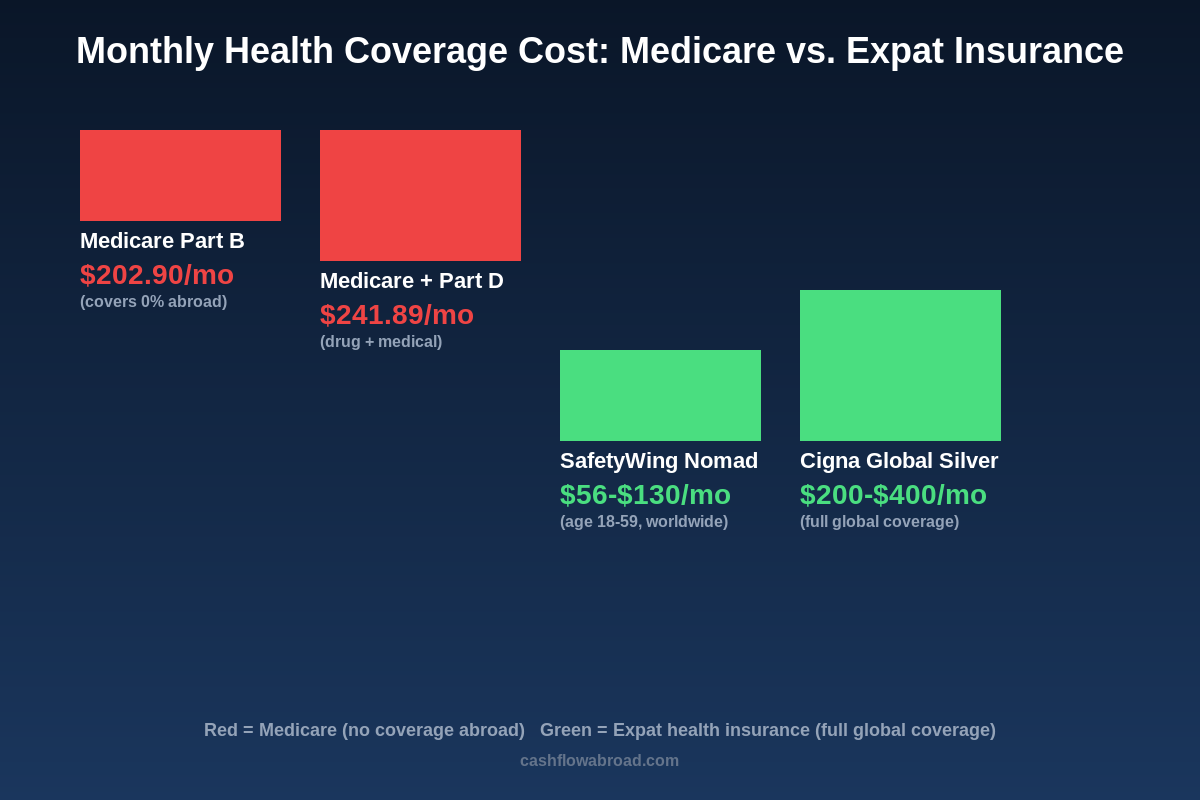

What Expat Health Insurance Actually Costs

If you drop Part B and qualify for the expat SEP when you return, you need real coverage to replace it. The international health insurance market has matured significantly, and the options are genuinely competitive — especially compared to what you'd spend on equivalent US care.

SafetyWing is the entry point. Their Nomad Insurance (Essential) runs $56–$130/month depending on age — $56 for ages 18–39, roughly $80 for 40–49, $130 for 50–59 — with a $250 deductible and coverage in 185 countries. Their Complete plan adds more comprehensive benefits starting around $161.50/month for younger adults. The key limitation: it doesn't include coverage while physically in the US (though it covers brief US visits up to 30 days), so if you plan significant time stateside, you'd want additional coverage or to maintain Part B.

For comprehensive global coverage including the US, Cigna Global and GeoBlue Xplorer are the standard picks. Cigna Silver runs roughly $200–$400/month for a 60-year-old depending on deductible selection. GeoBlue Xplorer, which routes through Blue Cross Blue Shield for US care, starts around $412/month but offers direct billing at US hospitals — no reimbursement paperwork. Both cover mental health, preventive care, and specialists globally.

Compare that to what Medicare Part B actually delivers abroad — zero — and the math simplifies. You're either paying $202.90/month for nothing, or paying a similar amount for real global coverage. The question is purely about the return-to-US calculus and whether your documentation supports the SEP.

For the full international health insurance breakdown, see our complete expat health insurance guide.

The Decision Framework

There's no universal answer. Here's how to think through it cleanly:

Keep Part B If:

- You spend 4+ months per year in the US — Part B becomes genuinely useful

- You have chronic conditions that may pull you back to US specialists regularly

- Your IRMAA bracket is low and $202.90/month feels manageable for peace of mind

- You're abroad for under 2–3 years and unsettled about your timeline

- You cannot reliably document foreign residency to support an SEP claim later

Drop Part B If:

- You're committed to 3+ years abroad and will document residency meticulously each year

- Your IRMAA bracket has you paying $300–$600/month for coverage you can't use

- You have solid international health coverage in place

- A US expat tax professional or Medicare counselor has confirmed your SEP eligibility and documentation plan

The Documentation Play

If you drop Part B, the single most important thing is building an airtight foreign residency file. Every year abroad, collect and store:

- Signed lease or property deed in your name

- Utility bills (electric, internet, water) in your name

- Foreign bank statements showing local transactions

- Foreign tax receipts or returns where applicable

- Any official foreign government correspondence

Keep these in a dedicated folder — digital and physical copies both. When you return to the US and visit your local Social Security office to re-enroll, this documentation is what eliminates the penalty. The SSA processes expat SEP claims regularly; it's written into the program rules, not an obscure workaround. But you have to prove it, and gaps in your documentation record hurt your case.

One More Thing: Medigap Doesn't Fix This

Medigap (Medicare Supplement Insurance) is private coverage designed to fill Medicare's domestic gaps — the 20% coinsurance, deductibles, and out-of-pocket maximums. Plans C and F include a foreign emergency care benefit: 80% coverage after a $250 deductible, up to a $50,000 lifetime maximum.

The expat trap: that benefit applies only to emergencies, only during travel (not residence), and hits a $50,000 lifetime cap that a single serious hospitalization abroad can exhaust. It was designed for the American tourist who breaks an ankle in Paris, not for the retiree living in Oaxaca year-round. Medigap is supplemental to Medicare — and Medicare itself covers nothing abroad. You'd still need a real international health policy.

Social Security vs. Medicare: Not the Same Program

This distinction is worth belaboring because the conflation causes real planning mistakes. Social Security retirement benefits are fully portable. The SSA deposits checks to bank accounts in most countries, or you can access funds via a US account and international debit card. Over 700,000 Americans receive Social Security payments from abroad.

Medicare doesn't work that way. It is a US domestic program. You can receive a Social Security check in Bali and not be able to use your Medicare card for anything there. The two programs share enrollment infrastructure but have entirely different geographic scope.

For expat retirees optimizing both, the common playbook looks like this: keep free Part A (no reason not to — surrendering it means forfeiting Social Security), drop Part B with documented foreign residency and a solid international health plan, collect Social Security from abroad, and re-enroll in Part B when returning using the expat SEP. It works cleanly when executed with proper documentation and a clear residency file.

If you're working out the broader retirement math, see how Social Security stretches further abroad — and our complete FBAR, FATCA, and FEIE guide for the banking and tax filing obligations that go alongside active US accounts while overseas.

The Bottom Line

Medicare is one of the most misunderstood pieces of the US expat financial puzzle. The program costs $202.90 to $608.90 per month in 2026 depending on your income — for coverage that is functionally useless outside the US. The decision to keep it or drop it hinges on a single variable: whether you can document your foreign residency well enough to claim a penalty-free Special Enrollment Period when you return.

If you can — and most organized expats can — dropping Part B saves thousands per year with no lasting downside. If you can't prove residency, or you're abroad for under 2–3 years, the permanent 10% annual surcharge makes keeping Part B the safer call. Either way, understanding the actual rules rather than assuming Medicare travels with your passport is worth real money over the course of a retirement.

Financial disclaimer: This post is for informational purposes only and does not constitute tax, legal, or financial advice. Medicare rules, IRMAA brackets, and premium amounts change annually. Consult a qualified financial advisor, certified Medicare counselor (SHIP), or expat tax professional before making any enrollment decisions. Individual circumstances — including years of Social Security contributions, existing enrollment status, and documentation of foreign residency — significantly affect which strategies apply to you.