You spent 30 years paying into Medicare. The payroll tax came out every single check. And then you moved to Portugal, Colombia, or Thailand — and discovered that Medicare won't cover a single doctor's visit there. Not one euro. Not one baht. And if you tried to stop paying the Part B premium to save money? You just bought yourself a permanent surcharge that compounds every year you stay abroad.

This is the Medicare trap. It catches tens of thousands of American retirees abroad every year, and most don't find out until they're already locked in. Here's exactly how it works — and how to navigate it without getting burned.

What Medicare Actually Covers Abroad (Spoiler: Almost Nothing)

Medicare is a domestic program. By statute, it does not pay for healthcare received outside the United States. The exceptions are so narrow they're almost not worth mentioning:

- A Canadian or Mexican hospital that's closer to your US location than the nearest US hospital during a US-border emergency

- A ship within US territorial waters (6 nautical miles of the coast)

- Certain dialysis situations at sea

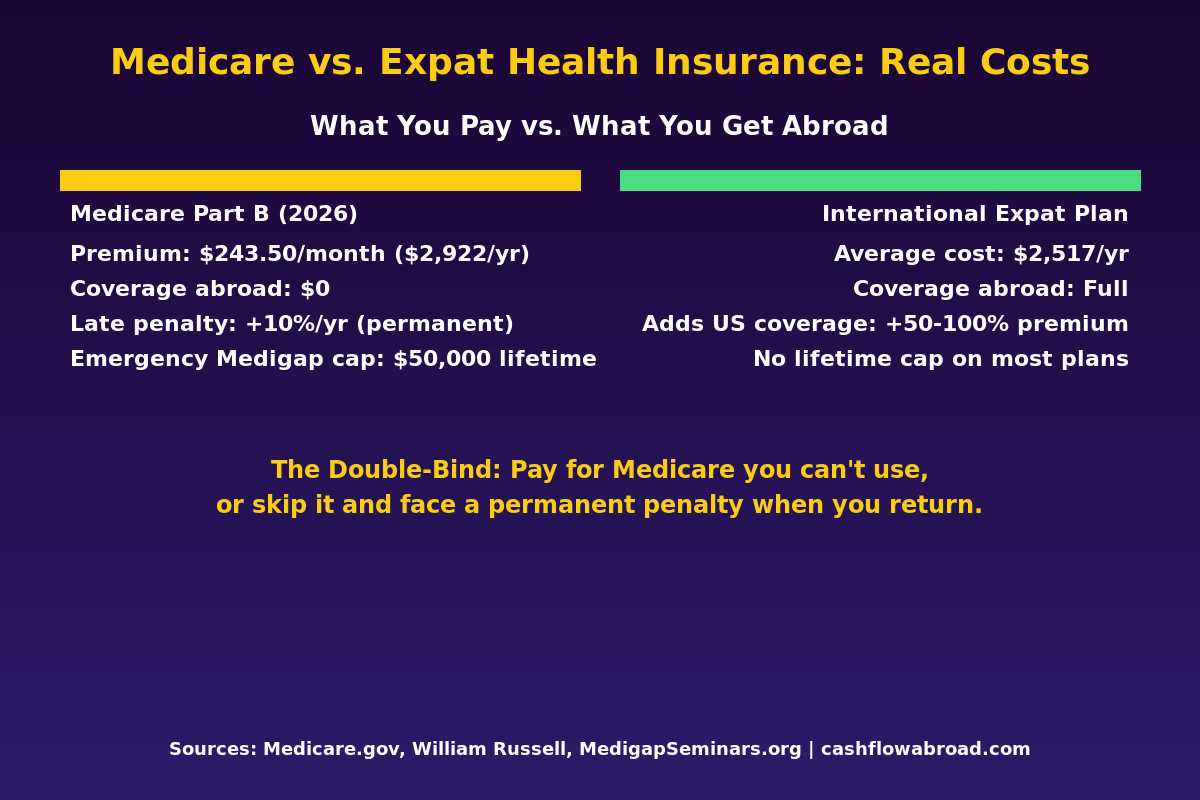

That's it. If you retire to Medellín and need heart surgery, Medicare pays $0. If you break your hip in Bangkok, Medicare pays $0. If you develop a chronic condition in Madrid and need ongoing specialist care, Medicare pays $0.

The 2026 Part B premium is $243.50/month — $2,922 per year — for coverage you literally cannot use where you live. Most retirees abroad also pay Part A premiums if they have fewer than 40 quarters of work credits, though the majority of Americans hit that threshold through their working years. Add Part D (drug coverage) and a Medigap supplement and you're looking at $400–$700/month for a plan that covers you nowhere outside the US.

The Penalty That Compounds for Life

Here's where it gets punishing. If you delay enrolling in Medicare Part B past your Initial Enrollment Period (a 7-month window around your 65th birthday), you owe a 10% premium surcharge for every 12-month period you were eligible but didn't enroll. That surcharge is permanent.

Live abroad for five years without enrolling in Part B? You come home at 70 to a 50% permanent surcharge on top of whatever the standard premium is that year. A 3-year delay means +30% forever. A decade abroad without enrollment doubles your Part B premium — for the rest of your life.

| Years of Delayed Enrollment | Permanent Premium Surcharge | Annual Extra Cost (2026 rates) |

|---|---|---|

| 1 year | +10% | +$292/year |

| 3 years | +30% | +$876/year |

| 5 years | +50% | +$1,461/year |

| 10 years | +100% | +$2,922/year |

The only escape from this penalty: you must have had qualifying "creditable coverage" during the delay period — typically employer-sponsored health insurance. If you retire abroad on your own savings with no employer health plan, the penalty clock starts ticking the month after your Initial Enrollment Period closes.

The 8-Month Window That Can Save You Thousands

There is one legitimate off-ramp from the penalty. If you return to the US and stop being covered by employer-sponsored insurance, you qualify for a Special Enrollment Period (SEP) of 8 months. During that window, you can enroll in Part B without penalty — regardless of how long you've been abroad.

The critical detail: the SEP starts the month after your employer coverage ends (or the month after you stop working, whichever is earlier). It does not start the day you land back in the US. Miss the 8-month window and you're stuck waiting for the next General Enrollment Period (January–March), with coverage that won't start until July — plus that penalty permanently attached.

For retirees abroad on private insurance or local country health coverage — not employer-sponsored plans — this SEP typically does not apply. You need to plan your enrollment around your actual situation, not what you assume qualifies.

The Medigap Foreign Travel Loophole (And Its Limits)

Some Medigap supplemental plans — specifically Plans C, D, F, G, M, and N — include emergency foreign travel coverage. On the surface, this sounds like a solution. In practice, it's a small bandage on a large wound.

The terms: $50,000 lifetime maximum, a $250 deductible, 80% coinsurance after that, and coverage limited to the first 60 days of each international trip. That means if you live abroad full-time, you might qualify only for brief trips — and even then, only for sudden, unforeseen emergencies, not the chronic care most retirees actually need.

A $50,000 lifetime limit evaporates fast with a serious medical event. A cardiac bypass in the US runs $80,000–$150,000. Even with foreign hospitals where care costs a fraction of US prices — Thailand's Bumrungrad hospital charges roughly $15,000–$25,000 for the same procedure — a single major event can exhaust your Medigap foreign limit in one hospitalization.

Your Three Real Options as a Retired Expat

There's no perfect answer. Every choice has a trade-off, and the right move depends on how long you plan to stay abroad, your age, your health, and your intentions around returning to the US.

Option 1: Enroll in Medicare and Pay the Premium Anyway

Many expats choose to enroll at 65 and eat the $243.50/month cost — even knowing they'll get zero benefit abroad. Why? Optionality. If you return to the US for any period, you have coverage immediately. If you develop a condition that makes you want to access the US healthcare system, you're not locked out. And you avoid the compounding penalty entirely.

This makes the most sense if you're in your mid-60s, your assets make $2,922/year relatively manageable, and you maintain close ties to the US. Think of Part B enrollment not as healthcare, but as keeping your US options open.

Option 2: Skip Part B and Accept the Eventual Penalty

Some long-term expats do the math and decide the penalty is worth accepting. If you're 65 and won't return until 80, you've saved 15 years of premiums. At 2026 rates: 15 × $2,922 = $43,830 saved. Even with a 100%+ permanent surcharge when you return, the break-even point might be 10–15 years of post-return Medicare enrollment. If you don't expect to live that far past your return date, the math might favor skipping.

This route only makes sense with solid expat health coverage throughout your time abroad. See the complete expat health insurance guide for providers that fill this gap properly.

Option 3: The Hybrid Approach

Enroll in Part A at 65 (it's premium-free for most Americans with 40+ work quarters). Delay Part B strategically if you have employer coverage — or accept enrollment if you don't. Supplement with an international health plan that covers your day-to-day care abroad.

SafetyWing's Nomad Insurance costs as little as $40–$100/month depending on age and coverage area, and fills the gap while your Medicare sits dormant. Pair this with local country insurance in your destination — national health systems in many expat-popular countries offer voluntary enrollment to legal residents at surprisingly low cost.

What Expat Health Insurance Actually Costs

The alternative to relying on Medicare abroad isn't a void — it's a robust international health insurance market that often delivers better value per dollar than US domestic coverage.

| Region | Annual Expat Plan Cost | Typical Coverage | US Coverage Add-On |

|---|---|---|---|

| Southeast Asia (Thailand, Vietnam) | $2,000–$4,000/year | Full inpatient + outpatient | +50–100% premium |

| Latin America (Mexico, Colombia) | $2,500–$5,000/year | Full inpatient + outpatient | +50–100% premium |

| Western Europe (Spain, Portugal) | $3,500–$7,000/year | Full inpatient + outpatient | +50–100% premium |

| Average (William Russell, 2026) | $2,517/year | Full international coverage | Varies by insurer |

Most international plans exclude US coverage by default — the US is the most expensive country in the world for healthcare, and premiums reflect that. A plan that covers you in Colombia and Thailand might cost $2,500/year. Add US coverage and you're often looking at $5,000–$7,000/year. For many retirees, the math points toward: international plan (low-cost, full coverage abroad) + Medicare Part A enrollment (for US hospitalization optionality) as the most flexible combination.

Maintaining a US Address for Medicare Enrollment

Medicare requires a US mailing address. You cannot maintain Part A or Part B benefits without one — and a PO Box doesn't cut it for most enrollment forms. If you're living abroad full-time, maintaining a legitimate US street address is a structural requirement, not a nice-to-have.

The solution most long-term expats use: a virtual mailbox service that provides a real US street address in a state of your choosing. Traveling Mailbox ($15/month) gives you a real street address in 50+ US cities, scans and uploads your mail, and handles check deposits — keeping your Medicare correspondence, IRS filings, and US banking all tied to a legitimate address.

State selection matters: Florida, Texas, and Nevada have no income tax and Florida has no estate tax — popular choices for expats who want to minimize their US tax footprint while maintaining legal domicile status. The US expat banking and taxes guide covers the state domicile decision in full.

Don't Forget Part D: The Drug Coverage Penalty

The same penalty logic applies to Medicare Part D (prescription drug coverage). A 1% surcharge per month of uncovered delay — paid every month for as long as you have Part D. Skip Part D for 5 years (60 months), and you owe a permanent 60% surcharge on your Part D premium.

Part D base premiums are lower ($36–$50/month nationally in 2025), so the dollar impact is smaller than Part B. But for retirees abroad in countries where prescription medications cost a fraction of US prices — $5 for a month of blood pressure medication in Colombia vs. $40+ in the US — the math often doesn't justify enrollment. As with Part B: know the rules before you opt out.

How to Make the Medicare Decision as an Expat

Cut through the noise with this framework:

- Enroll in Part A at 65 — It's free for most Americans. There's no reason to skip it.

- If you have employer coverage — Delay Part B without penalty while coverage is active. Track your SEP window carefully when it ends.

- If you're retiring abroad with no employer coverage — Decide at 65: enroll and pay ($2,922/year for optionality) or skip and accept the penalty math. There is no neutral choice.

- Build international health coverage independently — Don't assume Medicare will protect you abroad. It won't.

- Set a calendar reminder for your SEP window — If you ever return to the US and lose employer coverage, you have exactly 8 months to enroll in Part B without penalty. Miss it once and the surcharge is permanent.

For expats managing assets and investments across borders while navigating this, the expat investing playbook covers how to structure your portfolio without triggering PFIC rules or losing tax efficiency on your retirement accounts.

The Bottom Line

Medicare is built for people who live in the United States. If you don't, it becomes one of the most expensive non-coverages in personal finance: pay for something you can't use, or get penalized permanently for not paying. There's no middle ground.

The framework is simpler than the bureaucracy makes it seem. Enroll Part A. Make a deliberate, calculated decision about Part B at 65. Never let an enrollment deadline slip by accident. And build your actual healthcare strategy around an international plan that works where you actually live.

The retirees who get hurt aren't the ones who made the wrong choice — they're the ones who didn't know there was a choice to make.

Financial Disclaimer: This article is for informational and educational purposes only. It does not constitute legal, tax, medical, or financial advice. Medicare rules are complex and subject to change; consult a licensed Medicare advisor or financial planner with expat experience before making enrollment decisions. International health insurance products vary significantly by provider, country of residence, age, and health status. Premiums and regulations cited reflect available 2025–2026 data and may change.