Medicare Abroad: Your US Coverage Stops at the Border

Medicare pays $0 for virtually all care outside the US. Here is what expat retirees actually need — and how much it costs — before the penalty trap catches them.

Medicare covers $0 for most care outside the US. Learn the Part B penalty trap and the best international health insurance options for expat retirees.

Here's a number that should be on every retirement planning checklist but rarely is: Medicare pays exactly $0 for care received outside the United States in the vast majority of situations. Not reduced. Not reimbursed after paperwork. Zero.

The Social Security Administration sends retirement checks to beneficiaries in more than 160 countries. Hundreds of thousands of Americans receive those checks while living abroad. A significant share of them are also paying the $202.90 monthly Part B premium — and receiving absolutely nothing in healthcare coverage for it.

If you're planning to retire abroad, or already have, this gap isn't a minor administrative detail. It's a fundamental restructuring of how you need to think about healthcare risk. A single hospitalization in Germany running €40,000 will not be touched by Medicare. Surgery at a Thai private hospital — $15,000, entirely out of pocket. A cardiac event in Spain: the bill lands completely on you.

The good news: international healthcare for expat retirees is dramatically cheaper than US healthcare, and the coverage options have matured substantially. The bad news: most retirees discover the Medicare gap only after they've already moved.

What Medicare Actually Covers Abroad

Let's be precise about the three narrow situations where Medicare does pay for foreign care:

- Canadian border emergencies: If you're in a US border state and the nearest hospital is in Canada, Medicare may cover inpatient hospital, ambulance, and dialysis costs.

- Alaskan transit: Traveling between Alaska and another US state via the most direct Canadian route — genuine emergency, Canadian hospital closer than any US facility — Medicare applies.

- Cruise ships within 6 hours of a US port: Medically necessary care in international waters is covered only if the ship is within six hours' sailing time of a US port when care is provided.

That's it. If you have a stroke in Lisbon, a hip replacement in Medellín, or cancer treatment in Chiang Mai, Medicare Parts A and B cover none of it. Medicare Advantage (Part C) plans have the same limitation — they operate within US provider networks and cannot export that coverage globally.

Medigap Doesn't Save You Either — Mostly

Medicare Supplement (Medigap) plans have a limited foreign travel benefit that trips people up because it sounds better than it is. Plans C, D, F, G, M, and N provide emergency coverage abroad, but with a structure built for vacationers, not expats:

- 80% of "Medicare-eligible" emergency expenses after a $250 annual deductible

- Applies only during the first 60 days of a trip

- $50,000 lifetime maximum

- Covers only what Medicare would deem eligible — excluding most routine and non-emergency care

If you're residing abroad full-time, the 60-day trip limit renders this benefit meaningless. The $50,000 lifetime cap disappears fast against a serious oncology case or major cardiac intervention. Medigap's foreign travel benefit was designed for Americans who take two-week cruises, not Americans who live in Alicante.

The Part B Penalty Trap

Here's where the financial stakes get genuinely serious for anyone considering a permanent or long-term move abroad.

If you don't enroll in Medicare Part B when you first become eligible (generally at age 65) and later want to enroll, you face a 10% permanent premium increase for each 12-month period you were eligible but not enrolled. This penalty never goes away.

Someone who retired to Portugal at 65, skipped Part B for 10 years, then moved back to the US at 75 due to a health crisis faces this math:

- Base 2026 Part B premium: $202.90/month

- Penalty: 100% (10 years × 10%/year)

- Total monthly premium: $405.80/month, permanently

- At IRMAA thresholds ($106,000+ income for individuals), this climbs further still

The decision to skip Part B is a bet that you'll never return to the US healthcare system. That bet fails regularly — health events, family emergencies, and changing life circumstances bring people back. Most financial planners now recommend: pay the $202.90/month Part B premium even while abroad, keep Part A (free for those with 40+ quarters of Medicare taxes paid), and layer international health insurance on top. You preserve your Medicare intact while covering yourself globally.

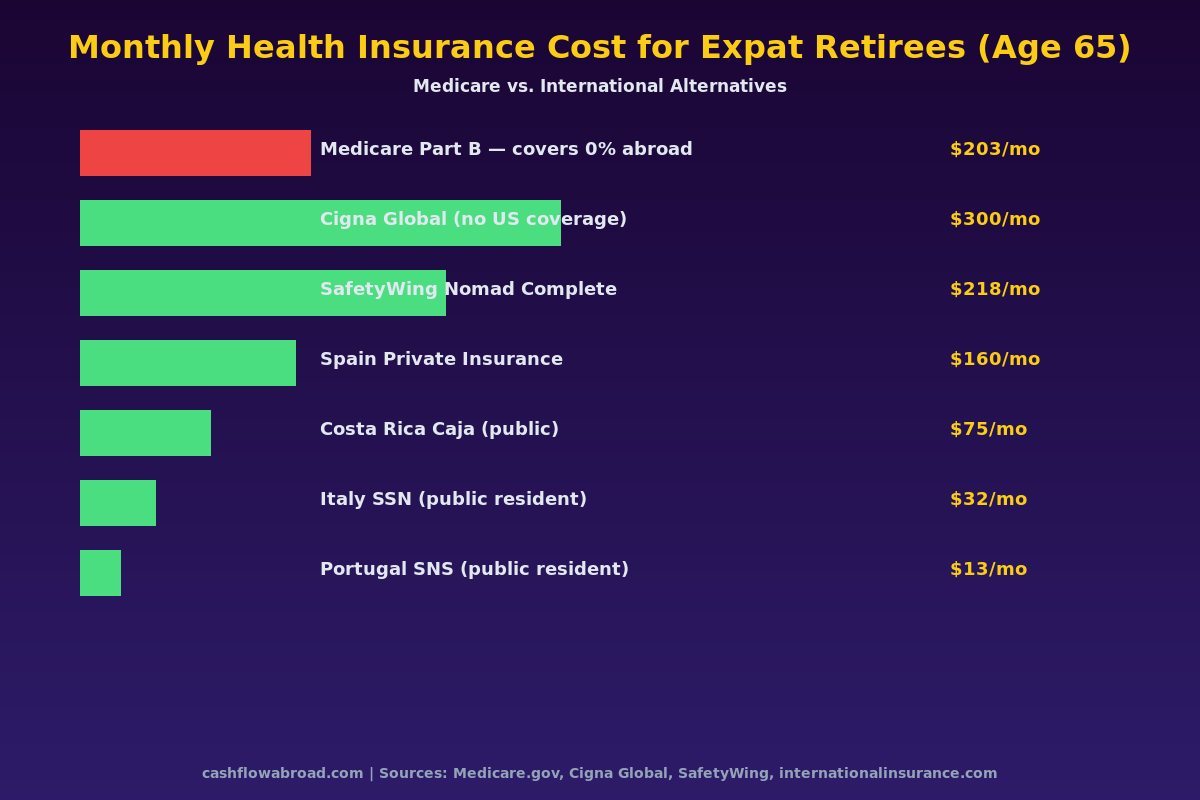

What International Coverage Actually Costs

The chart above illustrates monthly cost for a 65-year-old across major coverage options. A few things stand out immediately:

International health insurance excluding US coverage is substantially cheaper than US-inclusive plans. Adding US coverage to a Cigna Global policy roughly doubles the premium. If you're committed to living abroad and won't use US healthcare for routine care, the non-US option runs $250–$400/month for a 65-year-old versus $700–$1,200+ for a comprehensive US-inclusive plan.

Public healthcare in EU residency countries changes the math dramatically. Italy's SSN costs permanent residents approximately €388/year — under $35/month — for coverage comparable to most private plans. Portugal's SNS is available to legal residents for roughly €13–25/month. Spain's national system is accessible to residents with a social security contribution history, often supplemented by private top-up plans at €100–180/month.

SafetyWing Nomad Complete runs approximately $218/month for ages 60–64. It covers 175+ countries, includes emergency evacuation, and handles routine care — well-positioned for peripatetic retirees who aren't permanently settled anywhere yet. Note: coverage isn't renewable past age 69 without case-by-case negotiation, so it's a bridge plan rather than a long-term solution.

The 5 Real Coverage Options for Expat Retirees

Option 1: International Private Health Insurance

The gold standard for expats who want comprehensive global coverage with predictable claims processes:

| Provider | Est. Monthly Cost (Age 65, no US) | Network | Notable |

|---|---|---|---|

| Cigna Global | $280–$420 | 180+ countries | Strong hospital network, fast claims |

| Allianz Care | $200–$380 | 160+ countries | Dental/vision add-ons available |

| GeoBlue Xplorer | $250–$450 (US incl.) | Worldwide | BlueCross network access in US |

| AXA Global Health | $220–$400 | 180+ countries | Strong mental health coverage |

Critical caveat: pre-existing conditions are typically excluded or come with waiting periods. Apply before leaving the US, while you're in good health. A diagnosis on file can permanently exclude that condition from coverage or make premiums prohibitively expensive.

Option 2: SafetyWing Nomad Complete

SafetyWing provides real health coverage — not just travel emergency coverage — in 175+ countries. At $218/month for ages 60–64, it undercuts traditional international insurers while offering meaningful routine care benefits. Use it as a bridge for the first years abroad while you settle into a country with public healthcare access, or as ongoing coverage if you're moving frequently across destinations.

Option 3: Local Public Healthcare Enrollment

For retirees genuinely settling in one country with legal residency, local public healthcare often wins on cost by a wide margin:

| Country | System | Monthly Cost (Resident) | Access Condition |

|---|---|---|---|

| Italy | SSN (Servizio Sanitario Nazionale) | ~$32 | Registered resident + annual fee |

| Portugal | SNS (Serviço Nacional de Saúde) | ~$13–25 | Legal resident registration |

| Costa Rica | CCSS (Caja Costarricense) | ~$50–100 | Legal residency, income-based |

| Colombia | EPS Contributive Regime | ~$50–80 | Legal visa + income declaration |

| Mexico | IMSS Voluntary | ~$33 (≈$400/year) | Voluntary enrollment, wait periods apply |

Trade-off: wait times and specialist access. Routine care in Italy and Portugal is excellent; elective specialist appointments can take weeks. Many EU-based expats use a hybrid approach — public registration plus a private top-up policy for faster specialist access, typically adding €50–80/month.

Option 4: Local Private Insurance in Your Destination

Often overlooked: local private insurance in your retirement country is frequently 40–60% cheaper than internationally-issued policies covering the same territory. A comprehensive private policy in Spain for a 65-year-old runs approximately €100–180/month. In Mexico, private hospital plans start around $80–120/month. In Thailand, full-coverage policies from Bupa Thailand or Pacific Cross average $120–200/month for ages 60–65.

The downside: these policies don't travel. Leave Spain for three months and you're uninsured. They also require local banking and often local-language navigation for claims. If you're a permanent settler, this is a cost-effective option. If you're peripatetic, it's not the right tool.

Option 5: Keep Medicare, Layer International on Top

For retirees who spend 90+ days/year in the US or might return permanently if health deteriorates, keeping Medicare active while adding an international policy is the most robust — and most expensive — approach:

- Part A: $0 (free for 40+ quarters of Medicare taxes)

- Part B: $202.90/month

- Medigap Plan G (US use): ~$120–180/month

- International policy excluding US coverage: $280–350/month

- Total: ~$600–730/month — but you have comprehensive coverage on both sides of the border

What Care Actually Costs in Expat Retirement Destinations

One factor that reshapes the entire analysis: the underlying cost of healthcare in most expat retirement destinations is a fraction of US costs. Even without insurance, out-of-pocket care is often manageable:

| Procedure | US (avg. with insurance) | Spain | Thailand | Colombia | Mexico |

|---|---|---|---|---|---|

| Hip replacement | $15,000–40,000 | €5,000–12,000 | $8,000–14,000 | $4,000–8,000 | $5,000–12,000 |

| Cardiac stent | $20,000–50,000 | €8,000–18,000 | $7,000–15,000 | $5,000–10,000 | $6,000–14,000 |

| Specialist visit | $250–600 | €50–100 | $30–60 | $15–40 | $30–80 |

| MRI scan | $700–2,500 | €150–350 | $120–250 | $80–200 | $100–300 |

This cost differential means a well-funded retiree in Colombia or Thailand might spend less annually on healthcare — including a major procedure — than they would navigating US Medicare copays, deductibles, and supplemental premiums. This doesn't mean going uninsured is sensible (catastrophic coverage is non-negotiable), but it recalibrates the risk calculation entirely.

The US Infrastructure You Still Need Abroad

While Medicare enrollment is one thing to manage remotely, maintaining the underlying US financial infrastructure is equally important. Medicare Part B premiums are deducted directly from Social Security payments — that's handled automatically. But you still need a US mailing address for Medicare correspondence, Medigap policy documentation, and any billing disputes.

A virtual mailbox service like Traveling Mailbox ($15/month) gives you a real US street address in 50+ cities, scans incoming mail, and handles check deposits. It solves the address problem for Medicare, IRS correspondence, and banking simultaneously — essential infrastructure that most expats underestimate until they miss a critical notice.

For banking, Charles Schwab International remains the strongest expat banking account: no foreign transaction fees, free global ATM withdrawals refunded monthly, and no minimum balance. It keeps your US financial identity intact without penalizing you for living abroad. The full picture of how to structure your finances as a US expat retiree is covered in the expat banking and taxes guide.

When Your Health Fails Abroad: The Return Decision

The scenario most retirement planners underweight: a serious diagnosis arrives abroad, and the instinct is to return to the US for treatment at a major academic medical center.

If you maintained Medicare and Medigap, returning is straightforward. If you dropped Part B, you now face:

- No Special Enrollment Period triggers — "living abroad without coverage" doesn't qualify as a coverage loss event

- A General Enrollment Period (January–March each year) with coverage starting July 1 — meaning months without coverage during an active health crisis

- The permanent 10% per year late enrollment penalty on every Part B premium for life

Expats most vulnerable here are those who left with a firm "I'm never coming back" mindset, dropped Medicare entirely to save $203/month, and face a serious diagnosis at 72. The $203/month saved over 7 years ($17,052) doesn't approach covering the lifetime premium penalty — let alone the coverage gap during enrollment delays while managing an active diagnosis.

For how retirement income, Social Security, and foreign pensions interact — and how to structure your income to minimize Medicare IRMAA surcharges — see the retirement abroad income planning guide.

Your Pre-Move Healthcare Checklist

- Decide on Part B. Default to keeping it unless you're definitively never returning and can absorb the return penalty risk. The $203/month buys optionality.

- Apply for international health insurance before leaving the US. Your current health status is your best underwriting position. Apply while healthy.

- Research your destination country's residency healthcare access. EU countries offer some of the most cost-effective healthcare in the world for legal residents. Factor the residency pathway into your destination selection.

- Establish a US virtual mailbox. Medicare correspondence, insurance renewals, and IRS notices all need a physical US address.

- Model the total monthly healthcare cost. Part B + Medigap + international top-up is $600–730/month. Local public system + private top-up might be $150–250/month. Both are valid; they serve different circumstances.

- Revisit coverage annually. International insurance premiums increase with age. What works at 65 may need restructuring at 70.

For a comprehensive look at the digital nomad and expat visa landscape — which directly affects your healthcare eligibility in each country — the digital nomad visa guide breaks down access requirements by country.

The Bottom Line

Medicare is a benefit that took decades of payroll taxes to earn. It's also one that stops working the moment you cross the US border with any consistency. For the hundreds of thousands of Americans collecting Social Security checks across 160+ countries, the gap between what Medicare promises and what it delivers internationally is a financial risk that demands a deliberate response — not an afterthought discovered at the first ER visit abroad.

The silver lining is real: international health insurance for retirees is genuinely affordable, often dramatically so compared to equivalent US coverage. A 65-year-old can have comprehensive global coverage for $250–$400/month — frequently less than a US Medicare Advantage plan with meaningful out-of-pocket exposure. In countries with accessible public healthcare, the monthly cost drops under $100.

The cost of not planning is where it gets expensive.

Financial disclaimer: This article is for informational purposes only and does not constitute financial, tax, insurance, or legal advice. Healthcare costs, insurance premiums, Medicare rules, and foreign public healthcare eligibility requirements are subject to change. Consult a qualified financial planner, insurance specialist, or licensed advisor familiar with expat situations before making coverage decisions. Affiliate links may appear in this post — we may receive compensation for referrals at no additional cost to you.

This guide is general information, not personalized tax, legal, or investment advice. Rules change; verify current thresholds with official sources or a qualified professional before acting.

Next step

Turn healthcare risk into a retirement checklist

Medicare is only one layer. Retirees also need local coverage, evacuation, emergency cash, banking access, and tax documentation.

Related guides

Expat Health & InsuranceMay 18, 2026

Expat Health & InsuranceMay 18, 2026

The Expat HSA Guide: Triple Tax-Free Medical Savings Abroad

How US expats can use their HSA for tax-free medical expenses worldwide, who can still contribute abroad, and how FEIE interacts with HSA deductions.

Expat Health & InsuranceMarch 31, 2026

Expat Health & InsuranceMarch 31, 2026

Expat Health Insurance: How I Pay $120/Month for Better Coverage

Complete expat health insurance guide comparing costs across 7 countries. How to get better coverage for $120/month vs $450-1,500 in the US.

Expat Health & InsuranceJune 27, 2026

Expat Health & InsuranceJune 27, 2026

Dental Care Abroad: Costs, Coverage, and Where to Go

Root canals for $350, implants for $1,100. Compare dental costs in Mexico, Thailand, Hungary and Colombia — plus what your expat insurance covers.